Key Insights

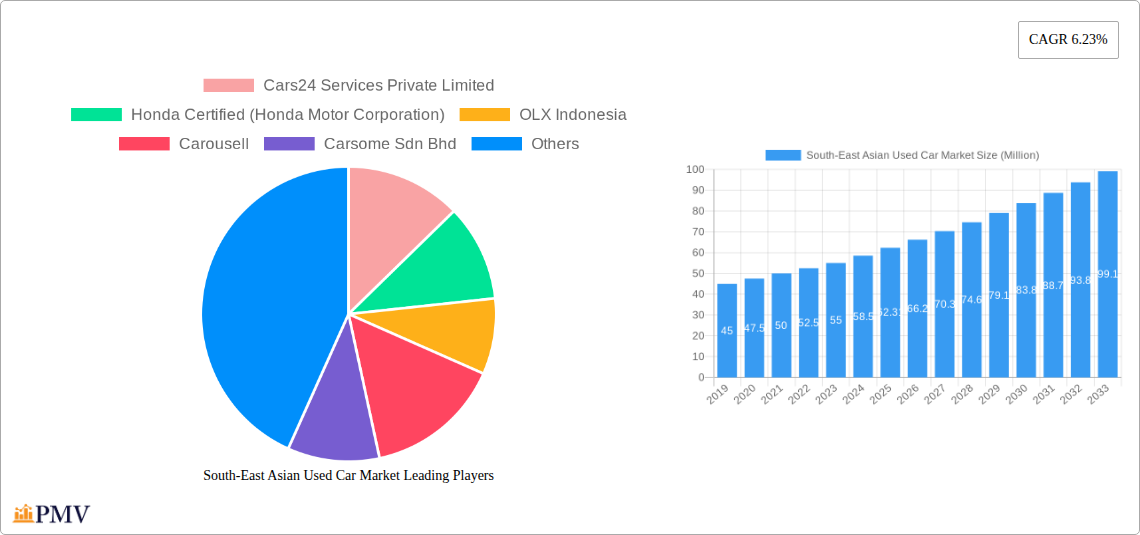

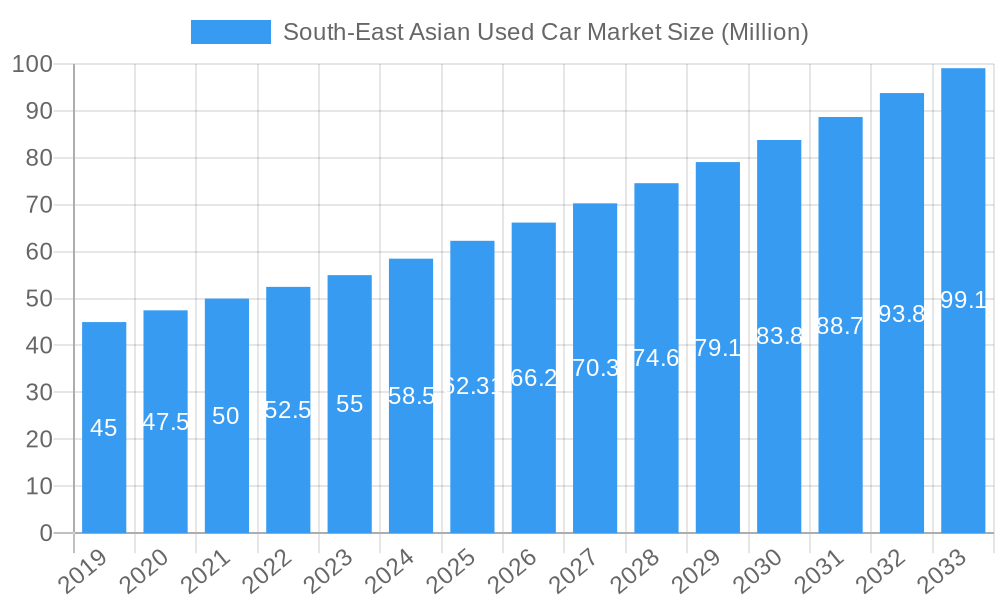

The South-East Asian used car market is poised for substantial growth, projected to reach an estimated market size of USD 62.31 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.23% anticipated throughout the forecast period of 2025-2033. This expansion is fueled by a confluence of factors, including increasing disposable incomes across key South-East Asian nations, a growing preference for affordable mobility solutions, and the burgeoning influence of organized online platforms that enhance trust and convenience in the used car buying process. The market's dynamism is further underscored by a diverse range of vehicle types, from fuel-efficient hatchbacks and sedans to versatile SUVs and MPVs, catering to the varied needs of consumers. Similarly, the proliferation of different fuel types, including gasoline, diesel, and increasingly, electric vehicles, alongside alternative fuels like LPG and CNG, reflects a market adapting to evolving environmental regulations and consumer preferences. The shift towards online sales channels is a significant trend, democratizing access to pre-owned vehicles and streamlining transactions, which in turn is driving the growth of organized vendor types over their unorganized counterparts. The prevalence of outright purchases, coupled with accessible financing options through captive financing, banks, and NBFCs, further stimulates market activity by making vehicle ownership more attainable for a broader segment of the population.

South-East Asian Used Car Market Market Size (In Million)

The competitive landscape is characterized by the presence of both established automotive manufacturers with certified pre-owned programs, such as Honda Certified and Toyota Trust, and agile online used car marketplaces like Cars24, OLX Indonesia, Carousell, Carsome, and iCar Asia. These players are actively innovating to address market restraints such as perceived risks associated with used vehicle quality and the need for greater transparency. Strategies like rigorous vehicle inspections, extended warranties, and transparent pricing models are crucial in building consumer confidence. The geographical focus on South-East Asia, encompassing dynamic economies like Indonesia, Malaysia, Singapore, Thailand, Vietnam, Philippines, Myanmar, Cambodia, and Laos, presents a vast and largely untapped potential. As these economies continue to develop, the demand for reliable and affordable transportation will only intensify, making the used car segment a critical component of the automotive ecosystem in the region. The interplay of these drivers, trends, and strategic initiatives by key companies suggests a thriving market characterized by technological adoption, evolving consumer behavior, and sustained economic development.

South-East Asian Used Car Market Company Market Share

Unlocking the Potential: South-East Asian Used Car Market Analysis 2019–2033

This comprehensive report delves deep into the burgeoning South-East Asian used car market, providing an in-depth analysis from 2019 to 2033. Covering historical trends, the base year of 2025, and an extensive forecast period, this study offers unparalleled insights for automotive stakeholders, investors, and policymakers. We meticulously examine market structure, competitive dynamics, industry trends, dominant segments, product innovations, key drivers, challenges, and the strategic outlook of this dynamic sector. With a focus on actionable intelligence and high-ranking SEO keywords, this report is your definitive guide to navigating the evolving landscape of pre-owned vehicles across South-East Asia.

South-East Asian Used Car Market Market Structure & Competitive Dynamics

The South-East Asian used car market exhibits a dynamic and evolving structure, characterized by a moderate level of market concentration. While established organized used car platforms and OEM-certified pre-owned programs are gaining significant traction, the unorganized used car vendor segment, comprising independent dealerships and individual sellers, still holds a substantial market share. Innovation ecosystems are rapidly developing, driven by online used car platforms that leverage technology to enhance transparency, convenience, and accessibility for buyers. Regulatory frameworks are becoming more sophisticated, with governments increasingly focusing on consumer protection and vehicle standardization, impacting both outright purchase and financed purchase models. Product substitutes, such as new vehicle sales and alternative transportation solutions, exert a constant influence, but the inherent cost-effectiveness of pre-owned vehicles continues to drive demand. End-user trends are shifting towards digital engagement, with a growing preference for online research and, increasingly, online purchasing. Mergers and acquisitions (M&A) activities are on the rise as larger players seek to consolidate their market positions and expand their geographical reach. For instance, recent M&A deals in the region have valued at over USD 50 Million, signaling significant investor confidence. Key market players are actively pursuing strategies to capture market share, estimated to be over 25% for leading organized players in key urban centers.

South-East Asian Used Car Market Industry Trends & Insights

The South-East Asian used car market is experiencing robust growth, fueled by a confluence of economic, technological, and social factors. The CAGR of the market is projected to be a healthy 8.5% over the forecast period. This growth is primarily driven by increasing disposable incomes, a growing middle class, and a persistent demand for affordable personal mobility solutions. Technological disruptions are at the forefront, with online used car platforms like Carsome, Carro, and OLX Indonesia revolutionizing the buying and selling experience. These platforms are employing advanced digital tools for vehicle valuation, inspection, financing, and nationwide delivery, significantly improving market transparency and efficiency. Consumer preferences are evolving rapidly; buyers are increasingly digital-native, seeking seamless online interfaces, comprehensive vehicle history reports, and flexible financing options, including captive financing, bank financing, and solutions from non-banking financial corporations (NBFCs). The competitive dynamics are intensifying, with both online and offline players striving to differentiate through service quality, pricing, and brand trust. OEMs are also actively participating with their certified pre-owned programs, such as Honda Certified and Toyota Trust, to leverage their brand reputation and customer loyalty. The penetration of digital channels in the used car market is expected to reach 60% by 2028, a significant leap from 35% in 2023. The increasing popularity of Sports Utility Vehicles (SUVs) and Multi-Purpose Utility Vehicles (MPVs), driven by family needs and lifestyle trends, is also shaping inventory and demand patterns. The market is also witnessing a gradual, albeit nascent, adoption of electric vehicle segments within the used car space, influenced by government incentives and growing environmental awareness, although gasoline and diesel fueled vehicles continue to dominate.

Dominant Markets & Segments in South-East Asian Used Car Market

The South-East Asian used car market is characterized by distinct dominant markets and segments, each contributing to the overall growth and evolution of the sector.

- Leading Region & Country: Singapore and Malaysia currently lead in terms of market maturity and penetration of organized players, primarily due to established economic stability and a higher adoption rate of digital services. However, Indonesia and Vietnam are emerging as high-growth markets, driven by their large populations and rapidly expanding middle classes. The market penetration in these emerging economies is projected to accelerate significantly in the coming years.

- Vehicle Type Dominance:

- Sports Utility Vehicle (SUV): SUVs are currently the most dominant vehicle type in the used car market across South-East Asia. This is driven by the region's diverse terrain, growing family sizes, and aspiration for vehicles that offer versatility and a commanding presence. Sales of used SUVs are expected to account for approximately 35% of the total used car market by 2025.

- Sedan: Sedans remain a strong contender, particularly in urban areas, offering a balance of fuel efficiency and comfort for daily commutes. They represent a significant segment, projected to hold around 28% of the market.

- Hatchback: Hatchbacks appeal to budget-conscious buyers and younger demographics due to their affordability and maneuverability in congested city environments. Their market share is estimated at 22%.

- Multi-Purpose Utility Vehicle (MPV): MPVs cater to larger families and are gaining popularity, reflecting changing demographic needs. Their share is currently around 15%.

- Fuel Type Dynamics:

- Gasoline: Gasoline-powered vehicles continue to dominate the used car market, constituting an estimated 70% of all sales, owing to their widespread availability and established refueling infrastructure.

- Diesel: Diesel vehicles hold a significant, though gradually declining, share, estimated at 25%, primarily in commercial applications and larger SUVs.

- Electric: Electric vehicles in the used market are still nascent, with a market share of less than 1%, but are projected for significant growth.

- Other Fuel Types (LPG, CNG, Etc.): These segments are niche, collectively representing less than 4% of the market.

- Sales Channel Preferences:

- Online: The online sales channel is experiencing exponential growth, driven by convenience, transparency, and wider inventory access. Its market share is projected to reach 60% by 2028.

- Offline: Offline channels, including traditional dealerships and physical marketplaces, still play a crucial role, especially for buyers who prefer in-person inspections. They currently hold a 40% share but are expected to see a gradual decline relative to online channels.

- Vendor Type Landscape:

- Organized: Organized vendors, including large dealerships and online platforms like Cars24, Carousell, and PT Moladin Digita, are increasingly dominating due to their structured processes, warranties, and financing options. Their market share is steadily increasing, projected to exceed 55% by 2026.

- Unorganized: Unorganized vendors, comprising independent used car dealers and individual sellers, still represent a significant portion of the market, particularly in smaller towns and for budget-focused transactions.

- Purchase Method Evolution:

- Financed Purchase: Financed Purchase is the prevailing method, accounting for over 75% of transactions. This includes:

- Captive Financing: Offered by OEMs and larger dealerships, contributing around 30% of financed sales.

- Bank Financing: Traditional bank loans remain a significant component, around 40%.

- Non-banking Financial Corporations (NBFCs): NBFCs are increasingly catering to a wider segment of buyers with more flexible, albeit sometimes higher-interest, loan products, accounting for approximately 30% of financed sales.

- Outright Purchase: Outright Purchase, while less common, still constitutes about 25% of transactions, often by buyers with readily available capital or for lower-value vehicles.

- Financed Purchase: Financed Purchase is the prevailing method, accounting for over 75% of transactions. This includes:

South-East Asian Used Car Market Product Innovations

Product innovations in the South-East Asian used car market are primarily focused on enhancing transparency, convenience, and trust for consumers. Leading players like Carsome and Carro are investing in advanced digital inspection technologies, utilizing AI-powered tools to provide detailed vehicle condition reports, thereby mitigating buyer concerns about undisclosed defects. The integration of blockchain technology for vehicle history tracking is an emerging trend, aiming to create an immutable record of a car's lifecycle. Furthermore, innovative service offerings such as nationwide doorstep delivery, extended warranties, and buy-back guarantees are becoming standard, adding significant value and competitive advantage. The development of sophisticated online financing portals, enabling quick approvals and personalized loan options from various financial institutions, is another key innovation that is streamlining the purchase process. These product developments are directly addressing market friction points and driving increased adoption of organized used car channels.

Report Segmentation & Scope

This report segments the South-East Asian used car market across critical dimensions to provide granular insights. The scope encompasses:

- Vehicle Type: Analysis includes Hatchback, Sedan, Sports Utility Vehicle (SUV), and Multi-Purpose Utility Vehicle (MPV), detailing their respective market sizes, growth projections, and competitive dynamics within the used car segment.

- Fuel Type: We examine Gasoline, Diesel, Electric, and Other Fuel Types (LPG, CNG, Etc.), evaluating their current market share, future trends, and the impact of evolving environmental regulations.

- Sales Channel: The report differentiates between Online and Offline sales channels, projecting their market penetration and analyzing the strategies driving their growth or decline.

- Vendor Type: A clear distinction is made between Organized and Unorganized vendors, assessing their market influence, competitive advantages, and potential for consolidation.

- Purchase Method: We delve into Outright Purchase and Financed Purchase, further dissecting financed options into Captive Financing, Bank Financing, and Non-banking Financial Corporations (NBFCs), providing insights into their market share and strategic importance.

Key Drivers of South-East Asian Used Car Market Growth

The South-East Asian used car market's growth is propelled by several key factors. Firstly, a burgeoning middle class with increasing disposable incomes seeks affordable personal mobility, making pre-owned vehicles an attractive option. Secondly, rapid urbanization and a growing demand for private transportation in densely populated cities further fuel this demand. Thirdly, the digital transformation of the region, with widespread smartphone penetration and internet access, has enabled the rise of online used car platforms, enhancing transparency, accessibility, and convenience. Fourthly, a range of flexible financing options, including captive financing, bank financing, and NBFC loans, has made vehicle ownership more attainable for a broader segment of the population. Finally, favorable government policies and initiatives aimed at boosting economic activity and providing consumer protection contribute to a more stable and predictable market environment.

Challenges in the South-East Asian Used Car Market Sector

Despite its strong growth trajectory, the South-East Asian used car market faces several significant challenges. A persistent issue is the lack of standardization and transparency in pricing and vehicle condition reporting, particularly within the unorganized sector, leading to potential consumer distrust. Supply chain disruptions, exacerbated by global manufacturing issues and logistical complexities, can impact the availability of desirable used car models. Regulatory hurdles and varying compliance standards across different countries within the region can also create operational complexities for cross-border players. Intense competition from both organized and unorganized players, coupled with the pressure to maintain competitive pricing while investing in technology and service enhancements, presents ongoing challenges for profitability. Furthermore, the nascent stage of the used electric vehicle market poses challenges related to battery diagnostics, charging infrastructure availability, and specialized repair expertise.

Leading Players in the South-East Asian Used Car Market Market

- Cars24 Services Private Limited

- Honda Certified (Honda Motor Corporation)

- OLX Indonesia

- Carousell

- Carsome Sdn Bhd

- PT Moladin Digita

- Toyota Trust (Toyota Motor Corporation)

- Nissan Intelligent Mobility (Nissan Motor Corporation)

- ICar Asia Limited

- Carro (Trusty Cars Pte Ltd)

Key Developments in South-East Asian Used Car Market Sector

- April 2022: Spinny, a prominent used car buying and selling platform, made a significant entry into the luxury used vehicle segment under its "Spinnymax" brand in the Vietnamese market. This expansion signifies a strategic move to capture a high-value segment and operate nationally, offering a wide array of luxury vehicles from brands like Mercedes-Benz, BMW, Audi, Jaguar, and Land Rover, supported by an extensive delivery network across 250 cities.

- January 2022: Moladin, a leading Indonesian used car platform, successfully secured USD 42 Million in Series A funding. This substantial investment, spearheaded by prominent venture capital firms Sequoia Capital India and Northstar Group, underscores the significant investor confidence in the growth potential of digital used car platforms in South-East Asia and will likely fuel further expansion and technological advancements.

Strategic South-East Asian Used Car Market Market Outlook

The strategic outlook for the South-East Asian used car market remains exceptionally positive, driven by ongoing economic development and evolving consumer behavior. Growth accelerators include the continued expansion of digital platforms, which will further enhance market transparency and accessibility, making used car purchases as convenient as new car transactions. The increasing focus on sustainability and affordability will continue to drive demand for pre-owned vehicles, especially as consumers become more environmentally conscious. Strategic opportunities lie in expanding financing solutions to cater to a wider demographic, including first-time buyers and those with non-traditional credit profiles. Investments in robust inspection technologies and post-sales services will be crucial for building enduring customer trust. Furthermore, the gradual emergence of the used electric vehicle market presents a significant long-term growth avenue, requiring strategic planning for infrastructure development and specialized service offerings. This dynamic market is poised for sustained expansion, offering lucrative opportunities for well-positioned stakeholders.

South-East Asian Used Car Market Segmentation

-

1. Vehicle Type

- 1.1. Hatchback

- 1.2. Sedan

- 1.3. Sports Utility Vehicle (SUV)

- 1.4. Multi-Purpose Utility Vehicle (MPV)

-

2. Fuel Type

- 2.1. Gasoline

- 2.2. Diesel

- 2.3. Electric

- 2.4. Other Fuel Types (LPG, CNG, Etc.)

-

3. Sales Channel

- 3.1. Online

- 3.2. Offline

-

4. Vendor Type

- 4.1. Organized

- 4.2. Unorganized

-

5. Purchase Method

- 5.1. Outright Purchase

-

5.2. Financed Purchase

- 5.2.1. Captive Financing

- 5.2.2. Bank Financing

- 5.2.3. Non-banking Financial Corporations (NBFC)

South-East Asian Used Car Market Segmentation By Geography

-

1. South East Asia

- 1.1. Indonesia

- 1.2. Malaysia

- 1.3. Singapore

- 1.4. Thailand

- 1.5. Vietnam

- 1.6. Philippines

- 1.7. Myanmar

- 1.8. Cambodia

- 1.9. Laos

South-East Asian Used Car Market Regional Market Share

Geographic Coverage of South-East Asian Used Car Market

South-East Asian Used Car Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Hatchback

- 5.1.2. Sedan

- 5.1.3. Sports Utility Vehicle (SUV)

- 5.1.4. Multi-Purpose Utility Vehicle (MPV)

- 5.2. Market Analysis, Insights and Forecast - by Fuel Type

- 5.2.1. Gasoline

- 5.2.2. Diesel

- 5.2.3. Electric

- 5.2.4. Other Fuel Types (LPG, CNG, Etc.)

- 5.3. Market Analysis, Insights and Forecast - by Sales Channel

- 5.3.1. Online

- 5.3.2. Offline

- 5.4. Market Analysis, Insights and Forecast - by Vendor Type

- 5.4.1. Organized

- 5.4.2. Unorganized

- 5.5. Market Analysis, Insights and Forecast - by Purchase Method

- 5.5.1. Outright Purchase

- 5.5.2. Financed Purchase

- 5.5.2.1. Captive Financing

- 5.5.2.2. Bank Financing

- 5.5.2.3. Non-banking Financial Corporations (NBFC)

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. South East Asia

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. South-East Asian Used Car Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Hatchback

- 6.1.2. Sedan

- 6.1.3. Sports Utility Vehicle (SUV)

- 6.1.4. Multi-Purpose Utility Vehicle (MPV)

- 6.2. Market Analysis, Insights and Forecast - by Fuel Type

- 6.2.1. Gasoline

- 6.2.2. Diesel

- 6.2.3. Electric

- 6.2.4. Other Fuel Types (LPG, CNG, Etc.)

- 6.3. Market Analysis, Insights and Forecast - by Sales Channel

- 6.3.1. Online

- 6.3.2. Offline

- 6.4. Market Analysis, Insights and Forecast - by Vendor Type

- 6.4.1. Organized

- 6.4.2. Unorganized

- 6.5. Market Analysis, Insights and Forecast - by Purchase Method

- 6.5.1. Outright Purchase

- 6.5.2. Financed Purchase

- 6.5.2.1. Captive Financing

- 6.5.2.2. Bank Financing

- 6.5.2.3. Non-banking Financial Corporations (NBFC)

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Cars24 Services Private Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Honda Certified (Honda Motor Corporation)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 OLX Indonesia

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Carousell

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Carsome Sdn Bhd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PT Moladin Digita

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Toyota Trust (Toyota Motor Corporation)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Nissan Intelligent Mobility (Nissan Motor Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ICar Asia Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Carro (Trusty Cars Pte Ltd)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Cars24 Services Private Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South-East Asian Used Car Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South-East Asian Used Car Market Share (%) by Company 2025

List of Tables

- Table 1: South-East Asian Used Car Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: South-East Asian Used Car Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 3: South-East Asian Used Car Market Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 4: South-East Asian Used Car Market Revenue Million Forecast, by Vendor Type 2020 & 2033

- Table 5: South-East Asian Used Car Market Revenue Million Forecast, by Purchase Method 2020 & 2033

- Table 6: South-East Asian Used Car Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: South-East Asian Used Car Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 8: South-East Asian Used Car Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 9: South-East Asian Used Car Market Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 10: South-East Asian Used Car Market Revenue Million Forecast, by Vendor Type 2020 & 2033

- Table 11: South-East Asian Used Car Market Revenue Million Forecast, by Purchase Method 2020 & 2033

- Table 12: South-East Asian Used Car Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Indonesia South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Malaysia South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Singapore South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Thailand South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Vietnam South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Philippines South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Myanmar South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Cambodia South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Laos South-East Asian Used Car Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South-East Asian Used Car Market?

The projected CAGR is approximately 6.23%.

2. Which companies are prominent players in the South-East Asian Used Car Market?

Key companies in the market include Cars24 Services Private Limited, Honda Certified (Honda Motor Corporation), OLX Indonesia, Carousell, Carsome Sdn Bhd, PT Moladin Digita, Toyota Trust (Toyota Motor Corporation), Nissan Intelligent Mobility (Nissan Motor Corporation, ICar Asia Limited, Carro (Trusty Cars Pte Ltd).

3. What are the main segments of the South-East Asian Used Car Market?

The market segments include Vehicle Type, Fuel Type, Sales Channel, Vendor Type, Purchase Method.

4. Can you provide details about the market size?

The market size is estimated to be USD 62.31 Million as of 2022.

5. What are some drivers contributing to market growth?

Expanding Distribution Channels; Others.

6. What are the notable trends driving market growth?

Strengthening of Digital Platforms is Driving the Online Booking Segment.

7. Are there any restraints impacting market growth?

Lack Of Trust And Transparency; Others.

8. Can you provide examples of recent developments in the market?

April 2022: Spinny, a used car buying and selling platform, entered the luxury car used vehicle segment under the Spinnymax brand in the Vietnamese market. The platform will operate at a national scale and offers over 500 cars from various brands, including Mercedes-Benz, BMW, Audi, Jaguar, and Land Rover, with an all-India delivery service through 250 cities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South-East Asian Used Car Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South-East Asian Used Car Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South-East Asian Used Car Market?

To stay informed about further developments, trends, and reports in the South-East Asian Used Car Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence