Key Insights

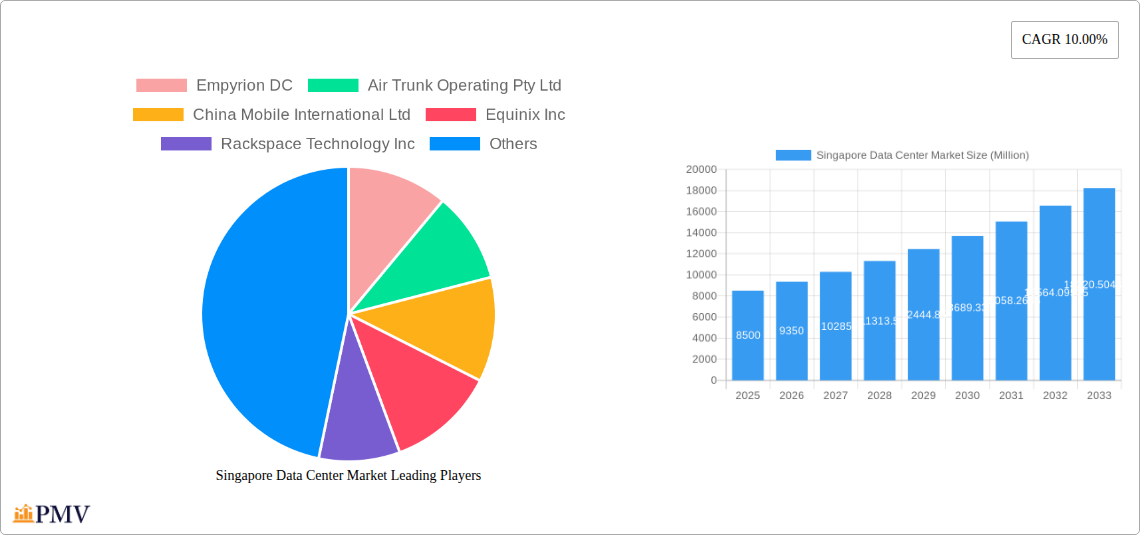

The Singapore Data Center Market is poised for substantial growth, projected to reach approximately USD XX million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 10.00% throughout the forecast period of 2025-2033. This upward trajectory is primarily propelled by an escalating demand for digital infrastructure, driven by the rapid adoption of cloud computing services across various sectors. Key growth drivers include the increasing proliferation of Big Data analytics, the surge in e-commerce activities, and the continuous expansion of the telecommunications sector, all of which necessitate more advanced and scalable data storage and processing capabilities. Furthermore, government initiatives aimed at fostering a digital economy and smart nation strategies are significantly contributing to the market's expansion by encouraging investment in high-quality data center facilities. The competitive landscape is characterized by the presence of major global and regional players, including Empyrion DC, Equinix Inc., and Digital Realty Trust Inc., who are actively investing in capacity expansion and technological upgrades to cater to evolving market needs.

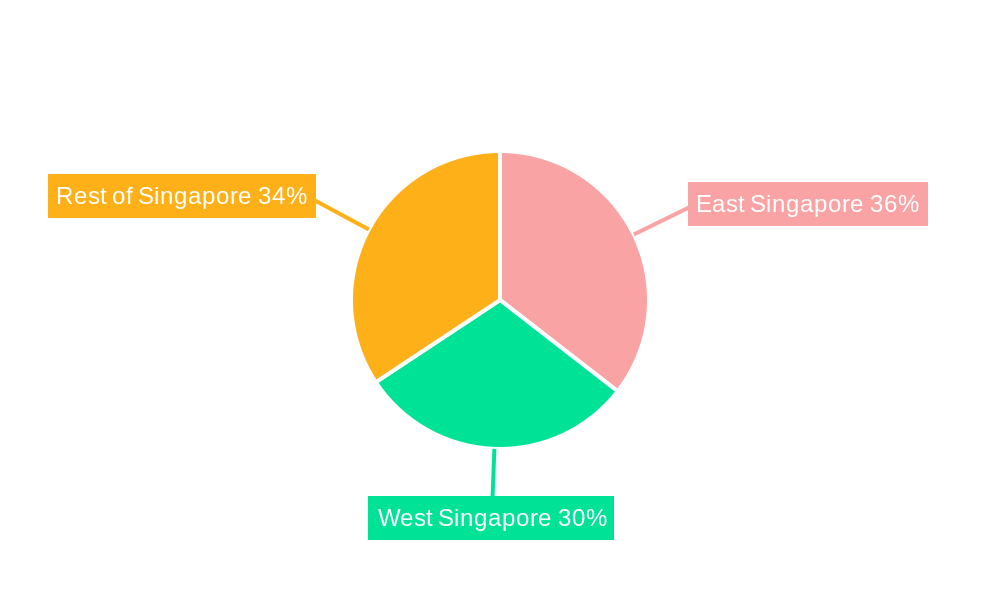

The market segmentation reveals a dynamic operational landscape. In terms of geographical focus, East Singapore and West Singapore are identified as key hotspots, likely due to their established infrastructure and strategic locations. Data center sizes are diversified, ranging from Small to Mega, indicating a comprehensive catering to varied client requirements, from niche startups to large-scale enterprises. The distribution across Tier Types (Tier 1 to Tier 4) highlights a commitment to reliability and high availability, essential for mission-critical applications. Notably, the absorption rate of Non-Utilized capacity suggests a healthy market with ongoing development to meet future demand. End-user segments such as Cloud, BFSI, E-Commerce, Government, Manufacturing, and Media & Entertainment are the primary beneficiaries and contributors to this growth, underscoring the pervasive digital transformation across the Singaporean economy. Despite the strong growth prospects, potential restraints such as escalating operational costs, stringent environmental regulations, and the need for continuous technological innovation present challenges that market players must strategically address.

Singapore Data Center Market Report Description

This comprehensive report offers an in-depth analysis of the Singapore Data Center Market, a critical hub for digital infrastructure in Asia. Covering the Study Period of 2019–2033, with a Base Year of 2025, Estimated Year of 2025, and Forecast Period of 2025–2033, it provides unparalleled insights into market dynamics, trends, and future outlook. Our detailed research spans the Historical Period of 2019–2024, delivering actionable intelligence for stakeholders.

The report delves into key segments including Hotspot: East Singapore, West Singapore, and Rest of Singapore, alongside Data Center Size: Large, Massive, Medium, Mega, and Small. It meticulously examines Tier Type: Tier 1, Tier 2, Tier 3, and Tier 4, and explores Absorption: Non-Utilized. Furthermore, it analyzes the influence of various End Users: Cloud, BFSI, E-Commerce, Government, Manufacturing, Media & Entertainment, Telecom, and Other End User. With a focus on hyperscale data center expansion and sustainable energy solutions, this report is an indispensable resource for investors, operators, and technology providers.

Singapore Data Center Market Market Structure & Competitive Dynamics

The Singapore Data Center Market exhibits a dynamic and evolving market structure characterized by intense competition and strategic alliances. Market concentration is moderate, with a few dominant players holding significant market share, while a growing number of specialized operators vie for niche segments. Innovation ecosystems are thriving, driven by the demand for advanced technologies such as AI, IoT, and edge computing, pushing operators to invest in cutting-edge infrastructure and solutions. Regulatory frameworks in Singapore are generally supportive of data center development, focusing on energy efficiency, security, and data privacy, though evolving environmental regulations present new challenges and opportunities. Product substitutes are limited, as purpose-built data centers offer superior performance and reliability compared to alternative solutions. End-user trends indicate a strong preference for cloud services, BFSI, and e-commerce, driving demand for high-density, low-latency facilities. Mergers and acquisitions (M&A) activities are prevalent, as larger players consolidate their market positions and smaller firms seek strategic partnerships to scale operations. Notable M&A deal values are expected to rise as the market matures and consolidation accelerates. The competitive landscape is shaped by investments in new builds, expansions, and upgrades to existing facilities, with companies constantly seeking to differentiate themselves through service offerings, sustainability initiatives, and geographical reach.

Singapore Data Center Market Industry Trends & Insights

The Singapore Data Center Market is experiencing robust growth, propelled by a confluence of technological advancements, escalating digital transformation across industries, and favorable government policies. The projected Compound Annual Growth Rate (CAGR) for the market is substantial, reflecting the increasing demand for digital services and the critical role of data centers in supporting them. Technological disruptions, including the adoption of AI, machine learning, and 5G, are fundamentally reshaping the requirements for data center infrastructure, driving demand for higher computing power, lower latency, and increased scalability. Consumer preferences are increasingly leaning towards on-demand, highly available digital services, which necessitate resilient and efficient data center operations. This trend is particularly evident in sectors like E-Commerce and Media & Entertainment, where seamless user experiences are paramount. Competitive dynamics are intensifying, with both established global players and emerging regional operators investing heavily in expanding their footprints and enhancing their service portfolios. Market penetration of advanced cooling technologies and renewable energy sources is on an upward trajectory, as operators strive to meet sustainability targets and reduce operational costs. The strategic location of Singapore as a digital gateway to Asia further bolsters its position, attracting significant foreign direct investment and fueling continuous expansion of colocation and hyperscale facilities. The growth in cloud adoption by enterprises of all sizes is a primary market driver, alongside the increasing data generation from IoT devices and the burgeoning digital economy.

Dominant Markets & Segments in Singapore Data Center Market

Within the Singapore Data Center Market, the East Singapore region emerges as a dominant hotspot due to its established infrastructure, proximity to key business districts, and excellent connectivity. This region benefits from significant investments in hyperscale facilities and colocation services, catering to the robust demand from Cloud and BFSI end-users. The dominance of East Singapore is further reinforced by its strategic location for subsea cable landings and its mature ecosystem of technology providers and service integrators.

Data Center Size segmentation reveals that Mega and Large data centers are currently dominating the market. This trend is driven by the increasing demand for hyperscale cloud providers and large enterprises requiring vast amounts of computing power and storage. The need for economies of scale and the efficiency gains associated with larger facilities contribute to their prominence.

In terms of Tier Type, Tier 3 data centers are widely prevalent, offering a balance of redundancy and availability essential for most business operations. However, there is a growing demand for Tier 4 facilities, particularly from mission-critical sectors like BFSI and Government, seeking the highest levels of uptime and resilience.

The End User landscape is dominated by Cloud providers, who are the primary drivers of hyperscale deployments. Following closely are BFSI, E-Commerce, and Government sectors, all of which are heavily reliant on robust and secure data center infrastructure to support their digital operations and services. The increasing digitalization within the Manufacturing sector and the demand for enhanced streaming capabilities in Media & Entertainment are also contributing to market growth.

Regarding Absorption, while Non-Utilized capacity exists, it is rapidly diminishing as demand outpaces new supply, especially in prime locations. The high rate of absorption indicates a healthy and growing market.

Key drivers for the dominance of these segments include:

- Government Initiatives: Proactive policies encouraging digital economy growth and investment in advanced infrastructure.

- Connectivity Excellence: Singapore's position as a global telecommunications hub with extensive subsea cable networks.

- Skilled Workforce: Availability of a highly skilled talent pool essential for managing complex data center operations.

- Business-Friendly Environment: A stable political climate and ease of doing business attracting significant foreign investment.

- Demand for High Performance Computing: The burgeoning need for AI, big data analytics, and IoT solutions.

Singapore Data Center Market Product Innovations

Product innovations in the Singapore Data Center Market are primarily focused on enhancing efficiency, sustainability, and performance. Advancements in liquid cooling technologies are gaining traction to manage the heat generated by high-density compute racks, crucial for AI and HPC workloads. Furthermore, the integration of AI-powered management systems is optimizing power usage, cooling efficiency, and predictive maintenance, leading to significant operational cost savings and improved reliability. The development of modular data center designs is enabling faster deployment and greater flexibility to meet fluctuating demand. Companies are also investing in greener energy solutions, including exploring the use of hydrogen fuel cells and increasing reliance on renewable energy sources to power their facilities, addressing growing environmental concerns and regulatory pressures. These innovations provide a competitive advantage by offering clients more sustainable, cost-effective, and high-performance solutions.

Report Segmentation & Scope

This report segments the Singapore Data Center Market comprehensively. We analyze Hotspot segmentation into East Singapore, West Singapore, and Rest of Singapore, providing granular insights into regional demand drivers and infrastructure development. Data Center Size is categorized into Large, Massive, Medium, Mega, and Small facilities, detailing capacity trends and investment patterns. The Tier Type segmentation covers Tier 1, Tier 2, Tier 3, and Tier 4 data centers, reflecting varying levels of availability and redundancy requirements. The report also examines Absorption rates, focusing on Non-Utilized capacity and its implications for market dynamics. Finally, End User analysis includes Cloud, BFSI, E-Commerce, Government, Manufacturing, Media & Entertainment, Telecom, and Other End User segments, mapping their specific data center needs and growth projections. Each segment is analyzed for its current market size, projected growth, and competitive landscape, offering a detailed view of the market's intricate structure.

Key Drivers of Singapore Data Center Market Growth

The Singapore Data Center Market is propelled by several key drivers. The escalating demand for cloud computing services from enterprises across all sectors, including BFSI, E-Commerce, and Government, is a primary growth accelerator. Singapore's strategic geographic location as a digital gateway to Asia and its robust submarine cable connectivity facilitate significant cross-border data flows and international business operations. Furthermore, government initiatives promoting digital transformation, smart nation development, and attracting foreign investment in the technology sector create a conducive environment for data center expansion. The increasing adoption of advanced technologies such as Artificial Intelligence, Big Data Analytics, and the Internet of Things (IoT) generates massive data volumes, necessitating more advanced and scalable data center infrastructure. Finally, the growing emphasis on sustainability and energy efficiency is driving investments in green data center technologies and renewable energy sources.

Challenges in the Singapore Data Center Market Sector

Despite its robust growth, the Singapore Data Center Market faces several challenges. Land scarcity and high real estate costs in Singapore present a significant barrier to new developments and expansions, impacting the overall cost of operations. Stringent environmental regulations, particularly concerning energy consumption and carbon emissions, require substantial investments in sustainable technologies and operational practices, increasing capital expenditure. The intense competition among existing players and the influx of new entrants can lead to price wars and pressure on profit margins. Furthermore, the global supply chain disruptions can affect the timely procurement of specialized equipment and components, potentially delaying project timelines. Ensuring an adequate supply of skilled labor for the operation and maintenance of sophisticated data center facilities remains a continuous challenge.

Leading Players in the Singapore Data Center Market Market

- Empyrion DC

- Air Trunk Operating Pty Ltd

- China Mobile International Ltd

- Equinix Inc

- Rackspace Technology Inc

- 1-Net Singapore Pte Ltd (Mediacorp)

- PhoenixNAP

- Princeton Digital Group

- Cyxtera Technologies

- Digital Realty Trust Inc

- Global Switch Holdings Limited

Key Developments in Singapore Data Center Market Sector

- November 2022: AirTrunk completed the final phase of SGP1 data center, expanding its total capacity to more than 78 MW, enabling hyperscale capacity deployment at unprecedented speed and scale.

- September 2022: Equinix, Inc. announced a partnership with the Centre for Energy Research & Technology (CERT) under the National University of Singapore's (NUS) College of Design and Engineering to explore hydrogen as a green fuel source for mission-critical data center infrastructure.

- June 2022: phoenixNAP announced a partnership with Pliops, a leading provider of data processors for cloud and enterprise data centers, enabling phoenixNAP to deliver on-demand cloud services for performance-sensitive users.

Strategic Singapore Data Center Market Market Outlook

The strategic outlook for the Singapore Data Center Market remains exceptionally positive, driven by its continued role as a pivotal digital hub in Asia. Growth accelerators include the sustained demand from hyperscale cloud providers, increasing enterprise adoption of hybrid and multi-cloud strategies, and the burgeoning need for edge computing solutions to support 5G and IoT deployments. Opportunities abound in the development of sustainable and energy-efficient data centers, aligning with global environmental goals and regulatory mandates. Strategic investments in advanced cooling technologies, renewable energy integration, and intelligent automation will be crucial for market leaders. The government's commitment to fostering innovation and its strategic initiatives to position Singapore as a leading digital economy will continue to attract significant investment, ensuring robust expansion and technological advancement within the market. The market is poised for continued growth through a combination of new build projects, expansions of existing facilities, and strategic acquisitions.

Singapore Data Center Market Segmentation

-

1. Hotspot

- 1.1. East Singapore

- 1.2. West Singapore

- 1.3. Rest of Singapore

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1

- 3.2. Tier 2

- 3.3. Tier 3

- 3.4. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

5. End User

- 5.1. Cloud

- 5.2. BFSI

- 5.3. E-Commerce

- 5.4. Government

- 5.5. Manufacturing

- 5.6. Media & Entertainment

- 5.7. Telecom

- 5.8. Other End User

Singapore Data Center Market Segmentation By Geography

- 1. Singapore

Singapore Data Center Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Awareness of Energy Consumption Control

- 3.3. Market Restrains

- 3.3.1. High Risk Associated with Data

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Singapore Data Center Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. East Singapore

- 5.1.2. West Singapore

- 5.1.3. Rest of Singapore

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1

- 5.3.2. Tier 2

- 5.3.3. Tier 3

- 5.3.4. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Cloud

- 5.5.2. BFSI

- 5.5.3. E-Commerce

- 5.5.4. Government

- 5.5.5. Manufacturing

- 5.5.6. Media & Entertainment

- 5.5.7. Telecom

- 5.5.8. Other End User

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Singapore

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Empyrion DC

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Air Trunk Operating Pty Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 China Mobile International Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Equinix Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Rackspace Technology Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 1-Net Singapore Pte Ltd (Mediacorp)

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 PhoenixNAP

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Princeton Digital Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Cyxtera Technologies

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Digital Realty Trust Inc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Global Switch Holdings Limited

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 Empyrion DC

List of Figures

- Figure 1: Singapore Data Center Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Singapore Data Center Market Share (%) by Company 2024

List of Tables

- Table 1: Singapore Data Center Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Singapore Data Center Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Singapore Data Center Market Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 4: Singapore Data Center Market Volume K Unit Forecast, by Hotspot 2019 & 2032

- Table 5: Singapore Data Center Market Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 6: Singapore Data Center Market Volume K Unit Forecast, by Data Center Size 2019 & 2032

- Table 7: Singapore Data Center Market Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 8: Singapore Data Center Market Volume K Unit Forecast, by Tier Type 2019 & 2032

- Table 9: Singapore Data Center Market Revenue Million Forecast, by Absorption 2019 & 2032

- Table 10: Singapore Data Center Market Volume K Unit Forecast, by Absorption 2019 & 2032

- Table 11: Singapore Data Center Market Revenue Million Forecast, by End User 2019 & 2032

- Table 12: Singapore Data Center Market Volume K Unit Forecast, by End User 2019 & 2032

- Table 13: Singapore Data Center Market Revenue Million Forecast, by Region 2019 & 2032

- Table 14: Singapore Data Center Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 15: Singapore Data Center Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Singapore Data Center Market Volume K Unit Forecast, by Country 2019 & 2032

- Table 17: Singapore Data Center Market Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 18: Singapore Data Center Market Volume K Unit Forecast, by Hotspot 2019 & 2032

- Table 19: Singapore Data Center Market Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 20: Singapore Data Center Market Volume K Unit Forecast, by Data Center Size 2019 & 2032

- Table 21: Singapore Data Center Market Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 22: Singapore Data Center Market Volume K Unit Forecast, by Tier Type 2019 & 2032

- Table 23: Singapore Data Center Market Revenue Million Forecast, by Absorption 2019 & 2032

- Table 24: Singapore Data Center Market Volume K Unit Forecast, by Absorption 2019 & 2032

- Table 25: Singapore Data Center Market Revenue Million Forecast, by End User 2019 & 2032

- Table 26: Singapore Data Center Market Volume K Unit Forecast, by End User 2019 & 2032

- Table 27: Singapore Data Center Market Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Singapore Data Center Market Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Singapore Data Center Market?

The projected CAGR is approximately 10.00%.

2. Which companies are prominent players in the Singapore Data Center Market?

Key companies in the market include Empyrion DC, Air Trunk Operating Pty Ltd, China Mobile International Ltd, Equinix Inc, Rackspace Technology Inc, 1-Net Singapore Pte Ltd (Mediacorp), PhoenixNAP, Princeton Digital Group, Cyxtera Technologies, Digital Realty Trust Inc, Global Switch Holdings Limited.

3. What are the main segments of the Singapore Data Center Market?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Awareness of Energy Consumption Control.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

High Risk Associated with Data.

8. Can you provide examples of recent developments in the market?

November 2022: AirTrunk completed the final phase of SGP1 data center expanding the total capacity of the data center to more than 78 MW to deploy hyperscale capacity at at unprecedented speed and scale.September 2022: Equinix, Inc. announced a partnership with the Centre for Energy Research & Technology (CERT) under the National University of Singapore's (NUS) College of Design and Engineering to explore technologies that enable the use of hydrogen as a green fuel source for mission-critical data center infrastructure.June 2022: phoenixNAP announced that it has entered into a partnership with Pliops, a leading provider of data processors for cloud and enterprise data centers. Through this collaboration, phoenixNAP will delivers on-demand cloud services that meet the needs of performance-sensitive users.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Singapore Data Center Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Singapore Data Center Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Singapore Data Center Market?

To stay informed about further developments, trends, and reports in the Singapore Data Center Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence