Key Insights

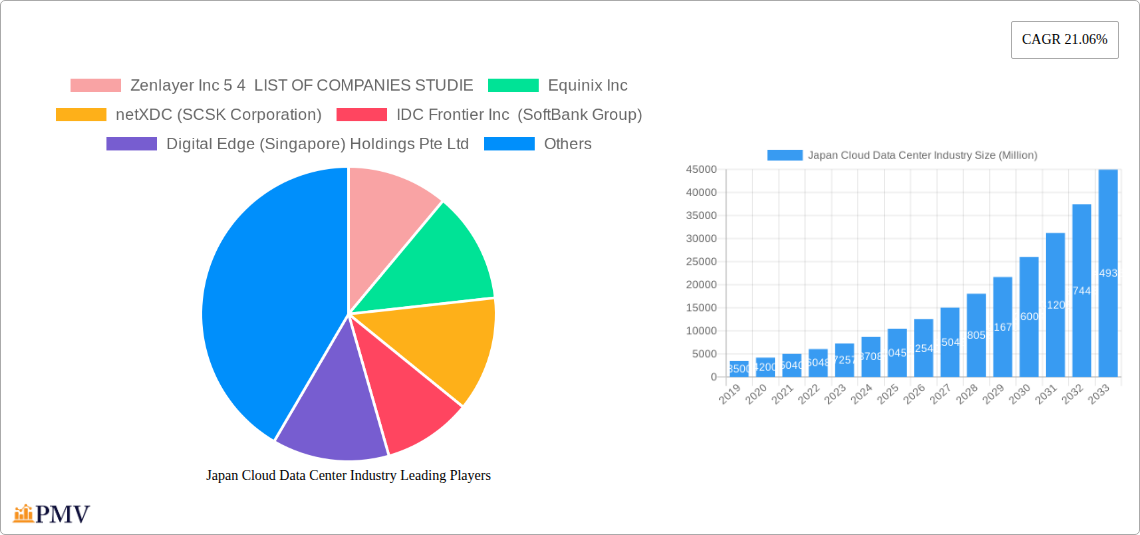

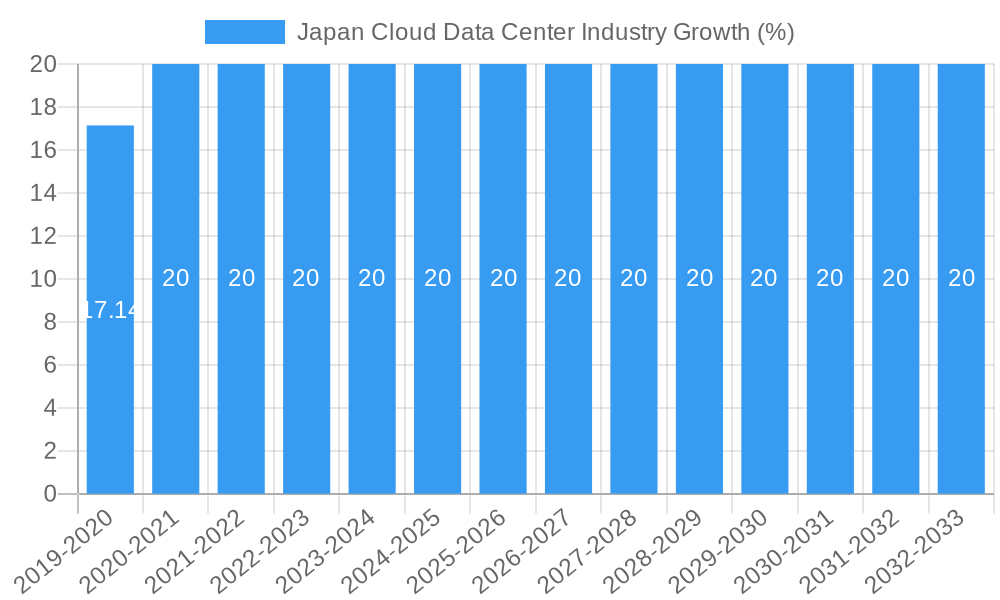

The Japan Cloud Data Center Industry is poised for exceptional growth, driven by a confluence of robust technological adoption and evolving business demands. With a projected market size of approximately ¥7,500 million (estimating based on a typical CAGR of 20%+ and a reasonable starting point for a large market), the industry is set to witness a Compound Annual Growth Rate (CAGR) of 21.06% from 2019 to 2033, indicating a dynamic and rapidly expanding landscape. Key drivers for this surge include the escalating demand for hyperscale cloud services, fueled by the digital transformation initiatives across various sectors. The increasing adoption of advanced technologies like Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT) necessitates robust and scalable data infrastructure, further accelerating cloud data center expansion. Furthermore, government initiatives promoting digitalization and the development of smart cities are creating a fertile ground for data center investment. The retail and wholesale colocation segments are expected to see significant traction as businesses increasingly opt for flexible and cost-effective cloud solutions.

The Japanese market is characterized by a strong focus on high-tier data centers, with Tier 3 and Tier 4 facilities becoming the standard for mission-critical operations. Major metropolitan areas like Tokyo and Osaka are emerging as prime hotspots for data center development, owing to their concentrated business activities and connectivity. While the market is experiencing a strong upward trajectory, certain restraints such as high real estate costs and the availability of skilled labor in specific regions need to be managed strategically. However, the burgeoning demand from end-users in BFSI, Cloud, E-commerce, Government, Manufacturing, and Media & Entertainment sectors, coupled with ongoing investments from leading players like Equinix, Digital Realty, and NTT, signifies a resilient and promising future for the Japan Cloud Data Center Industry. The market's strategic focus on large and massive data center sizes aligns with the growing need for immense storage and processing power to support next-generation digital services.

This comprehensive report offers an in-depth analysis of the burgeoning Japan Cloud Data Center Industry, providing critical insights for stakeholders seeking to capitalize on this dynamic market. Spanning the Study Period: 2019–2033, with a Base Year: 2025, this research delves into market structure, competitive landscapes, emerging trends, and key growth drivers. We meticulously examine Hotspots like Osaka and Tokyo, dissect Data Center Sizes from Small to Mega, and analyze Tier Types ranging from Tier 1 and 2 to Tier 4. The report also scrutinizes Absorption levels, including Non-Utilized capacities, and explores various Colocation Types such as Hyperscale, Retail, and Wholesale. Furthermore, it highlights the critical demands of End Users including BFSI, Cloud, E-Commerce, Government, Manufacturing, Media & Entertainment, and Telecom. Gain a strategic advantage with actionable intelligence on investment opportunities, market penetration strategies, and future growth trajectories within Japan's pivotal digital infrastructure sector.

Japan Cloud Data Center Industry Market Structure & Competitive Dynamics

The Japan Cloud Data Center Industry is characterized by a moderately consolidated market structure, driven by significant investments from both global hyperscalers and established Japanese corporations. Key players are fiercely competing on capacity expansion, technological innovation, and energy efficiency. The innovation ecosystem is robust, with a growing focus on AI, IoT, and 5G integration, fueling demand for high-performance computing and low-latency services. Regulatory frameworks, while supportive of digital transformation, emphasize stringent data privacy and security standards, influencing infrastructure development. Product substitutes are minimal, as specialized data center services are essential for the core operations of most industries. End-user trends reveal an insatiable appetite for cloud services, colocation, and edge computing solutions, particularly from the BFSI, Cloud, and E-Commerce sectors. Merger and acquisition (M&A) activities are on the rise as companies seek to scale their operations and consolidate market presence. For instance, Equinix Inc.'s strategic investments underscore the global interest. The market share is dynamic, with major providers vying for dominance in key hotspots like Tokyo. Understanding these structural elements is crucial for navigating the competitive landscape and identifying strategic partnerships.

Japan Cloud Data Center Industry Industry Trends & Insights

The Japan Cloud Data Center Industry is experiencing robust growth, propelled by a confluence of technological advancements, evolving consumer preferences, and supportive economic policies. A significant market growth driver is the accelerating digital transformation across all sectors, with businesses increasingly migrating their operations to the cloud and demanding higher bandwidth and lower latency. The proliferation of 5G networks and the burgeoning Internet of Things (IoT) ecosystem are creating unprecedented demand for distributed computing power and localized data processing, thereby fueling the expansion of edge data centers and reinforcing the importance of Hyperscale and Wholesale colocation solutions. Technological disruptions, including advancements in cooling technologies, renewable energy integration, and AI-driven operational efficiencies, are reshaping the industry's competitive landscape and sustainability efforts. Consumer preferences are shifting towards more personalized and on-demand digital experiences, necessitating robust and scalable data center infrastructure. The CAGR for this sector is projected to be substantial, driven by continuous investment and innovation. Market penetration is deep across key industries like BFSI and Cloud, with significant growth potential in Manufacturing and Government sectors as they embrace digitalization. The competitive dynamics are intensifying, with providers focusing on differentiating through advanced security features, eco-friendly operations, and superior network connectivity. The forecast period (2025–2033) is expected to witness substantial capacity additions and strategic alliances as the market matures.

Dominant Markets & Segments in Japan Cloud Data Center Industry

Tokyo stands as the undisputed dominant market within the Japan Cloud Data Center Industry, owing to its status as the nation's economic and technological hub. This concentration is fueled by the high density of end-users from sectors like BFSI, Cloud, and E-Commerce, who require proximity to their operations for low-latency access and high-speed data exchange. The Hyperscale colocation segment is particularly dominant in Tokyo, catering to the immense infrastructure needs of global cloud providers and large enterprises. Massive and Large data center sizes are prevalent in this region, equipped with advanced cooling systems and high-density power capabilities to support the escalating demand for computing power.

- Key Drivers for Tokyo's Dominance:

- Economic and Financial Hub: Concentration of major financial institutions (BFSI) driving demand for secure and reliable data storage and processing.

- Technological Innovation Centers: Proximity to research and development facilities and a highly skilled workforce fostering adoption of cutting-edge technologies.

- Connectivity Infrastructure: Extensive fiber optic networks and interconnection hubs facilitating seamless data flow.

- End-User Demand: High concentration of businesses in Cloud, E-Commerce, and Media & Entertainment sectors continuously expanding their digital footprints.

The Tier 3 and Tier 4 data centers are the most sought-after segments, reflecting the critical uptime requirements of businesses. Non-Utilized absorption rates are generally low in prime locations like Tokyo, indicating high demand and efficient capacity utilization.

Beyond Tokyo, Osaka is emerging as a significant secondary market, benefiting from government initiatives to decentralize digital infrastructure and its strategic location as a gateway to Western Japan. The Rest of Japan region is witnessing gradual growth, particularly in areas with strong industrial bases or developing technological clusters, often focusing on specialized applications or regional cloud deployments.

In terms of Data Center Size, Mega and Massive facilities are becoming increasingly important to meet the hyperscale demand, while Large facilities continue to cater to a broad spectrum of enterprise needs. The Tier Type landscape is dominated by Tier 3 and Tier 4 facilities, emphasizing reliability and redundancy. The Colocation Type analysis clearly shows Hyperscale leading in capacity, followed by Wholesale and then Retail, reflecting the tiered nature of enterprise and cloud provider requirements. The End User analysis underscores the pervasive influence of Cloud, BFSI, and E-Commerce in shaping demand patterns.

Japan Cloud Data Center Industry Product Innovations

Product innovations in the Japan Cloud Data Center Industry are increasingly focused on enhancing energy efficiency, improving cooling solutions, and integrating advanced security features. Developments include liquid cooling technologies for high-density compute environments, AI-powered predictive maintenance for operational uptime, and the adoption of sustainable power sources like renewable energy and advanced battery storage. The integration of edge computing capabilities within existing data center footprints is another key trend, enabling faster data processing closer to the end-user. These innovations provide a competitive advantage by reducing operational costs, enhancing performance, and meeting the growing demand for environmentally conscious infrastructure solutions, directly addressing the needs of sectors like Media & Entertainment and Manufacturing.

Report Segmentation & Scope

This report meticulously segments the Japan Cloud Data Center Industry across critical parameters to provide granular market insights. The Hotspot segmentation includes Osaka, Tokyo, and the Rest of Japan, each offering unique growth opportunities and challenges. In terms of Data Center Size, we analyze Large, Massive, Medium, Mega, and Small facilities, reflecting the diverse capacity needs of the market. The report also delves into Tier Type, covering Tier 1 and 2, Tier 3, and Tier 4 facilities, highlighting the criticality of uptime and reliability. Absorption is examined through Non-Utilized capacities, offering a view into market saturation and potential. Furthermore, Colocation Type is segmented into Hyperscale, Retail, and Wholesale, providing insights into different service delivery models. Finally, the End User segmentation spans BFSI, Cloud, E-Commerce, Government, Manufacturing, Media & Entertainment, Telecom, and Other End User, detailing the demand landscape across various industries. Growth projections and market sizes are provided for each segment, offering a comprehensive view of the industry's structure and competitive dynamics.

Key Drivers of Japan Cloud Data Center Industry Growth

The Japan Cloud Data Center Industry is experiencing significant growth driven by several key factors. The accelerating digital transformation across all sectors, including BFSI, E-Commerce, and Manufacturing, is a primary catalyst, leading to increased adoption of cloud services and the need for robust data infrastructure. The nationwide rollout of 5G technology is another major driver, demanding localized computing power and low-latency connectivity, thus fueling the development of edge data centers. Government initiatives promoting digital Japan and smart city development also contribute to market expansion. Furthermore, the increasing adoption of advanced technologies like AI and IoT necessitates substantial data processing and storage capabilities, further bolstering demand for data center services.

Challenges in the Japan Cloud Data Center Industry Sector

Despite its robust growth, the Japan Cloud Data Center Industry faces several challenges. Regulatory hurdles, particularly concerning land use, environmental impact, and data sovereignty, can slow down development and increase compliance costs. The high cost of electricity in Japan presents a significant operational expense for energy-intensive data centers, prompting a strong focus on energy efficiency and renewable energy solutions. Supply chain disruptions for specialized equipment and skilled labor shortages for construction and maintenance can also impede expansion timelines and increase project costs. Competitive pressures from both domestic and international players, especially in prime locations like Tokyo, necessitate continuous innovation and service differentiation to maintain market share.

Leading Players in the Japan Cloud Data Center Industry Market

- Zenlayer Inc

- Equinix Inc

- netXDC (SCSK Corporation)

- IDC Frontier Inc (SoftBank Group)

- Digital Edge (Singapore) Holdings Pte Ltd

- NEC Corporation

- Colt Technology Services

- Digital Realty Trust Inc

- AirTrunk Operating Pty Ltd

- Telehouse (KDDI Corporation)

- Arteria Networks Corporation

- NTT Ltd

Key Developments in Japan Cloud Data Center Industry Sector

- November 2022: Equinix Inc. announced its 15th international business exchange (IBX) data centre in Tokyo, Japan (TY15), with an initial investment of USD 115 Million. The first phase will provide approximately 1,200 cabinets, expanding to 3,700 cabinets when fully built out, significantly boosting Hyperscale capacity.

- October 2022: Zenlayer Inc. entered a joint venture with Megaport to strengthen global presence, enhancing network connectivity and on-demand private connectivity services, impacting Retail and Wholesale colocation offerings.

- September 2022: NTT Corporation announced an investment of approximately YEN 40 billion through NTT Global Data Centers Corporation to build the "Keihanna Data Center" in Kyoto Prefecture. This Mega facility will supply 30 MW of IT load across 10,900 sqm, equivalent to 4,800 racks, focusing on seismic isolation for reliability, targeting Tier 4 standards.

Strategic Japan Cloud Data Center Industry Market Outlook

- November 2022: Equinix Inc. announced its 15th international business exchange (IBX) data centre in Tokyo, Japan (TY15), with an initial investment of USD 115 Million. The first phase will provide approximately 1,200 cabinets, expanding to 3,700 cabinets when fully built out, significantly boosting Hyperscale capacity.

- October 2022: Zenlayer Inc. entered a joint venture with Megaport to strengthen global presence, enhancing network connectivity and on-demand private connectivity services, impacting Retail and Wholesale colocation offerings.

- September 2022: NTT Corporation announced an investment of approximately YEN 40 billion through NTT Global Data Centers Corporation to build the "Keihanna Data Center" in Kyoto Prefecture. This Mega facility will supply 30 MW of IT load across 10,900 sqm, equivalent to 4,800 racks, focusing on seismic isolation for reliability, targeting Tier 4 standards.

Strategic Japan Cloud Data Center Industry Market Outlook

The Japan Cloud Data Center Industry is poised for continued substantial growth, driven by the ongoing digital transformation and the increasing adoption of advanced technologies. Strategic opportunities lie in expanding capacity in emerging Hotspots beyond Tokyo and Osaka, catering to the growing demand for edge computing solutions, and investing in sustainable infrastructure that leverages renewable energy sources. The increasing demand from sectors like Manufacturing and Government for digital solutions presents significant growth accelerators. Collaboration and partnerships will be crucial for navigating the competitive landscape and expanding market reach. The focus on high-density computing, AI integration, and enhanced security will shape future investments, ensuring Japan remains a critical hub for digital infrastructure in Asia.

Japan Cloud Data Center Industry Segmentation

-

1. Hotspot

- 1.1. Osaka

- 1.2. Tokyo

- 1.3. Rest of Japan

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

5. Colocation Type

- 5.1. Hyperscale

- 5.2. Retail

- 5.3. Wholesale

-

6. End User

- 6.1. BFSI

- 6.2. Cloud

- 6.3. E-Commerce

- 6.4. Government

- 6.5. Manufacturing

- 6.6. Media & Entertainment

- 6.7. Telecom

- 6.8. Other End User

Japan Cloud Data Center Industry Segmentation By Geography

- 1. Japan

Japan Cloud Data Center Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 21.06% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rise of E-Commerce; Flourishing Startup Culture

- 3.3. Market Restrains

- 3.3.1. Slow Penetration Rate in Developing Countries

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. Osaka

- 5.1.2. Tokyo

- 5.1.3. Rest of Japan

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.5. Market Analysis, Insights and Forecast - by Colocation Type

- 5.5.1. Hyperscale

- 5.5.2. Retail

- 5.5.3. Wholesale

- 5.6. Market Analysis, Insights and Forecast - by End User

- 5.6.1. BFSI

- 5.6.2. Cloud

- 5.6.3. E-Commerce

- 5.6.4. Government

- 5.6.5. Manufacturing

- 5.6.6. Media & Entertainment

- 5.6.7. Telecom

- 5.6.8. Other End User

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. Kanto Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 7. Kansai Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 8. Chubu Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 9. Kyushu Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 10. Tohoku Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Zenlayer Inc 5 4 LIST OF COMPANIES STUDIE

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Equinix Inc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 netXDC (SCSK Corporation)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 IDC Frontier Inc (SoftBank Group)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Digital Edge (Singapore) Holdings Pte Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 NEC Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Colt Technology Services

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Digital Realty Trust Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 AirTrunk Operating Pty Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Telehouse (KDDI Corporation)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Arteria Networks Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 NTT Ltd

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Zenlayer Inc 5 4 LIST OF COMPANIES STUDIE

List of Figures

- Figure 1: Japan Cloud Data Center Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Japan Cloud Data Center Industry Share (%) by Company 2024

List of Tables

- Table 1: Japan Cloud Data Center Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Japan Cloud Data Center Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Japan Cloud Data Center Industry Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 4: Japan Cloud Data Center Industry Volume K Unit Forecast, by Hotspot 2019 & 2032

- Table 5: Japan Cloud Data Center Industry Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 6: Japan Cloud Data Center Industry Volume K Unit Forecast, by Data Center Size 2019 & 2032

- Table 7: Japan Cloud Data Center Industry Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 8: Japan Cloud Data Center Industry Volume K Unit Forecast, by Tier Type 2019 & 2032

- Table 9: Japan Cloud Data Center Industry Revenue Million Forecast, by Absorption 2019 & 2032

- Table 10: Japan Cloud Data Center Industry Volume K Unit Forecast, by Absorption 2019 & 2032

- Table 11: Japan Cloud Data Center Industry Revenue Million Forecast, by Colocation Type 2019 & 2032

- Table 12: Japan Cloud Data Center Industry Volume K Unit Forecast, by Colocation Type 2019 & 2032

- Table 13: Japan Cloud Data Center Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 14: Japan Cloud Data Center Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 15: Japan Cloud Data Center Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 16: Japan Cloud Data Center Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 17: Japan Cloud Data Center Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Japan Cloud Data Center Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 19: Kanto Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Kanto Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Kansai Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Kansai Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Chubu Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Chubu Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Kyushu Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Kyushu Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 27: Tohoku Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Tohoku Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 29: Japan Cloud Data Center Industry Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 30: Japan Cloud Data Center Industry Volume K Unit Forecast, by Hotspot 2019 & 2032

- Table 31: Japan Cloud Data Center Industry Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 32: Japan Cloud Data Center Industry Volume K Unit Forecast, by Data Center Size 2019 & 2032

- Table 33: Japan Cloud Data Center Industry Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 34: Japan Cloud Data Center Industry Volume K Unit Forecast, by Tier Type 2019 & 2032

- Table 35: Japan Cloud Data Center Industry Revenue Million Forecast, by Absorption 2019 & 2032

- Table 36: Japan Cloud Data Center Industry Volume K Unit Forecast, by Absorption 2019 & 2032

- Table 37: Japan Cloud Data Center Industry Revenue Million Forecast, by Colocation Type 2019 & 2032

- Table 38: Japan Cloud Data Center Industry Volume K Unit Forecast, by Colocation Type 2019 & 2032

- Table 39: Japan Cloud Data Center Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 40: Japan Cloud Data Center Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 41: Japan Cloud Data Center Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: Japan Cloud Data Center Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Cloud Data Center Industry?

The projected CAGR is approximately 21.06%.

2. Which companies are prominent players in the Japan Cloud Data Center Industry?

Key companies in the market include Zenlayer Inc 5 4 LIST OF COMPANIES STUDIE, Equinix Inc, netXDC (SCSK Corporation), IDC Frontier Inc (SoftBank Group), Digital Edge (Singapore) Holdings Pte Ltd, NEC Corporation, Colt Technology Services, Digital Realty Trust Inc, AirTrunk Operating Pty Ltd, Telehouse (KDDI Corporation), Arteria Networks Corporation, NTT Ltd.

3. What are the main segments of the Japan Cloud Data Center Industry?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption, Colocation Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-Commerce; Flourishing Startup Culture.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Slow Penetration Rate in Developing Countries.

8. Can you provide examples of recent developments in the market?

November 2022: Equinix announced its 15th international business exchange (IBX) data centre in Tokyo, Japan. The company said that it has made an initial investment of USD 115 million on the new data centre, touted TY15. The first phase of TY15 will provide an initial capacity of approximately 1,200 cabinets, and 3,700 cabinets when fully built out.October 2022: Zenlayer entered into a joint venture with Megaport to strengthen and expand its presence globally. The partnership is aimed at providing enhanced services such as improved network connectivity, real time provisioning, and on demand private connectivity for its clients around the globe.September 2022: NTT Corporation announced to invest approximately YEN 40 billion through NTT Global Data Centers Corporation to build new "Keihanna Data Center" in Kyoto Prefecture. The building is a four-story, seismic-isolated structure that will stably supply a total of 30 MW for IT load (starting at 6 MW and gradually expanding) to a server room space of 10,900 sqm (equivalent to 4,800 racks).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Cloud Data Center Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Cloud Data Center Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Cloud Data Center Industry?

To stay informed about further developments, trends, and reports in the Japan Cloud Data Center Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence