Key Insights

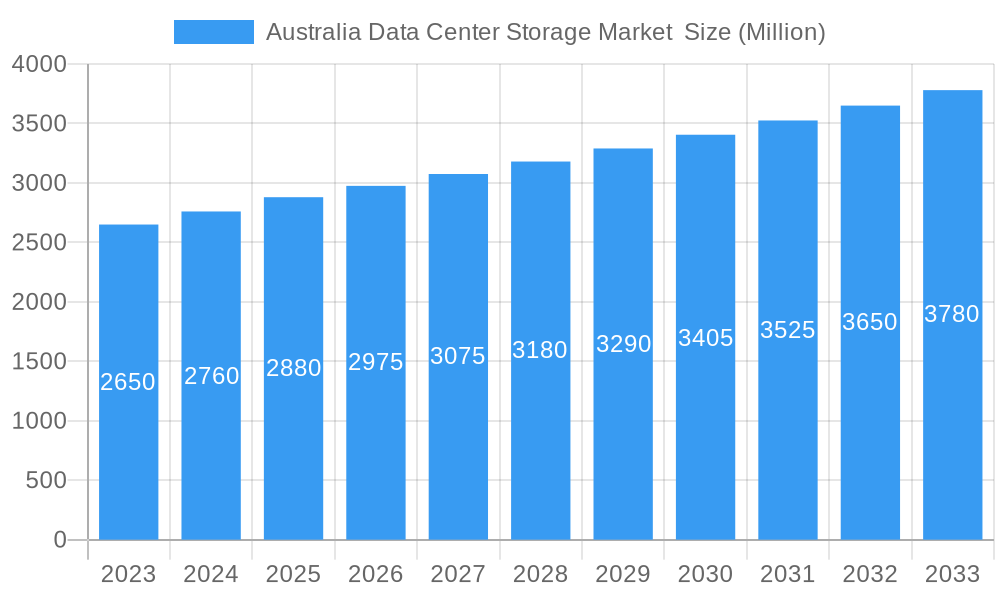

The Australian Data Center Storage Market is poised for steady expansion, projected to reach approximately AUD 2.88 billion in 2025. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 3.18% during the study period of 2019-2033, indicating sustained demand for robust storage solutions. Key drivers for this market include the escalating volume of data generated by businesses and government entities, the increasing adoption of cloud computing services, and the ongoing digital transformation initiatives across various sectors. Furthermore, the imperative for enhanced data security, compliance with evolving data privacy regulations, and the demand for high-performance storage to support analytics and AI workloads are significant contributing factors. The market is segmented across various storage technologies such as Network Attached Storage (NAS), Storage Area Network (SAN), and Direct Attached Storage (DAS), with a notable shift towards more advanced solutions like All-flash and Hybrid storage arrays. This evolution reflects a growing need for speed, efficiency, and scalability in data management.

Australia Data Center Storage Market Market Size (In Billion)

The competitive landscape features established players like Seagate Technology, Dell Inc., Hewlett Packard Enterprise, and NetApp Inc., alongside innovative companies like Pure Storage Inc. These vendors are actively engaged in offering solutions that cater to the specific needs of diverse end-users, including the IT and Telecommunication, BFSI, Government, and Media and Entertainment sectors. The increasing reliance on data for critical decision-making and operational efficiency across these industries will continue to fuel the demand for sophisticated data center storage. While the market benefits from strong growth drivers, potential restraints may include the high initial investment costs associated with advanced storage infrastructure and the ongoing challenges of cybersecurity threats that necessitate continuous investment in security solutions. Nevertheless, the overall outlook for the Australian Data Center Storage Market remains positive, driven by the relentless digital evolution and the critical role of data in modern business operations.

Australia Data Center Storage Market Company Market Share

Australia Data Center Storage Market: Comprehensive Analysis and Future Outlook (2019-2033)

This detailed report offers an in-depth analysis of the Australia Data Center Storage Market, providing critical insights into its current state and projected trajectory. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, this report is an indispensable resource for stakeholders seeking to understand the dynamics of Australian data storage solutions, enterprise storage Australia, and cloud storage Australia. We delve into market segmentation, key growth drivers, prevalent challenges, and the competitive landscape, offering actionable intelligence for strategic decision-making.

Australia Data Center Storage Market Market Structure & Competitive Dynamics

The Australia Data Center Storage Market exhibits a moderately concentrated structure, with key players like Dell Inc, Hewlett Packard Enterprise, and NetApp Inc holding significant market share. Innovation is a critical differentiator, driven by the continuous development of advanced storage technologies such as NVMe-oF and object storage, crucial for high-performance storage Australia. Regulatory frameworks, particularly those concerning data privacy and sovereignty (e.g., the Privacy Act 1988), shape market entry and operational strategies. Product substitutes, including cloud-based storage services, present a competitive challenge, forcing traditional storage providers to enhance their value propositions. End-user trends indicate a rising demand for scalable and flexible storage solutions, particularly from the IT and Telecommunication and BFSI sectors in Australia. Mergers and acquisitions (M&A) are infrequent but strategically important, aimed at consolidating market presence and expanding technological capabilities. For instance, past M&A activities have seen companies like Hitachi Vantara LLC acquire and integrate advanced storage capabilities.

- Market Concentration: Moderate, with a few dominant players.

- Innovation Ecosystem: Driven by advancements in flash storage, hybrid cloud solutions, and data management software.

- Regulatory Frameworks: Data sovereignty and privacy laws significantly influence market operations.

- Product Substitutes: Cloud storage services are the primary substitute, necessitating competitive differentiation.

- End-User Trends: Increasing adoption of hyper-converged infrastructure and software-defined storage.

- M&A Activities: Strategic acquisitions to gain market share and technological expertise. Key deal values are typically in the range of several tens to hundreds of millions of dollars.

Australia Data Center Storage Market Industry Trends & Insights

The Australia Data Center Storage Market is experiencing robust growth, fueled by an escalating volume of data generated from digital transformation initiatives, the proliferation of IoT devices, and the increasing adoption of cloud computing and hybrid cloud strategies. The projected Compound Annual Growth Rate (CAGR) for the forecast period is xx%, indicating a dynamic and expanding market. Technological disruptions, particularly the widespread adoption of all-flash storage and the increasing sophistication of software-defined storage (SDS) solutions, are fundamentally reshaping storage architectures. Consumers are exhibiting a clear preference for storage solutions that offer enhanced performance, scalability, data resiliency, and cost-efficiency. The competitive landscape is characterized by intense innovation and strategic partnerships aimed at delivering integrated solutions that address complex data management needs. Market penetration for advanced storage technologies is steadily increasing as organizations recognize the benefits in terms of reduced latency, improved application performance, and streamlined data operations. The demand for secure and reliable data storage is paramount, especially for sectors like BFSI and government, which handle sensitive information. Furthermore, the growing emphasis on data analytics and Artificial Intelligence (AI) workloads necessitates high-speed and efficient storage, further driving the demand for cutting-edge solutions. The evolution of Network Attached Storage (NAS) and Storage Area Network (SAN) technologies, alongside the persistent relevance of Direct Attached Storage (DAS) in specific use cases, highlights the diverse needs within the Australian market.

Dominant Markets & Segments in Australia Data Center Storage Market

The Australia Data Center Storage Market is significantly influenced by its dominant segments across various classifications.

Storage Technology:

- Network Attached Storage (NAS): This segment is experiencing strong growth driven by its ease of use, cost-effectiveness, and suitability for file sharing and collaboration in small to medium-sized businesses and enterprise departments. Key drivers include the increasing need for centralized data management and the accessibility of data for multiple users simultaneously.

- Storage Area Network (SAN): SAN solutions remain dominant for high-performance, mission-critical applications, particularly in large enterprises and demanding sectors like BFSI and IT and Telecommunication. The demand for high throughput and low latency makes SAN the preferred choice for databases, virtualization, and high-transaction environments.

- Direct Attached Storage (DAS): While less prevalent as a primary enterprise solution, DAS continues to be relevant for specific applications requiring direct, high-speed access to storage, such as in some high-performance computing clusters or embedded systems.

Storage Type:

- All-flash Storage: This segment is the fastest-growing, driven by the relentless pursuit of performance. The decline in flash memory costs and the increasing demand for faster application response times are key economic policies and infrastructure developments enabling this dominance. Pure Storage Inc and Dell Inc are key players in this rapidly evolving space.

- Hybrid Storage: Hybrid solutions, offering a blend of flash and traditional hard disk drives (HDDs), continue to hold a significant market share, providing a balanced approach to performance, capacity, and cost for a wide range of workloads.

- Traditional Storage: While declining in its standalone dominance, traditional HDD-based storage remains crucial for bulk data storage and archival purposes where cost per terabyte is the primary consideration.

End-user:

- IT and Telecommunication: This sector is the largest consumer of data center storage solutions, driven by massive data growth, cloud service expansion, and network infrastructure demands.

- BFSI: The banking, financial services, and insurance sectors are significant adopters, demanding highly secure, reliable, and high-performance storage for transactional data, analytics, and regulatory compliance. Economic policies promoting digital banking further fuel this demand.

- Government: Government agencies require robust, secure, and compliant storage solutions for public records, defense, and critical infrastructure data. Data sovereignty and security are paramount drivers in this segment.

- Media and Entertainment: This sector demands high-capacity, high-throughput storage for content creation, editing, archiving, and streaming, necessitating solutions that can handle large file sizes and rapid access.

Australia Data Center Storage Market Product Innovations

Product innovations in the Australia Data Center Storage Market are primarily focused on enhancing performance, scalability, and data intelligence. Companies like Seagate Technology LLC and Kingston Technology Company Inc are leading advancements in storage media and hardware, offering higher densities and faster transfer speeds. NetApp Inc and Pure Storage Inc are at the forefront of software-defined storage solutions, enabling greater flexibility and automation. Key innovations include the development of intelligent data management platforms, advanced data deduplication and compression techniques for improved efficiency, and the integration of AI/ML capabilities for predictive analytics and automated tiering. These advancements are crucial for addressing the growing demands of big data analytics, IoT, and modern application workloads, providing a competitive advantage for vendors and enhanced capabilities for end-users.

Report Segmentation & Scope

This report meticulously segments the Australia Data Center Storage Market to provide granular insights. The scope covers the following classifications:

- Storage Technology: This includes Network Attached Storage (NAS), Storage Area Network (SAN), Direct Attached Storage (DAS), and Other Technologies. Each segment’s growth projections and market sizes are analyzed, with NAS and SAN expected to show significant expansion, driven by evolving enterprise needs.

- Storage Type: Analysis extends to Traditional Storage, All-flash Storage, and Hybrid Storage. All-flash storage is projected for the highest growth rate, reflecting the industry's push towards performance optimization, while hybrid solutions will maintain a strong presence, balancing cost and speed.

- End-user: The report segments the market by end-user industries: IT and Telecommunication, BFSI, Government, Media and Entertainment, and Other End-users. The IT and Telecommunication and BFSI sectors are expected to dominate, exhibiting substantial market shares and high growth due to their data-intensive operations and digital transformation efforts.

Key Drivers of Australia Data Center Storage Market Growth

The growth of the Australia Data Center Storage Market is propelled by several key factors. Digital transformation initiatives across all industries are generating unprecedented volumes of data, necessitating expanded storage capacity. The escalating adoption of cloud computing and hybrid cloud models requires robust and scalable storage solutions to manage data across different environments. Advancements in technologies like Artificial Intelligence (AI) and the Internet of Things (IoT) are creating new data streams that demand sophisticated storage and processing capabilities. Government initiatives promoting digital infrastructure and data sovereignty also play a crucial role. Furthermore, the increasing focus on data analytics for business intelligence and operational efficiency compels organizations to invest in high-performance storage systems.

Challenges in the Australia Data Center Storage Market Sector

Despite the robust growth, the Australia Data Center Storage Market faces several challenges. Data security and privacy concerns remain paramount, with stringent regulations requiring significant investment in compliant storage solutions. The increasing complexity of data management, coupled with the need for efficient data lifecycle management, poses a technical hurdle. Supply chain disruptions, particularly in the sourcing of crucial components like semiconductors, can impact product availability and pricing. Furthermore, the competitive pressure from cloud-based storage providers continues to challenge traditional on-premises storage vendors, requiring them to constantly innovate and offer compelling value propositions. The high initial capital expenditure for enterprise-grade storage solutions can also be a barrier for smaller organizations.

Leading Players in the Australia Data Center Storage Market Market

- Seagate Technology LLC

- Lenovo Group Limited

- Hewlett Packard Enterprise

- Fujitsu Limited

- Overland Tandber

- Dell Inc

- NetApp Inc

- Kingston Technology Company Inc

- Pure Storage Inc

- Hitachi Vantara LLC

Key Developments in Australia Data Center Storage Market Sector

- 2023: Dell Technologies launched new updates to its APEX data storage portfolio, enhancing hybrid cloud capabilities for Australian enterprises.

- 2023: NetApp Inc expanded its all-flash storage offerings, focusing on improved performance and AI/ML workload support in Australia.

- 2024 (Q1): Hewlett Packard Enterprise announced strategic partnerships with Australian cloud providers to offer integrated storage solutions.

- 2024 (Q2): Pure Storage Inc released advancements in its FlashArray product line, emphasizing sustainability and energy efficiency for Australian data centers.

- 2024 (Q3): Hitachi Vantara LLC introduced new data fabric solutions designed to simplify data management across hybrid cloud environments in Australia.

Strategic Australia Data Center Storage Market Market Outlook

The Australia Data Center Storage Market is poised for continued expansion, driven by ongoing digital transformation and the increasing importance of data as a strategic asset. Key growth accelerators include the further maturation of all-flash storage technology, the broader adoption of software-defined storage (SDS), and the integration of AI and machine learning capabilities into storage management platforms. Strategic opportunities lie in catering to specific industry needs, such as enhanced security for BFSI and government sectors, and high-throughput solutions for media and entertainment. The trend towards hybrid and multi-cloud environments will continue to shape demand, necessitating flexible and interoperable storage solutions. Companies that focus on providing scalable, secure, and intelligent data storage will be well-positioned for future success in this dynamic Australian market.

Australia Data Center Storage Market Segmentation

-

1. Storage Technology

- 1.1. Network Attached Storage (NAS)

- 1.2. Storage Area Network (SAN)

- 1.3. Direct Attached Storage (DAS)

- 1.4. Other Technologies

-

2. Storage Type

- 2.1. Traditional Storage

- 2.2. All-flash Storage

- 2.3. Hybrid Storage

-

3. End-user

- 3.1. IT and Telecommunication

- 3.2. BFSI

- 3.3. Government

- 3.4. Media and Entertainment

- 3.5. Other End-users

Australia Data Center Storage Market Segmentation By Geography

- 1. Australia

Australia Data Center Storage Market Regional Market Share

Geographic Coverage of Australia Data Center Storage Market

Australia Data Center Storage Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.18% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Expansion of IT Infrastructure to Increase Market Growth; Increased Investments in Hyperscale Data Centers to Increase Market Growth

- 3.3. Market Restrains

- 3.3.1. High Initial Investment Cost to Hinder Market Growth

- 3.4. Market Trends

- 3.4.1. IT and Telecommunication Segment to Hold Major Share in the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Data Center Storage Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Storage Technology

- 5.1.1. Network Attached Storage (NAS)

- 5.1.2. Storage Area Network (SAN)

- 5.1.3. Direct Attached Storage (DAS)

- 5.1.4. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Storage Type

- 5.2.1. Traditional Storage

- 5.2.2. All-flash Storage

- 5.2.3. Hybrid Storage

- 5.3. Market Analysis, Insights and Forecast - by End-user

- 5.3.1. IT and Telecommunication

- 5.3.2. BFSI

- 5.3.3. Government

- 5.3.4. Media and Entertainment

- 5.3.5. Other End-users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Storage Technology

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Seagate Technology LLC

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Lenovo Group Limited

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Hewlett Packard Enterprise

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Fujitsu Limited

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Overland Tandber

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Dell Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 NetApp Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Kingston Technology Company Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Pure Storage Inc

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Hitachi Vantara LLC

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Seagate Technology LLC

List of Figures

- Figure 1: Australia Data Center Storage Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Australia Data Center Storage Market Share (%) by Company 2025

List of Tables

- Table 1: Australia Data Center Storage Market Revenue Million Forecast, by Storage Technology 2020 & 2033

- Table 2: Australia Data Center Storage Market Revenue Million Forecast, by Storage Type 2020 & 2033

- Table 3: Australia Data Center Storage Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 4: Australia Data Center Storage Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Australia Data Center Storage Market Revenue Million Forecast, by Storage Technology 2020 & 2033

- Table 6: Australia Data Center Storage Market Revenue Million Forecast, by Storage Type 2020 & 2033

- Table 7: Australia Data Center Storage Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 8: Australia Data Center Storage Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Data Center Storage Market ?

The projected CAGR is approximately 3.18%.

2. Which companies are prominent players in the Australia Data Center Storage Market ?

Key companies in the market include Seagate Technology LLC, Lenovo Group Limited, Hewlett Packard Enterprise, Fujitsu Limited, Overland Tandber, Dell Inc, NetApp Inc, Kingston Technology Company Inc, Pure Storage Inc, Hitachi Vantara LLC.

3. What are the main segments of the Australia Data Center Storage Market ?

The market segments include Storage Technology, Storage Type, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.88 Million as of 2022.

5. What are some drivers contributing to market growth?

Expansion of IT Infrastructure to Increase Market Growth; Increased Investments in Hyperscale Data Centers to Increase Market Growth.

6. What are the notable trends driving market growth?

IT and Telecommunication Segment to Hold Major Share in the Market.

7. Are there any restraints impacting market growth?

High Initial Investment Cost to Hinder Market Growth.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Data Center Storage Market ," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Data Center Storage Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Data Center Storage Market ?

To stay informed about further developments, trends, and reports in the Australia Data Center Storage Market , consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence