Key Insights

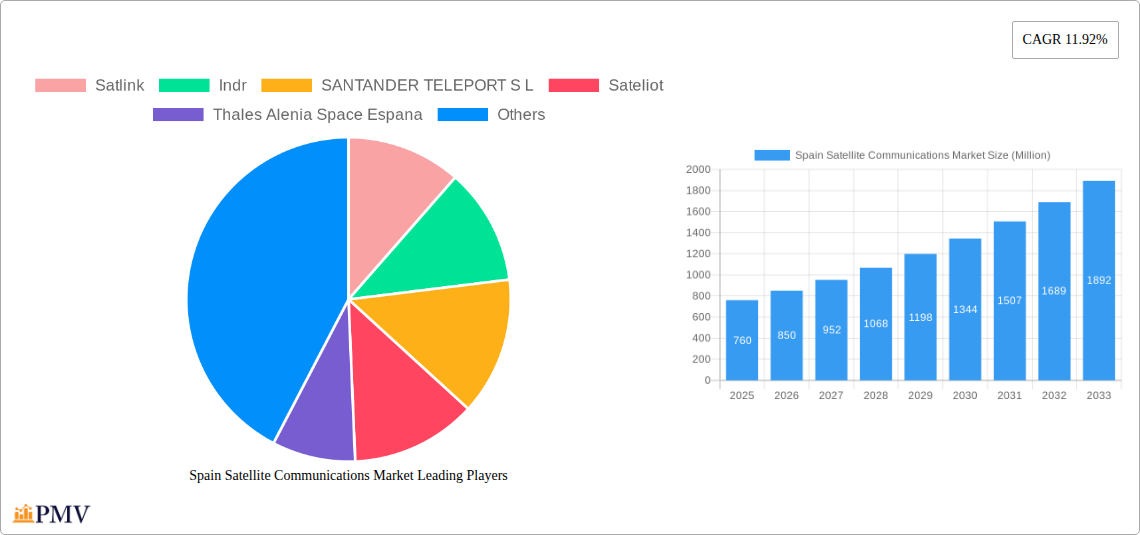

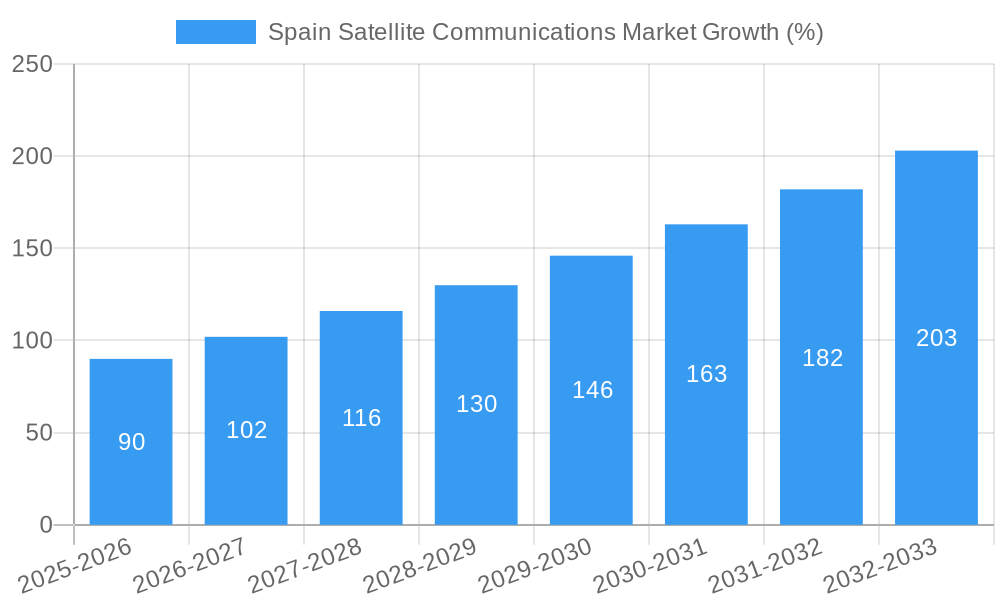

The Spain Satellite Communications Market, valued at €0.76 billion in 2025, is projected to experience robust growth, driven by increasing demand for high-speed broadband access in underserved areas, the expanding adoption of satellite-based IoT applications, and the growing need for secure government and defense communications. The market's Compound Annual Growth Rate (CAGR) of 11.92% from 2025 to 2033 indicates significant expansion potential. Key drivers include the government's initiatives to improve digital infrastructure, the rising adoption of satellite-based navigation and positioning systems, and the increasing reliance on satellite communication services by the maritime and media sectors. The market segmentation reveals a strong presence across various platforms, with significant contributions from portable, land-based, and maritime segments. The strong presence of established players like Hispasat and Thales Alenia Space España, alongside emerging innovative companies like Sateliot, indicates a healthy competitive landscape encouraging technological advancement and market expansion.

The market’s growth will be further influenced by trends such as the adoption of advanced satellite technologies like Low Earth Orbit (LEO) constellations and the integration of 5G capabilities with satellite networks. However, the market may face challenges related to regulatory hurdles, the high initial investment costs associated with satellite infrastructure, and potential competition from terrestrial communication networks in densely populated areas. Nevertheless, the projected CAGR suggests that the market will continue its upward trajectory, fueled by the aforementioned growth drivers and the increasing demand for reliable and ubiquitous connectivity across various sectors in Spain. The market's segmentation by end-user vertical reveals strong growth in maritime, defense and government, and media and entertainment sectors, indicating diverse applications and market opportunities.

Spain Satellite Communications Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Spain Satellite Communications Market, offering valuable insights for businesses, investors, and industry stakeholders. The study covers the period from 2019 to 2033, with 2025 as the base year and a forecast period extending to 2033. The report meticulously segments the market by type (Ground Equipment, Services), platform (Portable, Land, Maritime, Airborne), and end-user vertical (Maritime, Defense and Government, Enterprises, Media and Entertainment, Other End-user Verticals), providing a granular understanding of market dynamics. The total market size is expected to reach xx Million by 2033.

Spain Satellite Communications Market Market Structure & Competitive Dynamics

The Spanish satellite communications market exhibits a moderately consolidated structure, with key players such as Hispasat and Hisdesat Servicios EstratEgicos SA holding significant market share. However, the presence of several smaller, specialized companies like Satlink and Verasat Global SL fosters competition and innovation. The market is characterized by a dynamic interplay of technological advancements, evolving regulatory frameworks, and increasing demand from various end-user verticals.

The innovative ecosystem is fueled by collaborations between established players and emerging technology companies, particularly in the development of advanced ground equipment and satellite-based services. The regulatory landscape, largely governed by the Spanish government and the European Union, plays a critical role in shaping market growth and investment. Substitutes for satellite communication, such as terrestrial fiber optic networks and terrestrial microwave links, exert competitive pressure, particularly in specific geographical areas and applications. However, the unique capabilities of satellite communication, especially for remote areas and mobile applications, provide a strong competitive advantage. End-user trends showcase a growing preference for high-throughput satellite (HTS) solutions and demand for enhanced security and reliability.

Mergers and acquisitions (M&A) activity in the Spanish satellite communications sector has been moderate, with deal values varying significantly depending on the size and strategic objectives of the participating companies. For example, the contract awarded to GMV by Hisdesat for the SPAINSAT NG project represents a significant investment in the sector. Analyzing M&A deal values and market share data reveals a clear trend toward consolidation, with larger companies strategically acquiring smaller ones to expand their capabilities and market reach. Further analysis identifies key strategic partnerships and alliances that shape the market landscape. A detailed competitive analysis explores market shares of key players highlighting the strengths, weaknesses, opportunities, and threats influencing their market positioning.

Spain Satellite Communications Market Industry Trends & Insights

The Spain Satellite Communications Market is experiencing significant growth driven by several key factors. The increasing demand for reliable and high-speed broadband connectivity in remote areas, coupled with the government's initiatives to promote digitalization and technological advancement, is a primary growth driver. Technological disruptions, especially the adoption of HTS technologies and the emergence of new satellite constellations, are revolutionizing the market. Consumer preferences are shifting toward cost-effective, high-performance solutions with improved security and reliability. The competitive landscape is becoming increasingly dynamic as new players enter the market, while established players focus on enhancing their service offerings and expanding into new market segments. The market is projected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration of satellite communication services, particularly in the maritime and defense sectors, is expected to increase significantly. Detailed analysis explores evolving consumer preferences and competitive strategies that shape market dynamics.

Dominant Markets & Segments in Spain Satellite Communications Market

Within the Spanish Satellite Communications Market, the Maritime sector currently represents a dominant segment due to the critical need for reliable communication in offshore operations and coastal surveillance. The Defense and Government sector is another significant contributor, driven by the demand for secure and resilient communication systems for national security and public safety. The land-based segment holds substantial market share in serving the enterprise and media & entertainment industries.

- Key Drivers for Maritime Dominance: Stringent maritime regulations requiring reliable communication, increasing maritime trade, and growing adoption of satellite-based navigation systems.

- Key Drivers for Defense and Government Dominance: Government initiatives promoting national security, increased investments in military modernization, and rising demand for secure communication networks.

- Key Drivers for Land-Based Segment: Growth in enterprise IT infrastructure development and modernization, expansion of remote areas and digital inclusion programs.

The dominance analysis details the significant role of government initiatives, favorable regulatory environments, and the increasing adoption of cutting-edge technologies. Analysis also considers geographic variations in market penetration and consumption trends.

Spain Satellite Communications Market Product Innovations

Recent innovations in the Spanish satellite communications market focus on higher-throughput satellites, improved ground equipment capabilities, and the integration of advanced technologies such as artificial intelligence and machine learning. These innovations enhance the speed, reliability, and security of satellite communication services, making them more attractive to a wider range of end-users. New applications are emerging in various sectors, including the Internet of Things (IoT), remote sensing, and disaster management, driving market growth and creating new opportunities for market players. The successful integration of these technologies provides a significant competitive advantage in terms of improved performance, cost-effectiveness, and efficiency.

Report Segmentation & Scope

This report segments the Spain Satellite Communications Market across several key parameters:

By Type:

Ground Equipment: This segment encompasses the hardware and software used to establish and maintain satellite communication links, including earth stations, antennas, modems, and related infrastructure. The market size is projected to grow at xx% CAGR during the forecast period, with ongoing technological advancements driving innovation.

Services: This encompasses satellite-based communication services, including data transmission, voice communication, and broadcasting. The segment shows a CAGR of xx%, fueled by increasing demand for high-speed and reliable communication.

By Platform:

Portable: This segment covers portable satellite communication systems used in various applications, from emergency response to mobile journalism. The growth of this segment depends on improvements in battery life and portability.

Land: Satellite communication systems for fixed locations, serving businesses and organizations.

Maritime: Satellite communication tailored to maritime vessels and offshore operations. A major driver of growth for this segment is increased maritime trade and security protocols.

Airborne: Satellite communication systems deployed in aircraft and drones, primarily benefiting from the rising adoption of air mobility.

By End-user Vertical: Market segmentation details the unique requirements and growth potential in each vertical, from maritime and defense to media and entertainment.

Key Drivers of Spain Satellite Communications Market Growth

Several key factors are driving the growth of the Spain Satellite Communications Market:

- Government initiatives: Government funding and policies supporting infrastructure development and digitalization are accelerating market expansion.

- Technological advancements: The development of high-throughput satellites and improved ground equipment enhances speed and reliability.

- Increasing demand: Rising demand for broadband connectivity in remote areas and from various end-user segments is fueling market growth.

Challenges in the Spain Satellite Communications Market Sector

The Spanish satellite communications sector faces certain challenges:

- Regulatory hurdles: Navigating complex regulatory frameworks can create delays and increase project costs.

- Supply chain issues: Global supply chain disruptions can impact the availability and cost of satellite equipment and services.

- Competition: Intense competition from other communication technologies requires continuous innovation and investment.

Leading Players in the Spain Satellite Communications Market Market

- Satlink

- Indr

- SANTANDER TELEPORT S L

- Sateliot

- Thales Alenia Space Espana

- Hispasat

- Hisdesat Servicios EstratEgicos SA

- Telespazio S p A

- GMV

- Verasat Global SL

Key Developments in Spain Satellite Communications Market Sector

- January 2023: GMV secures a contract from Hisdesat for the SPAINSAT NG project, signifying significant investment in the sector and improving satellite functionality.

- July 2022: Satlink wins a three-year contract to provide broadband satellite communication solutions to the Spanish Civil Guard's patrol vessels, highlighting the growth in the maritime segment.

Strategic Spain Satellite Communications Market Market Outlook

The Spain Satellite Communications Market is poised for continued growth, driven by ongoing technological advancements, increasing demand for high-speed connectivity, and government support. Strategic opportunities exist for companies to expand their service offerings, enter new market segments, and leverage partnerships to enhance market share. The continued adoption of HTS technology and the expansion of satellite constellations promise to further enhance market potential. Companies that effectively navigate the regulatory landscape and address supply chain challenges will be best positioned for success.

Spain Satellite Communications Market Segmentation

-

1. Type

- 1.1. Ground Equipment

- 1.2. Services

-

2. Platform

- 2.1. Portable

- 2.2. Land

- 2.3. Maritime

- 2.4. Airborne

-

3. End-user Vertical

- 3.1. Maritime

- 3.2. Defense and Government

- 3.3. Enterprises

- 3.4. Media and Entertainment

- 3.5. Other End-user Verticals

Spain Satellite Communications Market Segmentation By Geography

- 1. Spain

Spain Satellite Communications Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.92% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Digital Transformation; Increasing Demand for Broadband Connectivity

- 3.3. Market Restrains

- 3.3.1. Interference in Transmission of Data; Regulatory and Spectrum Constraints

- 3.4. Market Trends

- 3.4.1. The media and entertainment segment is expected to hold a considerable market share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Satellite Communications Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Ground Equipment

- 5.1.2. Services

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Portable

- 5.2.2. Land

- 5.2.3. Maritime

- 5.2.4. Airborne

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. Maritime

- 5.3.2. Defense and Government

- 5.3.3. Enterprises

- 5.3.4. Media and Entertainment

- 5.3.5. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Satlink

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Indr

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 SANTANDER TELEPORT S L

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Sateliot

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Thales Alenia Space Espana

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Hispasat

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Hisdesat Servicios EstratEgicos SA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Telespazio S p A

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 GMV

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Verasat Global SL

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Satlink

List of Figures

- Figure 1: Spain Satellite Communications Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain Satellite Communications Market Share (%) by Company 2024

List of Tables

- Table 1: Spain Satellite Communications Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain Satellite Communications Market Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Spain Satellite Communications Market Revenue Million Forecast, by Platform 2019 & 2032

- Table 4: Spain Satellite Communications Market Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 5: Spain Satellite Communications Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Spain Satellite Communications Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Spain Satellite Communications Market Revenue Million Forecast, by Type 2019 & 2032

- Table 8: Spain Satellite Communications Market Revenue Million Forecast, by Platform 2019 & 2032

- Table 9: Spain Satellite Communications Market Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 10: Spain Satellite Communications Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Satellite Communications Market?

The projected CAGR is approximately 11.92%.

2. Which companies are prominent players in the Spain Satellite Communications Market?

Key companies in the market include Satlink, Indr, SANTANDER TELEPORT S L, Sateliot, Thales Alenia Space Espana, Hispasat, Hisdesat Servicios EstratEgicos SA, Telespazio S p A, GMV, Verasat Global SL.

3. What are the main segments of the Spain Satellite Communications Market?

The market segments include Type, Platform, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.76 Million as of 2022.

5. What are some drivers contributing to market growth?

Digital Transformation; Increasing Demand for Broadband Connectivity.

6. What are the notable trends driving market growth?

The media and entertainment segment is expected to hold a considerable market share.

7. Are there any restraints impacting market growth?

Interference in Transmission of Data; Regulatory and Spectrum Constraints.

8. Can you provide examples of recent developments in the market?

January 2023: A contract for the construction and development of the ground segment of the SPAINSAT NG project satellites was provided to multinational GMV by the Spanish government satellite provider Hisdesat. These two additional satellites, whose launches are planned for 2024 and 2025, will succeed the operator's existing SpainSat and XTAR-EUR spacecraft and significantly improve their functionality.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Satellite Communications Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Satellite Communications Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Satellite Communications Market?

To stay informed about further developments, trends, and reports in the Spain Satellite Communications Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence