Key Insights

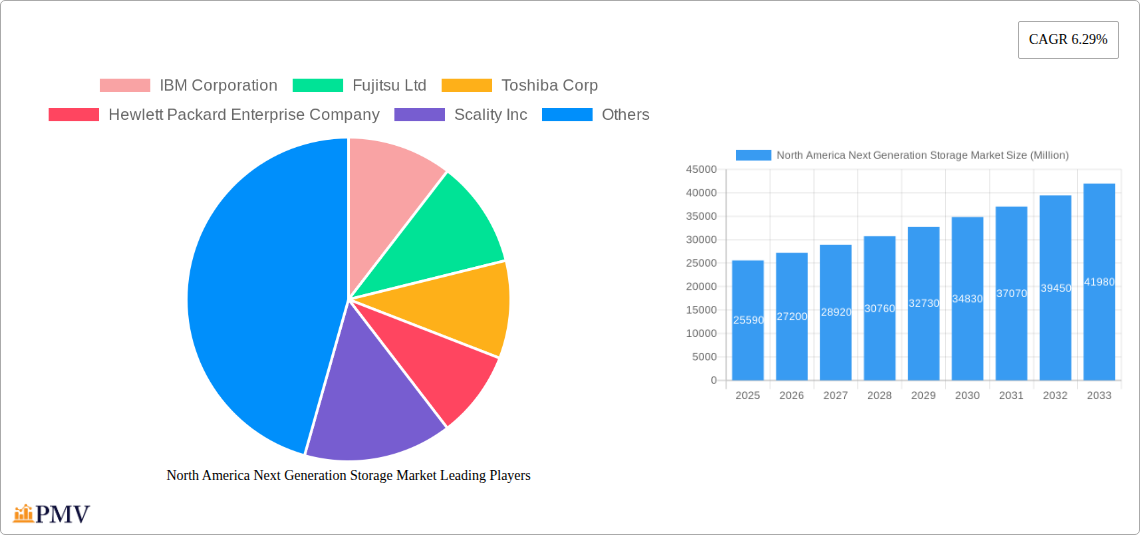

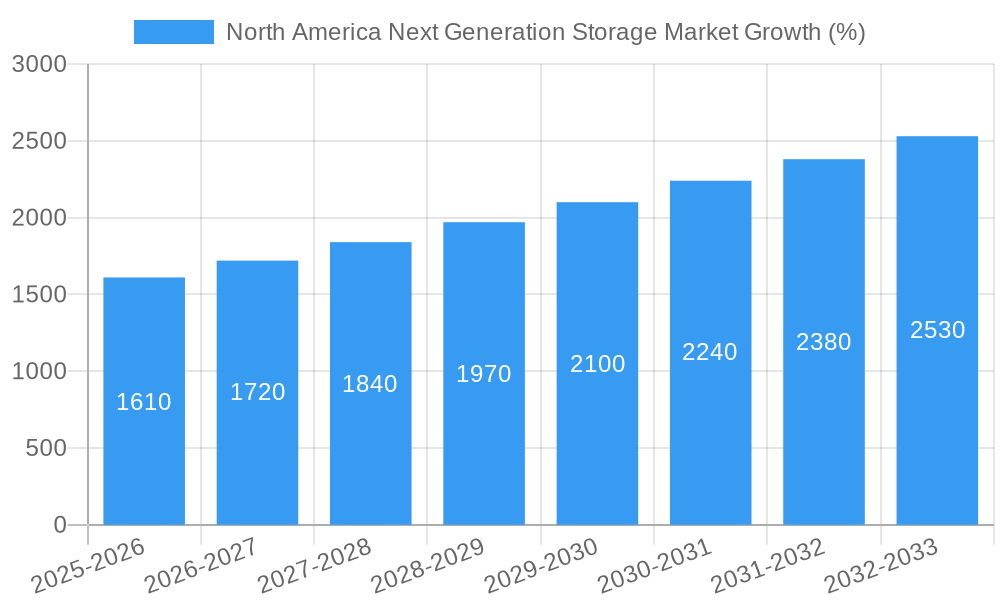

The North American next-generation storage market, valued at $25.59 billion in 2025, is projected to experience robust growth, driven by the increasing adoption of cloud computing, big data analytics, and the Internet of Things (IoT). The market's Compound Annual Growth Rate (CAGR) of 6.29% from 2019 to 2024 indicates a consistent upward trajectory, which is expected to continue throughout the forecast period (2025-2033). Key drivers include the rising demand for enhanced data security and disaster recovery solutions, coupled with the need for scalable and efficient storage infrastructure to manage ever-increasing data volumes generated by various end-user industries. The BFSI, retail, IT and telecom, healthcare, and media and entertainment sectors are significant contributors to market growth, fueled by their increasing reliance on data-driven decision-making and digital transformation initiatives. Growth within the segment is further spurred by the transition towards advanced storage architectures like File and Object-based Storage (FOBS) and Block Storage, offering improved performance, flexibility, and cost optimization compared to traditional Direct Attached Storage (DAS) and Network Attached Storage (NAS) systems. While the market faces some restraints, including concerns regarding data privacy and security, and the complexity of managing hybrid cloud environments, the overall outlook remains positive, driven by continuous innovation and the adoption of advanced storage technologies.

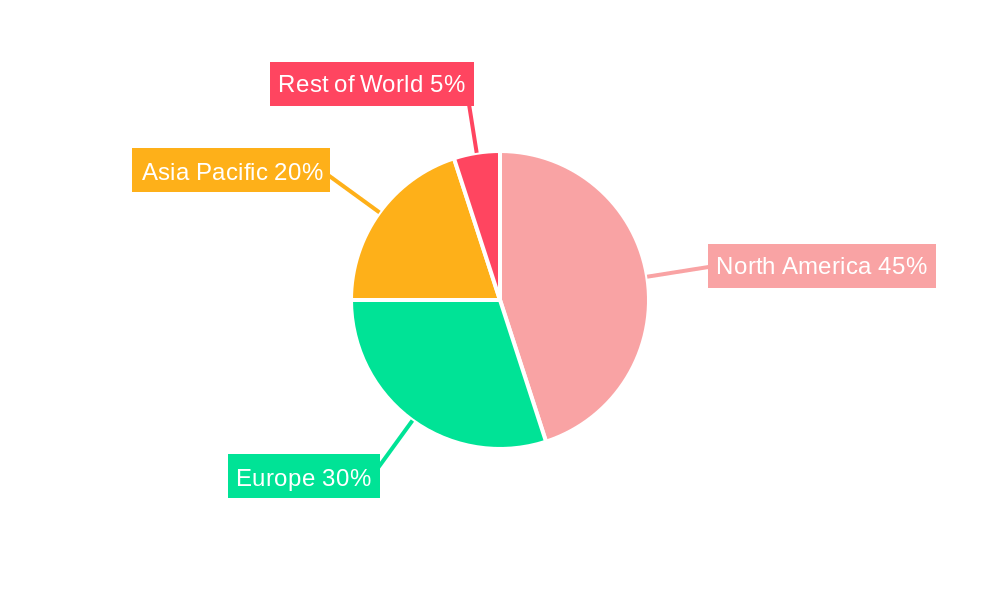

The competitive landscape is characterized by the presence of both established players like IBM, Dell, NetApp, and Hewlett Packard Enterprise, and emerging innovative companies such as Scality and Pure Storage. These companies are strategically investing in research and development to enhance their product offerings and expand their market share. The North American market, encompassing the United States, Canada, and Mexico, holds a significant portion of the global next-generation storage market, owing to its advanced technological infrastructure and strong adoption of cloud-based solutions. Continued growth is expected to be fueled by the increasing investment in digital infrastructure, the burgeoning adoption of artificial intelligence and machine learning applications, and the sustained demand for high-performance computing resources. Further penetration into specific market segments, particularly within healthcare and the media and entertainment sectors, presents significant opportunities for vendors to expand their reach and revenue streams.

North America Next Generation Storage Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America next-generation storage market, covering the period 2019-2033. It delves into market structure, competitive dynamics, industry trends, dominant segments, product innovations, and key challenges, offering valuable insights for stakeholders across the storage ecosystem. The report leverages extensive data analysis, including market size estimations (in Millions), CAGR projections, and competitive benchmarking, to paint a complete picture of this rapidly evolving market. The Base Year for this report is 2025, with an Estimated Year of 2025 and a Forecast Period of 2025-2033. The Historical Period covered is 2019-2024.

North America Next Generation Storage Market Structure & Competitive Dynamics

The North American next-generation storage market is characterized by a moderately concentrated landscape, with a few major players holding significant market share. However, the presence of numerous smaller, specialized vendors fosters a dynamic competitive environment driven by continuous innovation. The market is subject to evolving regulatory frameworks concerning data privacy and security, impacting vendor strategies and investment decisions. Product substitution, particularly the shift towards cloud-based solutions, is a significant factor, compelling traditional vendors to adapt their offerings. End-user trends, such as increasing adoption of digital transformation initiatives across various sectors, fuel demand for robust and scalable storage solutions. Mergers and acquisitions (M&A) activity is relatively frequent, reflecting industry consolidation and the pursuit of technological capabilities.

- Market Concentration: The top 5 vendors account for approximately xx% of the market share in 2025.

- Innovation Ecosystems: Strong emphasis on R&D, particularly in areas like AI-driven data management and edge computing.

- Regulatory Frameworks: Compliance with regulations like GDPR and CCPA influences storage solutions design and implementation.

- Product Substitutes: Cloud storage services pose a significant challenge to traditional on-premises storage solutions.

- End-User Trends: Growing demand for high-performance computing (HPC) and big data analytics drives storage capacity requirements.

- M&A Activities: The total value of M&A deals in the sector during 2019-2024 was approximately $xx Million, with an average deal size of $xx Million.

North America Next Generation Storage Market Industry Trends & Insights

The North American next-generation storage market exhibits robust growth, driven by factors such as the proliferation of data, the rise of cloud computing, and the increasing adoption of digital transformation initiatives across various industries. The market is experiencing significant technological disruptions, particularly in areas such as NVMe, flash storage, and software-defined storage. Consumer preferences are shifting towards solutions offering enhanced scalability, agility, and cost-effectiveness. Intense competitive dynamics necessitate continuous innovation and the development of value-added services to retain market share. The market is expected to achieve a CAGR of xx% during the forecast period (2025-2033), with market penetration in key sectors like BFSI and healthcare exceeding xx% by 2033.

Dominant Markets & Segments in North America Next Generation Storage Market

The United States dominates the North American next-generation storage market, driven by a strong IT infrastructure, high technology adoption rates, and substantial investments in data centers. Within storage systems, SAN continues to hold a significant market share, though NAS and DAS remain relevant for specific use cases. File and object-based storage (FOBS) is gaining traction due to its scalability and cost-effectiveness, while block storage remains crucial for mission-critical applications.

- Leading Region: United States

- Dominant Storage System: SAN (Storage Area Network)

- Leading Storage Architecture: FOBS (File and Object-based Storage), driven by cloud adoption.

- Leading End-User Industries: BFSI (Banking, Financial Services, and Insurance), IT and Telecom, and Healthcare.

Key Drivers for Dominant Segments:

- BFSI: Stringent regulatory compliance requirements and the need for secure data management.

- IT and Telecom: High data volumes and the demand for high-performance computing.

- Healthcare: Growing adoption of electronic health records (EHRs) and the need for data security.

North America Next Generation Storage Market Product Innovations

Recent product innovations focus on enhanced performance, scalability, and data security. The adoption of NVMe technology significantly boosts storage speeds, while advancements in flash storage offer increased density and reduced latency. Software-defined storage solutions enable greater agility and flexibility. The integration of AI and machine learning is enhancing data management capabilities, optimizing storage utilization, and improving data protection. These innovations are improving market fit by addressing the growing needs for efficient and secure data storage in diverse environments.

Report Segmentation & Scope

This report segments the North America next-generation storage market based on storage system (DAS, NAS, SAN), storage architecture (FOBS, Block Storage), and end-user industry (BFSI, Retail, IT & Telecom, Healthcare, Media & Entertainment). Each segment's growth projections, market size, and competitive dynamics are analyzed in detail. For example, the SAN segment is projected to grow at a CAGR of xx% due to its suitability for mission-critical applications, while the FOBS segment is experiencing rapid expansion due to cloud adoption and its cost-effectiveness. The competitive landscape within each segment varies, with some dominated by a few key players while others showcase more diverse participation.

Key Drivers of North America Next Generation Storage Market Growth

Several factors fuel the growth of the North American next-generation storage market. The exponential growth of data necessitates scalable storage solutions. The increasing adoption of cloud computing, big data analytics, and AI requires robust and efficient storage infrastructure. Furthermore, government initiatives promoting digital transformation across various sectors are driving investments in advanced storage technologies. Finally, the strengthening emphasis on data security and compliance further stimulates demand for robust and secure storage solutions.

Challenges in the North America Next Generation Storage Market Sector

The North American next-generation storage market faces challenges including the high initial investment costs associated with adopting advanced storage technologies, the complexity of integrating new storage solutions into existing IT infrastructure, and the need for skilled personnel to manage and maintain these systems. Supply chain disruptions can impact the availability of components, and competitive pressures from both established players and emerging cloud-based solutions create a dynamic and challenging market environment. These factors can impact overall market growth and adoption rates in certain segments.

Leading Players in the North America Next Generation Storage Market Market

- IBM Corporation

- Fujitsu Ltd

- Toshiba Corp

- Hewlett Packard Enterprise Company

- Scality Inc

- Hitachi Ltd

- Netgear Inc

- Dell Inc

- DataDirect Networks

- NetApp Inc

- Pure Storage Inc

Key Developments in North America Next Generation Storage Market Sector

- July 2022: QNAP Systems, Inc. launched an industrial 10GbE NAS (TS-i410X), targeting demanding environments like factories and warehouses. This expansion into ruggedized storage solutions addresses a niche market with specific needs.

- June 2022: Nasuni Corporation's acquisition of Storage Made Easy (SME) strengthens its cloud file services portfolio, enhancing its competitive position in the market for remote work and compliance-focused solutions. This acquisition signals a trend towards consolidation and enhanced capabilities in cloud-based file management.

Strategic North America Next Generation Storage Market Outlook

The future of the North American next-generation storage market is bright, driven by continued data growth, the expansion of cloud computing adoption, and the increasing demand for high-performance computing resources. Strategic opportunities exist for vendors who can effectively address the challenges of data security, compliance, and cost optimization. Investments in AI and machine learning for data management will play a key role in shaping future market dynamics. The market will continue to see consolidation through M&A activities as companies seek to expand their capabilities and market share. This report offers insights and analyses to help vendors, investors, and other stakeholders navigate this evolving landscape effectively and capitalize on emerging opportunities.

North America Next Generation Storage Market Segmentation

-

1. Storage System

- 1.1. Direct Attached Storage (DAS)

- 1.2. Network Attached Storage (NAS)

- 1.3. Storage Area Network (SAN)

-

2. Storage Architecture

- 2.1. File and Object-based Storage (FOBS)

- 2.2. Block Storage

-

3. End-User Industry

- 3.1. BFSI

- 3.2. Retail

- 3.3. IT and Telecom

- 3.4. Healthcare

- 3.5. Media and Entertainment

North America Next Generation Storage Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Next Generation Storage Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.29% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Volume of Digital Data; Rising Adoption of Solid-state Devices; Increasing Proliferation of Smartphones

- 3.2.2 Laptops

- 3.2.3 and Tablets

- 3.3. Market Restrains

- 3.3.1. Lack of Data Security in Cloud- and Server-based Services

- 3.4. Market Trends

- 3.4.1 Increasing Proliferation of Smartphones

- 3.4.2 connected devices and electronic devices will drive the market.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Next Generation Storage Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Storage System

- 5.1.1. Direct Attached Storage (DAS)

- 5.1.2. Network Attached Storage (NAS)

- 5.1.3. Storage Area Network (SAN)

- 5.2. Market Analysis, Insights and Forecast - by Storage Architecture

- 5.2.1. File and Object-based Storage (FOBS)

- 5.2.2. Block Storage

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. BFSI

- 5.3.2. Retail

- 5.3.3. IT and Telecom

- 5.3.4. Healthcare

- 5.3.5. Media and Entertainment

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Storage System

- 6. United States North America Next Generation Storage Market Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Next Generation Storage Market Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Next Generation Storage Market Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Next Generation Storage Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 IBM Corporation

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Fujitsu Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Toshiba Corp

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Hewlett Packard Enterprise Company

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Scality Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Hitachi Ltd

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Netgear Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Dell Inc

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 DataDirect Networks

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 NetApp Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Pure Storage Inc

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.1 IBM Corporation

List of Figures

- Figure 1: North America Next Generation Storage Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Next Generation Storage Market Share (%) by Company 2024

List of Tables

- Table 1: North America Next Generation Storage Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Next Generation Storage Market Revenue Million Forecast, by Storage System 2019 & 2032

- Table 3: North America Next Generation Storage Market Revenue Million Forecast, by Storage Architecture 2019 & 2032

- Table 4: North America Next Generation Storage Market Revenue Million Forecast, by End-User Industry 2019 & 2032

- Table 5: North America Next Generation Storage Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Next Generation Storage Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Next Generation Storage Market Revenue Million Forecast, by Storage System 2019 & 2032

- Table 12: North America Next Generation Storage Market Revenue Million Forecast, by Storage Architecture 2019 & 2032

- Table 13: North America Next Generation Storage Market Revenue Million Forecast, by End-User Industry 2019 & 2032

- Table 14: North America Next Generation Storage Market Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Next Generation Storage Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Next Generation Storage Market?

The projected CAGR is approximately 6.29%.

2. Which companies are prominent players in the North America Next Generation Storage Market?

Key companies in the market include IBM Corporation, Fujitsu Ltd, Toshiba Corp, Hewlett Packard Enterprise Company, Scality Inc, Hitachi Ltd, Netgear Inc , Dell Inc, DataDirect Networks, NetApp Inc, Pure Storage Inc.

3. What are the main segments of the North America Next Generation Storage Market?

The market segments include Storage System, Storage Architecture, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.59 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Volume of Digital Data; Rising Adoption of Solid-state Devices; Increasing Proliferation of Smartphones. Laptops. and Tablets.

6. What are the notable trends driving market growth?

Increasing Proliferation of Smartphones. connected devices and electronic devices will drive the market..

7. Are there any restraints impacting market growth?

Lack of Data Security in Cloud- and Server-based Services.

8. Can you provide examples of recent developments in the market?

July 2022: QNAP Systems, Inc., a computing, networking, and storage solutions provider, announced the launch of an industrial 10GbE NAS - TS-i410X. It is built with a fanless design, a rock-solid chassis, multiple flexible installation options, and a wide-range temperature and DC power support. The solution is suited for factories and warehouses, semi-outdoor environments, and transportation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Next Generation Storage Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Next Generation Storage Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Next Generation Storage Market?

To stay informed about further developments, trends, and reports in the North America Next Generation Storage Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence