Key Insights

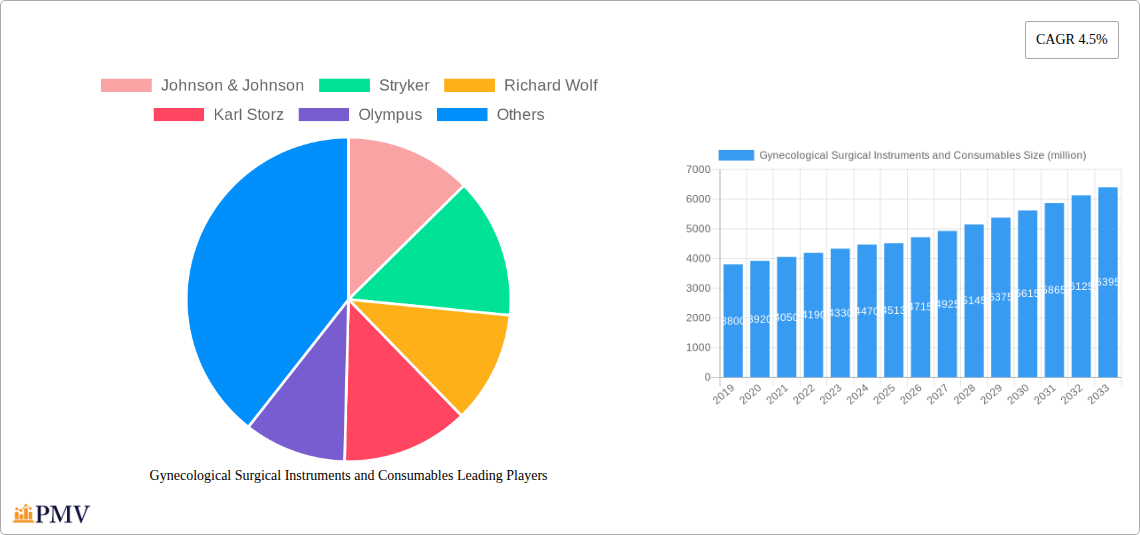

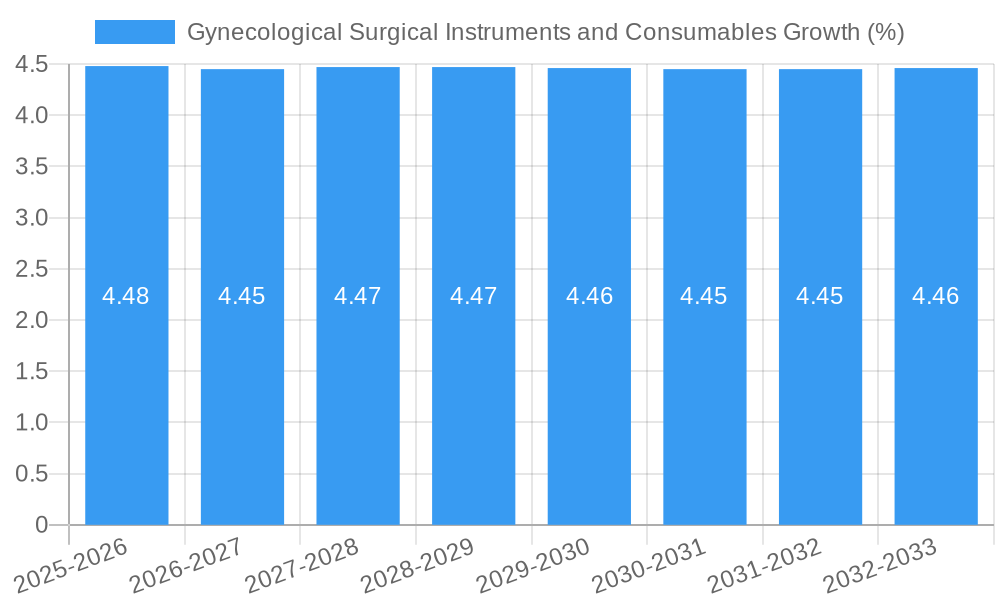

The global Gynecological Surgical Instruments and Consumables market is poised for robust growth, with an estimated market size of approximately USD 4,513 million in 2025. This expansion is driven by a confluence of factors, including the increasing prevalence of gynecological disorders, rising awareness among women regarding reproductive health, and advancements in minimally invasive surgical techniques. The market is projected to witness a Compound Annual Growth Rate (CAGR) of 4.5% from 2025 to 2033, signifying sustained demand for innovative and effective solutions. Key drivers contributing to this growth include a growing aging population susceptible to gynecological conditions, the continuous development of sophisticated instruments, and an increasing preference for less invasive procedures that offer faster recovery times and reduced complications. The market's expansion is further bolstered by a growing emphasis on women's health initiatives and improved healthcare infrastructure in developing regions.

The market can be segmented into Instruments and Consumables, with both segments experiencing significant demand. Within applications, Hospitals and Clinics represent the primary end-users, reflecting the centralized nature of advanced gynecological care. Key trends shaping the market landscape include the adoption of robotic-assisted surgery, the development of single-use disposable instruments to enhance patient safety and reduce infection risks, and the integration of advanced imaging technologies for improved surgical precision. While the market enjoys strong growth prospects, certain restraints, such as the high cost of advanced surgical equipment and the need for specialized training for healthcare professionals, could temper the pace of adoption in some regions. However, the overall outlook remains highly positive, with major players like Johnson & Johnson, Stryker, and Karl Storz actively investing in research and development to meet the evolving needs of gynecological care worldwide.

Comprehensive Gynecological Surgical Instruments and Consumables Market Report

This in-depth report provides a definitive analysis of the global gynecological surgical instruments and consumables market. Covering the historical period from 2019 to 2024, a base year of 2025, and a forecast period extending to 2033, this study offers unparalleled insights into market dynamics, growth trajectories, and competitive landscapes. We meticulously examine key segments, product innovations, and the strategic imperatives shaping the future of women's healthcare instrumentation. The projected market size is estimated to reach over $XX million by 2033, driven by a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period.

Gynecological Surgical Instruments and Consumables Market Structure & Competitive Dynamics

The gynecological surgical instruments and consumables market exhibits a moderately concentrated structure, with key players like Johnson & Johnson, Stryker, Richard Wolf, Karl Storz, and Olympus holding significant market shares. Innovation ecosystems are robust, driven by continuous research and development in minimally invasive surgical techniques and advanced diagnostic tools. Regulatory frameworks, including FDA and EMA approvals, play a crucial role in market entry and product dissemination. Product substitutes, while present, are often limited in their efficacy for complex gynecological procedures. End-user trends lean towards increased adoption of hysteroscopy, laparoscopy, and advanced pelvic reconstructive surgeries, demanding sophisticated and reliable instrumentation. Mergers and acquisitions (M&A) activities are strategically employed to expand product portfolios and geographical reach. Notable M&A deals in the historical period accounted for an estimated $XXX million in transaction values, indicating consolidation efforts.

- Market Concentration: Moderately concentrated with dominant global players.

- Innovation Ecosystems: Strong emphasis on R&D for minimally invasive and advanced techniques.

- Regulatory Frameworks: Strict compliance with global health authorities is paramount.

- Product Substitutes: Limited impact on specialized gynecological procedures.

- End-User Trends: Growing demand for minimally invasive procedures.

- M&A Activities: Strategic for portfolio expansion and market consolidation.

Gynecological Surgical Instruments and Consumables Industry Trends & Insights

The gynecological surgical instruments and consumables market is experiencing robust growth, fueled by a confluence of factors including increasing awareness of women's health, rising incidence of gynecological disorders such as uterine fibroids and ovarian cysts, and the global surge in aging populations who are more susceptible to these conditions. The technological advancement in surgical tools, particularly the widespread adoption of minimally invasive surgical techniques like laparoscopy and hysteroscopy, is a significant market driver. These procedures offer reduced patient recovery times, lower complication rates, and improved cosmetic outcomes, thereby enhancing patient satisfaction and surgeon preference. The market penetration of advanced diagnostic and therapeutic instruments is expanding, as healthcare providers increasingly invest in state-of-the-art technology to improve patient care and procedural efficiency.

The growing demand for single-use consumables, driven by infection control protocols and the need for consistent performance, is another key trend. Companies are investing heavily in the development of advanced biocompatible materials and innovative designs for consumables, ranging from specialized surgical meshes and sutures to advanced visualization systems and electrosurgical devices. The telehealth and remote surgery trend, though nascent in gynecology, presents a long-term growth opportunity, potentially increasing the reach of specialized surgical expertise. Furthermore, government initiatives promoting women's health and improved access to healthcare services in emerging economies are creating new market opportunities. The competitive landscape is dynamic, characterized by product innovation, strategic partnerships, and a focus on cost-effectiveness without compromising quality. The CAGR is projected to remain strong at XX% during the forecast period, with market penetration expected to reach over XX% by 2033.

Dominant Markets & Segments in Gynecological Surgical Instruments and Consumables

The gynecological surgical instruments and consumables market is significantly influenced by the dominance of the Hospital application segment. Hospitals, equipped with advanced surgical infrastructure and serving a larger patient volume, represent the primary end-users for a wide array of gynecological surgical instruments and consumables. This segment is driven by factors such as greater access to funding for capital equipment, the presence of specialized gynecological departments, and the increasing complexity of procedures performed within hospital settings. The Instruments type segment also holds a dominant position, encompassing sophisticated devices like hysteroscopes, laparoscopes, surgical robots, electrosurgical units, and diagnostic imaging equipment, all crucial for modern gynecological surgery.

- Dominant Application: Hospital

- Drivers: Comprehensive surgical facilities, higher patient throughput, access to advanced technology.

- Economic Policies: Government investments in healthcare infrastructure and public hospitals.

- Infrastructure: Well-established operating rooms and specialized units.

- Technological Adoption: Early and widespread adoption of advanced surgical systems.

- Dominant Type: Instruments

- Drivers: Necessity for complex diagnostic and therapeutic interventions.

- Innovation: Continuous development of minimally invasive and robotic surgical instruments.

- Surgeon Preference: Growing preference for precise and efficient instruments.

- Market Size: Historically accounts for a larger share due to the high cost of advanced instrumentation.

While Clinics represent a growing segment, particularly for routine procedures and diagnostic services, the breadth and complexity of surgical interventions performed in hospitals solidify its leading position. The Other application segment, which may include specialized surgical centers or outpatient facilities, contributes to market diversity but lags behind hospitals in overall market share. Within the Types segmentation, Consumables, while crucial and experiencing steady growth, are generally outpaced by the upfront investment required for sophisticated instruments. The market penetration in hospitals for advanced instruments is estimated to be over XX%, driving overall market dominance.

Gynecological Surgical Instruments and Consumables Product Innovations

Product innovations in the gynecological surgical instruments and consumables market are heavily focused on enhancing precision, miniaturization, and patient safety. The development of advanced hysteroscopes with enhanced visualization, including 4K imaging and augmented reality capabilities, is revolutionizing intrauterine diagnostics and interventions. Furthermore, the integration of artificial intelligence (AI) into surgical planning and execution is a significant trend, promising improved outcomes. Novel biomaterials are being developed for gynecological meshes and sutures, offering superior biocompatibility and reduced infection rates. The introduction of single-use, sterile instrument sets also caters to increasing infection control demands. These innovations offer competitive advantages by improving procedural efficiency, reducing patient trauma, and expanding the scope of minimally invasive treatments.

Report Segmentation & Scope

This report segmentations provide a granular view of the gynecological surgical instruments and consumables market. The Application segment is divided into: Hospital, representing the largest market share due to advanced infrastructure and higher patient volumes; Clinic, a growing segment for routine procedures and diagnostics; and Other, encompassing specialized surgical centers. The Types segment includes: Instruments, comprising sophisticated surgical devices and equipment; and Consumables, covering disposable items like sutures, meshes, and surgical disposables. Projections indicate that the Hospital segment will continue to dominate, with an estimated market size of over $XX million by 2033. The Instruments segment is expected to grow at a CAGR of XX%, while Consumables will see a CAGR of XX%. Competitive dynamics within each segment are driven by technological advancements and specific end-user needs.

Key Drivers of Gynecological Surgical Instruments and Consumables Growth

The gynecological surgical instruments and consumables market is propelled by several key drivers. Technologically, the relentless advancement in minimally invasive surgical techniques, including laparoscopy and hysteroscopy, necessitates sophisticated instruments and specialized consumables. Economically, increasing healthcare expenditure globally, coupled with rising disposable incomes in emerging economies, enhances the affordability and accessibility of these procedures. Regulatory bodies, while stringent, are also facilitating market growth by approving innovative technologies that improve patient outcomes. Specific examples include the widespread adoption of robotic-assisted surgery for complex gynecological procedures, which significantly boosts the demand for specialized instruments and integrated consumables. Furthermore, the growing awareness and focus on women's health issues are leading to increased demand for diagnostic and therapeutic interventions.

Challenges in the Gynecological Surgical Instruments and Consumables Sector

Despite robust growth, the gynecological surgical instruments and consumables sector faces several challenges. High initial investment costs for advanced surgical equipment can be a significant barrier for smaller healthcare facilities, particularly in resource-constrained regions. Stringent regulatory approval processes in various countries can lead to prolonged product launch timelines and increased R&D expenses. Supply chain disruptions, as witnessed in recent global events, can impact the availability and cost of critical raw materials and finished products. Intense competition from both established players and emerging manufacturers also pressures profit margins, necessitating continuous innovation and cost optimization. The adoption rate of new technologies can also be hindered by surgeon training requirements and resistance to change.

Leading Players in the Gynecological Surgical Instruments and Consumables Market

- Johnson & Johnson

- Stryker

- Richard Wolf

- Karl Storz

- Olympus

- Hologic

- Medtronic

- Boston Scientific

- CooperSurgical

- PFM Medical

- Herniamesh

- Hangzhou Kangji Medical

- Zhejiang Tiansong Medical Instrument

Key Developments in Gynecological Surgical Instruments and Consumables Sector

- 2023 (Q4): Olympus launches a new generation of advanced hysteroscopes with enhanced imaging capabilities, improving diagnostic accuracy.

- 2024 (Q1): Stryker announces a strategic partnership with a leading AI company to integrate AI-driven analytics into its surgical platforms, aiming to optimize gynecological procedures.

- 2024 (Q2): Hologic expands its minimally invasive surgical portfolio with the acquisition of a smaller competitor specializing in laparoscopic instruments, valued at approximately $XX million.

- 2024 (Q3): Karl Storz introduces a new range of reusable and single-use consumables designed for enhanced ergonomics and safety in complex laparoscopic surgeries.

- 2024 (Q4): Boston Scientific receives FDA clearance for a novel uterine fibroid ablation device, expanding its interventional gynecology offerings.

Strategic Gynecological Surgical Instruments and Consumables Market Outlook

The strategic outlook for the gynecological surgical instruments and consumables market is highly promising, driven by an accelerating shift towards value-based healthcare and personalized medicine. Key growth accelerators include the continued global embrace of minimally invasive techniques, the integration of AI and robotics to enhance surgical precision, and the development of advanced biomaterials for improved patient outcomes. Strategic opportunities lie in expanding market reach in emerging economies through localized manufacturing and distribution, as well as focusing on niche segments like advanced oncology surgery. Partnerships and collaborations with academic institutions for clinical research and product validation will further solidify market positions. The market is poised for sustained growth, with a strong emphasis on innovation that addresses unmet clinical needs and improves the overall quality of life for women.

Gynecological Surgical Instruments and Consumables Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Other

-

2. Types

- 2.1. Instruments

- 2.2. Consumables

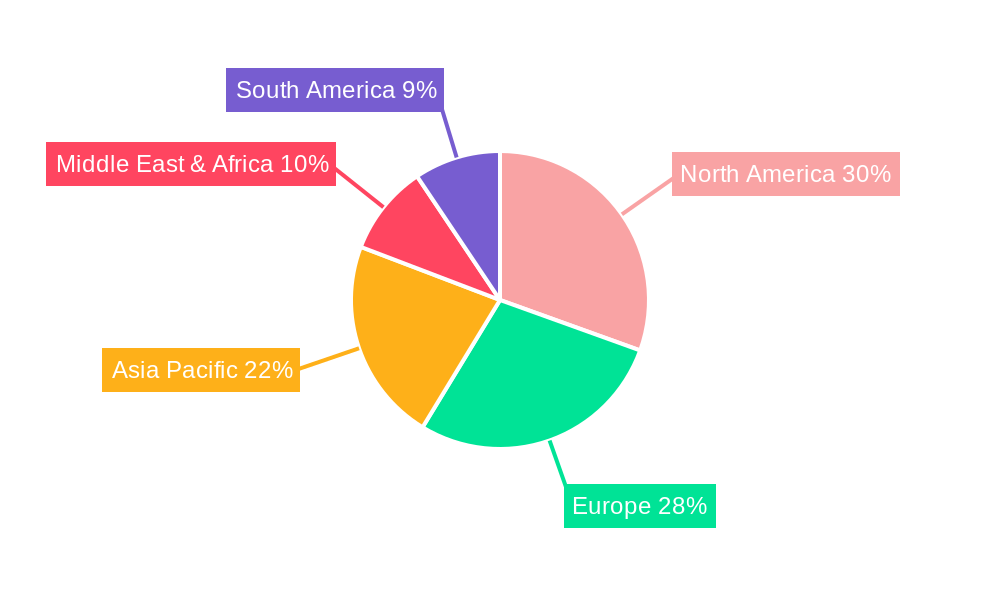

Gynecological Surgical Instruments and Consumables Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Gynecological Surgical Instruments and Consumables REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.5% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Gynecological Surgical Instruments and Consumables Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Instruments

- 5.2.2. Consumables

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Gynecological Surgical Instruments and Consumables Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Instruments

- 6.2.2. Consumables

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Gynecological Surgical Instruments and Consumables Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Instruments

- 7.2.2. Consumables

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Gynecological Surgical Instruments and Consumables Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Instruments

- 8.2.2. Consumables

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Gynecological Surgical Instruments and Consumables Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Instruments

- 9.2.2. Consumables

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Gynecological Surgical Instruments and Consumables Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Instruments

- 10.2.2. Consumables

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Johnson & Johnson

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Stryker

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Richard Wolf

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Karl Storz

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Olympus

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hologic

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Medtronic

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Boston Scientific

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 CooperSurgical

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 PFM Medical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Herniamesh

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Hangzhou Kangji Medical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Zhejiang Tiansong Medical Instrument

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Johnson & Johnson

List of Figures

- Figure 1: Global Gynecological Surgical Instruments and Consumables Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Gynecological Surgical Instruments and Consumables Revenue (million), by Application 2024 & 2032

- Figure 3: North America Gynecological Surgical Instruments and Consumables Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Gynecological Surgical Instruments and Consumables Revenue (million), by Types 2024 & 2032

- Figure 5: North America Gynecological Surgical Instruments and Consumables Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Gynecological Surgical Instruments and Consumables Revenue (million), by Country 2024 & 2032

- Figure 7: North America Gynecological Surgical Instruments and Consumables Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Gynecological Surgical Instruments and Consumables Revenue (million), by Application 2024 & 2032

- Figure 9: South America Gynecological Surgical Instruments and Consumables Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Gynecological Surgical Instruments and Consumables Revenue (million), by Types 2024 & 2032

- Figure 11: South America Gynecological Surgical Instruments and Consumables Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Gynecological Surgical Instruments and Consumables Revenue (million), by Country 2024 & 2032

- Figure 13: South America Gynecological Surgical Instruments and Consumables Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Gynecological Surgical Instruments and Consumables Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Gynecological Surgical Instruments and Consumables Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Gynecological Surgical Instruments and Consumables Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Gynecological Surgical Instruments and Consumables Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Gynecological Surgical Instruments and Consumables Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Gynecological Surgical Instruments and Consumables Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Gynecological Surgical Instruments and Consumables Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Gynecological Surgical Instruments and Consumables Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Gynecological Surgical Instruments and Consumables Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Gynecological Surgical Instruments and Consumables Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Gynecological Surgical Instruments and Consumables Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Gynecological Surgical Instruments and Consumables Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Gynecological Surgical Instruments and Consumables Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Gynecological Surgical Instruments and Consumables Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gynecological Surgical Instruments and Consumables?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Gynecological Surgical Instruments and Consumables?

Key companies in the market include Johnson & Johnson, Stryker, Richard Wolf, Karl Storz, Olympus, Hologic, Medtronic, Boston Scientific, CooperSurgical, PFM Medical, Herniamesh, Hangzhou Kangji Medical, Zhejiang Tiansong Medical Instrument.

3. What are the main segments of the Gynecological Surgical Instruments and Consumables?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 4513 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gynecological Surgical Instruments and Consumables," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gynecological Surgical Instruments and Consumables report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gynecological Surgical Instruments and Consumables?

To stay informed about further developments, trends, and reports in the Gynecological Surgical Instruments and Consumables, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence