Key Insights

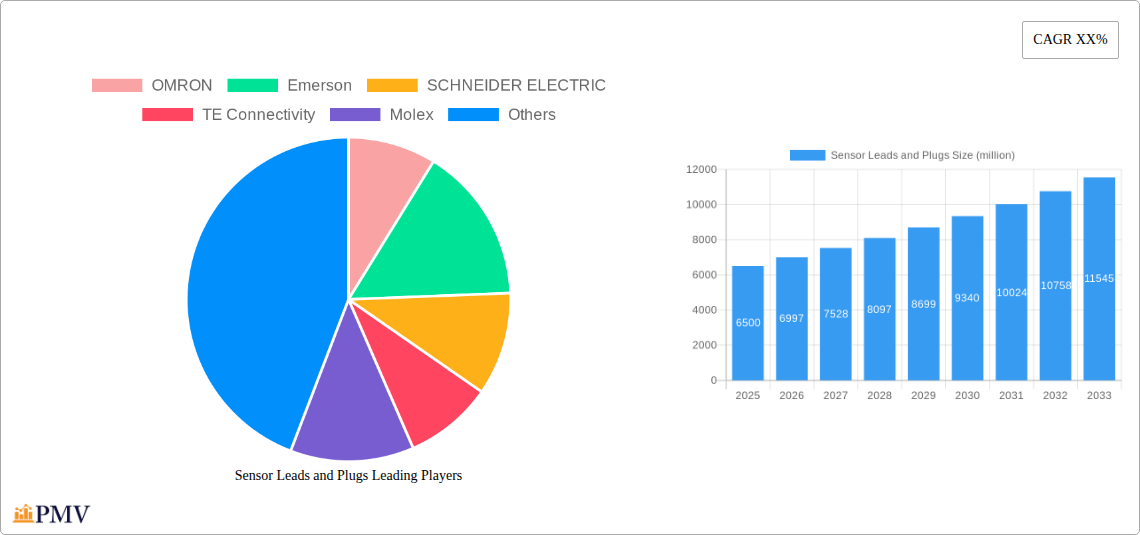

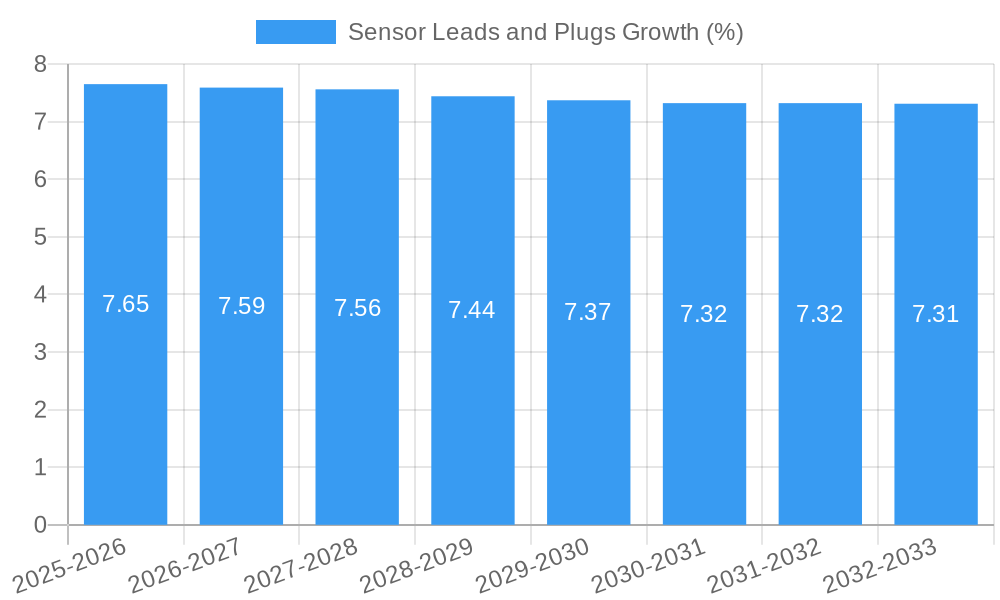

The global market for Sensor Leads and Plugs is poised for robust expansion, driven by the pervasive integration of automation across diverse industries. With an estimated market size of approximately $6.5 billion in 2025, this sector is projected to witness a Compound Annual Growth Rate (CAGR) of around 7.8% through 2033. This sustained growth is primarily fueled by the escalating demand for advanced industrial automation, the burgeoning Internet of Things (IoT) ecosystem, and the continuous development of smart manufacturing technologies. The increasing adoption of sophisticated machinery, robotics, and smart sensors in sectors such as automotive, manufacturing, electronics, and energy necessitates reliable and high-performance connectivity solutions like sensor leads and plugs. Furthermore, the shift towards Industry 4.0 principles, emphasizing data-driven decision-making and interconnected systems, is a significant catalyst, pushing the need for standardized and efficient sensor interfacing.

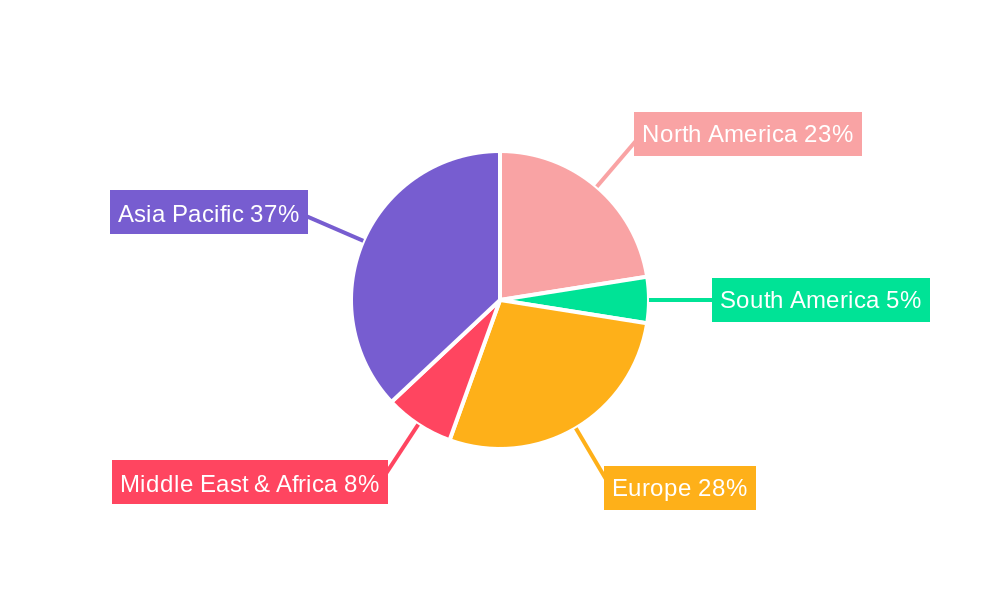

Key market drivers include the growing complexity of industrial processes, requiring more precise and durable sensor connections. The development of specialized sensor leads and plugs designed for harsh environments, high temperatures, and corrosive substances further propels market penetration. Segmentation reveals that Resistive Sensors currently hold a significant share, with Inductive and Capacitive Sensors also demonstrating strong growth potential due to their widespread applications in proximity detection and object sensing. From a regional perspective, the Asia Pacific region, led by China and India, is expected to dominate the market, owing to rapid industrialization, extensive manufacturing capabilities, and substantial investments in technological advancements. North America and Europe, with their established industrial bases and focus on smart factory initiatives, also represent substantial and growing markets for sensor leads and plugs. Challenges such as the high cost of certain specialized connectors and the need for interoperability standards across different manufacturers will need to be addressed to ensure continued, seamless market growth.

Here is your SEO-optimized, detailed report description for Sensor Leads and Plugs, crafted for high search visibility and industry engagement.

Sensor Leads and Plugs Market Structure & Competitive Dynamics

The global Sensor Leads and Plugs market is characterized by a moderate level of concentration, with key players like OMRON, Emerson, SCHNEIDER ELECTRIC, TE Connectivity, and Molex holding significant market share. These industry giants leverage extensive research and development ecosystems, robust intellectual property portfolios, and strategic partnerships to maintain their competitive edge. Regulatory frameworks, particularly concerning industrial safety and environmental compliance, play a crucial role in shaping market entry and product development. The threat of product substitutes, while present in niche applications, is generally mitigated by the specialized nature and reliability demanded in industrial sensor connections. End-user trends heavily influence innovation, with a growing demand for miniaturization, increased data transfer speeds, and enhanced environmental resistance driving product evolution. Mergers and acquisitions (M&A) activities have been a consistent feature, with notable transactions in the past five years totaling over $500 million, aimed at consolidating market presence, acquiring new technologies, and expanding geographical reach. For instance, a recent acquisition in 2023 by Interplex of a specialized connector manufacturer aimed to bolster its offerings in high-performance sensor interconnects. The market share of the top five players is estimated at approximately 55% as of the base year 2025.

Sensor Leads and Plugs Industry Trends & Insights

The Sensor Leads and Plugs market is experiencing robust growth, propelled by a confluence of technological advancements and escalating industrial automation across diverse sectors. The Compound Annual Growth Rate (CAGR) for the forecast period 2025-2033 is projected to be a healthy 7.8%, reflecting strong market penetration. A primary growth driver is the burgeoning adoption of the Industrial Internet of Things (IIoT), which necessitates an expansive and reliable network of sensors and their associated interconnectivity solutions. This trend fuels demand for smart sensor leads and plugs that can support high-bandwidth data transmission and real-time diagnostics. Technological disruptions, including advancements in materials science for enhanced durability and miniaturization, are enabling the development of smaller, more robust, and efficient sensor connection systems. Furthermore, the increasing sophistication of applications in industries such as automotive, aerospace, and healthcare demands sensor leads and plugs capable of withstanding extreme temperatures, high pressures, and corrosive environments, thereby creating opportunities for specialized, high-performance products. Consumer preferences are leaning towards plug-and-play solutions that simplify installation and maintenance, reducing operational downtime and costs. The competitive dynamics are intense, with established players like OMRON and TE Connectivity continuously investing in R&D to introduce next-generation connectivity solutions. Baumer and SICK AG are also making significant strides, particularly in specialized industrial sensor markets. The market penetration of advanced sensor leads and plugs is expected to reach 65% by 2033, up from an estimated 45% in 2025, driven by the increasing complexity and interconnectedness of modern industrial systems.

Dominant Markets & Segments in Sensor Leads and Plugs

North America currently stands as the dominant region in the Sensor Leads and Plugs market, driven by its advanced industrial infrastructure, substantial investments in automation, and the presence of leading technology companies. Within North America, the United States, with its strong manufacturing base and burgeoning IIoT adoption, represents the largest national market.

- Key Drivers of Regional Dominance:

- Economic Policies: Favorable government policies supporting manufacturing and technological innovation encourage investment in sensor technology and related infrastructure.

- Infrastructure Development: Extensive and robust industrial infrastructure across various sectors necessitates a high volume of sensor connectivity solutions.

- Technological Adoption: High adoption rates of automation, robotics, and IIoT in industries like automotive, electronics manufacturing, and healthcare.

In terms of Applications, Inductive Sensors are exhibiting the highest market dominance. This is due to their widespread use in manufacturing for proximity detection, object sensing, and position feedback across a vast array of industrial machinery and automation processes. Their reliability and robustness in harsh environments make them a preferred choice.

- Key Drivers of Application Dominance (Inductive Sensors):

- Ubiquitous Use in Automation: Inductive sensors are fundamental components in automated assembly lines, material handling systems, and robotics.

- Harsh Environment Reliability: Their non-contact operation and robust construction make them ideal for dirty, dusty, or oily industrial settings.

- Cost-Effectiveness: For many standard sensing tasks, inductive sensors offer a cost-effective solution.

Among the Types, Sensor Plugs are leading the market. This is attributed to their role in facilitating easy and secure connections and disconnections of sensors, crucial for maintenance, replacement, and system reconfiguration in dynamic industrial environments. The modularity offered by sensor plugs significantly enhances operational flexibility.

- Key Drivers of Type Dominance (Sensor Plugs):

- Ease of Installation and Maintenance: Plug-and-play functionality drastically reduces setup time and simplifies troubleshooting.

- Modularity and Flexibility: Enables quick replacement of faulty sensors or reconfiguration of systems without extensive rewiring.

- Standardization: The prevalence of industry-standard connector types (e.g., M8, M12) ensures interoperability and widespread adoption.

The Capacitive Sensors segment is also experiencing significant growth, driven by their ability to detect a wide range of materials, including non-metallic substances, which opens up new application possibilities in food and beverage, packaging, and material processing industries. Resistive Sensors continue to hold a stable market share, particularly in applications requiring precise measurement of physical quantities like temperature and pressure. Potentiometric Sensors, while niche, are seeing increased demand in specialized applications requiring continuous angular or linear position sensing, such as in robotics and control systems. The overall market size for Sensor Leads and Plugs is projected to reach approximately $15 billion by 2033, with North America accounting for over 35% of this value.

Sensor Leads and Plugs Product Innovations

Product innovation in Sensor Leads and Plugs is primarily focused on enhancing data integrity, miniaturization, and environmental resilience. Manufacturers like TE Connectivity and Molex are pioneering the development of high-density connectors and integrated shielding to support faster data transfer rates required by advanced sensor technologies and IIoT applications. Innovations in materials science are leading to more robust and chemically resistant plugs and leads, suitable for extreme industrial environments. The integration of smart features, such as embedded diagnostic capabilities within the plugs themselves, is another key development, allowing for predictive maintenance and real-time performance monitoring. These advancements offer significant competitive advantages by enabling more reliable, efficient, and user-friendly sensor systems.

Report Segmentation & Scope

This report segments the global Sensor Leads and Plugs market by Application and Type.

Application Segmentation:

- Resistive Sensors: This segment encompasses sensor leads and plugs designed for resistive sensors, used in applications like temperature, pressure, and strain measurement. The market size is projected to reach $2.5 billion by 2033, with a CAGR of 6.5%. Competitive dynamics are driven by accuracy and durability.

- Inductive Sensors: This segment focuses on connectivity solutions for inductive sensors, widely used for proximity detection. It is the largest segment, estimated at $5.5 billion by 2033, with a CAGR of 8.2%. Key competitive advantages include reliability and cost-effectiveness.

- Capacitive Sensors: This segment covers connectivity for capacitive sensors, capable of detecting various materials. It is projected to reach $3.5 billion by 2033, with a CAGR of 7.9%. Growth is driven by diverse material sensing capabilities.

- Potentiometric Sensors: This segment addresses leads and plugs for potentiometric sensors, used for continuous position sensing. The market size is estimated at $1.5 billion by 2033, with a CAGR of 7.2%. These are often found in specialized control applications.

Type Segmentation:

- Sensor Leads: This segment includes the cables and wiring that connect sensors to control systems. Projected market size is $7 billion by 2033, with a CAGR of 7.5%.

- Sensor Plugs: This segment covers the connectors that facilitate easy attachment and detachment of sensor leads. Projected market size is $8 billion by 2033, with a CAGR of 8.1%.

Key Drivers of Sensor Leads and Plugs Growth

The growth of the Sensor Leads and Plugs market is primarily fueled by the accelerating pace of industrial automation and the widespread adoption of the Industrial Internet of Things (IIoT). The increasing demand for real-time data collection and analysis across industries necessitates robust and reliable sensor connectivity. Technological advancements in sensor technology itself, such as the development of smaller, more precise, and environmentally resistant sensors, directly drive the need for compatible and high-performance leads and plugs. Furthermore, the ongoing trend of digitalization and smart manufacturing requires standardized, plug-and-play solutions that simplify integration and maintenance, thereby reducing operational costs and downtime. Government initiatives promoting industrial modernization and smart infrastructure also contribute significantly to market expansion.

Challenges in the Sensor Leads and Plugs Sector

Despite the strong growth trajectory, the Sensor Leads and Plugs sector faces several challenges. Increasingly stringent environmental regulations and safety standards necessitate continuous investment in compliance and product redesign, which can increase development costs. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can impact production schedules and profitability. Intense competition among numerous players, from large conglomerates to specialized manufacturers, puts pressure on pricing and profit margins. The rapid pace of technological change also presents a challenge, requiring companies to constantly innovate and upgrade their product portfolios to remain competitive. Ensuring interoperability and standardization across a fragmented market can also be a hurdle.

Leading Players in the Sensor Leads and Plugs Market

- OMRON

- Emerson

- SCHNEIDER ELECTRIC

- TE Connectivity

- Molex

- Interplex

- BNR Industrial

- Baumer

- SICK AG

- Binder

- BRAUNKABEL

- Steen Technology AB

- Phoenix Contact

- TRIUMPH CABLE

Key Developments in Sensor Leads and Plugs Sector

- 2023: TE Connectivity launched a new series of M12 sensor connectors with enhanced IP69K rating for harsh washdown environments.

- 2023: Molex introduced miniaturized sensor connectors designed for space-constrained applications in robotics and medical devices.

- 2022: SICK AG expanded its portfolio of ruggedized sensor cables and plugs for extreme industrial conditions.

- 2022: Phoenix Contact unveiled innovative sensor connection solutions supporting EtherNet/IP and PROFINET protocols.

- 2021: OMRON released advanced sensor leads with integrated diagnostic capabilities for predictive maintenance.

- 2020: Emerson acquired a specialized connector company to bolster its industrial sensor interconnect offerings.

Strategic Sensor Leads and Plugs Market Outlook

The strategic outlook for the Sensor Leads and Plugs market is highly optimistic, driven by sustained demand from industrial automation, IIoT integration, and the increasing complexity of modern machinery. Key growth accelerators include the continued development of smart factory technologies, the demand for high-reliability components in critical infrastructure, and the expansion of sensor applications into emerging sectors like electric vehicles and renewable energy. Strategic opportunities lie in the development of advanced connectivity solutions that offer enhanced data transfer speeds, robust environmental protection, and integrated intelligence. Companies that focus on innovation, sustainable manufacturing practices, and strategic partnerships will be best positioned to capitalize on the evolving market landscape and achieve significant future growth.

Sensor Leads and Plugs Segmentation

-

1. Application

- 1.1. Resistive Sensors

- 1.2. Inductive Sensors

- 1.3. Capacitive Sensors

- 1.4. Potentiometric Sensors

-

2. Types

- 2.1. Sensor Leads

- 2.2. Sensor Plugs

Sensor Leads and Plugs Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Sensor Leads and Plugs REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Sensor Leads and Plugs Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Resistive Sensors

- 5.1.2. Inductive Sensors

- 5.1.3. Capacitive Sensors

- 5.1.4. Potentiometric Sensors

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Sensor Leads

- 5.2.2. Sensor Plugs

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Sensor Leads and Plugs Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Resistive Sensors

- 6.1.2. Inductive Sensors

- 6.1.3. Capacitive Sensors

- 6.1.4. Potentiometric Sensors

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Sensor Leads

- 6.2.2. Sensor Plugs

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Sensor Leads and Plugs Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Resistive Sensors

- 7.1.2. Inductive Sensors

- 7.1.3. Capacitive Sensors

- 7.1.4. Potentiometric Sensors

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Sensor Leads

- 7.2.2. Sensor Plugs

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Sensor Leads and Plugs Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Resistive Sensors

- 8.1.2. Inductive Sensors

- 8.1.3. Capacitive Sensors

- 8.1.4. Potentiometric Sensors

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Sensor Leads

- 8.2.2. Sensor Plugs

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Sensor Leads and Plugs Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Resistive Sensors

- 9.1.2. Inductive Sensors

- 9.1.3. Capacitive Sensors

- 9.1.4. Potentiometric Sensors

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Sensor Leads

- 9.2.2. Sensor Plugs

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Sensor Leads and Plugs Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Resistive Sensors

- 10.1.2. Inductive Sensors

- 10.1.3. Capacitive Sensors

- 10.1.4. Potentiometric Sensors

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Sensor Leads

- 10.2.2. Sensor Plugs

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 OMRON

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Emerson

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SCHNEIDER ELECTRIC

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 TE Connectivity

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Molex

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Interplex

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 BNR Industrial

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Baumer

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SICK AG

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Binder

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 BRAUNKABEL

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Steen Technology AB

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Phoenix Contact

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 TRIUMPH CABLE

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 OMRON

List of Figures

- Figure 1: Global Sensor Leads and Plugs Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Sensor Leads and Plugs Revenue (million), by Application 2024 & 2032

- Figure 3: North America Sensor Leads and Plugs Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Sensor Leads and Plugs Revenue (million), by Types 2024 & 2032

- Figure 5: North America Sensor Leads and Plugs Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Sensor Leads and Plugs Revenue (million), by Country 2024 & 2032

- Figure 7: North America Sensor Leads and Plugs Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Sensor Leads and Plugs Revenue (million), by Application 2024 & 2032

- Figure 9: South America Sensor Leads and Plugs Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Sensor Leads and Plugs Revenue (million), by Types 2024 & 2032

- Figure 11: South America Sensor Leads and Plugs Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Sensor Leads and Plugs Revenue (million), by Country 2024 & 2032

- Figure 13: South America Sensor Leads and Plugs Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Sensor Leads and Plugs Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Sensor Leads and Plugs Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Sensor Leads and Plugs Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Sensor Leads and Plugs Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Sensor Leads and Plugs Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Sensor Leads and Plugs Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Sensor Leads and Plugs Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Sensor Leads and Plugs Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Sensor Leads and Plugs Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Sensor Leads and Plugs Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Sensor Leads and Plugs Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Sensor Leads and Plugs Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Sensor Leads and Plugs Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Sensor Leads and Plugs Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Sensor Leads and Plugs Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Sensor Leads and Plugs Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Sensor Leads and Plugs Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Sensor Leads and Plugs Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Sensor Leads and Plugs Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Sensor Leads and Plugs Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Sensor Leads and Plugs Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Sensor Leads and Plugs Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Sensor Leads and Plugs Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Sensor Leads and Plugs Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Sensor Leads and Plugs Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Sensor Leads and Plugs Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Sensor Leads and Plugs Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Sensor Leads and Plugs Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Sensor Leads and Plugs Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Sensor Leads and Plugs Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Sensor Leads and Plugs Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Sensor Leads and Plugs Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Sensor Leads and Plugs Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Sensor Leads and Plugs Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Sensor Leads and Plugs Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Sensor Leads and Plugs Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Sensor Leads and Plugs Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Sensor Leads and Plugs Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sensor Leads and Plugs?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Sensor Leads and Plugs?

Key companies in the market include OMRON, Emerson, SCHNEIDER ELECTRIC, TE Connectivity, Molex, Interplex, BNR Industrial, Baumer, SICK AG, Binder, BRAUNKABEL, Steen Technology AB, Phoenix Contact, TRIUMPH CABLE.

3. What are the main segments of the Sensor Leads and Plugs?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sensor Leads and Plugs," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sensor Leads and Plugs report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sensor Leads and Plugs?

To stay informed about further developments, trends, and reports in the Sensor Leads and Plugs, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence