Key Insights

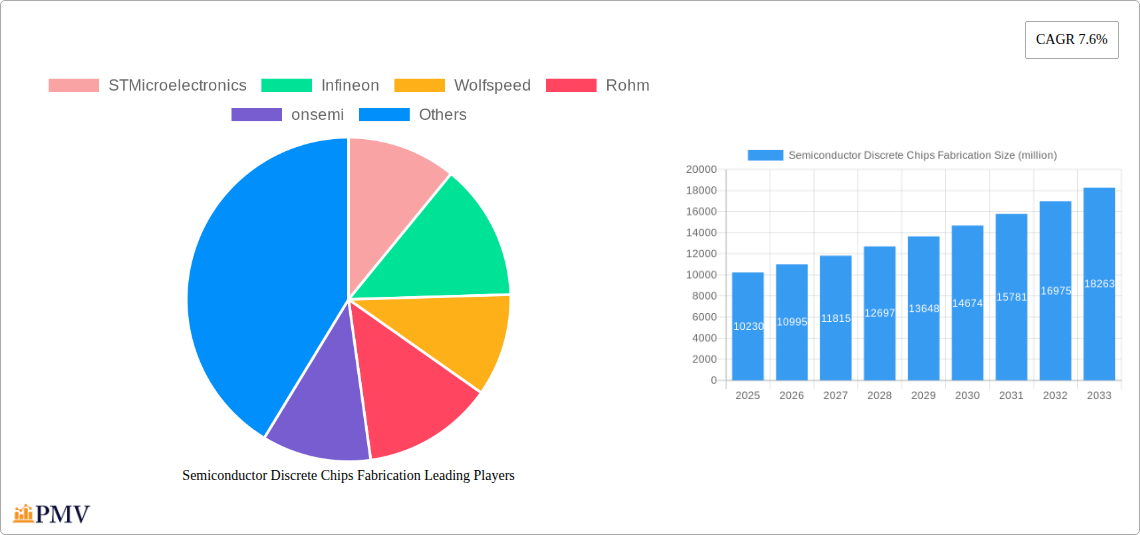

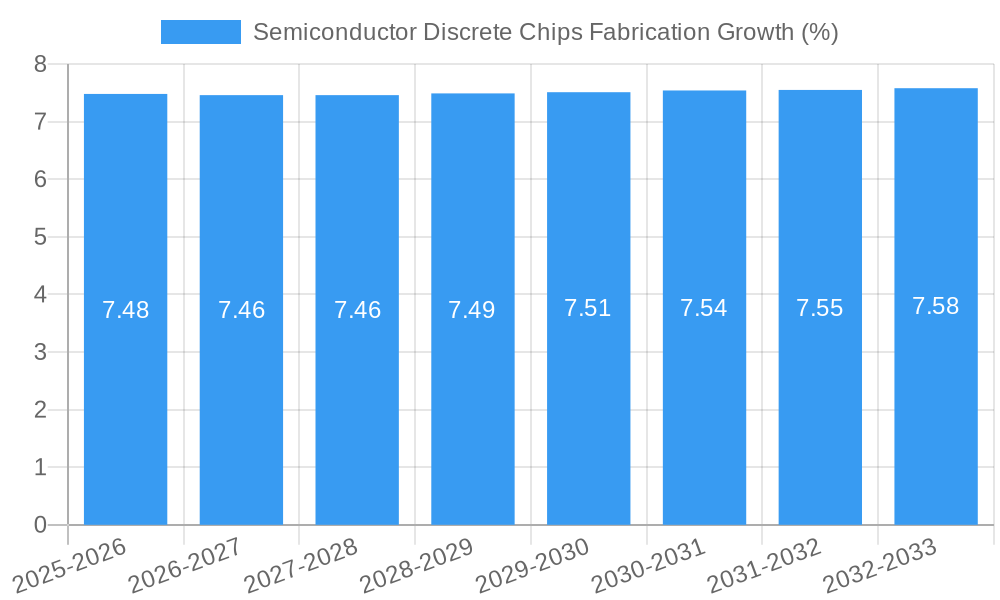

The Semiconductor Discrete Chips Fabrication market is poised for significant expansion, with an estimated market size of USD 10,230 million in the base year 2025. Driven by a robust Compound Annual Growth Rate (CAGR) of 7.6%, the market is projected to reach substantial valuations by 2033. Key growth engines fueling this ascent include the escalating demand for electrification in the automotive sector, where discrete components are fundamental to power management and control systems. The burgeoning industrial automation landscape, characterized by the adoption of advanced robotics and smart manufacturing processes, further necessitates a steady supply of high-performance discrete chips. Additionally, the relentless innovation in consumer electronics, from high-end smartphones to wearable devices, continues to be a primary catalyst, demanding smaller, more efficient, and reliable discrete components. The increasing global emphasis on renewable energy solutions and grid modernization also contributes to this upward trajectory, as discrete chips play a crucial role in power converters and control circuits within these systems.

While the market demonstrates strong growth potential, certain factors present challenges. Intense competition among a large and diverse set of fabrication foundries, coupled with the high capital expenditure required for advanced manufacturing facilities, can exert pressure on profit margins. Furthermore, supply chain volatilities, exacerbated by geopolitical tensions and the inherent complexities of semiconductor manufacturing, can lead to production delays and price fluctuations. Nonetheless, technological advancements such as the transition to next-generation materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) for high-power applications, alongside continuous improvements in wafer fabrication processes, are expected to overcome these restraints. The market's segmentation across various applications, including automotive, industrial, and consumer electronics, along with diverse types like IGBT, MOSFET, and Diode wafer foundries, indicates a broad and multifaceted demand, positioning the Semiconductor Discrete Chips Fabrication market for sustained and dynamic growth throughout the forecast period.

This in-depth report provides a thorough analysis of the global Semiconductor Discrete Chips Fabrication market, covering historical performance, current trends, and future projections. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period of 2025–2033, this report offers critical insights for stakeholders seeking to understand market dynamics, identify growth opportunities, and navigate the competitive landscape. We delve into the intricacies of discrete semiconductor manufacturing, including IGBT wafer foundry, MOSFET wafer foundry, diode wafer foundry, and BJT wafer foundry, across key applications like Automotive, Industrial, Consumer Electronics, and UPS & Data Center.

Semiconductor Discrete Chips Fabrication Market Structure & Competitive Dynamics

The Semiconductor Discrete Chips Fabrication market exhibits a complex structure characterized by both established giants and emerging players. Market concentration varies across different segments, with high-end power semiconductor fabrication often dominated by a few key companies possessing advanced R&D capabilities and substantial manufacturing infrastructure. The innovation ecosystem thrives on continuous advancements in materials science, process technology, and device architecture, driving the demand for higher efficiency, smaller form factors, and increased power density in discrete semiconductor devices. Regulatory frameworks, particularly concerning environmental impact and supply chain security, play a significant role in shaping market entry and operational strategies for discrete chip manufacturers.

Product substitutes are minimal in the core applications of discrete semiconductors, where their unique characteristics of high voltage, high current handling, and fast switching speeds are often indispensable. However, integration into System-on-Chip (SoC) solutions for certain consumer electronics applications can represent a form of substitution. End-user trends are heavily influenced by the burgeoning demand from the automotive sector for electric vehicles (EVs) and advanced driver-assistance systems (ADAS), the growing need for energy-efficient solutions in industrial automation, and the increasing adoption of smart technologies in consumer electronics. Merger and acquisition (M&A) activities are prevalent as companies seek to expand their product portfolios, acquire cutting-edge technologies, and gain market share. Recent M&A deals in the semiconductor foundry space have seen valuations in the hundreds of millions to billions of dollars, reflecting the strategic importance of this sector. For instance, the acquisition of a specialized IGBT wafer foundry by a major automotive supplier would be valued in the tens of millions of dollars, while the acquisition of a leading MOSFET wafer foundry by a global semiconductor company could easily exceed several hundred million dollars.

Semiconductor Discrete Chips Fabrication Industry Trends & Insights

The Semiconductor Discrete Chips Fabrication industry is experiencing robust growth, driven by a confluence of technological advancements, evolving consumer preferences, and critical industry developments. The CAGR for the discrete semiconductor market is projected to be approximately 8.7% over the forecast period, reaching an estimated market size of USD 35 million by 2025. Key market growth drivers include the relentless expansion of the electric vehicle (EV) market, which demands high-performance power semiconductors like IGBTs and MOSFETs for inverters, converters, and battery management systems. The industrial sector's drive towards automation, smart grids, and renewable energy integration further fuels demand for efficient and reliable discrete components.

Technological disruptions are primarily centered around advancements in wide-bandgap (WBG) materials such as Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials enable higher operating temperatures, faster switching speeds, and reduced power losses compared to traditional silicon-based devices, leading to more compact and efficient power systems. The adoption of WBG discrete semiconductor chips is a significant trend, with the SiC and GaN segment expected to grow at a CAGR of 25%. Consumer preferences are shifting towards energy-efficient appliances, advanced audio-visual equipment, and the proliferation of smart home devices, all of which rely on discrete power management solutions. The competitive dynamics are intensifying, with semiconductor foundries investing heavily in next-generation fabrication technologies and expanding their capacity to meet soaring demand. Companies are focusing on vertical integration and strategic partnerships to secure supply chains and accelerate product development. The market penetration of advanced discrete semiconductor solutions in emerging economies is also on the rise, driven by government initiatives promoting industrialization and technological adoption. For example, the automotive sector's share of the discrete market is expected to reach 40% by 2025, a substantial increase from 30% in 2019, with the value of discrete components per EV reaching an average of USD 200 million. Similarly, the industrial segment is projected to account for 35% of the market, with an estimated market size of USD 15 million in 2025.

Dominant Markets & Segments in Semiconductor Discrete Chips Fabrication

The Automotive application segment is emerging as a dominant force in the Semiconductor Discrete Chips Fabrication market. This dominance is primarily fueled by the global shift towards electrification, with electric vehicles (EVs) requiring a significantly higher number of discrete power semiconductor components compared to their internal combustion engine (ICE) counterparts.

- Key Drivers for Automotive Dominance:

- EV Growth: The exponential rise in EV adoption worldwide, driven by environmental concerns, government incentives, and improving battery technology, necessitates advanced power electronics for efficient power conversion and battery management. This includes high-performance IGBT modules and MOSFETs for inverters, DC-DC converters, and onboard chargers. The market for automotive-grade discrete semiconductors is projected to reach USD 15 million by 2025.

- ADAS & Infotainment: The increasing integration of Advanced Driver-Assistance Systems (ADAS) and sophisticated infotainment systems in modern vehicles also increases the demand for various discrete components for power management and signal processing.

- Regulatory Mandates: Stringent emission regulations globally are pushing automakers to electrify their vehicle fleets, directly impacting the demand for discrete power semiconductors.

In terms of device types, MOSFET Wafer Foundry and IGBT Wafer Foundry services are experiencing the most significant traction.

- Dominance of MOSFET & IGBT Wafer Foundry:

- MOSFETs: Their versatility, high switching speeds, and ease of integration make them indispensable for a wide range of applications, from power supplies in consumer electronics to motor control in industrial machinery and power management in EVs. The global MOSFET market is expected to reach USD 10 million by 2025.

- IGBTs: Critical for high-power applications, IGBTs are the workhorses for applications like EV inverters, industrial motor drives, and renewable energy systems due to their superior voltage and current handling capabilities. The IGBT market is projected to reach USD 5 million by 2025, with a significant portion dedicated to wafer fabrication services.

- Technological Advancements: Continuous innovation in SiC MOSFETs and GaN power devices is further bolstering the demand for specialized wafer foundry services capable of manufacturing these next-generation components. Foundry capacity expansion for WBG devices is a critical industry trend.

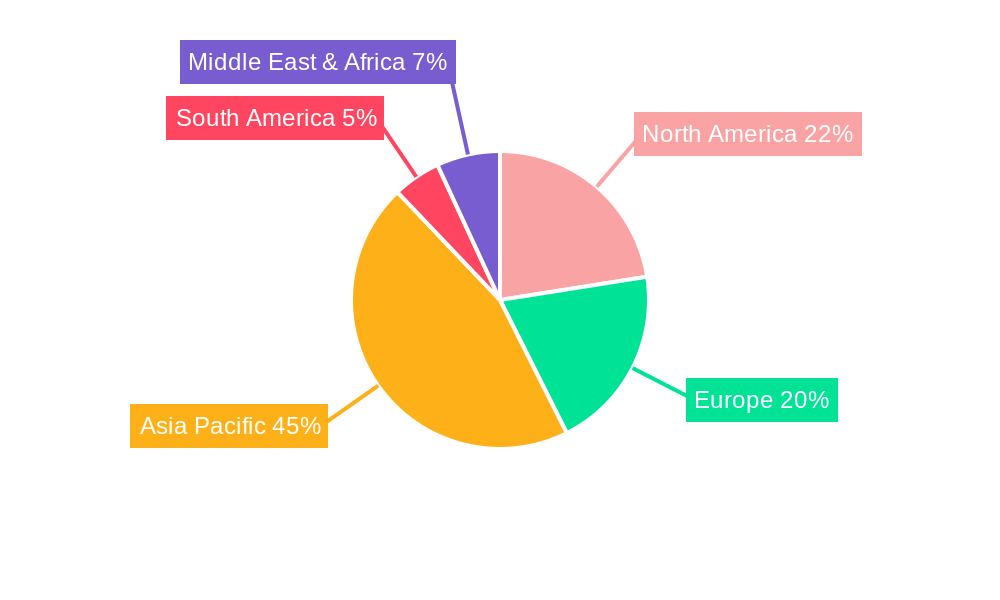

Geographically, Asia Pacific continues to be the largest and fastest-growing market for Semiconductor Discrete Chips Fabrication, driven by its strong manufacturing base, burgeoning automotive industry, and significant investments in industrial automation and consumer electronics. Countries like China, South Korea, Taiwan, and Japan are major hubs for both discrete chip manufacturing and consumption. The North America and Europe regions remain crucial for high-end automotive and industrial discrete semiconductor applications, particularly in advanced WBG device development and adoption. The overall market size for discrete chip fabrication services in 2025 is estimated to be USD 35 million.

Semiconductor Discrete Chips Fabrication Product Innovations

Recent product innovations in Semiconductor Discrete Chips Fabrication are revolutionizing performance and efficiency. The widespread adoption of wide-bandgap materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) is a key trend, enabling discrete devices to operate at higher voltages and temperatures with significantly reduced energy losses. These advancements are crucial for enhancing the efficiency of electric vehicles, industrial power supplies, and renewable energy inverters. Innovations in packaging technologies, such as advanced thermal management solutions and higher power density designs, are also critical for meeting the demands of compact and high-performance applications. The focus is on developing discrete semiconductor solutions that offer smaller footprints, improved reliability, and cost-effectiveness for mass adoption.

Report Segmentation & Scope

This report meticulously segments the Semiconductor Discrete Chips Fabrication market to provide granular insights into its diverse landscape. The segmentation is based on key application areas and device types, offering a comprehensive view of market dynamics and growth opportunities.

Application Segments:

- Automotive: Encompassing discrete semiconductors for EVs, ADAS, and traditional automotive systems. The projected market size for this segment in 2025 is USD 14 million.

- Industrial: Covering discrete components for automation, power grids, renewable energy, and heavy machinery. This segment is expected to reach USD 12 million in 2025.

- Consumer Electronics: Including discrete chips for home appliances, entertainment systems, and personal computing devices. The market size for this segment in 2025 is estimated at USD 5 million.

- UPS & Data Center: Focusing on discrete power solutions for uninterruptible power supplies and data center infrastructure. This segment's projected market size for 2025 is USD 3 million.

- Others: Encompassing emerging applications and niche markets. This segment is estimated at USD 1 million for 2025.

Device Type Segments:

- IGBT Wafer Foundry: Specialized fabrication of Insulated-Gate Bipolar Transistor wafers, crucial for high-power applications. Projected market size in 2025 is USD 7 million.

- MOSFET Wafer Foundry: Fabrication of Metal-Oxide-Semiconductor Field-Effect Transistor wafers, known for their versatility. The market size for this segment in 2025 is estimated at USD 15 million.

- Diode Wafer Foundry: Manufacturing of diode wafers for rectification and switching applications. This segment is projected to reach USD 5 million in 2025.

- BJT Wafer Foundry: Fabrication of Bipolar Junction Transistor wafers, used in amplification and switching. The market size for this segment in 2025 is estimated at USD 2 million.

- Others: Including specialized wafer types and emerging technologies. This segment is valued at USD 6 million for 2025.

Key Drivers of Semiconductor Discrete Chips Fabrication Growth

The Semiconductor Discrete Chips Fabrication market is propelled by several interconnected factors. The burgeoning electric vehicle (EV) revolution stands as a primary driver, demanding advanced power discrete semiconductor chips for efficient energy management and propulsion systems. This sector alone is projected to contribute USD 14 million to the market by 2025. Furthermore, the global push towards renewable energy sources, such as solar and wind power, necessitates robust IGBT and MOSFET components for power conversion and grid integration. Industrial automation, driven by the Industry 4.0 paradigm, requires sophisticated discrete semiconductor devices for motor control, robotics, and smart manufacturing processes, contributing an estimated USD 12 million to the market in 2025. Technological advancements in wide-bandgap materials like SiC and GaN offer higher efficiency and performance, accelerating their adoption across various applications. The increasing demand for energy-efficient consumer electronics also plays a crucial role.

Challenges in the Semiconductor Discrete Chips Fabrication Sector

Despite robust growth, the Semiconductor Discrete Chips Fabrication sector faces several significant challenges. Supply chain vulnerabilities, exacerbated by geopolitical tensions and natural disasters, pose a constant threat to production continuity and cost stability. Securing raw materials and managing lead times for specialized equipment remain critical concerns for discrete chip manufacturers. The high capital expenditure required for establishing and upgrading advanced semiconductor fabrication facilities, particularly for cutting-edge technologies like SiC and GaN, presents a substantial barrier to entry and expansion. Intense competition among leading semiconductor foundries and device manufacturers drives down profit margins, necessitating continuous innovation and cost optimization. Regulatory hurdles related to environmental compliance and evolving trade policies can also impact operational flexibility and market access. The estimated impact of supply chain disruptions on production schedules can range from 5% to 15%.

Leading Players in the Semiconductor Discrete Chips Fabrication Market

- STMicroelectronics

- Infineon

- Wolfspeed

- Rohm

- onsemi

- BYD Semiconductor

- Microchip (Microsemi)

- Mitsubishi Electric (Vincotech)

- Semikron Danfoss

- Fuji Electric

- Toshiba

- San'an Optoelectronics

- Littelfuse (IXYS)

- CETC 55

- Diodes Incorporated

- Vishay Intertechnology

- Zhuzhou CRRC Times Electric

- China Resources Microelectronics Limited

- Hangzhou Silan Microelectronics

- Jilin Sino-Microelectronics

- Nexperia

- Renesas Electronics

- Sanken Electric

- Magnachip

- Texas Instruments

- PANJIT Group

- VIS (Vanguard International Semiconductor)

- Hua Hong Semiconductor

- HLMC

- GTA Semiconductor Co.,Ltd.

- Tower Semiconductor

- PSMC

- DB HiTek

- United Nova Technology

- Beijing Yandong Microelectronics

- Wuhu Tus-Semiconductor

- CanSemi

- SiCamore Semi

- Polar Semiconductor, LLC

- SkyWater Technology

- SK keyfoundry Inc.

- X-Fab

- JS Foundry KK.

- LAPIS Semiconductor

- Episil Technology Inc.

- Global Power Technology

- Nanjing Quenergy Semiconductor

Key Developments in Semiconductor Discrete Chips Fabrication Sector

- 2023 Q4: Infineon announces expansion of its SiC manufacturing capacity, investing USD 500 million to meet soaring automotive and industrial demand.

- 2024 Q1: Wolfspeed inaugurates a new USD 1 billion GaN fabrication facility in North Carolina, significantly boosting its supply capabilities.

- 2024 Q2: STMicroelectronics launches a new generation of automotive-grade IGBT modules with enhanced thermal performance, valued at USD 50 million in R&D investment.

- 2024 Q3: BYD Semiconductor unveils a novel high-voltage SiC MOSFET, achieving breakthrough efficiency levels, estimated to capture 5% market share in its niche.

- 2024 Q4: Rohm partners with a major automotive OEM to co-develop advanced discrete solutions for future EV platforms.

- 2025 Q1: Onsemi acquires a specialized discrete chip foundry, expanding its wafer fabrication capabilities by 10% and valued at USD 300 million.

- 2025 Q2: China Resources Microelectronics Limited announces plans for a new IGBT wafer fabrication line, targeting a USD 100 million expansion.

Strategic Semiconductor Discrete Chips Fabrication Market Outlook

- 2023 Q4: Infineon announces expansion of its SiC manufacturing capacity, investing USD 500 million to meet soaring automotive and industrial demand.

- 2024 Q1: Wolfspeed inaugurates a new USD 1 billion GaN fabrication facility in North Carolina, significantly boosting its supply capabilities.

- 2024 Q2: STMicroelectronics launches a new generation of automotive-grade IGBT modules with enhanced thermal performance, valued at USD 50 million in R&D investment.

- 2024 Q3: BYD Semiconductor unveils a novel high-voltage SiC MOSFET, achieving breakthrough efficiency levels, estimated to capture 5% market share in its niche.

- 2024 Q4: Rohm partners with a major automotive OEM to co-develop advanced discrete solutions for future EV platforms.

- 2025 Q1: Onsemi acquires a specialized discrete chip foundry, expanding its wafer fabrication capabilities by 10% and valued at USD 300 million.

- 2025 Q2: China Resources Microelectronics Limited announces plans for a new IGBT wafer fabrication line, targeting a USD 100 million expansion.

Strategic Semiconductor Discrete Chips Fabrication Market Outlook

The strategic outlook for the Semiconductor Discrete Chips Fabrication market is exceptionally positive, characterized by sustained high demand and rapid technological evolution. The continued electrification of the automotive industry and the accelerated transition to renewable energy sources are foundational growth accelerators, ensuring a robust pipeline of demand for power discrete semiconductors. Innovations in wide-bandgap technologies (SiC and GaN) are creating new market opportunities for higher-performance and more efficient devices. Strategic investments in expanding foundry capacity, particularly for WBG materials, and fostering strong partnerships across the value chain will be crucial for market leaders. The integration of artificial intelligence (AI) and machine learning in process optimization and yield improvement offers further avenues for enhanced competitiveness. Companies that can effectively navigate supply chain complexities, invest in next-generation fabrication, and cater to the evolving needs of sectors like automotive and industrial are poised for significant growth and market leadership in the coming years. The market is projected to see continued expansion, with strategic opportunities in power electronics innovation valued at billions of dollars.

Semiconductor Discrete Chips Fabrication Segmentation

-

1. Application

- 1.1. Automotive

- 1.2. Industrial

- 1.3. Consumer Electronics

- 1.4. UPS & Data Center

- 1.5. Others

-

2. Types

- 2.1. IGBT Wafer Foundry

- 2.2. MOSFET Wafer Foundry

- 2.3. Diode Wafer Foundry

- 2.4. BJT Wafer Foundry

- 2.5. Others

Semiconductor Discrete Chips Fabrication Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Semiconductor Discrete Chips Fabrication REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.6% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Semiconductor Discrete Chips Fabrication Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive

- 5.1.2. Industrial

- 5.1.3. Consumer Electronics

- 5.1.4. UPS & Data Center

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. IGBT Wafer Foundry

- 5.2.2. MOSFET Wafer Foundry

- 5.2.3. Diode Wafer Foundry

- 5.2.4. BJT Wafer Foundry

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Semiconductor Discrete Chips Fabrication Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive

- 6.1.2. Industrial

- 6.1.3. Consumer Electronics

- 6.1.4. UPS & Data Center

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. IGBT Wafer Foundry

- 6.2.2. MOSFET Wafer Foundry

- 6.2.3. Diode Wafer Foundry

- 6.2.4. BJT Wafer Foundry

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Semiconductor Discrete Chips Fabrication Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive

- 7.1.2. Industrial

- 7.1.3. Consumer Electronics

- 7.1.4. UPS & Data Center

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. IGBT Wafer Foundry

- 7.2.2. MOSFET Wafer Foundry

- 7.2.3. Diode Wafer Foundry

- 7.2.4. BJT Wafer Foundry

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Semiconductor Discrete Chips Fabrication Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive

- 8.1.2. Industrial

- 8.1.3. Consumer Electronics

- 8.1.4. UPS & Data Center

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. IGBT Wafer Foundry

- 8.2.2. MOSFET Wafer Foundry

- 8.2.3. Diode Wafer Foundry

- 8.2.4. BJT Wafer Foundry

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Semiconductor Discrete Chips Fabrication Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive

- 9.1.2. Industrial

- 9.1.3. Consumer Electronics

- 9.1.4. UPS & Data Center

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. IGBT Wafer Foundry

- 9.2.2. MOSFET Wafer Foundry

- 9.2.3. Diode Wafer Foundry

- 9.2.4. BJT Wafer Foundry

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Semiconductor Discrete Chips Fabrication Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive

- 10.1.2. Industrial

- 10.1.3. Consumer Electronics

- 10.1.4. UPS & Data Center

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. IGBT Wafer Foundry

- 10.2.2. MOSFET Wafer Foundry

- 10.2.3. Diode Wafer Foundry

- 10.2.4. BJT Wafer Foundry

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 STMicroelectronics

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Infineon

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Wolfspeed

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Rohm

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 onsemi

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 BYD Semiconductor

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Microchip (Microsemi)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mitsubishi Electric (Vincotech)

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Semikron Danfoss

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Fuji Electric

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Toshiba

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 San'an Optoelectronics

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Littelfuse (IXYS)

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 CETC 55

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Diodes Incorporated

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Vishay Intertechnology

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Zhuzhou CRRC Times Electric

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 China Resources Microelectronics Limited

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Hangzhou Silan Microelectronics

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Jilin Sino-Microelectronics

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Nexperia

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Renesas Electronics

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Sanken Electric

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Magnachip

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Texas Instruments

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 PANJIT Group

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 VIS (Vanguard International Semiconductor)

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 Hua Hong Semiconductor

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 HLMC

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 GTA Semiconductor Co.

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 Ltd.

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.32 Tower Semiconductor

- 11.2.32.1. Overview

- 11.2.32.2. Products

- 11.2.32.3. SWOT Analysis

- 11.2.32.4. Recent Developments

- 11.2.32.5. Financials (Based on Availability)

- 11.2.33 PSMC

- 11.2.33.1. Overview

- 11.2.33.2. Products

- 11.2.33.3. SWOT Analysis

- 11.2.33.4. Recent Developments

- 11.2.33.5. Financials (Based on Availability)

- 11.2.34 DB HiTek

- 11.2.34.1. Overview

- 11.2.34.2. Products

- 11.2.34.3. SWOT Analysis

- 11.2.34.4. Recent Developments

- 11.2.34.5. Financials (Based on Availability)

- 11.2.35 United Nova Technology

- 11.2.35.1. Overview

- 11.2.35.2. Products

- 11.2.35.3. SWOT Analysis

- 11.2.35.4. Recent Developments

- 11.2.35.5. Financials (Based on Availability)

- 11.2.36 Beijing Yandong Microelectronics

- 11.2.36.1. Overview

- 11.2.36.2. Products

- 11.2.36.3. SWOT Analysis

- 11.2.36.4. Recent Developments

- 11.2.36.5. Financials (Based on Availability)

- 11.2.37 Wuhu Tus-Semiconductor

- 11.2.37.1. Overview

- 11.2.37.2. Products

- 11.2.37.3. SWOT Analysis

- 11.2.37.4. Recent Developments

- 11.2.37.5. Financials (Based on Availability)

- 11.2.38 CanSemi

- 11.2.38.1. Overview

- 11.2.38.2. Products

- 11.2.38.3. SWOT Analysis

- 11.2.38.4. Recent Developments

- 11.2.38.5. Financials (Based on Availability)

- 11.2.39 SiCamore Semi

- 11.2.39.1. Overview

- 11.2.39.2. Products

- 11.2.39.3. SWOT Analysis

- 11.2.39.4. Recent Developments

- 11.2.39.5. Financials (Based on Availability)

- 11.2.40 Polar Semiconductor

- 11.2.40.1. Overview

- 11.2.40.2. Products

- 11.2.40.3. SWOT Analysis

- 11.2.40.4. Recent Developments

- 11.2.40.5. Financials (Based on Availability)

- 11.2.41 LLC

- 11.2.41.1. Overview

- 11.2.41.2. Products

- 11.2.41.3. SWOT Analysis

- 11.2.41.4. Recent Developments

- 11.2.41.5. Financials (Based on Availability)

- 11.2.42 SkyWater Technology

- 11.2.42.1. Overview

- 11.2.42.2. Products

- 11.2.42.3. SWOT Analysis

- 11.2.42.4. Recent Developments

- 11.2.42.5. Financials (Based on Availability)

- 11.2.43 SK keyfoundry Inc.

- 11.2.43.1. Overview

- 11.2.43.2. Products

- 11.2.43.3. SWOT Analysis

- 11.2.43.4. Recent Developments

- 11.2.43.5. Financials (Based on Availability)

- 11.2.44 X-Fab

- 11.2.44.1. Overview

- 11.2.44.2. Products

- 11.2.44.3. SWOT Analysis

- 11.2.44.4. Recent Developments

- 11.2.44.5. Financials (Based on Availability)

- 11.2.45 JS Foundry KK.

- 11.2.45.1. Overview

- 11.2.45.2. Products

- 11.2.45.3. SWOT Analysis

- 11.2.45.4. Recent Developments

- 11.2.45.5. Financials (Based on Availability)

- 11.2.46 LAPIS Semiconductor

- 11.2.46.1. Overview

- 11.2.46.2. Products

- 11.2.46.3. SWOT Analysis

- 11.2.46.4. Recent Developments

- 11.2.46.5. Financials (Based on Availability)

- 11.2.47 Episil Technology Inc.

- 11.2.47.1. Overview

- 11.2.47.2. Products

- 11.2.47.3. SWOT Analysis

- 11.2.47.4. Recent Developments

- 11.2.47.5. Financials (Based on Availability)

- 11.2.48 Global Power Technology

- 11.2.48.1. Overview

- 11.2.48.2. Products

- 11.2.48.3. SWOT Analysis

- 11.2.48.4. Recent Developments

- 11.2.48.5. Financials (Based on Availability)

- 11.2.49 Nanjing Quenergy Semiconductor

- 11.2.49.1. Overview

- 11.2.49.2. Products

- 11.2.49.3. SWOT Analysis

- 11.2.49.4. Recent Developments

- 11.2.49.5. Financials (Based on Availability)

- 11.2.1 STMicroelectronics

List of Figures

- Figure 1: Global Semiconductor Discrete Chips Fabrication Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Semiconductor Discrete Chips Fabrication Revenue (million), by Application 2024 & 2032

- Figure 3: North America Semiconductor Discrete Chips Fabrication Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Semiconductor Discrete Chips Fabrication Revenue (million), by Types 2024 & 2032

- Figure 5: North America Semiconductor Discrete Chips Fabrication Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Semiconductor Discrete Chips Fabrication Revenue (million), by Country 2024 & 2032

- Figure 7: North America Semiconductor Discrete Chips Fabrication Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Semiconductor Discrete Chips Fabrication Revenue (million), by Application 2024 & 2032

- Figure 9: South America Semiconductor Discrete Chips Fabrication Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Semiconductor Discrete Chips Fabrication Revenue (million), by Types 2024 & 2032

- Figure 11: South America Semiconductor Discrete Chips Fabrication Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Semiconductor Discrete Chips Fabrication Revenue (million), by Country 2024 & 2032

- Figure 13: South America Semiconductor Discrete Chips Fabrication Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Semiconductor Discrete Chips Fabrication Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Semiconductor Discrete Chips Fabrication Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Semiconductor Discrete Chips Fabrication Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Semiconductor Discrete Chips Fabrication Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Semiconductor Discrete Chips Fabrication Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Semiconductor Discrete Chips Fabrication Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Semiconductor Discrete Chips Fabrication Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Semiconductor Discrete Chips Fabrication Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Semiconductor Discrete Chips Fabrication Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Semiconductor Discrete Chips Fabrication Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Semiconductor Discrete Chips Fabrication Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Semiconductor Discrete Chips Fabrication Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Semiconductor Discrete Chips Fabrication Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Semiconductor Discrete Chips Fabrication Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Discrete Chips Fabrication?

The projected CAGR is approximately 7.6%.

2. Which companies are prominent players in the Semiconductor Discrete Chips Fabrication?

Key companies in the market include STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, BYD Semiconductor, Microchip (Microsemi), Mitsubishi Electric (Vincotech), Semikron Danfoss, Fuji Electric, Toshiba, San'an Optoelectronics, Littelfuse (IXYS), CETC 55, Diodes Incorporated, Vishay Intertechnology, Zhuzhou CRRC Times Electric, China Resources Microelectronics Limited, Hangzhou Silan Microelectronics, Jilin Sino-Microelectronics, Nexperia, Renesas Electronics, Sanken Electric, Magnachip, Texas Instruments, PANJIT Group, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, GTA Semiconductor Co., Ltd., Tower Semiconductor, PSMC, DB HiTek, United Nova Technology, Beijing Yandong Microelectronics, Wuhu Tus-Semiconductor, CanSemi, SiCamore Semi, Polar Semiconductor, LLC, SkyWater Technology, SK keyfoundry Inc., X-Fab, JS Foundry KK., LAPIS Semiconductor, Episil Technology Inc., Global Power Technology, Nanjing Quenergy Semiconductor.

3. What are the main segments of the Semiconductor Discrete Chips Fabrication?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10230 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Discrete Chips Fabrication," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Discrete Chips Fabrication report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Discrete Chips Fabrication?

To stay informed about further developments, trends, and reports in the Semiconductor Discrete Chips Fabrication, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence