Key Insights

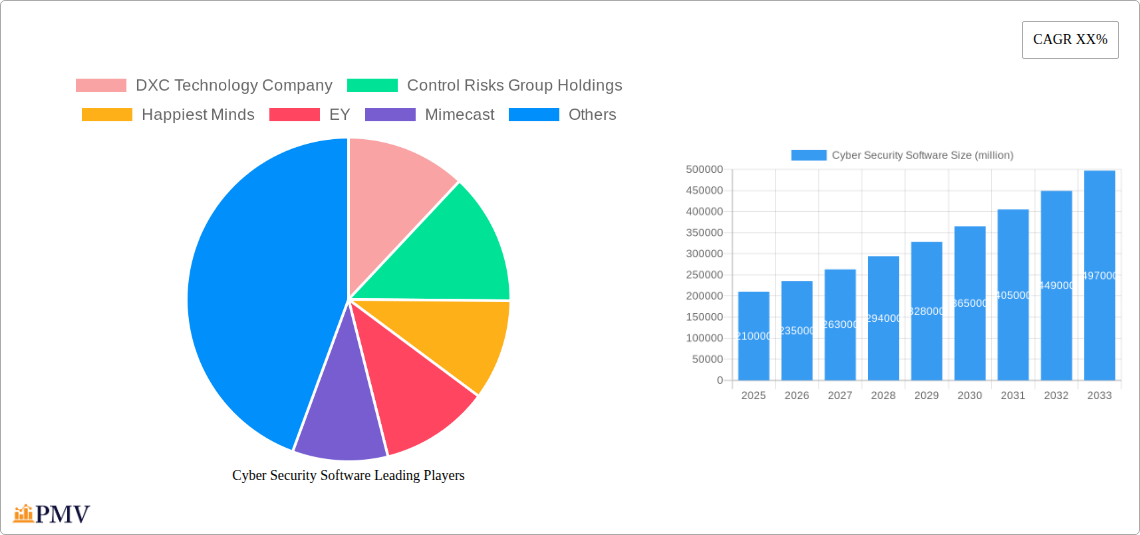

The global Cyber Security Software market is projected for robust expansion, poised to reach an estimated market size of approximately $210 billion in 2025. This growth is driven by the escalating sophistication and frequency of cyber threats, compelling organizations across all sectors to bolster their digital defenses. Key drivers include the pervasive adoption of cloud computing, the increasing prevalence of remote workforces, and the burgeoning Internet of Things (IoT) ecosystem, all of which present new attack vectors. Furthermore, stringent regulatory landscapes, such as GDPR and CCPA, are compelling businesses to invest in advanced cybersecurity solutions to ensure data privacy and compliance. The market's trajectory is further fueled by the continuous evolution of cyberattack techniques, necessitating constant innovation and upgrades in cybersecurity software capabilities. Industries like finance, healthcare, and government are leading the charge in adopting comprehensive cybersecurity solutions due to the sensitive nature of the data they handle.

The market is segmented into various applications, with "Household" and "Commercial" applications showing significant adoption, reflecting both individual and enterprise-level concerns. The "School" segment is also experiencing growth as educational institutions increasingly digitize their operations and student data. Within types, the "Advanced Version" and "Professional Version" are expected to dominate, catering to sophisticated threat landscapes and demanding enterprise requirements. Key players such as IBM Security, Cisco, Sophos, and BAE Systems are at the forefront, investing heavily in research and development to offer integrated and AI-powered cybersecurity platforms. However, the market faces restraints such as the escalating cost of implementation and maintenance, a persistent shortage of skilled cybersecurity professionals, and the challenge of keeping pace with rapidly evolving threats. Despite these challenges, the persistent need for robust threat detection, prevention, and response mechanisms ensures a strong and sustained growth outlook for the cyber security software market over the forecast period.

Gain unparalleled insights into the dynamic and rapidly evolving Cyber Security Software market. This in-depth report, covering the period from 2019 to 2033 with a base and estimated year of 2025 and a forecast period of 2025-2033, provides a robust analysis of market structure, competitive landscapes, emerging trends, dominant segments, and strategic outlook. Equip your business with the knowledge to navigate the complex threat landscape and capitalize on growth opportunities. Discover actionable intelligence essential for industry leaders, cybersecurity professionals, and strategic investors.

Cyber Security Software Market Structure & Competitive Dynamics

The global Cyber Security Software market is characterized by a moderate to high level of concentration, with a significant portion of the market share held by a few key players, alongside a vibrant ecosystem of innovative startups and specialized solution providers. The innovation ecosystem is a driving force, with continuous advancements in artificial intelligence (AI), machine learning (ML), and cloud-native security solutions. Regulatory frameworks such as GDPR, CCPA, and emerging cybersecurity mandates are increasingly shaping market dynamics, compelling organizations to invest in advanced protection. Product substitutes are present, ranging from in-house security teams to managed security services, but dedicated cyber security software offers specialized, scalable, and integrated solutions. End-user trends are heavily influenced by the escalating sophistication of cyber threats, the rise of remote work, and the expansion of the Internet of Things (IoT), all of which necessitate robust cybersecurity measures. Mergers and Acquisition (M&A) activities are a constant feature, aimed at consolidating market share, acquiring innovative technologies, and expanding service portfolios. For instance, M&A deals in the past have seen values in the range of hundreds of million to billions of dollars, reflecting strategic consolidation. Key players are continually acquiring smaller entities to bolster their offerings and competitive edge, leading to a dynamic market where strategic partnerships and acquisitions are critical for sustained growth. Market share analysis indicates that the top five players collectively hold an estimated 55% of the global market.

Cyber Security Software Industry Trends & Insights

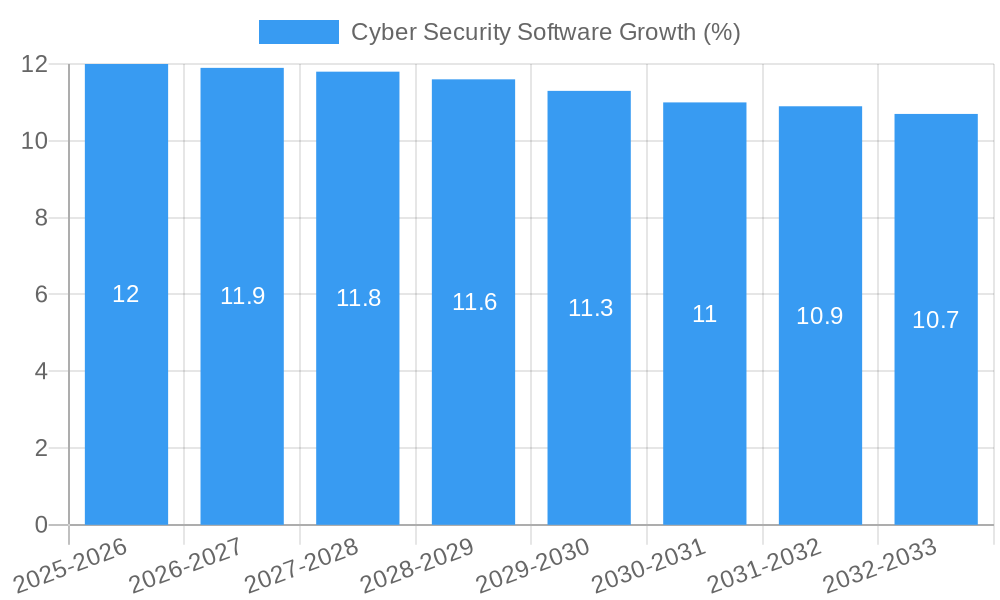

The Cyber Security Software industry is experiencing unprecedented growth, driven by a confluence of factors. The compound annual growth rate (CAGR) is projected to be a robust 12.5% over the forecast period, a testament to the escalating need for digital protection. Market penetration of advanced cyber security solutions is steadily increasing across all sectors, as organizations recognize the financial and reputational risks associated with breaches. Technological disruptions, particularly the rapid adoption of cloud computing, big data analytics, and AI, are creating new attack vectors and simultaneously empowering defensive capabilities. AI and ML are revolutionizing threat detection and response, enabling predictive analytics and automated remediation. The rise of sophisticated cybercrime, including ransomware attacks and advanced persistent threats (APTs), continues to be a primary market growth driver. Consumer preferences are shifting towards user-friendly, integrated security platforms that offer comprehensive protection without compromising performance. The competitive dynamics are intense, with established behemoths investing heavily in R&D and agile startups introducing disruptive innovations. The increasing frequency and severity of cyberattacks have led to a heightened awareness among businesses and individuals alike, fueling demand for robust and reliable cyber security software. Furthermore, the evolving regulatory landscape, mandating stringent data protection and privacy measures, compels organizations to adopt advanced software solutions. The remote work paradigm has also expanded the attack surface, necessitating advanced endpoint security and network monitoring tools. The growing adoption of BYOD (Bring Your Own Device) policies and the proliferation of IoT devices further amplify the need for comprehensive security solutions. The economic impact of cybercrime, estimated to cost economies billions of dollars annually, underscores the critical role of cyber security software in safeguarding digital assets and business continuity.

Dominant Markets & Segments in Cyber Security Software

The Commercial segment stands out as the dominant market within the Cyber Security Software landscape. This dominance is fueled by substantial IT budgets, a greater perceived threat surface due to extensive digital operations, and stricter regulatory compliance requirements for businesses. Economic policies that encourage digital transformation and cloud adoption inadvertently increase the reliance on robust cybersecurity measures. The infrastructure in the commercial sector, encompassing vast networks and sensitive data repositories, necessitates sophisticated protection.

- Commercial: This segment commands the largest market share, estimated at over 70% of the total market. Key drivers include the increasing complexity of business operations, the rise of cloud-based services, and the growing threat of data breaches and ransomware attacks targeting corporate assets. The need for compliance with industry-specific regulations (e.g., HIPAA in healthcare, PCI DSS in finance) further propels demand.

- School: While a growing segment, schools often operate with tighter budgets, leading to a greater reliance on more basic or bundled security solutions. However, the increasing digitalization of educational platforms and the growing concern for student data privacy are driving investments in advanced security. The market penetration here is estimated at around 15%.

- Household: This segment is characterized by individual user awareness and the need for personal data protection. While the adoption of advanced solutions is growing, budget constraints and a less sophisticated understanding of complex threats can limit market penetration, estimated at approximately 15%.

Within the Types of Cyber Security Software:

- Professional Version: This version, offering comprehensive feature sets and advanced capabilities, is the most dominant type, projected to capture over 50% of the market share. Its appeal lies in its ability to address complex enterprise-level security needs.

- Advanced Version: This mid-tier offering provides a balance of features and affordability, making it a strong contender and projected to hold around 30% of the market.

- Basic Version: Primarily aimed at smaller businesses or individuals with simpler needs, this version is expected to constitute around 20% of the market.

Cyber Security Software Product Innovations

Recent cyber security software product innovations are centered on proactive threat intelligence, AI-driven anomaly detection, and automated incident response. Companies are developing solutions that offer predictive analytics to anticipate and neutralize threats before they impact systems, a significant competitive advantage. Zero-trust architectures and cloud-native security platforms are gaining traction, providing enhanced visibility and control in complex hybrid environments. The integration of behavioral analytics allows software to identify unusual patterns indicative of compromise, moving beyond signature-based detection. These advancements cater to the growing demand for more intelligent, adaptive, and efficient cybersecurity solutions that minimize human intervention while maximizing protection against sophisticated cyber threats.

Report Segmentation & Scope

This report meticulously segments the Cyber Security Software market to provide granular insights. The segmentation includes:

Application:

- Household: This segment encompasses security solutions tailored for individual users and home networks. It includes antivirus, personal firewalls, and VPNs, with an estimated market size of $500 million and a projected CAGR of 9%.

- School: This segment covers security needs for educational institutions, including endpoint protection, network security, and data privacy solutions for student information. It's projected to reach $1.2 billion with a CAGR of 11%.

- Commercial: This is the largest segment, focusing on businesses of all sizes. It includes enterprise-grade security solutions, threat intelligence platforms, and compliance management tools, estimated at $15 billion with a CAGR of 13%.

Types:

- Basic Version: Entry-level solutions offering fundamental protection. Projected market size of $2 billion with a 7% CAGR.

- Advanced Version: Mid-tier solutions with enhanced features for small to medium-sized businesses. Projected market size of $5 billion with a 12% CAGR.

- Professional Version: Comprehensive, enterprise-level solutions with advanced functionalities. Projected market size of $10 billion with a 14% CAGR.

Key Drivers of Cyber Security Software Growth

The growth of the Cyber Security Software sector is primarily driven by the escalating sophistication and frequency of cyber threats, including ransomware, phishing, and advanced persistent threats. The increasing digitalization of businesses and everyday life, coupled with the widespread adoption of cloud computing and IoT devices, expands the attack surface, creating a continuous demand for enhanced security. Furthermore, stringent data privacy regulations like GDPR and CCPA impose significant compliance obligations, forcing organizations to invest in robust security software. The economic imperative to protect sensitive data, intellectual property, and operational continuity from costly breaches also serves as a powerful growth catalyst.

Challenges in the Cyber Security Software Sector

Despite robust growth, the Cyber Security Software sector faces significant challenges. The ever-evolving nature of cyber threats necessitates constant innovation and adaptation, posing a substantial R&D burden. Talent shortages in skilled cybersecurity professionals limit the ability of companies to develop, implement, and manage advanced solutions. The complexity of integration with existing IT infrastructures can be a barrier for some organizations. Moreover, price sensitivity and budget constraints, particularly in smaller businesses and emerging markets, can hinder the adoption of premium security software. Regulatory compliance fatigue and the ever-changing landscape of legal requirements add another layer of complexity for software providers.

Leading Players in the Cyber Security Software Market

- DXC Technology Company

- Control Risks Group Holdings

- Happiest Minds

- EY

- Mimecast

- Lockheed Martin

- Sophos

- Symantec

- Sera-Brynn

- Clearwater Compliance

- IBM Security

- Cisco

- Raytheon Cyber

- BAE Systems

- Digital Defense

- Rapid7

Key Developments in Cyber Security Software Sector

- 2023/Q3: Launch of AI-powered threat intelligence platforms by IBM Security, enhancing proactive threat detection.

- 2023/Q4: Mimecast announces strategic acquisition of a cloud security startup for an undisclosed sum to bolster its email security offerings.

- 2024/Q1: Sophos releases new endpoint detection and response (EDR) capabilities, integrating machine learning for advanced malware protection.

- 2024/Q2: Cisco unveils a comprehensive cloud security suite aimed at securing hybrid work environments, responding to evolving IT landscapes.

- 2024/Q3: Symantec (now Broadcom) expands its managed detection and response (MDR) services, leveraging automation for faster incident remediation.

Strategic Cyber Security Software Market Outlook

- 2023/Q3: Launch of AI-powered threat intelligence platforms by IBM Security, enhancing proactive threat detection.

- 2023/Q4: Mimecast announces strategic acquisition of a cloud security startup for an undisclosed sum to bolster its email security offerings.

- 2024/Q1: Sophos releases new endpoint detection and response (EDR) capabilities, integrating machine learning for advanced malware protection.

- 2024/Q2: Cisco unveils a comprehensive cloud security suite aimed at securing hybrid work environments, responding to evolving IT landscapes.

- 2024/Q3: Symantec (now Broadcom) expands its managed detection and response (MDR) services, leveraging automation for faster incident remediation.

Strategic Cyber Security Software Market Outlook

The strategic outlook for the Cyber Security Software market remains exceptionally bright. Growth accelerators include the continued surge in cloud adoption, the proliferation of IoT devices, and the increasing adoption of AI and ML for both offensive and defensive cybersecurity operations. Emerging markets present significant untapped potential as digital transformation accelerates globally. Strategic opportunities lie in developing specialized solutions for niche industries, enhancing integrated security platforms, and focusing on user-friendly interfaces that cater to a wider audience. The ongoing arms race between cybercriminals and defenders ensures a perpetual demand for innovative and effective cybersecurity software, positioning the market for sustained and robust expansion.

Cyber Security Software Segmentation

-

1. Application

- 1.1. Household

- 1.2. School

- 1.3. Commercial

-

2. Types

- 2.1. Basic Version

- 2.2. Advanced Version

- 2.3. Professional Version

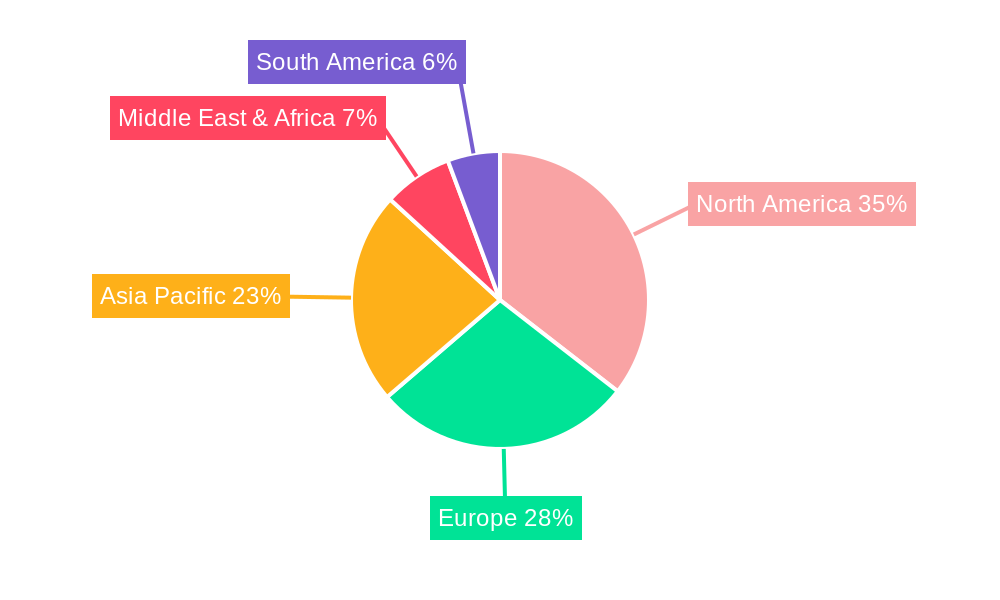

Cyber Security Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cyber Security Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cyber Security Software Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. School

- 5.1.3. Commercial

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Basic Version

- 5.2.2. Advanced Version

- 5.2.3. Professional Version

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cyber Security Software Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. School

- 6.1.3. Commercial

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Basic Version

- 6.2.2. Advanced Version

- 6.2.3. Professional Version

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cyber Security Software Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. School

- 7.1.3. Commercial

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Basic Version

- 7.2.2. Advanced Version

- 7.2.3. Professional Version

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cyber Security Software Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. School

- 8.1.3. Commercial

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Basic Version

- 8.2.2. Advanced Version

- 8.2.3. Professional Version

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cyber Security Software Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. School

- 9.1.3. Commercial

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Basic Version

- 9.2.2. Advanced Version

- 9.2.3. Professional Version

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cyber Security Software Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. School

- 10.1.3. Commercial

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Basic Version

- 10.2.2. Advanced Version

- 10.2.3. Professional Version

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 DXC Technology Company

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Control Risks Group Holdings

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Happiest Minds

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 EY

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Mimecast

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 DXC Technology Company

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Lockheed Martin

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sophos

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Symantec

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sera-Brynn

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Clearwater Compliance

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 IBM Security

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Cisco

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Raytheon Cyber

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 BAE Systems

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Digital Defense

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Rapid7

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 DXC Technology Company

List of Figures

- Figure 1: Global Cyber Security Software Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Cyber Security Software Revenue (million), by Application 2024 & 2032

- Figure 3: North America Cyber Security Software Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Cyber Security Software Revenue (million), by Types 2024 & 2032

- Figure 5: North America Cyber Security Software Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Cyber Security Software Revenue (million), by Country 2024 & 2032

- Figure 7: North America Cyber Security Software Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Cyber Security Software Revenue (million), by Application 2024 & 2032

- Figure 9: South America Cyber Security Software Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Cyber Security Software Revenue (million), by Types 2024 & 2032

- Figure 11: South America Cyber Security Software Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Cyber Security Software Revenue (million), by Country 2024 & 2032

- Figure 13: South America Cyber Security Software Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Cyber Security Software Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Cyber Security Software Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Cyber Security Software Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Cyber Security Software Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Cyber Security Software Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Cyber Security Software Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Cyber Security Software Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Cyber Security Software Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Cyber Security Software Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Cyber Security Software Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Cyber Security Software Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Cyber Security Software Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Cyber Security Software Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Cyber Security Software Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Cyber Security Software Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Cyber Security Software Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Cyber Security Software Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Cyber Security Software Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Cyber Security Software Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Cyber Security Software Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Cyber Security Software Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Cyber Security Software Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Cyber Security Software Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Cyber Security Software Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Cyber Security Software Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Cyber Security Software Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Cyber Security Software Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Cyber Security Software Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Cyber Security Software Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Cyber Security Software Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Cyber Security Software Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Cyber Security Software Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Cyber Security Software Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Cyber Security Software Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Cyber Security Software Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Cyber Security Software Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Cyber Security Software Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Cyber Security Software Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cyber Security Software?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Cyber Security Software?

Key companies in the market include DXC Technology Company, Control Risks Group Holdings, Happiest Minds, EY, Mimecast, DXC Technology Company, Lockheed Martin, Sophos, Symantec, Sera-Brynn, Clearwater Compliance, IBM Security, Cisco, Raytheon Cyber, BAE Systems, Digital Defense, Rapid7.

3. What are the main segments of the Cyber Security Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cyber Security Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cyber Security Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cyber Security Software?

To stay informed about further developments, trends, and reports in the Cyber Security Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence