Key Insights

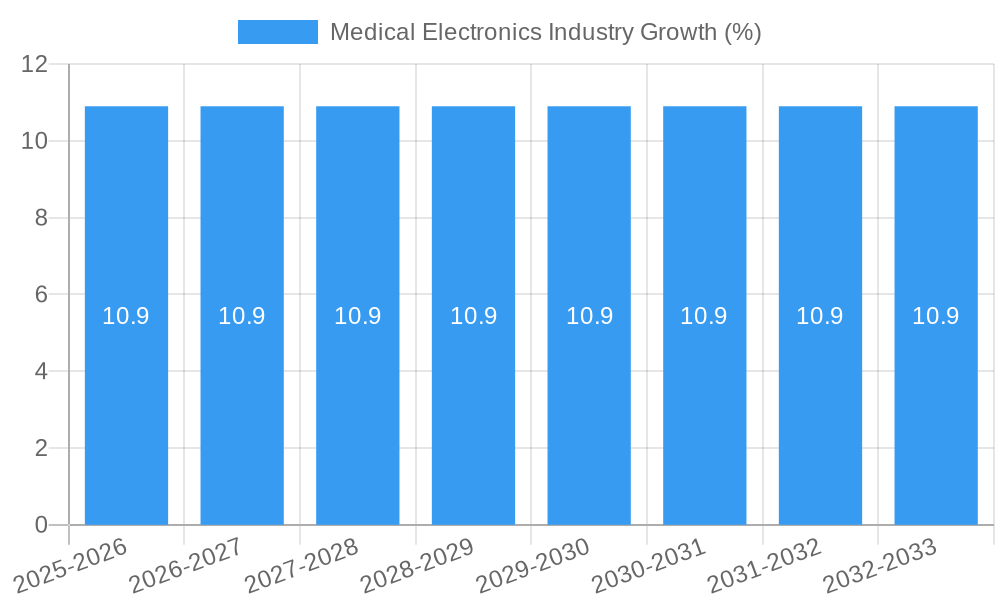

The global medical electronics market is poised for significant expansion, projected to reach a substantial market size by 2033, driven by a robust Compound Annual Growth Rate (CAGR) of 10.90%. This impressive growth is fueled by an increasing demand for advanced diagnostic and therapeutic solutions, propelled by factors such as the rising prevalence of chronic diseases, an aging global population, and escalating healthcare expenditure worldwide. The continuous innovation in medical technology, including the development of sophisticated non-invasive and minimally invasive devices, is also a key catalyst. The market is witnessing a strong trend towards digitalization and miniaturization of medical devices, enhancing patient care and improving diagnostic accuracy. Furthermore, the growing adoption of telemedicine and remote patient monitoring systems is further accelerating market penetration.

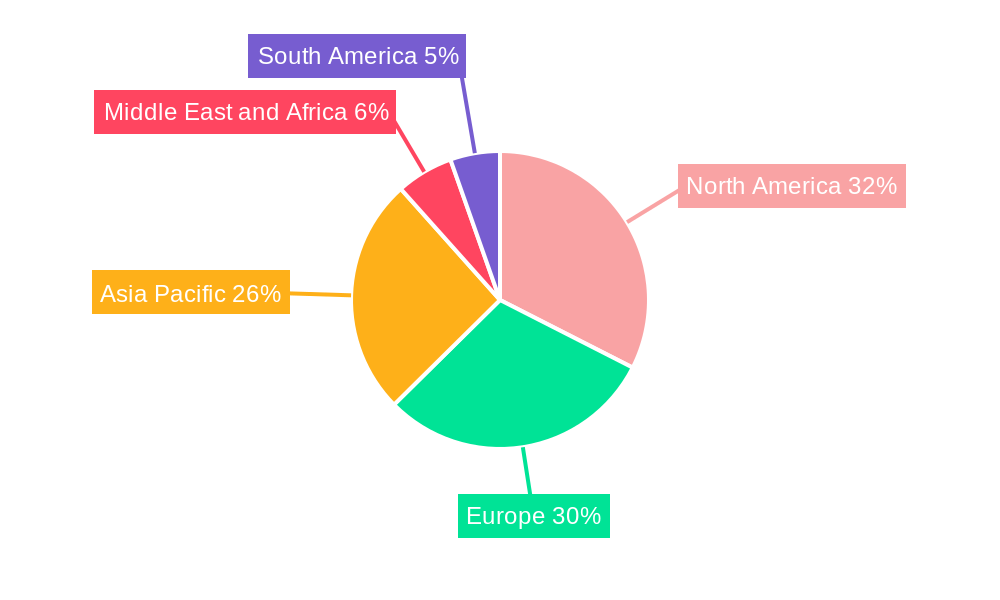

The competitive landscape is characterized by the presence of major global players, including Siemens Healthcare GmbH, GE Healthcare, and Medtronic PLC, who are actively investing in research and development to introduce groundbreaking products and expand their market reach. Segmentation analysis reveals that both non-invasive products, such as MRI, X-ray, and CT scanners, and invasive products, including pacemakers and ICDs, are experiencing healthy demand. The diagnostics and monitoring segments are particularly prominent, catering to the growing need for early disease detection and continuous patient management. Hospitals and clinics represent the largest end-user segment, followed by ambulatory surgical centers. Geographically, North America and Europe are anticipated to maintain their leadership positions, owing to well-established healthcare infrastructures and high adoption rates of advanced medical technologies. However, the Asia Pacific region is expected to exhibit the fastest growth, driven by increasing healthcare investments, a burgeoning patient population, and the expansion of healthcare facilities.

This comprehensive report provides an in-depth analysis of the global Medical Electronics Industry, a dynamic sector characterized by rapid technological advancements and increasing demand for sophisticated healthcare solutions. Covering the historical period from 2019 to 2024, the base year of 2025, and projecting through the forecast period of 2025–2033, this report offers critical insights into market structure, competitive landscape, emerging trends, and future growth trajectories. We analyze key segments including non-invasive and invasive products, diagnostic, monitoring, and therapeutic applications, and various end-user groups such as hospitals, clinics, and ambulatory surgical centers. With a focus on actionable intelligence, this report is an indispensable resource for stakeholders seeking to navigate and capitalize on the evolving medical electronics market.

Medical Electronics Industry Market Structure & Competitive Dynamics

The medical electronics market exhibits a moderately concentrated structure, with a few major players like Siemens Healthcare GmbH, GE Healthcare, and Koninklijke Philips NV holding significant market shares, estimated in the billions. However, the presence of numerous specialized companies in niche segments ensures a vibrant competitive landscape. Innovation ecosystems are driven by substantial R&D investments, particularly in areas like AI-powered diagnostics and minimally invasive technologies. Regulatory frameworks, such as FDA approvals and CE marking, play a crucial role in market entry and product lifecycle, influencing the pace of innovation and market access. Product substitutes are emerging, especially in diagnostics, with advanced software solutions complementing hardware. End-user trends are shifting towards home healthcare and remote patient monitoring, driving demand for portable and connected devices. Mergers and acquisitions (M&A) are active, with deal values in the hundreds of millions, as larger companies seek to acquire innovative technologies and expand their portfolios. For example, Medtronic PLC has been actively involved in strategic acquisitions to bolster its offerings in areas like neuromodulation and diabetes management. The overall market capitalization of the leading players contributes significantly to the global economy, with the sector projected for substantial growth.

Medical Electronics Industry Industry Trends & Insights

The medical electronics industry is experiencing robust growth, driven by several pivotal trends and insights. The increasing prevalence of chronic diseases worldwide, coupled with an aging global population, is a primary growth driver, escalating the demand for advanced diagnostic and monitoring devices. Technological disruptions are at the forefront, with Artificial Intelligence (AI) and Machine Learning (ML) revolutionizing medical imaging interpretation, predictive diagnostics, and personalized treatment plans. The integration of the Internet of Medical Things (IoMT) is fostering a connected healthcare ecosystem, enabling real-time data collection, remote patient monitoring, and improved telehealth services, thereby enhancing patient outcomes and operational efficiency. Consumer preferences are increasingly leaning towards non-invasive diagnostic tools and patient-centric devices that offer convenience and improved user experience. The push for value-based healthcare is also influencing market dynamics, encouraging the development of cost-effective and highly reliable medical electronics that demonstrate tangible benefits.

Furthermore, advancements in miniaturization and wireless technology are leading to the development of more portable and wearable medical devices, expanding their application beyond traditional clinical settings to home care and personalized wellness. The development of novel materials and manufacturing techniques, such as 3D printing, is enabling the creation of customized implantable devices and prosthetics. The competitive landscape is characterized by intense innovation, strategic partnerships, and an ongoing pursuit of market share. Companies are investing heavily in R&D to stay ahead of the curve, particularly in areas like robotics for surgery, advanced imaging modalities, and AI-driven diagnostic platforms. The Compound Annual Growth Rate (CAGR) for the medical electronics market is projected to be robust, estimated between 6% and 8% over the forecast period. Market penetration of advanced medical electronics is continuously increasing, driven by expanding healthcare infrastructure in emerging economies and growing awareness of the benefits of early and accurate diagnosis. The global market size is expected to reach hundreds of billions by the end of the forecast period, underscoring the sector's significant economic impact and its critical role in global health.

Dominant Markets & Segments in Medical Electronics Industry

The Non-invasive Products segment is a dominant force within the medical electronics industry, driven by the broad application of technologies like MRI, X-Ray, CT Scans, and Ultrasound. These imaging systems are indispensable for diagnostics across a vast array of medical conditions, from routine check-ups to complex surgical planning. The market penetration of these devices is high in developed economies, and is rapidly expanding in emerging markets due to increasing healthcare expenditure and the growing demand for advanced diagnostic capabilities. Key drivers for this segment's dominance include:

- Technological Advancements: Continuous innovation in image resolution, speed, and portability.

- Growing Geriatric Population: Increased incidence of age-related diseases necessitating sophisticated diagnostic tools.

- Early Disease Detection Initiatives: Government and private sector focus on proactive healthcare.

- AI Integration: Enhancing diagnostic accuracy and reducing interpretation time.

In terms of applications, Diagnostics stands out as the primary revenue generator. This is directly linked to the widespread use of non-invasive imaging and monitoring equipment for identifying diseases and assessing patient health. The need for accurate and timely diagnoses fuels substantial investment in this area.

Among end-users, Hospitals and Clinics represent the largest market share. These institutions are the primary consumers of high-end medical electronic equipment due to the volume of patient care and the complexity of procedures performed.

- Economic Policies: Government initiatives promoting healthcare infrastructure development and reimbursement policies favoring advanced diagnostic procedures.

- Infrastructure Development: Investment in new hospitals and upgrading existing facilities in both developed and developing nations.

- Physician Training and Adoption: Availability of trained professionals proficient in operating and interpreting data from advanced medical electronics.

The North America region, particularly the United States, holds a dominant position due to its well-established healthcare infrastructure, high per capita healthcare spending, and strong emphasis on research and development. Countries like Germany and the UK in Europe also contribute significantly. Emerging economies in the Asia Pacific region, such as China and India, are witnessing rapid growth, driven by increasing disposable incomes, expanding healthcare access, and government investments in medical technology.

Invasive Products, while a smaller segment compared to non-invasive, is critically important for therapeutic applications. Devices like pacemakers and implantable cardioverter defibrillators (ICDs) are life-saving technologies for cardiovascular conditions. The market for these products is driven by the increasing burden of cardiovascular diseases and advancements in implantable device technology, including miniaturization and extended battery life. The demand for these specialized products, though niche, offers substantial revenue potential.

Medical Electronics Industry Product Innovations

Product innovation in the medical electronics industry is characterized by the relentless pursuit of enhanced precision, patient comfort, and connectivity. Key developments include advancements in AI-driven imaging analysis, leading to more accurate and faster diagnoses with reduced radiation exposure. Miniaturization of devices like pacemakers and wearable sensors is enabling less invasive procedures and improved patient compliance. The integration of IoMT is creating a connected ecosystem, facilitating remote patient monitoring and personalized treatment plans. Competitive advantages are gained through superior imaging quality, sophisticated data analytics capabilities, user-friendly interfaces, and seamless integration with existing hospital IT systems. For instance, companies are focusing on developing devices that offer real-time feedback and personalized therapy delivery, thereby improving patient outcomes and driving market adoption.

Report Segmentation & Scope

This report meticulously segments the Medical Electronics Industry across crucial dimensions to provide a granular market overview. The Product segmentation encompasses Non-invasive Products, including advanced imaging systems such as MRI, X-Ray, CT Scan, Ultrasound, and Nuclear Imaging Systems, alongside vital monitoring devices like Cardiac Monitors, Respiratory Monitors, Hemodynamic Monitors, Multipara Monitors, and Digital Thermometers, plus Other Products. The Invasive Products segment features critical implantable devices such as Pacemakers, Implantable Cardioverter Defibrillators (ICD), Implantable Loop Recorders, Spinal Cord Stimulators, and Other Invasive Products. The Application segmentation divides the market into Diagnostics, Monitoring, and Therapeutics. The End User segmentation identifies key consumer groups including Hospitals and Clinics, Ambulatory Surgical Centers, and Other End Users. Growth projections for each segment are meticulously analyzed, estimating market sizes in the billions and assessing competitive dynamics, with a focus on market share and key technological trends influencing each category.

Key Drivers of Medical Electronics Industry Growth

Several key drivers are propelling the growth of the medical electronics industry. Technological advancements, particularly in AI, ML, and IoMT, are revolutionizing diagnostics and patient care, creating demand for sophisticated devices. The increasing global prevalence of chronic diseases and an aging population are significant market expanders, necessitating advanced medical interventions. Government initiatives promoting healthcare infrastructure development and increased R&D funding are further stimulating market expansion. Economic growth in emerging economies is leading to higher disposable incomes and greater access to advanced healthcare, boosting demand for medical electronics.

Challenges in the Medical Electronics Industry Sector

Despite robust growth, the medical electronics industry faces several challenges. Stringent regulatory hurdles and lengthy approval processes for new medical devices can significantly impact time-to-market and R&D costs. Supply chain disruptions, exacerbated by geopolitical factors and global events, can affect component availability and manufacturing timelines. High development and manufacturing costs for cutting-edge medical electronics can limit accessibility for some healthcare providers. Intense competition and the need for continuous innovation also exert pressure on profit margins. Furthermore, data security and privacy concerns associated with connected medical devices require robust cybersecurity measures.

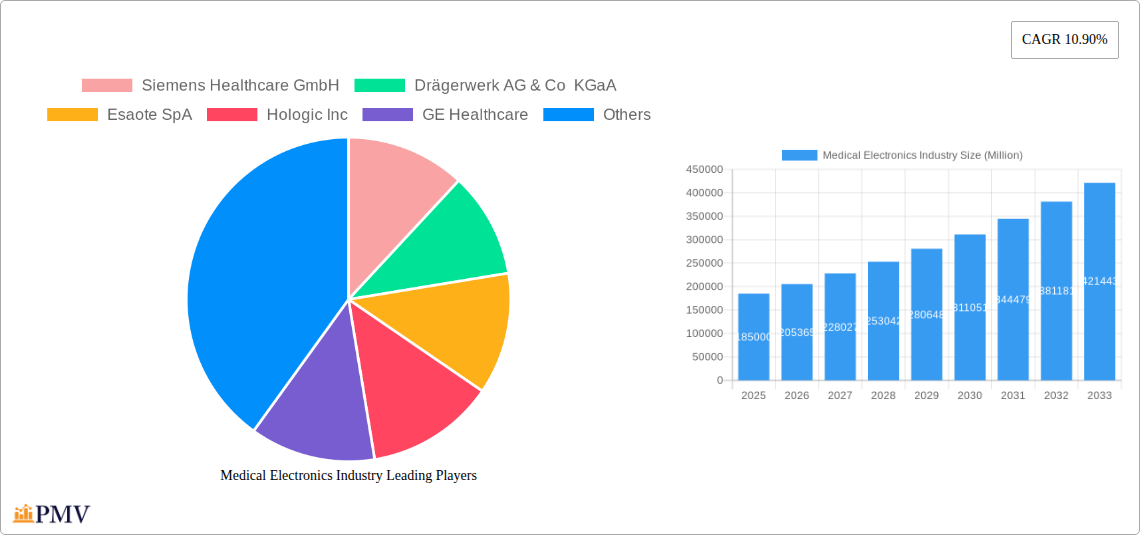

Leading Players in the Medical Electronics Industry Market

- Siemens Healthcare GmbH

- Drägerwerk AG & Co KGaA

- Esaote SpA

- Hologic Inc

- GE Healthcare

- Getinge Inc

- Medtronic PLC

- Fujifilm Corporation

- Mindray Medical International Limited

- Koninklijke Philips NV

- Canon Medical Systems

- McKesson Corporation

- Olympus Corporation

Key Developments in Medical Electronics Industry Sector

- August 2022: The South Korean Ministry of Food and Drug Safety granted clearance to VUNO, a medical artificial intelligence company, for its ECG device, Hativ Pro, a portable medical device that measures a user's heart rate and sends this data through a connected mobile phone app. This development highlights the growing integration of AI in portable diagnostic devices.

- February 2022: Shineco, Inc. entered a partnership with Weifang Jianyi Medical Devices Co., Ltd., one of the leading Chinese medical device companies based in Shandong Province, to jointly manufacture and sell imaging devices, including PET, PET-CT, and PET-MRI. This collaboration signifies strategic alliances aimed at expanding manufacturing capabilities and market reach for advanced imaging technologies.

Strategic Medical Electronics Industry Market Outlook

The strategic outlook for the medical electronics industry remains exceptionally positive, driven by ongoing innovation and expanding global healthcare needs. The increasing adoption of AI and IoMT technologies is poised to unlock new frontiers in personalized medicine and remote patient care, creating significant market potential. Strategic opportunities lie in developing integrated diagnostic and therapeutic solutions, enhancing data analytics capabilities, and focusing on emerging markets with growing healthcare demands. Investments in R&D for novel materials, miniaturized devices, and advanced imaging techniques will be crucial for maintaining a competitive edge. Collaborations between technology providers and healthcare institutions will further accelerate the adoption of advanced medical electronics, paving the way for a future of more efficient, accessible, and patient-centric healthcare globally. The market is expected to see continued expansion, driven by these strategic growth accelerators.

Medical Electronics Industry Segmentation

-

1. Product

-

1.1. Non-invasive Products

- 1.1.1. MRI

- 1.1.2. X-Ray

- 1.1.3. CT Scan

- 1.1.4. Ultrasound

- 1.1.5. Nuclear Imaging Systems

- 1.1.6. Cardiac Monitors

- 1.1.7. Respiratory Monitors

- 1.1.8. Hemodynamic Monitors

- 1.1.9. Multipara Monitors

- 1.1.10. Digital Thermometers

- 1.1.11. Other Products

-

1.2. Invasive Products

- 1.2.1. Endoscopes

- 1.2.2. Pacemakers

- 1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 1.2.4. Implantable Loop Recorders

- 1.2.5. Spinal Cord Stimulator

- 1.2.6. Other Invasive Products

-

1.1. Non-invasive Products

-

2. Application

- 2.1. Diagnostics

- 2.2. Monitoring

- 2.3. Therapeutics

-

3. End User

- 3.1. Hospitals and Clinics

- 3.2. Ambulatory Surgical Centers

- 3.3. Other End Users

Medical Electronics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Medical Electronics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.90% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Geriatric Population; Rising Application of Imaging Devices

- 3.3. Market Restrains

- 3.3.1. Ramped up regulatory scrutiny; High Cost and Maintenance

- 3.4. Market Trends

- 3.4.1. MRI Segment Expected to Hold Significant Market Share in the Medical Electronics Market Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Non-invasive Products

- 5.1.1.1. MRI

- 5.1.1.2. X-Ray

- 5.1.1.3. CT Scan

- 5.1.1.4. Ultrasound

- 5.1.1.5. Nuclear Imaging Systems

- 5.1.1.6. Cardiac Monitors

- 5.1.1.7. Respiratory Monitors

- 5.1.1.8. Hemodynamic Monitors

- 5.1.1.9. Multipara Monitors

- 5.1.1.10. Digital Thermometers

- 5.1.1.11. Other Products

- 5.1.2. Invasive Products

- 5.1.2.1. Endoscopes

- 5.1.2.2. Pacemakers

- 5.1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 5.1.2.4. Implantable Loop Recorders

- 5.1.2.5. Spinal Cord Stimulator

- 5.1.2.6. Other Invasive Products

- 5.1.1. Non-invasive Products

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Diagnostics

- 5.2.2. Monitoring

- 5.2.3. Therapeutics

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals and Clinics

- 5.3.2. Ambulatory Surgical Centers

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Non-invasive Products

- 6.1.1.1. MRI

- 6.1.1.2. X-Ray

- 6.1.1.3. CT Scan

- 6.1.1.4. Ultrasound

- 6.1.1.5. Nuclear Imaging Systems

- 6.1.1.6. Cardiac Monitors

- 6.1.1.7. Respiratory Monitors

- 6.1.1.8. Hemodynamic Monitors

- 6.1.1.9. Multipara Monitors

- 6.1.1.10. Digital Thermometers

- 6.1.1.11. Other Products

- 6.1.2. Invasive Products

- 6.1.2.1. Endoscopes

- 6.1.2.2. Pacemakers

- 6.1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 6.1.2.4. Implantable Loop Recorders

- 6.1.2.5. Spinal Cord Stimulator

- 6.1.2.6. Other Invasive Products

- 6.1.1. Non-invasive Products

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Diagnostics

- 6.2.2. Monitoring

- 6.2.3. Therapeutics

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals and Clinics

- 6.3.2. Ambulatory Surgical Centers

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Europe Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Non-invasive Products

- 7.1.1.1. MRI

- 7.1.1.2. X-Ray

- 7.1.1.3. CT Scan

- 7.1.1.4. Ultrasound

- 7.1.1.5. Nuclear Imaging Systems

- 7.1.1.6. Cardiac Monitors

- 7.1.1.7. Respiratory Monitors

- 7.1.1.8. Hemodynamic Monitors

- 7.1.1.9. Multipara Monitors

- 7.1.1.10. Digital Thermometers

- 7.1.1.11. Other Products

- 7.1.2. Invasive Products

- 7.1.2.1. Endoscopes

- 7.1.2.2. Pacemakers

- 7.1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 7.1.2.4. Implantable Loop Recorders

- 7.1.2.5. Spinal Cord Stimulator

- 7.1.2.6. Other Invasive Products

- 7.1.1. Non-invasive Products

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Diagnostics

- 7.2.2. Monitoring

- 7.2.3. Therapeutics

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals and Clinics

- 7.3.2. Ambulatory Surgical Centers

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Asia Pacific Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Non-invasive Products

- 8.1.1.1. MRI

- 8.1.1.2. X-Ray

- 8.1.1.3. CT Scan

- 8.1.1.4. Ultrasound

- 8.1.1.5. Nuclear Imaging Systems

- 8.1.1.6. Cardiac Monitors

- 8.1.1.7. Respiratory Monitors

- 8.1.1.8. Hemodynamic Monitors

- 8.1.1.9. Multipara Monitors

- 8.1.1.10. Digital Thermometers

- 8.1.1.11. Other Products

- 8.1.2. Invasive Products

- 8.1.2.1. Endoscopes

- 8.1.2.2. Pacemakers

- 8.1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 8.1.2.4. Implantable Loop Recorders

- 8.1.2.5. Spinal Cord Stimulator

- 8.1.2.6. Other Invasive Products

- 8.1.1. Non-invasive Products

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Diagnostics

- 8.2.2. Monitoring

- 8.2.3. Therapeutics

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals and Clinics

- 8.3.2. Ambulatory Surgical Centers

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Middle East and Africa Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Non-invasive Products

- 9.1.1.1. MRI

- 9.1.1.2. X-Ray

- 9.1.1.3. CT Scan

- 9.1.1.4. Ultrasound

- 9.1.1.5. Nuclear Imaging Systems

- 9.1.1.6. Cardiac Monitors

- 9.1.1.7. Respiratory Monitors

- 9.1.1.8. Hemodynamic Monitors

- 9.1.1.9. Multipara Monitors

- 9.1.1.10. Digital Thermometers

- 9.1.1.11. Other Products

- 9.1.2. Invasive Products

- 9.1.2.1. Endoscopes

- 9.1.2.2. Pacemakers

- 9.1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 9.1.2.4. Implantable Loop Recorders

- 9.1.2.5. Spinal Cord Stimulator

- 9.1.2.6. Other Invasive Products

- 9.1.1. Non-invasive Products

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Diagnostics

- 9.2.2. Monitoring

- 9.2.3. Therapeutics

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals and Clinics

- 9.3.2. Ambulatory Surgical Centers

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. South America Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Non-invasive Products

- 10.1.1.1. MRI

- 10.1.1.2. X-Ray

- 10.1.1.3. CT Scan

- 10.1.1.4. Ultrasound

- 10.1.1.5. Nuclear Imaging Systems

- 10.1.1.6. Cardiac Monitors

- 10.1.1.7. Respiratory Monitors

- 10.1.1.8. Hemodynamic Monitors

- 10.1.1.9. Multipara Monitors

- 10.1.1.10. Digital Thermometers

- 10.1.1.11. Other Products

- 10.1.2. Invasive Products

- 10.1.2.1. Endoscopes

- 10.1.2.2. Pacemakers

- 10.1.2.3. Implantable Cardioverter Defibrillator (ICD)

- 10.1.2.4. Implantable Loop Recorders

- 10.1.2.5. Spinal Cord Stimulator

- 10.1.2.6. Other Invasive Products

- 10.1.1. Non-invasive Products

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Diagnostics

- 10.2.2. Monitoring

- 10.2.3. Therapeutics

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals and Clinics

- 10.3.2. Ambulatory Surgical Centers

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. North America Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1. undefined

- 12. Europe Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1. undefined

- 13. Asia Pacific Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1. undefined

- 14. Middle East and Africa Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1. undefined

- 15. South America Medical Electronics Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1. undefined

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Siemens Healthcare GmbH

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Drägerwerk AG & Co KGaA

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Esaote SpA

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Hologic Inc

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 GE Healthcare

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Getinge Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Medtronic PLC

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Fujifilm Corporation

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Mindray Medical International Limited

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Koninklijke Philips NV

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Canon Medical Systems

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 McKesson Corporation

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Olympus Corporation

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.1 Siemens Healthcare GmbH

List of Figures

- Figure 1: Global Medical Electronics Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Global Medical Electronics Industry Volume Breakdown (K Unit, %) by Region 2024 & 2032

- Figure 3: North America Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 4: North America Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 5: North America Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: North America Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 7: Europe Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 8: Europe Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 9: Europe Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Europe Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 11: Asia Pacific Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 12: Asia Pacific Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 13: Asia Pacific Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: Asia Pacific Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 15: Middle East and Africa Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 16: Middle East and Africa Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 17: Middle East and Africa Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Middle East and Africa Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 19: South America Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 20: South America Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 21: South America Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: South America Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 23: North America Medical Electronics Industry Revenue (Million), by Product 2024 & 2032

- Figure 24: North America Medical Electronics Industry Volume (K Unit), by Product 2024 & 2032

- Figure 25: North America Medical Electronics Industry Revenue Share (%), by Product 2024 & 2032

- Figure 26: North America Medical Electronics Industry Volume Share (%), by Product 2024 & 2032

- Figure 27: North America Medical Electronics Industry Revenue (Million), by Application 2024 & 2032

- Figure 28: North America Medical Electronics Industry Volume (K Unit), by Application 2024 & 2032

- Figure 29: North America Medical Electronics Industry Revenue Share (%), by Application 2024 & 2032

- Figure 30: North America Medical Electronics Industry Volume Share (%), by Application 2024 & 2032

- Figure 31: North America Medical Electronics Industry Revenue (Million), by End User 2024 & 2032

- Figure 32: North America Medical Electronics Industry Volume (K Unit), by End User 2024 & 2032

- Figure 33: North America Medical Electronics Industry Revenue Share (%), by End User 2024 & 2032

- Figure 34: North America Medical Electronics Industry Volume Share (%), by End User 2024 & 2032

- Figure 35: North America Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 36: North America Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 37: North America Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 38: North America Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 39: Europe Medical Electronics Industry Revenue (Million), by Product 2024 & 2032

- Figure 40: Europe Medical Electronics Industry Volume (K Unit), by Product 2024 & 2032

- Figure 41: Europe Medical Electronics Industry Revenue Share (%), by Product 2024 & 2032

- Figure 42: Europe Medical Electronics Industry Volume Share (%), by Product 2024 & 2032

- Figure 43: Europe Medical Electronics Industry Revenue (Million), by Application 2024 & 2032

- Figure 44: Europe Medical Electronics Industry Volume (K Unit), by Application 2024 & 2032

- Figure 45: Europe Medical Electronics Industry Revenue Share (%), by Application 2024 & 2032

- Figure 46: Europe Medical Electronics Industry Volume Share (%), by Application 2024 & 2032

- Figure 47: Europe Medical Electronics Industry Revenue (Million), by End User 2024 & 2032

- Figure 48: Europe Medical Electronics Industry Volume (K Unit), by End User 2024 & 2032

- Figure 49: Europe Medical Electronics Industry Revenue Share (%), by End User 2024 & 2032

- Figure 50: Europe Medical Electronics Industry Volume Share (%), by End User 2024 & 2032

- Figure 51: Europe Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 52: Europe Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 53: Europe Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 54: Europe Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 55: Asia Pacific Medical Electronics Industry Revenue (Million), by Product 2024 & 2032

- Figure 56: Asia Pacific Medical Electronics Industry Volume (K Unit), by Product 2024 & 2032

- Figure 57: Asia Pacific Medical Electronics Industry Revenue Share (%), by Product 2024 & 2032

- Figure 58: Asia Pacific Medical Electronics Industry Volume Share (%), by Product 2024 & 2032

- Figure 59: Asia Pacific Medical Electronics Industry Revenue (Million), by Application 2024 & 2032

- Figure 60: Asia Pacific Medical Electronics Industry Volume (K Unit), by Application 2024 & 2032

- Figure 61: Asia Pacific Medical Electronics Industry Revenue Share (%), by Application 2024 & 2032

- Figure 62: Asia Pacific Medical Electronics Industry Volume Share (%), by Application 2024 & 2032

- Figure 63: Asia Pacific Medical Electronics Industry Revenue (Million), by End User 2024 & 2032

- Figure 64: Asia Pacific Medical Electronics Industry Volume (K Unit), by End User 2024 & 2032

- Figure 65: Asia Pacific Medical Electronics Industry Revenue Share (%), by End User 2024 & 2032

- Figure 66: Asia Pacific Medical Electronics Industry Volume Share (%), by End User 2024 & 2032

- Figure 67: Asia Pacific Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 68: Asia Pacific Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 69: Asia Pacific Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 70: Asia Pacific Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 71: Middle East and Africa Medical Electronics Industry Revenue (Million), by Product 2024 & 2032

- Figure 72: Middle East and Africa Medical Electronics Industry Volume (K Unit), by Product 2024 & 2032

- Figure 73: Middle East and Africa Medical Electronics Industry Revenue Share (%), by Product 2024 & 2032

- Figure 74: Middle East and Africa Medical Electronics Industry Volume Share (%), by Product 2024 & 2032

- Figure 75: Middle East and Africa Medical Electronics Industry Revenue (Million), by Application 2024 & 2032

- Figure 76: Middle East and Africa Medical Electronics Industry Volume (K Unit), by Application 2024 & 2032

- Figure 77: Middle East and Africa Medical Electronics Industry Revenue Share (%), by Application 2024 & 2032

- Figure 78: Middle East and Africa Medical Electronics Industry Volume Share (%), by Application 2024 & 2032

- Figure 79: Middle East and Africa Medical Electronics Industry Revenue (Million), by End User 2024 & 2032

- Figure 80: Middle East and Africa Medical Electronics Industry Volume (K Unit), by End User 2024 & 2032

- Figure 81: Middle East and Africa Medical Electronics Industry Revenue Share (%), by End User 2024 & 2032

- Figure 82: Middle East and Africa Medical Electronics Industry Volume Share (%), by End User 2024 & 2032

- Figure 83: Middle East and Africa Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 84: Middle East and Africa Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 85: Middle East and Africa Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 86: Middle East and Africa Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

- Figure 87: South America Medical Electronics Industry Revenue (Million), by Product 2024 & 2032

- Figure 88: South America Medical Electronics Industry Volume (K Unit), by Product 2024 & 2032

- Figure 89: South America Medical Electronics Industry Revenue Share (%), by Product 2024 & 2032

- Figure 90: South America Medical Electronics Industry Volume Share (%), by Product 2024 & 2032

- Figure 91: South America Medical Electronics Industry Revenue (Million), by Application 2024 & 2032

- Figure 92: South America Medical Electronics Industry Volume (K Unit), by Application 2024 & 2032

- Figure 93: South America Medical Electronics Industry Revenue Share (%), by Application 2024 & 2032

- Figure 94: South America Medical Electronics Industry Volume Share (%), by Application 2024 & 2032

- Figure 95: South America Medical Electronics Industry Revenue (Million), by End User 2024 & 2032

- Figure 96: South America Medical Electronics Industry Volume (K Unit), by End User 2024 & 2032

- Figure 97: South America Medical Electronics Industry Revenue Share (%), by End User 2024 & 2032

- Figure 98: South America Medical Electronics Industry Volume Share (%), by End User 2024 & 2032

- Figure 99: South America Medical Electronics Industry Revenue (Million), by Country 2024 & 2032

- Figure 100: South America Medical Electronics Industry Volume (K Unit), by Country 2024 & 2032

- Figure 101: South America Medical Electronics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 102: South America Medical Electronics Industry Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Medical Electronics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Medical Electronics Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Global Medical Electronics Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 4: Global Medical Electronics Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 5: Global Medical Electronics Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 6: Global Medical Electronics Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 7: Global Medical Electronics Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 8: Global Medical Electronics Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 9: Global Medical Electronics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Global Medical Electronics Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 11: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 15: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 17: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 19: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 21: Global Medical Electronics Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 22: Global Medical Electronics Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 23: Global Medical Electronics Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 24: Global Medical Electronics Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 25: Global Medical Electronics Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 26: Global Medical Electronics Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 27: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 29: United States Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: United States Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 31: Canada Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Canada Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 33: Mexico Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Mexico Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 35: Global Medical Electronics Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 36: Global Medical Electronics Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 37: Global Medical Electronics Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 38: Global Medical Electronics Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 39: Global Medical Electronics Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 40: Global Medical Electronics Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 41: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 43: Germany Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Germany Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: United Kingdom Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: United Kingdom Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 47: France Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: France Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 49: Italy Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Italy Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 51: Spain Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Spain Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 53: Rest of Europe Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Rest of Europe Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 55: Global Medical Electronics Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 56: Global Medical Electronics Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 57: Global Medical Electronics Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 58: Global Medical Electronics Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 59: Global Medical Electronics Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 60: Global Medical Electronics Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 61: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 62: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 63: China Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 64: China Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 65: Japan Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Japan Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 67: India Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 68: India Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 69: Australia Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 70: Australia Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 71: South Korea Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 72: South Korea Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 73: Rest of Asia Pacific Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Asia Pacific Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 75: Global Medical Electronics Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 76: Global Medical Electronics Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 77: Global Medical Electronics Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 78: Global Medical Electronics Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 79: Global Medical Electronics Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 80: Global Medical Electronics Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 81: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 82: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 83: GCC Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 84: GCC Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 85: South Africa Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 86: South Africa Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 87: Rest of Middle East and Africa Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 88: Rest of Middle East and Africa Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 89: Global Medical Electronics Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 90: Global Medical Electronics Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 91: Global Medical Electronics Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 92: Global Medical Electronics Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 93: Global Medical Electronics Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 94: Global Medical Electronics Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 95: Global Medical Electronics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 96: Global Medical Electronics Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 97: Brazil Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 98: Brazil Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 99: Argentina Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 100: Argentina Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 101: Rest of South America Medical Electronics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 102: Rest of South America Medical Electronics Industry Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Electronics Industry?

The projected CAGR is approximately 10.90%.

2. Which companies are prominent players in the Medical Electronics Industry?

Key companies in the market include Siemens Healthcare GmbH, Drägerwerk AG & Co KGaA, Esaote SpA, Hologic Inc, GE Healthcare, Getinge Inc, Medtronic PLC, Fujifilm Corporation, Mindray Medical International Limited, Koninklijke Philips NV, Canon Medical Systems, McKesson Corporation, Olympus Corporation.

3. What are the main segments of the Medical Electronics Industry?

The market segments include Product, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Geriatric Population; Rising Application of Imaging Devices.

6. What are the notable trends driving market growth?

MRI Segment Expected to Hold Significant Market Share in the Medical Electronics Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Ramped up regulatory scrutiny; High Cost and Maintenance.

8. Can you provide examples of recent developments in the market?

In August 2022, the South Korean Ministry of Food and Drug Safety granted clearance to VUNO, a medical artificial intelligence company, for its ECG device, Hativ Pro, a portable medical device that measures a user's heart rate and sends this data through a connected mobile phone app.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Electronics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Electronics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Electronics Industry?

To stay informed about further developments, trends, and reports in the Medical Electronics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence