Key Insights

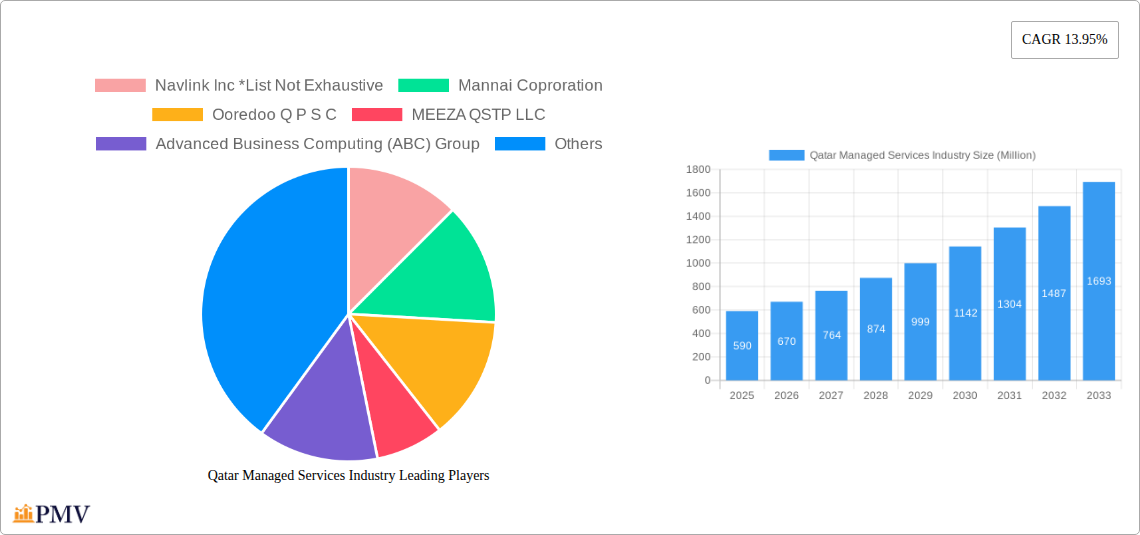

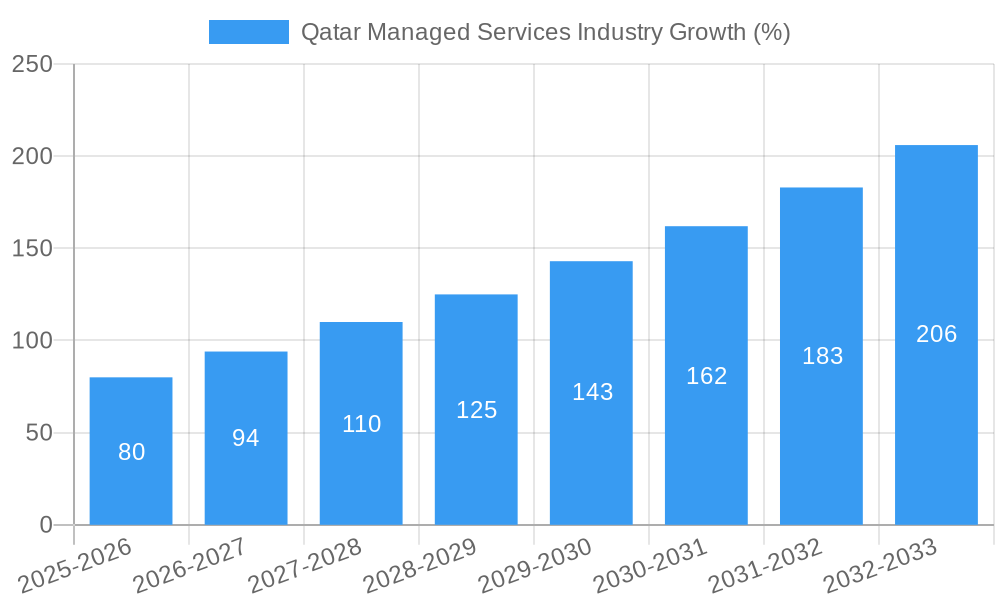

The Qatar managed services market, valued at $0.59 billion in 2025, exhibits robust growth potential, projected to expand at a Compound Annual Growth Rate (CAGR) of 13.95% from 2025 to 2033. This expansion is fueled by several key drivers. The increasing adoption of cloud computing and digital transformation initiatives across various sectors, particularly BFSI (Banking, Financial Services, and Insurance), government, and oil & gas, necessitates reliable and efficient managed services. Furthermore, the growing need for enhanced cybersecurity and disaster recovery solutions in a digitally connected world is significantly boosting market demand. The market is segmented by service type (Managed Infrastructure, Managed Hosting, Managed Security, Managed Cloud Services, Disaster Recovery) and end-user vertical (Government, BFSI, Oil & Gas, IT & Telecom, Healthcare, and others). Competition is relatively diverse, with both international players and local companies like Navlink Inc, Mannai Corporation, and MEEZA QSTP LLC vying for market share. The strong government support for digitalization in Qatar further contributes to the positive outlook.

The sustained growth trajectory is anticipated to continue through 2033, driven by further technological advancements and evolving business needs. However, challenges remain, including the potential for skills shortages in the IT sector and the need for continuous investment in infrastructure to support the expanding digital ecosystem. Nevertheless, the overall market outlook remains positive, with significant opportunities for managed service providers offering innovative and tailored solutions to meet the diverse needs of Qatar's businesses and government entities. The focus on data security and compliance regulations will also drive demand for specialized managed security services. The relatively high cost of implementation for some managed services might pose a restraint, but the long-term benefits of improved efficiency and reduced operational costs are likely to outweigh this factor.

Qatar Managed Services Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Qatar managed services industry, covering market size, growth projections, competitive landscape, and key industry trends from 2019 to 2033. The report leverages data from the historical period (2019-2024), the base year (2025), and the estimated year (2025) to forecast market trends until 2033. The study includes a detailed segmentation analysis by type and end-user vertical, identifying dominant market segments and highlighting growth opportunities for stakeholders. This report is crucial for businesses, investors, and policymakers seeking to understand and participate in the dynamic Qatar managed services market.

Qatar Managed Services Industry Market Structure & Competitive Dynamics

The Qatar managed services market exhibits a moderately concentrated structure, with several large players vying for market share alongside smaller, specialized firms. Key players include Navlink Inc, Mannai Corporation, Ooredoo Q.P.S.C, MEEZA QSTP LLC, Advanced Business Computing (ABC) Group, Gulf Business Machines Qatar WLL, Paladion Qatar WLL, Diyar Group, and Paramount Computer Systems FZ-LLC. However, the market shows signs of increasing competition, particularly with the entry of international players and the rise of cloud-based solutions.

The regulatory framework in Qatar is supportive of technological advancements, with initiatives to encourage digital transformation across various sectors. This has fostered innovation within the managed services ecosystem, leading to the development of sophisticated solutions. While direct product substitutes are limited, alternative approaches such as in-house IT management represent a competitive threat. The industry is witnessing increased M&A activity, with deal values reaching an estimated xx Million in 2024. These mergers and acquisitions are largely driven by the need to expand service offerings, enhance technological capabilities, and consolidate market share.

- Market Concentration: Moderately concentrated, with a few dominant players and numerous smaller firms.

- Innovation Ecosystem: Active, supported by government initiatives and the adoption of new technologies.

- Regulatory Framework: Supportive of technological advancements and digital transformation.

- M&A Activity: Increasing, with deal values estimated at xx Million in 2024.

- Market Share: Dominant players hold approximately xx% of the market share collectively (2024).

Qatar Managed Services Industry Industry Trends & Insights

The Qatar managed services market is experiencing robust growth, driven by increasing digitalization across various sectors. The Compound Annual Growth Rate (CAGR) is projected to be xx% during the forecast period (2025-2033), exceeding the global average. This growth is fueled by several factors, including the government's initiatives promoting digital transformation (Qatar National Vision 2030), the expanding adoption of cloud computing, and the growing demand for cybersecurity solutions. Furthermore, the rise of the Internet of Things (IoT) and big data analytics is contributing to the market’s expansion. The increasing penetration of cloud-based solutions is reshaping the landscape, with a market penetration rate projected to reach xx% by 2033. The heightened awareness of data security and the need for robust disaster recovery and business continuity services are key drivers influencing consumer preferences. The market dynamics are influenced by competition among established players and the emergence of new entrants leveraging innovative technologies.

Dominant Markets & Segments in Qatar Managed Services Industry

The Qatar managed services market is dominated by the Government and BFSI (Banking, Financial Services, and Insurance) sectors due to their high dependence on robust IT infrastructure and stringent security requirements. The Oil and Gas sector also presents a significant market segment, demanding specialized managed services to support critical operations.

Key Drivers for Dominant Segments:

- Government: Government initiatives to digitalize public services and enhance cybersecurity.

- BFSI: Strict regulatory compliance needs and the increasing adoption of digital banking and financial technologies.

- Oil and Gas: Need for reliable and secure IT infrastructure to support critical operations and data management.

Dominance Analysis: The Government sector is likely to maintain its leading position throughout the forecast period due to significant investments in digital infrastructure and ongoing initiatives focused on improving public services through technology. The BFSI sector is also expected to show robust growth driven by the expansion of digital financial services. The Oil and Gas sector will continue to be a significant contributor to the market, although its growth might be comparatively slower.

- Managed Infrastructure (Network and Desktop): This segment will experience substantial growth due to the increasing adoption of cloud technologies and remote work models.

- Managed Hosting (Application and Data Center): This segment will remain pivotal, offering scalable and secure data center solutions for businesses.

- Managed Security: The rising cybersecurity threats will drive the growth of this segment, with strong demand for advanced security solutions.

- Managed Cloud Services: High adoption rates projected as businesses migrate to the cloud for cost efficiency and scalability.

- Disaster Recovery and Business Continuity Services: This segment will witness steady growth due to increased awareness of the importance of business resilience.

Qatar Managed Services Industry Product Innovations

Recent innovations focus on AI-powered security solutions, enhanced cloud-based disaster recovery systems, and integrated network management tools. These advancements cater to the evolving demands of the market, providing clients with greater efficiency, security, and cost-effectiveness. The market trend favors integrated and automated solutions that simplify management and improve responsiveness.

Report Segmentation & Scope

The report segments the Qatar managed services market by Type (Managed Infrastructure, Managed Hosting, Managed Security, Managed Cloud Services, Disaster Recovery and Business Continuity Services) and End-user Vertical (Government, BFSI, Oil and Gas, IT and Telecom, Healthcare, Other). Each segment's growth trajectory, market size, and competitive dynamics are analyzed in detail, offering granular insights into the market structure. Growth projections for each segment vary based on specific industry trends and adoption rates of new technologies. For example, the Managed Cloud Services segment is projected to experience the fastest growth, driven by the ongoing cloud adoption across various industries.

Key Drivers of Qatar Managed Services Industry Growth

Several factors drive the growth of the Qatar managed services market, including:

- Government Initiatives: The Qatari government's commitment to digital transformation and infrastructure development fosters market growth.

- Technological Advancements: Innovations like cloud computing, AI, and IoT are creating new opportunities for managed service providers.

- Economic Growth: Qatar's robust economy creates a favorable environment for IT spending and adoption of new technologies.

Challenges in the Qatar Managed Services Industry Sector

The industry faces challenges including:

- Competition: Intense competition among existing and new players demands continuous innovation and service differentiation.

- Talent Acquisition: Finding and retaining skilled professionals is a constant challenge for the industry.

- Cybersecurity Threats: The rising threat of cyberattacks necessitates continuous investment in security technologies and expertise.

Leading Players in the Qatar Managed Services Industry Market

- Navlink Inc

- Mannai Corporation

- Ooredoo Q.P.S.C

- MEEZA QSTP LLC

- Advanced Business Computing (ABC) Group

- Gulf Business Machines Qatar WLL

- Paladion Qatar WLL

- Diyar Group

- Paramount Computer Systems FZ-LLC

Key Developments in Qatar Managed Services Industry Sector

January 2022: Microsoft and Vodafone Qatar expanded their collaboration to offer digital solutions, leveraging Microsoft Azure for IoT services. This development significantly boosts the adoption of cloud-based solutions and enhances the security and reliability of managed services.

June 2022: Starlink W.L.L. and Huawei partnered to offer cloud network managed services, providing scalable and flexible network solutions for businesses. This collaboration enhances the availability of advanced network management capabilities within the Qatari market.

Strategic Qatar Managed Services Industry Market Outlook

The Qatar managed services market presents substantial growth potential. Ongoing government investments, the expanding adoption of cloud and IoT technologies, and the increasing demand for cybersecurity solutions promise a positive outlook. Strategic opportunities exist for companies focusing on innovative solutions, specialized services for niche sectors, and robust cybersecurity offerings. The market is poised for sustained growth, making it an attractive sector for investment and expansion.

Qatar Managed Services Industry Segmentation

-

1. Type

- 1.1. Managed Infrastructure (Network and Desktop)

- 1.2. Managed Hosting (Application and Data Center)

-

1.3. Managed Security

- 1.3.1. Asset Management and Monitoring

- 1.3.2. Threat Intelligence and Management

- 1.3.3. Risk and Compliance

- 1.3.4. Other Managed Securities

- 1.4. Managed

- 1.5. Disaster Recovery and Business Continuity Services

-

2. End-user Vertical

- 2.1. Government

- 2.2. BFSI

- 2.3. Oil and Gas

- 2.4. IT and Telecom

- 2.5. Healthcare

- 2.6. Other En

Qatar Managed Services Industry Segmentation By Geography

- 1. Qatar

Qatar Managed Services Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 13.95% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand for Outsourcing of Non-core Operations and Lack of In-house Capabilities Among Key End Users in the Country; Growing Availability of Diversified Offerings Supported by Partnerships Between Local MSPs And Large-Scale Organizations; Supportive Government Policies and Development of Local Landscape due to the Recent Changes in Geopolitical Conditions

- 3.3. Market Restrains

- 3.3.1. Dependency on Host Mobile Network Operators (MNO); Government Regulations and Policies May Affect The Maintenance of Profit Margins of MVNOS

- 3.4. Market Trends

- 3.4.1. Managed Cloud Services is Expected to Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Qatar Managed Services Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Managed Infrastructure (Network and Desktop)

- 5.1.2. Managed Hosting (Application and Data Center)

- 5.1.3. Managed Security

- 5.1.3.1. Asset Management and Monitoring

- 5.1.3.2. Threat Intelligence and Management

- 5.1.3.3. Risk and Compliance

- 5.1.3.4. Other Managed Securities

- 5.1.4. Managed

- 5.1.5. Disaster Recovery and Business Continuity Services

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Government

- 5.2.2. BFSI

- 5.2.3. Oil and Gas

- 5.2.4. IT and Telecom

- 5.2.5. Healthcare

- 5.2.6. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Navlink Inc *List Not Exhaustive

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Mannai Coproration

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Ooredoo Q P S C

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 MEEZA QSTP LLC

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Advanced Business Computing (ABC) Group

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Gulf Business Machines Qatar WLL

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Paladion Qatar WLL

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Diyar Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Paramount Computer Systems FZ-LLC

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.1 Navlink Inc *List Not Exhaustive

List of Figures

- Figure 1: Qatar Managed Services Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Qatar Managed Services Industry Share (%) by Company 2024

List of Tables

- Table 1: Qatar Managed Services Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Qatar Managed Services Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Qatar Managed Services Industry Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 4: Qatar Managed Services Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Qatar Managed Services Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Qatar Managed Services Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 7: Qatar Managed Services Industry Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 8: Qatar Managed Services Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Managed Services Industry?

The projected CAGR is approximately 13.95%.

2. Which companies are prominent players in the Qatar Managed Services Industry?

Key companies in the market include Navlink Inc *List Not Exhaustive, Mannai Coproration, Ooredoo Q P S C, MEEZA QSTP LLC, Advanced Business Computing (ABC) Group, Gulf Business Machines Qatar WLL, Paladion Qatar WLL, Diyar Group, Paramount Computer Systems FZ-LLC.

3. What are the main segments of the Qatar Managed Services Industry?

The market segments include Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.59 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Outsourcing of Non-core Operations and Lack of In-house Capabilities Among Key End Users in the Country; Growing Availability of Diversified Offerings Supported by Partnerships Between Local MSPs And Large-Scale Organizations; Supportive Government Policies and Development of Local Landscape due to the Recent Changes in Geopolitical Conditions.

6. What are the notable trends driving market growth?

Managed Cloud Services is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Dependency on Host Mobile Network Operators (MNO); Government Regulations and Policies May Affect The Maintenance of Profit Margins of MVNOS.

8. Can you provide examples of recent developments in the market?

January 2022 - Microsoft and Vodafone Qatar announced that they are expanding their current collaboration to offer more digital solutions to businesses across the country. Vodafone's IoT product and service offerings will incorporate Microsoft Azure to help the firms unify their respective technology portfolios. Vodafone's IoT solutions hosted on Microsoft Azure are projected to offer highly secure, dependable, and tailored features and benefits to Qatar's commercial clients, including public and private organisations and governmental entities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Managed Services Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Managed Services Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Managed Services Industry?

To stay informed about further developments, trends, and reports in the Qatar Managed Services Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence