Key Insights

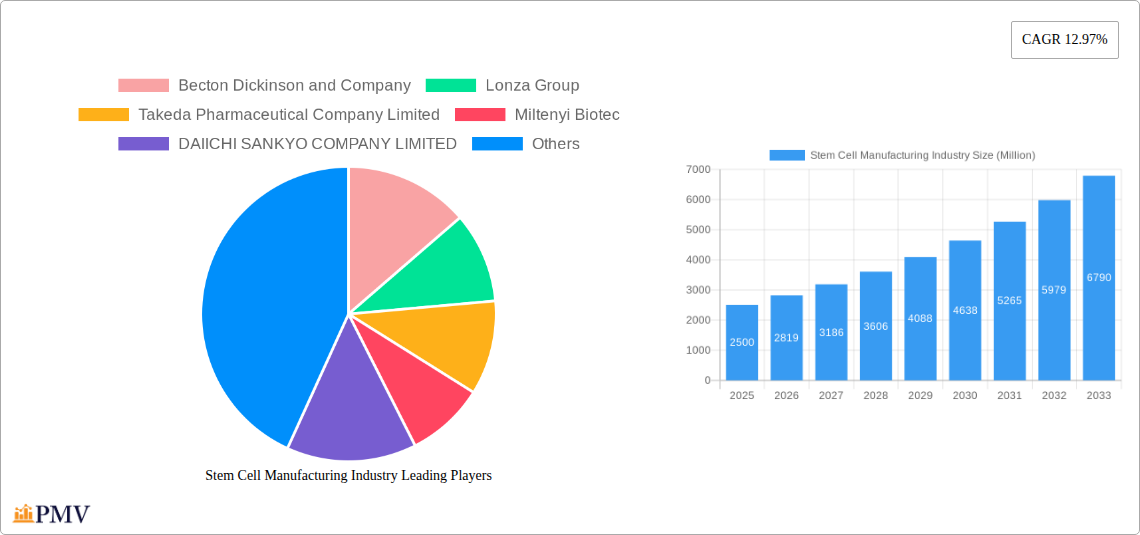

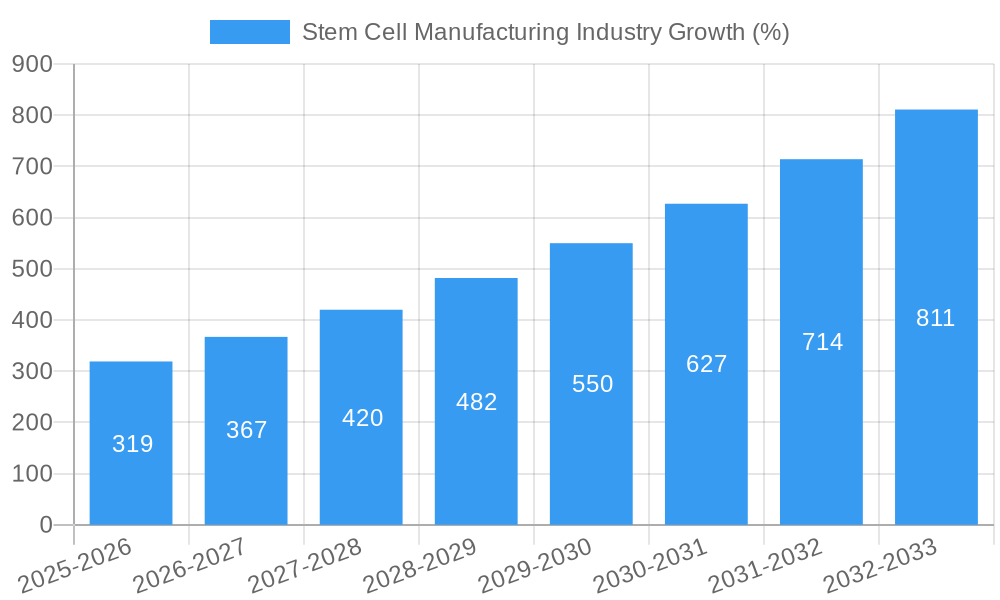

The global stem cell manufacturing market is experiencing robust growth, driven by the escalating demand for stem cell-based therapies and the increasing prevalence of chronic diseases requiring regenerative medicine solutions. The market, currently valued at approximately $XX million in 2025 (assuming a reasonable market size based on industry reports and the provided CAGR), is projected to expand at a compound annual growth rate (CAGR) of 12.97% from 2025 to 2033. This significant growth is fueled by several key factors, including advancements in stem cell research and technology, leading to improved efficacy and safety profiles of stem cell-based treatments. Furthermore, increased investments in research and development by pharmaceutical and biotechnology companies are accelerating the development of innovative stem cell therapies targeting a wide range of diseases, thus significantly boosting market expansion. The growing adoption of stem cell banking and the rising demand for personalized medicine also contribute to this positive trajectory. Different stem cell lines (embryonic, induced pluripotent, and adult) fuel the market’s diversity, with services encompassing cell culture, cryopreservation, and quality control vital to the industry's success. Products, such as culture media, purification reagents, and bioreactors, are essential components of the manufacturing process. Key players like Becton Dickinson, Lonza, and Thermo Fisher Scientific are actively shaping the market landscape through innovation and strategic collaborations.

The market segmentation reveals strong growth across various applications, with stem cell therapy and drug discovery and development leading the charge. Pharmaceutical and biotechnology companies represent the largest end-user segment, indicating the industry's strong reliance on this sector for research, development, and commercialization. Geographically, North America and Europe currently hold significant market share, owing to robust research infrastructure and regulatory frameworks. However, the Asia-Pacific region is expected to witness remarkable growth in the forecast period, driven by increased healthcare spending, burgeoning biotech industries, and rising awareness of advanced medical therapies. While challenges such as stringent regulatory approvals and ethical considerations may act as restraints, the overall outlook for the stem cell manufacturing market remains highly optimistic, fueled by continuous technological advancements and the urgent need for effective treatments for debilitating diseases.

This in-depth report provides a comprehensive analysis of the global stem cell manufacturing industry, offering valuable insights for stakeholders across the value chain. The study covers the period from 2019 to 2033, with a focus on the forecast period from 2025 to 2033 and a base year of 2025. The report projects a market size of xx Million by 2033, exhibiting a CAGR of xx% during the forecast period. This detailed analysis incorporates key market segments, leading players, technological advancements, and regulatory landscapes to provide a complete picture of this rapidly evolving sector.

Stem Cell Manufacturing Industry Market Structure & Competitive Dynamics

The stem cell manufacturing industry is characterized by a moderately concentrated market structure, with several large multinational corporations holding significant market share. Key players like Becton Dickinson and Company, Lonza Group, and Thermo Fisher Scientific dominate the market, leveraging their established infrastructure and extensive product portfolios. However, a number of smaller, specialized companies are also actively participating, particularly in niche applications. The industry is witnessing increased M&A activity, driven by the desire to expand product offerings, access new technologies, and enhance market presence. Recent deals, although exact values are not publicly available for all, have involved investments in the hundreds of Millions of USD, showcasing the significant capital investment in this sector.

Market Concentration: The top 5 players account for approximately xx% of the global market share in 2025. This percentage is projected to remain relatively stable throughout the forecast period, however, the market dynamics may shift due to increasing competition and technological advancements.

Innovation Ecosystems: Collaboration between academic institutions, research organizations, and private companies is a prominent feature of the stem cell manufacturing industry, leading to significant advancements in cell culture technologies and manufacturing processes.

Regulatory Frameworks: Stringent regulatory frameworks, particularly those related to Good Manufacturing Practices (GMP) and cell therapy approval processes, play a significant role in shaping industry dynamics. These regulations influence the cost and timeline for product development and commercialization.

Product Substitutes: While direct substitutes for stem cell-based products are limited, emerging technologies such as gene therapy and other regenerative medicine approaches present indirect competition.

End-User Trends: The increasing demand for personalized medicine and advanced therapeutic modalities is driving growth in the stem cell manufacturing industry. Pharmaceutical and biotechnology companies are significant end-users, leveraging stem cells for drug discovery and development. Additionally, the expansion of stem cell banking and regenerative medicine applications is fueling market growth.

M&A Activities: Several significant mergers and acquisitions have occurred in recent years, exceeding xx Million USD in total value. These transactions reflect the strategic importance of this industry and the consolidation trends among market participants. For instance, the acquisition of xx by xx in xx resulted in an expansion of the product portfolio and market access.

Stem Cell Manufacturing Industry Industry Trends & Insights

The stem cell manufacturing industry is experiencing significant growth, driven by several key trends. The rising prevalence of chronic diseases like cancer, diabetes, and neurodegenerative disorders is a major driver of demand for stem cell-based therapies. Technological advancements, particularly in automation and process optimization, are contributing to increased efficiency and reduced manufacturing costs. Furthermore, a growing understanding of stem cell biology and its therapeutic potential is leading to the development of novel therapies and applications. The industry is undergoing a transformation, propelled by increased funding, accelerated technological innovation, and evolving regulatory landscapes. This is fostering a competitive environment, with significant R&D investments fueling the expansion of the market. However, the market penetration of stem cell therapies remains relatively low compared to traditional medical treatments, creating opportunities for industry players to capture market share. Significant government investments and initiatives are accelerating the growth of the stem cell manufacturing industry, providing financial support for research and development projects and promoting the commercialization of stem cell-based products. The adoption of advanced technologies like artificial intelligence and machine learning (AI/ML) for process optimization and quality control is likely to be a primary growth driver in the coming years.

The Compound Annual Growth Rate (CAGR) for the industry is projected to be xx% from 2025 to 2033. Market penetration of stem cell therapies is expected to increase significantly over the forecast period. However, challenges, such as regulatory hurdles and high manufacturing costs, are anticipated to remain barriers to market penetration.

Dominant Markets & Segments in Stem Cell Manufacturing Industry

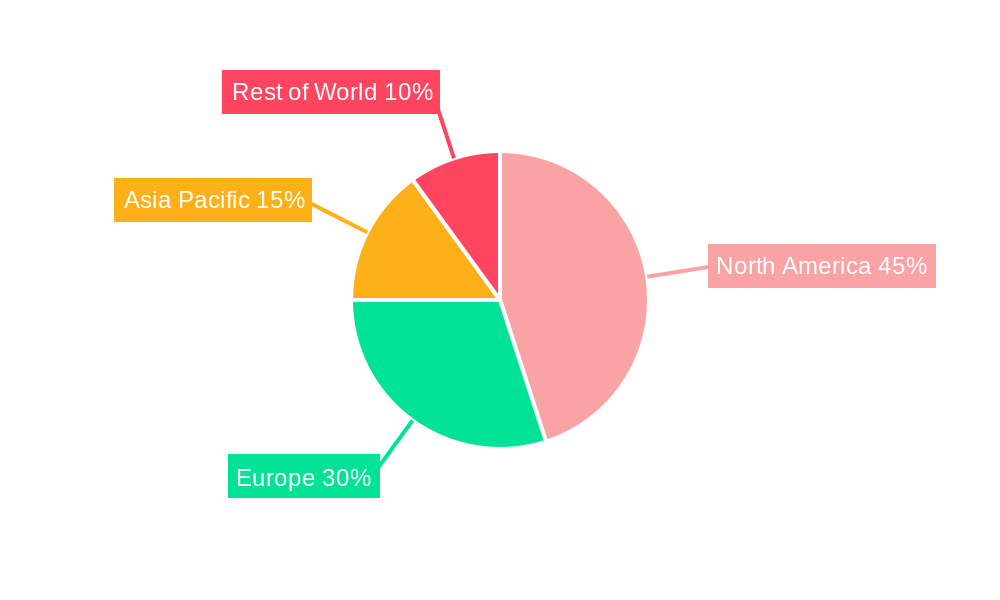

The North American region currently holds the largest market share in the stem cell manufacturing industry, driven by robust research infrastructure, substantial funding, and an established regulatory framework. However, regions such as Asia Pacific are experiencing rapid growth, especially in countries with expanding healthcare infrastructure and increasing government support for biotechnology. This expansion is attributed to factors such as rising disposable incomes, and increased healthcare awareness.

Key Drivers:

- Economic policies: Favorable government policies and funding programs supporting the development of stem cell therapies.

- Infrastructure: Advanced research facilities and well-developed healthcare infrastructure.

- Regulatory framework: Supportive regulations that accelerate the approval and commercialization of innovative therapies.

Dominance Analysis: North America's dominance stems from a combination of factors including advanced research infrastructure, early adoption of stem cell technologies, and substantial investments from both public and private sectors. While the European market is also substantial, regulatory complexities and slower adoption rates contribute to its relatively smaller share compared to North America. Asia Pacific represents a significant growth opportunity, exhibiting strong potential due to its large population and growing healthcare sector, however, regulatory hurdles remain a challenge.

Stem Cell Lines: Induced pluripotent stem cells (iPSCs) are rapidly gaining traction owing to their versatility and potential for personalized medicine. Embryonic stem cells (ESCs) remain a significant segment, although ethical considerations and regulatory hurdles restrict their widespread use. Adult stem cells are another important segment, offering advantages such as reduced ethical concerns and easier accessibility. The market is anticipated to be dominated by iPSCs in the near future, with xx Million revenue by 2033.

Type: Bioreactors are expected to be a significant segment owing to their ability to facilitate large-scale stem cell production and process optimization. The market for purification reagents and culture media is expected to experience substantial growth, driven by increasing demand for high-quality stem cell products.

Services: Cell culture services form the largest segment due to the widespread use of outsourced manufacturing capabilities. Cryopreservation services are also essential for long-term storage and preservation of stem cells.

Applications: Stem cell therapy is projected to be the largest application segment, followed by drug discovery and development. Stem cell banking is also showing increasing demand for future clinical applications.

End Users: Pharmaceutical and biotechnology companies represent the largest end-user segment, with a substantial market share. Academic and research institutions contribute significantly to the market growth. Cell banks and tissue banks serve as important intermediaries in the supply chain.

Stem Cell Manufacturing Industry Product Innovations

Significant advancements in bioreactor technology, including single-use systems and automated platforms, are improving the efficiency and scalability of stem cell manufacturing processes. Advances in cell purification techniques and media formulations are enhancing the quality and consistency of stem cell products. This leads to cost reductions and improved product yields for the industry. These innovations are not only streamlining the manufacturing process but also enhancing the safety and efficacy of stem cell-based therapies. This innovation drive is fostering new applications for stem cells in various therapeutic areas.

Report Segmentation & Scope

This report segments the stem cell manufacturing industry by stem cell lines (embryonic, iPSC, adult), product type (culture media, purification reagents, bioreactors), services (cell culture, cryopreservation, quality control), applications (stem cell therapy, drug discovery, stem cell banking, regenerative medicine), and end users (pharmaceutical/biotech companies, cell banks, academic institutions). Growth projections, market sizes, and competitive dynamics are analyzed for each segment. The market for each segment is expected to experience significant growth over the next decade, driven by advancements in stem cell research, increased demand, and technological advancements. The competitive landscape within each segment varies, with some characterized by a high degree of concentration and others showing greater fragmentation.

Key Drivers of Stem Cell Manufacturing Industry Growth

Technological advancements, such as the development of advanced bioreactors and automated cell processing systems, are significantly driving market growth. Increased government funding for stem cell research and development, coupled with a growing acceptance of stem cell therapies, is further accelerating market expansion. The rising prevalence of chronic diseases, along with the increased demand for regenerative medicine solutions, are fueling market growth. Regulatory approvals for new stem cell-based therapies are also key growth drivers. For example, the recent approval of xx by xx in xx significantly boosted the market.

Challenges in the Stem Cell Manufacturing Industry Sector

The high cost of manufacturing stem cell products, particularly in complying with stringent GMP regulations, poses a major challenge. Supply chain complexities and the need to maintain the quality and consistency of stem cells throughout the manufacturing process create additional difficulties. Regulatory uncertainties and varying regulatory pathways across different jurisdictions further add to the challenges faced by manufacturers. Competition from emerging therapeutic modalities, such as gene therapy, is further adding pressure to the industry. Moreover, the limited availability of skilled labor in stem cell manufacturing poses a significant recruitment hurdle for many companies.

Leading Players in the Stem Cell Manufacturing Industry Market

- Becton Dickinson and Company

- Lonza Group

- Takeda Pharmaceutical Company Limited

- Miltenyi Biotec

- DAIICHI SANKYO COMPANY LIMITED

- AbbVie Inc

- Pluristem Therapeutics Inc

- Sartorius

- Merck Group

- Fujifilm Holdings Corporation (Cellular Dynamics)

- Thermo Fisher Scientific

- Stemcell Technologies

- Corning Incorporated

Key Developments in Stem Cell Manufacturing Industry Sector

August 2022: Applied StemCell, Inc. (ASC) expanded its Current Good Manufacturing (cGMP) facility, adding 4 new cGMP cleanrooms, cryo-storage, process development, and QC/QA space. This expansion signifies a significant increase in manufacturing capacity and the growing demand for cGMP-compliant stem cell manufacturing services.

January 2022: Cellino Biotech raised USD 80 Million in Series A funding, highlighting the significant investment in stem cell manufacturing technology and its potential to address the challenges in the biotech industry. This funding will support the company's goal of building the first autonomous human cell foundry by 2025.

Strategic Stem Cell Manufacturing Industry Market Outlook

The future of the stem cell manufacturing industry is exceptionally promising. Continued advancements in stem cell technology and the growing understanding of stem cell biology are expected to fuel further market growth. The increasing demand for personalized medicine and the expansion of regenerative medicine applications will create significant opportunities for market participants. Strategic partnerships and collaborations between research institutions, biotechnology companies, and pharmaceutical companies are likely to play a pivotal role in driving innovation and accelerating the commercialization of stem cell-based therapies. The industry is poised for significant expansion, with a continued focus on improving the efficiency, scalability, and affordability of stem cell manufacturing processes. The global market is expected to witness a substantial increase in adoption, and the continued exploration of novel stem cell applications will contribute to sustained market growth.

Stem Cell Manufacturing Industry Segmentation

-

1. Type

-

1.1. Product

- 1.1.1. Culture Media

- 1.1.2. Consumables

- 1.1.3. Instruments

- 1.1.4. Stem Cell Lines

- 1.2. Services

-

1.1. Product

-

2. Application

- 2.1. Stem Cell Therapy

- 2.2. Drug Discovery and Development

- 2.3. Stem Cell Banking

-

3. End User

- 3.1. Pharmaceutical and Biotechnology Companies

- 3.2. Cell Banks and Tissue Banks

- 3.3. Other End Users

Stem Cell Manufacturing Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Stem Cell Manufacturing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 12.97% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Technological Advancements in Stem Cell Manufacturing and Preservation; Growing Public Awareness About the Therapeutic Potency of Stem Cell Products; Growing Public-Private Investments and Funding in Stem Cell-based Research

- 3.3. Market Restrains

- 3.3.1. High Operational Costs Associated with Stem Cell Manufacturing and Banking

- 3.4. Market Trends

- 3.4.1. Stem Cell Banking Segment is Likely to Witness a Significant Growth in the Stem Cell Manufacturing Market Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Product

- 5.1.1.1. Culture Media

- 5.1.1.2. Consumables

- 5.1.1.3. Instruments

- 5.1.1.4. Stem Cell Lines

- 5.1.2. Services

- 5.1.1. Product

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Stem Cell Therapy

- 5.2.2. Drug Discovery and Development

- 5.2.3. Stem Cell Banking

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Pharmaceutical and Biotechnology Companies

- 5.3.2. Cell Banks and Tissue Banks

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Product

- 6.1.1.1. Culture Media

- 6.1.1.2. Consumables

- 6.1.1.3. Instruments

- 6.1.1.4. Stem Cell Lines

- 6.1.2. Services

- 6.1.1. Product

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Stem Cell Therapy

- 6.2.2. Drug Discovery and Development

- 6.2.3. Stem Cell Banking

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Pharmaceutical and Biotechnology Companies

- 6.3.2. Cell Banks and Tissue Banks

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Product

- 7.1.1.1. Culture Media

- 7.1.1.2. Consumables

- 7.1.1.3. Instruments

- 7.1.1.4. Stem Cell Lines

- 7.1.2. Services

- 7.1.1. Product

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Stem Cell Therapy

- 7.2.2. Drug Discovery and Development

- 7.2.3. Stem Cell Banking

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Pharmaceutical and Biotechnology Companies

- 7.3.2. Cell Banks and Tissue Banks

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Product

- 8.1.1.1. Culture Media

- 8.1.1.2. Consumables

- 8.1.1.3. Instruments

- 8.1.1.4. Stem Cell Lines

- 8.1.2. Services

- 8.1.1. Product

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Stem Cell Therapy

- 8.2.2. Drug Discovery and Development

- 8.2.3. Stem Cell Banking

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Pharmaceutical and Biotechnology Companies

- 8.3.2. Cell Banks and Tissue Banks

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East and Africa Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Product

- 9.1.1.1. Culture Media

- 9.1.1.2. Consumables

- 9.1.1.3. Instruments

- 9.1.1.4. Stem Cell Lines

- 9.1.2. Services

- 9.1.1. Product

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Stem Cell Therapy

- 9.2.2. Drug Discovery and Development

- 9.2.3. Stem Cell Banking

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Pharmaceutical and Biotechnology Companies

- 9.3.2. Cell Banks and Tissue Banks

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Product

- 10.1.1.1. Culture Media

- 10.1.1.2. Consumables

- 10.1.1.3. Instruments

- 10.1.1.4. Stem Cell Lines

- 10.1.2. Services

- 10.1.1. Product

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Stem Cell Therapy

- 10.2.2. Drug Discovery and Development

- 10.2.3. Stem Cell Banking

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Pharmaceutical and Biotechnology Companies

- 10.3.2. Cell Banks and Tissue Banks

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. North America Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America Stem Cell Manufacturing Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Becton Dickinson and Company

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Lonza Group

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Takeda Pharmaceutical Company Limited

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Miltenyi Biotec

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 DAIICHI SANKYO COMPANY LIMITED

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 AbbVie Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Pluristem Therapeutics Inc

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Sartorius

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Merck Group

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Fujifilm Holdings Corporation (Cellular Dynamics)

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Thermo Fisher Scientific

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Stemcell Technologies

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Corning Incorporated

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.1 Becton Dickinson and Company

List of Figures

- Figure 1: Global Stem Cell Manufacturing Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Stem Cell Manufacturing Industry Revenue (Million), by Type 2024 & 2032

- Figure 13: North America Stem Cell Manufacturing Industry Revenue Share (%), by Type 2024 & 2032

- Figure 14: North America Stem Cell Manufacturing Industry Revenue (Million), by Application 2024 & 2032

- Figure 15: North America Stem Cell Manufacturing Industry Revenue Share (%), by Application 2024 & 2032

- Figure 16: North America Stem Cell Manufacturing Industry Revenue (Million), by End User 2024 & 2032

- Figure 17: North America Stem Cell Manufacturing Industry Revenue Share (%), by End User 2024 & 2032

- Figure 18: North America Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: North America Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Europe Stem Cell Manufacturing Industry Revenue (Million), by Type 2024 & 2032

- Figure 21: Europe Stem Cell Manufacturing Industry Revenue Share (%), by Type 2024 & 2032

- Figure 22: Europe Stem Cell Manufacturing Industry Revenue (Million), by Application 2024 & 2032

- Figure 23: Europe Stem Cell Manufacturing Industry Revenue Share (%), by Application 2024 & 2032

- Figure 24: Europe Stem Cell Manufacturing Industry Revenue (Million), by End User 2024 & 2032

- Figure 25: Europe Stem Cell Manufacturing Industry Revenue Share (%), by End User 2024 & 2032

- Figure 26: Europe Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Europe Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Asia Pacific Stem Cell Manufacturing Industry Revenue (Million), by Type 2024 & 2032

- Figure 29: Asia Pacific Stem Cell Manufacturing Industry Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Stem Cell Manufacturing Industry Revenue (Million), by Application 2024 & 2032

- Figure 31: Asia Pacific Stem Cell Manufacturing Industry Revenue Share (%), by Application 2024 & 2032

- Figure 32: Asia Pacific Stem Cell Manufacturing Industry Revenue (Million), by End User 2024 & 2032

- Figure 33: Asia Pacific Stem Cell Manufacturing Industry Revenue Share (%), by End User 2024 & 2032

- Figure 34: Asia Pacific Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Asia Pacific Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million), by Type 2024 & 2032

- Figure 37: Middle East and Africa Stem Cell Manufacturing Industry Revenue Share (%), by Type 2024 & 2032

- Figure 38: Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million), by Application 2024 & 2032

- Figure 39: Middle East and Africa Stem Cell Manufacturing Industry Revenue Share (%), by Application 2024 & 2032

- Figure 40: Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million), by End User 2024 & 2032

- Figure 41: Middle East and Africa Stem Cell Manufacturing Industry Revenue Share (%), by End User 2024 & 2032

- Figure 42: Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Middle East and Africa Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

- Figure 44: South America Stem Cell Manufacturing Industry Revenue (Million), by Type 2024 & 2032

- Figure 45: South America Stem Cell Manufacturing Industry Revenue Share (%), by Type 2024 & 2032

- Figure 46: South America Stem Cell Manufacturing Industry Revenue (Million), by Application 2024 & 2032

- Figure 47: South America Stem Cell Manufacturing Industry Revenue Share (%), by Application 2024 & 2032

- Figure 48: South America Stem Cell Manufacturing Industry Revenue (Million), by End User 2024 & 2032

- Figure 49: South America Stem Cell Manufacturing Industry Revenue Share (%), by End User 2024 & 2032

- Figure 50: South America Stem Cell Manufacturing Industry Revenue (Million), by Country 2024 & 2032

- Figure 51: South America Stem Cell Manufacturing Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Germany Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United Kingdom Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: France Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Italy Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Spain Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Rest of Europe Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: China Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Japan Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: India Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Australia Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: South Korea Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Rest of Asia Pacific Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 25: GCC Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: South Africa Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Rest of Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: Brazil Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 33: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 34: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 35: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: United States Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Canada Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Mexico Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 40: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 41: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 42: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 43: Germany Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: United Kingdom Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: France Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Italy Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Spain Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Europe Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 50: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 51: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 52: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 53: China Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Japan Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: India Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Australia Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: South Korea Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: Rest of Asia Pacific Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 60: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 61: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 62: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 63: GCC Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 64: South Africa Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Rest of Middle East and Africa Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 67: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 68: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 69: Global Stem Cell Manufacturing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 70: Brazil Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 71: Argentina Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 72: Rest of South America Stem Cell Manufacturing Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Stem Cell Manufacturing Industry?

The projected CAGR is approximately 12.97%.

2. Which companies are prominent players in the Stem Cell Manufacturing Industry?

Key companies in the market include Becton Dickinson and Company, Lonza Group, Takeda Pharmaceutical Company Limited, Miltenyi Biotec, DAIICHI SANKYO COMPANY LIMITED, AbbVie Inc, Pluristem Therapeutics Inc, Sartorius, Merck Group, Fujifilm Holdings Corporation (Cellular Dynamics), Thermo Fisher Scientific, Stemcell Technologies, Corning Incorporated.

3. What are the main segments of the Stem Cell Manufacturing Industry?

The market segments include Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Technological Advancements in Stem Cell Manufacturing and Preservation; Growing Public Awareness About the Therapeutic Potency of Stem Cell Products; Growing Public-Private Investments and Funding in Stem Cell-based Research.

6. What are the notable trends driving market growth?

Stem Cell Banking Segment is Likely to Witness a Significant Growth in the Stem Cell Manufacturing Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Operational Costs Associated with Stem Cell Manufacturing and Banking.

8. Can you provide examples of recent developments in the market?

In August 2022, Applied StemCell, Inc. (ASC), a cell and gene therapy CRO/CDMO focused on supporting the research community and biotechnology industry for their needs in developing and manufacturing cell and gene products, expanded its Current Good Manufacturing (cGMP) facility. ASC has successfully carried out cell banking and product manufacturing projects in its current cGMP suite and is now set on building 4 additional cGMP cleanrooms, cryo-storage space, process development, and QC/QA space.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Stem Cell Manufacturing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Stem Cell Manufacturing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Stem Cell Manufacturing Industry?

To stay informed about further developments, trends, and reports in the Stem Cell Manufacturing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence