Key Insights

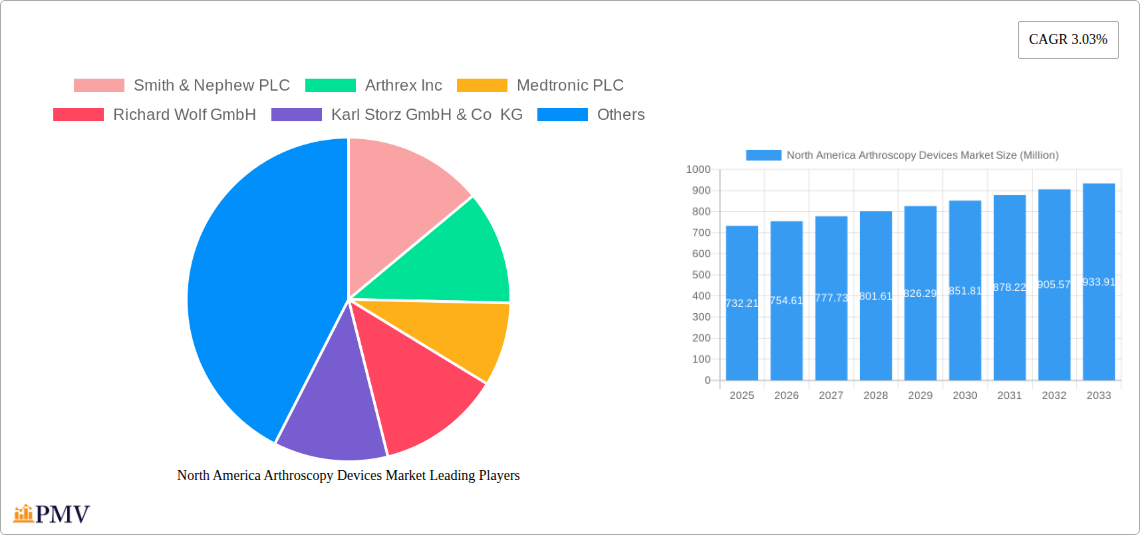

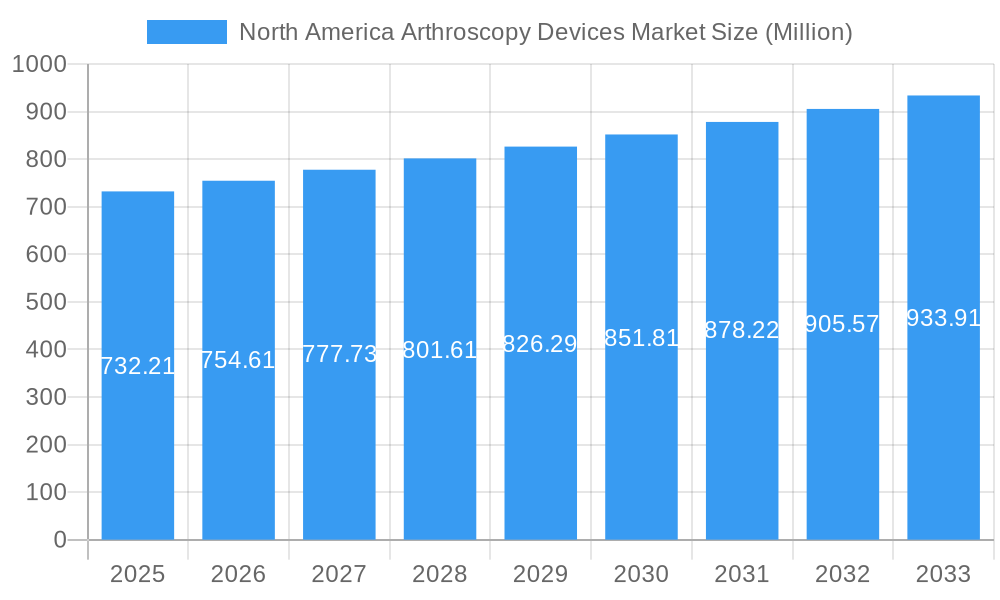

The North America Arthroscopy Devices Market is poised for steady expansion, projected to reach USD 732.21 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 3.03% from 2019 to 2033. This growth is underpinned by increasing prevalence of orthopedic conditions, a rising geriatric population prone to joint ailments, and a growing demand for minimally invasive surgical procedures. Arthroscopy, offering reduced recovery times and improved patient outcomes compared to traditional open surgery, is a key driver for this market. Technological advancements in arthroscopic instruments, such as enhanced visualization systems, sophisticated fluid management, and innovative implants, are further propelling market adoption. The Knee Arthroscopy segment is expected to dominate, driven by the high incidence of sports-related injuries and degenerative knee conditions like osteoarthritis. Similarly, Hip Arthroscopy is gaining traction for treating impingement syndromes and labral tears, reflecting a shift towards earlier intervention for joint pain. The Spine Arthroscopy segment, though nascent, holds significant future potential due to its ability to address complex spinal issues with minimal disruption.

North America Arthroscopy Devices Market Market Size (In Million)

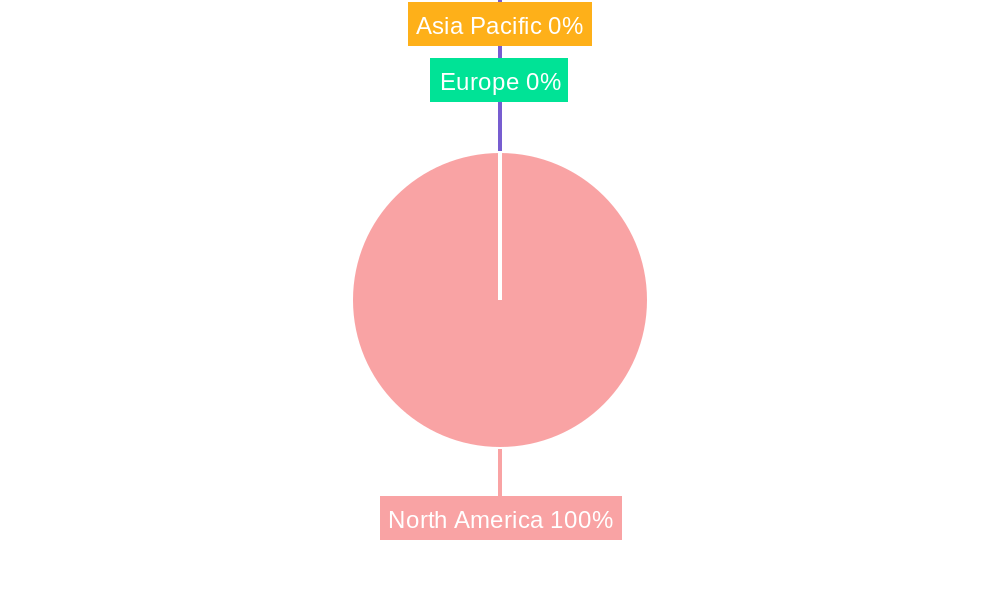

Geographically, the United States leads the North America market, attributed to its advanced healthcare infrastructure, high disposable incomes, and significant investment in orthopedic research and development. Canada and Mexico also contribute to market growth, driven by expanding healthcare access and increasing adoption of advanced medical technologies. Key players like Smith & Nephew PLC, Arthrex Inc., and Medtronic PLC are at the forefront of innovation, actively investing in R&D and strategic collaborations to expand their product portfolios and market reach. The market is also characterized by a strong emphasis on developing user-friendly and cost-effective arthroscopic solutions to cater to a wider patient demographic. While the market demonstrates robust growth, factors such as the high cost of advanced arthroscopic equipment and the availability of non-surgical treatment alternatives present potential restraints. However, the sustained demand for effective joint repair and the ongoing innovation within the field strongly indicate a positive trajectory for the North America Arthroscopy Devices Market in the coming years.

North America Arthroscopy Devices Market Company Market Share

Here's the SEO-optimized, detailed report description for the North America Arthroscopy Devices Market:

North America Arthroscopy Devices Market: Growth Drivers, Emerging Technologies, and Competitive Landscape (2019–2033)

This comprehensive report delves into the dynamic North America Arthroscopy Devices Market, providing in-depth analysis and actionable insights for stakeholders. Our study covers the period from 2019 to 2033, with a base year of 2025, and includes detailed historical data from 2019-2024 and forecast projections from 2025-2033. We explore key market segments, including applications in knee, hip, spine, and shoulder arthroscopy, alongside a breakdown of essential products like arthroscopes, arthroscopic implants, fluid management systems, RF systems, and visualization systems. The geographical scope encompasses the United States, Canada, and Mexico, offering regional-specific analyses.

The North America arthroscopy devices market is experiencing robust growth driven by an aging population, increasing prevalence of sports-related injuries and degenerative joint diseases, and advancements in minimally invasive surgical techniques. The demand for sophisticated arthroscopic instruments and implants is on the rise, propelling innovation and market expansion. This report provides a granular view of market trends, competitive strategies, and future opportunities within this burgeoning sector.

North America Arthroscopy Devices Market Market Structure & Competitive Dynamics

The North America arthroscopy devices market is characterized by a moderately concentrated structure, with a few key global players holding significant market share. Companies like Smith & Nephew PLC, Arthrex Inc., Medtronic PLC, and Stryker Corporation are at the forefront, investing heavily in research and development to maintain their competitive edge. The innovation ecosystem is robust, fueled by continuous technological advancements in visualization, instrumentation, and implantable devices designed to enhance surgical outcomes and patient recovery. Regulatory frameworks, primarily driven by the FDA in the United States, play a crucial role in market entry and product approval, influencing the pace of innovation and market access. Product substitutes, though limited in direct arthroscopic applications, can emerge from alternative surgical techniques or non-invasive treatments. End-user trends are increasingly focused on patient-centric care, demanding less invasive procedures, faster recovery times, and improved long-term joint health. Mergers and acquisitions (M&A) are a significant aspect of the market dynamics, as larger companies seek to acquire innovative technologies and expand their product portfolios. For instance, the acquisition of Embody, Inc. by Zimmer Biomet Holdings Inc. for up to USD 275 million underscores the strategic importance of acquiring specialized orthopaedic solutions. The market share of the top players is estimated to be around 70% combined, indicating a competitive yet consolidated landscape. M&A deal values are often substantial, reflecting the high growth potential and strategic value of companies within this sector.

North America Arthroscopy Devices Market Industry Trends & Insights

The North America arthroscopy devices market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025-2033). This upward trajectory is underpinned by several interconnected industry trends and insights. Firstly, the increasing incidence of sports-related injuries, particularly among the growing physically active population, is a primary market driver. Conditions like ligament tears, meniscal damage, and rotator cuff injuries frequently necessitate arthroscopic interventions. Secondly, the rising prevalence of degenerative joint diseases, such as osteoarthritis, is contributing significantly to market expansion, especially in aging demographics. Arthroscopy offers a less invasive alternative to traditional open surgeries for managing these conditions, leading to reduced patient recovery times and hospital stays.

Technological disruptions are continuously reshaping the market. The development of advanced imaging technologies, including high-definition and 4K arthroscopes, coupled with artificial intelligence-powered diagnostic tools, is enhancing surgical precision and diagnostic accuracy. Miniaturization of instruments allows for smaller incisions and improved patient comfort. Furthermore, the integration of robotics and augmented reality in arthroscopic procedures is an emerging trend that promises to revolutionize surgical workflows and outcomes. Consumer preferences are shifting towards minimally invasive procedures, driven by a desire for quicker recovery, less scarring, and reduced pain. Patients are becoming more informed and actively involved in their treatment decisions, seeking out procedures with proven efficacy and minimal post-operative complications.

Competitive dynamics are intensifying, with established players continuously innovating and smaller, agile companies focusing on niche applications and disruptive technologies. Strategic partnerships and collaborations are common, aimed at accelerating product development and market penetration. For example, the collaboration between Lazurite and the Hospital for Special Surgery (HSS) for the ArthroFree Wireless Surgical Camera System, the first wireless surgical camera for arthroscopy, exemplifies this trend towards innovative solutions that address unmet clinical needs and improve workflow efficiency. The market penetration of arthroscopy procedures continues to rise, replacing more invasive open surgeries across various joint applications. Economic factors, such as increasing healthcare expenditure and insurance coverage for minimally invasive procedures, also play a vital role in market growth. The North American region, with its advanced healthcare infrastructure and high disposable income, represents a significant market share, driving global demand for arthroscopy devices. The focus on value-based healthcare is also pushing for the development of cost-effective and outcome-driven arthroscopic solutions.

Dominant Markets & Segments in North America Arthroscopy Devices Market

The North America Arthroscopy Devices Market is dominated by the United States, which accounts for the largest market share due to its advanced healthcare infrastructure, high patient volume, and significant investments in medical technology research and development. The country's strong reimbursement policies for minimally invasive procedures further bolster its dominance.

Within the Application segment, Knee Arthroscopy is the most dominant application, driven by the high prevalence of sports injuries, osteoarthritis, and meniscal tears in this joint. The increasing adoption of advanced arthroscopic implants and surgical techniques for knee reconstruction and repair contributes significantly to this segment's leading position.

In terms of Product, the Arthroscope segment holds a substantial market share. These devices are the fundamental visual tools for performing arthroscopic procedures. Continuous advancements in imaging technology, such as high-definition and 4K resolution, and the development of smaller, more maneuverable scopes are driving growth in this segment. The Arthroscopic Implant segment is also experiencing robust growth, fueled by innovations in biomaterials and implant designs for ligament reconstruction, meniscal repair, and cartilage regeneration.

Key drivers for the dominance of the United States include:

- Economic Policies: Favorable reimbursement policies and substantial private and public healthcare spending on orthopaedic procedures.

- Infrastructure: A well-established network of hospitals, surgical centers, and specialized orthopaedic clinics equipped with advanced technology.

- Research & Development: Significant investment in R&D by leading medical device manufacturers, fostering rapid innovation and product adoption.

- Patient Demographics: A large population with a high incidence of sports injuries and degenerative joint diseases, coupled with a growing elderly population.

Mexico represents a significant emerging market within North America, exhibiting a growing demand for arthroscopy devices driven by increasing healthcare expenditure, improving access to medical facilities, and a rise in sports-related activities. While currently smaller than the US market, its growth potential is substantial.

The Shoulder and Elbow Arthroscopy application segment is also a major contributor to market growth, with increasing diagnoses of rotator cuff tears, impingement syndrome, and instability issues, particularly among athletes and the aging population.

The Visualization System segment is crucial, as advancements in imaging technology directly impact surgical precision and outcomes, making it a vital component of the overall arthroscopy ecosystem. The Fluid Management System is essential for maintaining clear surgical fields and optimal intra-articular pressure, contributing to procedural efficiency and safety.

North America Arthroscopy Devices Market Product Innovations

Product innovations in the North America arthroscopy devices market are primarily focused on enhancing surgical precision, improving patient outcomes, and streamlining surgical workflows. Key developments include the introduction of wireless arthroscopic camera systems, such as Lazurite's ArthroFree, which eliminates cable clutter and enhances surgeon mobility. Advancements in arthroscopic implants, utilizing novel biomaterials for better tissue integration and faster healing, are also prominent. Furthermore, the integration of artificial intelligence and augmented reality into visualization systems is enabling surgeons to gain deeper insights and plan procedures with greater accuracy. These innovations aim to reduce operative time, minimize patient trauma, and accelerate recovery periods, thereby offering a competitive advantage to companies that can successfully bring these advanced solutions to market.

Report Segmentation & Scope

This report segments the North America Arthroscopy Devices Market comprehensively across key categories. The Application segment includes Knee Arthroscopy, Hip Arthroscopy, Spine Arthroscopy, Shoulder and Elbow Arthroscopy, and Other Arthroscopy Applications, each analyzed for market size and growth projections. The Product segment breaks down the market into Arthroscope, Arthroscopic Implant, Fluid Management System, Radiofrequency (RF) System, Visualization System, and Other Products, detailing their respective market shares and competitive dynamics. Geographically, the market is analyzed across the United States, Canada, and Mexico, providing specific insights into regional growth drivers and market penetration. Each segment is evaluated based on historical performance and future potential, offering a detailed outlook on market trends and competitive strategies.

Key Drivers of North America Arthroscopy Devices Market Growth

The North America Arthroscopy Devices Market growth is primarily driven by a confluence of factors. Firstly, the increasing prevalence of sports-related injuries and degenerative joint diseases, such as osteoarthritis, among an aging and active population fuels the demand for minimally invasive arthroscopic procedures. Secondly, significant advancements in arthroscopic technology, including high-definition visualization systems, robotic-assisted surgery, and innovative implant designs, enhance surgical precision and patient recovery, thereby promoting adoption. Thirdly, favorable reimbursement policies and growing healthcare expenditure in countries like the United States support the widespread use of these advanced medical devices. The ongoing shift in patient preference towards less invasive surgical options also significantly contributes to market expansion.

Challenges in the North America Arthroscopy Devices Market Sector

Despite its robust growth, the North America Arthroscopy Devices Market faces several challenges. High development and manufacturing costs associated with sophisticated medical devices can lead to higher procedural costs, potentially impacting affordability and accessibility for some patient populations. Stringent regulatory approvals for new medical technologies, although crucial for patient safety, can prolong time-to-market and increase R&D expenses. Reimbursement challenges and variations across different healthcare systems and insurance providers can create complexities for market penetration and adoption. Furthermore, increasing competition from both established giants and innovative startups necessitates continuous innovation and strategic pricing. Limited availability of skilled arthroscopic surgeons in certain regions can also act as a restraint on market growth.

Leading Players in the North America Arthroscopy Devices Market Market

- Smith & Nephew PLC

- Arthrex Inc.

- Medtronic PLC

- Richard Wolf GmbH

- Karl Storz GmbH & Co KG

- Conmed Corporation

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

Key Developments in North America Arthroscopy Devices Market Sector

- January 2023: Zimmer Biomet signed a definitive agreement to acquire Embody, Inc., a privately-held medical device company focused on soft tissue healing, for USD 155 million at closing and up to an additional USD 120 million, subject to achieving future regulatory and commercial milestones over a three-year period. This acquisition aims to strengthen Zimmer Biomet's orthopaedic portfolio with innovative solutions for soft tissue repair.

- November 2022: Lazurite and the Hospital for Special Surgery (HSS) received U.S. FDA clearance for a collaborative relationship based on Lazurite's ArthroFree Wireless Surgical Camera System, the first wireless surgical camera system for arthroscopy and general endoscopy. This development signifies a major technological advancement, promising to reduce operative complexity and improve surgeon ergonomics.

Strategic North America Arthroscopy Devices Market Market Outlook

The strategic outlook for the North America Arthroscopy Devices Market remains exceptionally positive, driven by sustained innovation and increasing demand for minimally invasive orthopaedic solutions. Future growth accelerators will likely include the continued development of AI-integrated visualization systems for enhanced surgical planning and execution, as well as the expansion of robotic-assisted arthroscopy, offering greater precision and control. The market will also witness growth in the development of advanced biological solutions for cartilage regeneration and faster tissue healing, addressing unmet clinical needs. Companies are expected to focus on expanding their product portfolios through strategic partnerships and acquisitions to capture market share. Furthermore, the increasing adoption of telehealth and remote surgical support technologies could further democratize access to advanced arthroscopic expertise across the region, presenting significant strategic opportunities for market players.

North America Arthroscopy Devices Market Segmentation

-

1. Application

- 1.1. Knee Arthroscopy

- 1.2. Hip Arthroscopy

- 1.3. Spine Arthroscopy

- 1.4. Shoulder and Elbow Arthroscopy

- 1.5. Other Arthroscopy Applications

-

2. Product

- 2.1. Arthroscope

- 2.2. Arthroscopic Implant

- 2.3. Fluid Management System

- 2.4. Radiofrequency (RF) System

- 2.5. Visualization System

- 2.6. Other Products

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Arthroscopy Devices Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Arthroscopy Devices Market Regional Market Share

Geographic Coverage of North America Arthroscopy Devices Market

North America Arthroscopy Devices Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.03% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Knee Arthroscopy

- 5.1.2. Hip Arthroscopy

- 5.1.3. Spine Arthroscopy

- 5.1.4. Shoulder and Elbow Arthroscopy

- 5.1.5. Other Arthroscopy Applications

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Arthroscope

- 5.2.2. Arthroscopic Implant

- 5.2.3. Fluid Management System

- 5.2.4. Radiofrequency (RF) System

- 5.2.5. Visualization System

- 5.2.6. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Arthroscopy Devices Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Knee Arthroscopy

- 6.1.2. Hip Arthroscopy

- 6.1.3. Spine Arthroscopy

- 6.1.4. Shoulder and Elbow Arthroscopy

- 6.1.5. Other Arthroscopy Applications

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Arthroscope

- 6.2.2. Arthroscopic Implant

- 6.2.3. Fluid Management System

- 6.2.4. Radiofrequency (RF) System

- 6.2.5. Visualization System

- 6.2.6. Other Products

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. United States North America Arthroscopy Devices Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Knee Arthroscopy

- 7.1.2. Hip Arthroscopy

- 7.1.3. Spine Arthroscopy

- 7.1.4. Shoulder and Elbow Arthroscopy

- 7.1.5. Other Arthroscopy Applications

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Arthroscope

- 7.2.2. Arthroscopic Implant

- 7.2.3. Fluid Management System

- 7.2.4. Radiofrequency (RF) System

- 7.2.5. Visualization System

- 7.2.6. Other Products

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Canada North America Arthroscopy Devices Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Knee Arthroscopy

- 8.1.2. Hip Arthroscopy

- 8.1.3. Spine Arthroscopy

- 8.1.4. Shoulder and Elbow Arthroscopy

- 8.1.5. Other Arthroscopy Applications

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Arthroscope

- 8.2.2. Arthroscopic Implant

- 8.2.3. Fluid Management System

- 8.2.4. Radiofrequency (RF) System

- 8.2.5. Visualization System

- 8.2.6. Other Products

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Mexico North America Arthroscopy Devices Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Knee Arthroscopy

- 9.1.2. Hip Arthroscopy

- 9.1.3. Spine Arthroscopy

- 9.1.4. Shoulder and Elbow Arthroscopy

- 9.1.5. Other Arthroscopy Applications

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Arthroscope

- 9.2.2. Arthroscopic Implant

- 9.2.3. Fluid Management System

- 9.2.4. Radiofrequency (RF) System

- 9.2.5. Visualization System

- 9.2.6. Other Products

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Smith & Nephew PLC

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Arthrex Inc

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Medtronic PLC

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Richard Wolf GmbH

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Karl Storz GmbH & Co KG

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Conmed Corporation

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Johnson & Johnson

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Stryker Corporation

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Zimmer Biomet Holdings Inc

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Smith & Nephew PLC

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Arthroscopy Devices Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Arthroscopy Devices Market Share (%) by Company 2025

List of Tables

- Table 1: North America Arthroscopy Devices Market Revenue Million Forecast, by Application 2020 & 2033

- Table 2: North America Arthroscopy Devices Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 3: North America Arthroscopy Devices Market Revenue Million Forecast, by Product 2020 & 2033

- Table 4: North America Arthroscopy Devices Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 5: North America Arthroscopy Devices Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: North America Arthroscopy Devices Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 7: North America Arthroscopy Devices Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: North America Arthroscopy Devices Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: North America Arthroscopy Devices Market Revenue Million Forecast, by Application 2020 & 2033

- Table 10: North America Arthroscopy Devices Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: North America Arthroscopy Devices Market Revenue Million Forecast, by Product 2020 & 2033

- Table 12: North America Arthroscopy Devices Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 13: North America Arthroscopy Devices Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: North America Arthroscopy Devices Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 15: North America Arthroscopy Devices Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: North America Arthroscopy Devices Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: North America Arthroscopy Devices Market Revenue Million Forecast, by Application 2020 & 2033

- Table 18: North America Arthroscopy Devices Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 19: North America Arthroscopy Devices Market Revenue Million Forecast, by Product 2020 & 2033

- Table 20: North America Arthroscopy Devices Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 21: North America Arthroscopy Devices Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: North America Arthroscopy Devices Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 23: North America Arthroscopy Devices Market Revenue Million Forecast, by Country 2020 & 2033

- Table 24: North America Arthroscopy Devices Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: North America Arthroscopy Devices Market Revenue Million Forecast, by Application 2020 & 2033

- Table 26: North America Arthroscopy Devices Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 27: North America Arthroscopy Devices Market Revenue Million Forecast, by Product 2020 & 2033

- Table 28: North America Arthroscopy Devices Market Volume K Unit Forecast, by Product 2020 & 2033

- Table 29: North America Arthroscopy Devices Market Revenue Million Forecast, by Geography 2020 & 2033

- Table 30: North America Arthroscopy Devices Market Volume K Unit Forecast, by Geography 2020 & 2033

- Table 31: North America Arthroscopy Devices Market Revenue Million Forecast, by Country 2020 & 2033

- Table 32: North America Arthroscopy Devices Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Arthroscopy Devices Market?

The projected CAGR is approximately 3.03%.

2. Which companies are prominent players in the North America Arthroscopy Devices Market?

Key companies in the market include Smith & Nephew PLC, Arthrex Inc, Medtronic PLC, Richard Wolf GmbH, Karl Storz GmbH & Co KG, Conmed Corporation, Johnson & Johnson, Stryker Corporation, Zimmer Biomet Holdings Inc.

3. What are the main segments of the North America Arthroscopy Devices Market?

The market segments include Application, Product, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 732.21 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidences of Sports Injuries; Rising Geriatric Population; Technological Advancements in Arthroscopic Implants.

6. What are the notable trends driving market growth?

Arthroscope is Expected to Hold Significant Market Share over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Skilled Surgeons; Stringent Regulatory Requirements; High Cost of Arthroscopy Devices.

8. Can you provide examples of recent developments in the market?

In January 2023, Zimmer Biomet signed a definitive agreement to acquire Embody, Inc., a privately-held medical device company focused on soft tissue healing, for USD 155 million at closing and up to an additional USD 120 million, subject to achieving future regulatory and commercial milestones over a three-year period.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Arthroscopy Devices Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Arthroscopy Devices Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Arthroscopy Devices Market?

To stay informed about further developments, trends, and reports in the North America Arthroscopy Devices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence