Key Insights

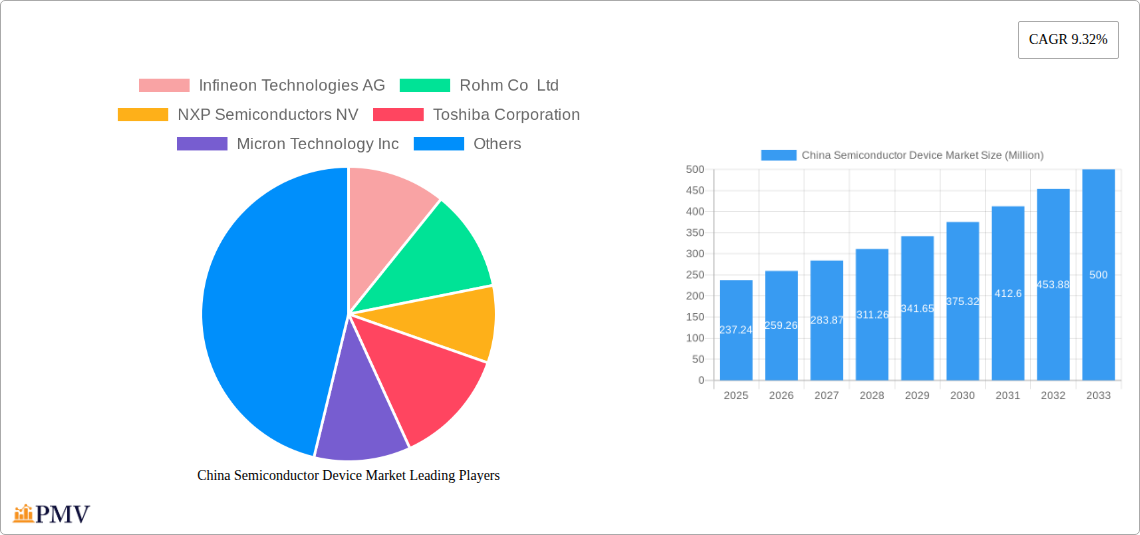

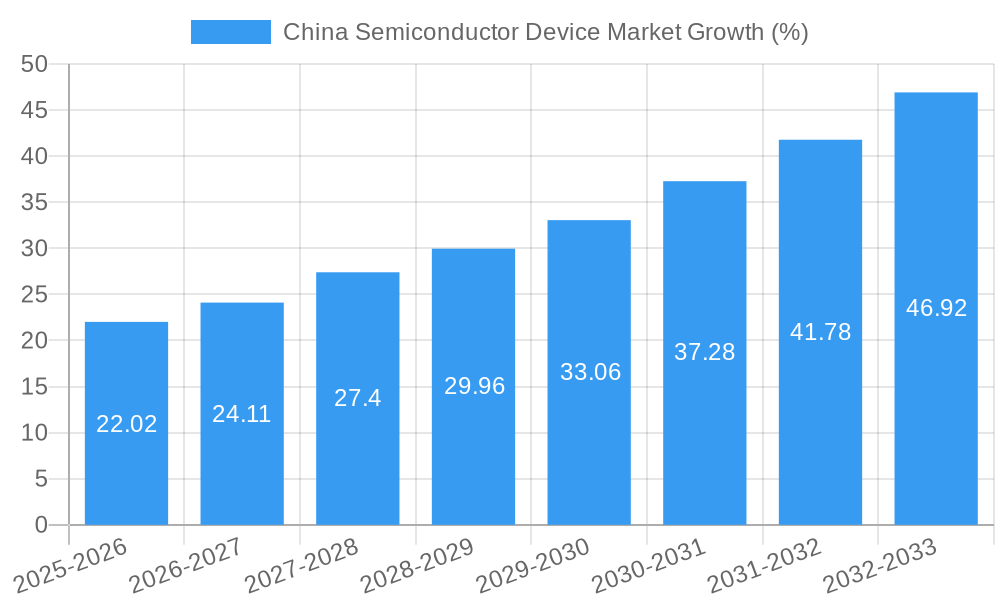

The China semiconductor device market, valued at $237.24 million in 2025, is projected to experience robust growth, driven by the country's expanding technological advancements and increasing domestic demand across various sectors. A Compound Annual Growth Rate (CAGR) of 9.32% from 2025 to 2033 indicates a significant market expansion, reaching an estimated value exceeding $500 million by 2033. Key growth drivers include the surging adoption of semiconductors in automotive electronics, particularly electric vehicles and advanced driver-assistance systems (ADAS), the rapid expansion of 5G and related communication infrastructure, and the increasing integration of semiconductors into consumer electronics like smartphones and wearables. Furthermore, the Chinese government's continued investment in domestic semiconductor manufacturing capabilities, through initiatives aimed at achieving technological self-reliance, is expected to further fuel market growth. While potential supply chain disruptions and global geopolitical uncertainties pose some challenges, the overall market outlook remains positive, fueled by innovation and strong government support.

The market segmentation reveals significant opportunities within specific areas. Integrated circuits, microprocessors (MPUs), and microcontrollers (MCUs) are expected to be the largest segments, driven by their widespread application across electronics. The automotive and communication sectors are projected to be the major end-user verticals, contributing significantly to the overall market value. Leading players like Infineon Technologies AG, Rohm Co Ltd, and NXP Semiconductors NV are well-positioned to capitalize on this growth, although intense competition among domestic and international companies is anticipated. The substantial market size and high CAGR indicate significant investment potential for both established players and new entrants seeking to capitalize on the growing demand for semiconductor devices in China. Analyzing specific regional variations within China itself, and identifying emerging niche applications within the broader segments, will be critical for future market success.

China Semiconductor Device Market: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the China semiconductor device market, covering the period from 2019 to 2033. It offers detailed insights into market size, growth drivers, challenges, competitive landscape, and future outlook, equipping stakeholders with actionable intelligence to navigate this dynamic industry. The report meticulously examines various segments, including device types and end-user verticals, providing granular data for informed decision-making. With a base year of 2025 and a forecast period extending to 2033, this report is an indispensable resource for businesses operating within or seeking to enter the burgeoning Chinese semiconductor market. The total market size is predicted to reach xx Million by 2033.

China Semiconductor Device Market Market Structure & Competitive Dynamics

The China semiconductor device market exhibits a complex interplay of factors shaping its structure and competitive dynamics. Market concentration is moderate, with a few dominant players and numerous smaller, specialized firms. The industry is characterized by a vibrant innovation ecosystem, fueled by government initiatives promoting technological advancements and domestic chip production. However, the regulatory framework remains a significant influence, with policies aimed at both encouraging domestic growth and managing foreign participation. The presence of substitute technologies, particularly in specific applications, also impacts market share. End-user trends, particularly the rapid growth of sectors like automotive and 5G communication, significantly influence demand. Mergers and acquisitions (M&A) are frequent, with deal values varying considerably based on the target company's size and technology portfolio.

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2025, indicating a moderately concentrated market.

- Innovation Ecosystems: Government initiatives like the "Made in China 2025" program are driving significant investment in R&D and innovation.

- Regulatory Frameworks: Stringent regulations regarding data security and intellectual property are impacting market strategies.

- Product Substitutes: The emergence of alternative technologies, such as photonics, poses a competitive threat to certain semiconductor segments.

- M&A Activity: Significant M&A activity was observed between 2019 and 2024, with total deal values exceeding xx Million.

China Semiconductor Device Market Industry Trends & Insights

The China semiconductor device market is experiencing robust growth, driven by several key trends. Technological advancements, particularly in areas like artificial intelligence (AI), 5G, and the Internet of Things (IoT), are creating significant demand for advanced semiconductor devices. Consumer preferences are shifting towards higher-performance, energy-efficient devices, pushing innovation in semiconductor technology. The market is also witnessing intense competitive pressure, with both domestic and international players vying for market share. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is projected to be xx%, driven primarily by increased adoption in the automotive and communication sectors. Market penetration of advanced semiconductor technologies, such as advanced node fabrication, is expected to increase by xx% by 2033.

Dominant Markets & Segments in China Semiconductor Device Market

The Chinese semiconductor device market shows significant regional variations in growth and adoption. Integrated Circuits (ICs) represent the largest segment by device type, driven by strong demand from the electronics and communication sectors. The Automotive sector is the fastest-growing end-user vertical, fueled by the increasing adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs).

- Leading Regions/Segments: The eastern coastal regions of China (e.g., Guangdong, Jiangsu, Shanghai) dominate the market due to advanced infrastructure and established electronics manufacturing hubs.

- Key Drivers (Automotive):

- Rapid expansion of the electric vehicle market.

- Government support for the development of the automotive industry.

- Increasing demand for advanced driver-assistance systems (ADAS).

- Key Drivers (Communication):

- Rapid 5G network rollout.

- Growth of the IoT market.

- Increasing demand for high-speed data transmission.

Detailed analysis reveals the dominance of Integrated Circuits (ICs) within the device type segment, largely driven by the robust growth in consumer electronics and the burgeoning 5G infrastructure development. Similarly, the Automotive end-user vertical exhibits the highest growth trajectory, propelled by China's ambitious electric vehicle (EV) and autonomous driving initiatives.

China Semiconductor Device Market Product Innovations

Significant advancements in semiconductor technology are shaping the market landscape. The introduction of advanced process nodes (e.g., 22nm and below) is enabling the development of more powerful and energy-efficient chips. New materials and packaging technologies are improving device performance and reliability. These innovations are leading to the development of new applications in various sectors, fostering intense competition based on technological differentiation and market fit.

Report Segmentation & Scope

This report segments the China semiconductor device market in two primary ways:

- By Device Type: Discrete Semiconductors, Optoelectronics, Sensors, Integrated Circuits (further divided into Microprocessors (MPU), Microcontrollers (MCU), and Digital Signal Processors). Each segment's growth projection, market size, and competitive dynamics are analyzed in detail, showing significant growth in ICs particularly in Microcontrollers due to IoT and automotive applications.

- By End-User Vertical: Automotive, Communication (Wired and Wireless), Consumer Electronics, Industrial, Computing/Data Storage, and Other End-User Verticals. Market analysis for each segment reveals the Automotive sector's significant growth, exceeding xx Million by 2033, due to the rapid EV adoption and ADAS implementation.

Key Drivers of China Semiconductor Device Market Growth

The growth of the China semiconductor device market is propelled by a combination of factors. Technological advancements, particularly in AI, 5G, and IoT, are creating immense demand for sophisticated semiconductor devices. Government policies supporting domestic chip manufacturing and technological self-reliance are stimulating investments and innovation. Favorable economic conditions and increasing consumer spending are further fueling market expansion.

Challenges in the China Semiconductor Device Market Sector

The China semiconductor device market faces several challenges. Supply chain disruptions, particularly the impact of geopolitical uncertainties and trade tensions, can affect the availability of raw materials and components. Intense competition from both domestic and international players necessitates continuous innovation and cost optimization. Regulatory hurdles and intellectual property concerns also pose significant challenges for market participants. The combined impact of these factors is estimated to cause an annual loss of xx Million to the market growth between 2025 and 2030.

Leading Players in the China Semiconductor Device Market Market

- Infineon Technologies AG

- Rohm Co Ltd

- NXP Semiconductors NV

- Toshiba Corporation

- Micron Technology Inc

- Kyocera Corporation

- Xilinx Inc

- Texas Instruments Inc

- Samsung Electronics Co Ltd

- Broadcom Inc

- STMicroelectronics NV

- Qualcomm Incorporated

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- SK Hynix Inc

- Advanced Semiconductor Engineering Inc

- Nvidia Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- Intel Corporation

- Fujitsu Semiconductor Ltd

Key Developments in China Semiconductor Device Market Sector

- April 2023: Renesas Electronics Corp. launched its first 22nm microcontroller (MCU), boosting performance while reducing power consumption. This highlights advancements in process technology and integration capabilities, impacting the MCU segment significantly.

- January 2022: WeEn Semiconductors' launch of its Global Operation Center in Shanghai signifies a renewed focus on global expansion, enhancing its competitiveness in the Chinese market.

Strategic China Semiconductor Device Market Market Outlook

The China semiconductor device market presents significant growth potential, driven by continuous technological innovation, supportive government policies, and rising domestic demand. Strategic opportunities exist for companies focused on developing advanced semiconductor technologies tailored to specific market needs, particularly in the automotive, 5G, and IoT sectors. Collaborations and strategic partnerships will be crucial for navigating the complex regulatory landscape and ensuring access to resources and expertise. The market's future is marked by expansion in both scale and technological sophistication.

China Semiconductor Device Market Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

-

1.4.4. Micro

- 1.4.4.1. Microprocessors (MPU)

- 1.4.4.2. Microcontrollers (MCU)

- 1.4.4.3. Digital Signal Processors

-

2. End-User Vertical

- 2.1. Automotive

- 2.2. Communication (Wired and Wireless)

- 2.3. Consumer Electronics

- 2.4. Industrial

- 2.5. Computing/Data Storage

- 2.6. Other End-User Verticals

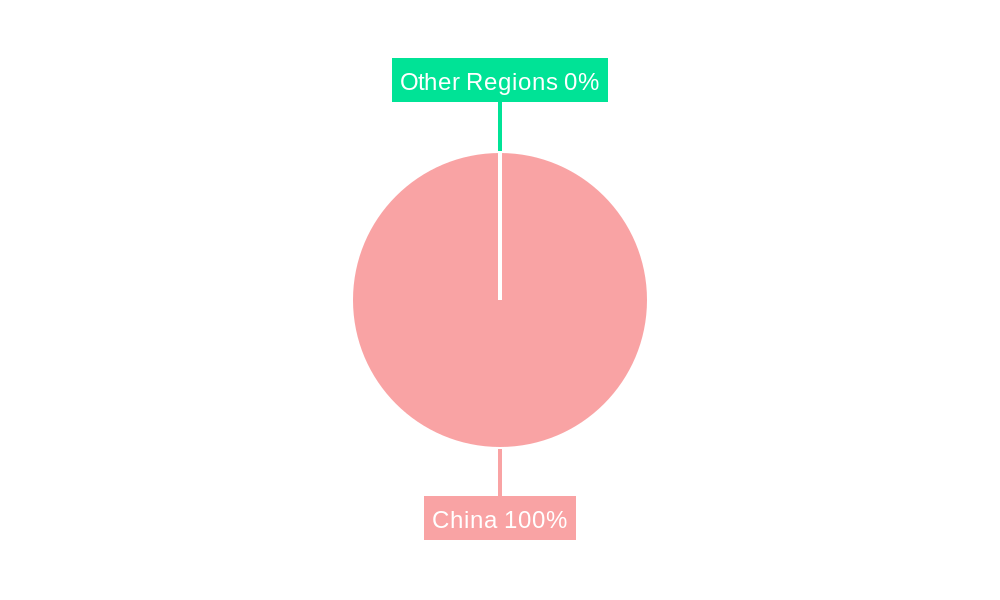

China Semiconductor Device Market Segmentation By Geography

- 1. China

China Semiconductor Device Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 9.32% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Adoption of Technologies like IoT and AI; Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 3.3. Market Restrains

- 3.3.1. Supply Chain Disruptions Resulting in Semiconductor Chip Shortage

- 3.4. Market Trends

- 3.4.1. Automotive Sector is Expected to Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Semiconductor Device Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro

- 5.1.4.4.1. Microprocessors (MPU)

- 5.1.4.4.2. Microcontrollers (MCU)

- 5.1.4.4.3. Digital Signal Processors

- 5.2. Market Analysis, Insights and Forecast - by End-User Vertical

- 5.2.1. Automotive

- 5.2.2. Communication (Wired and Wireless)

- 5.2.3. Consumer Electronics

- 5.2.4. Industrial

- 5.2.5. Computing/Data Storage

- 5.2.6. Other End-User Verticals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Infineon Technologies AG

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Rohm Co Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 NXP Semiconductors NV

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Toshiba Corporation

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Micron Technology Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Kyocera Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Xilinx Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Texas Instruments Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Samsung Electronics Co Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Broadcom Inc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 STMicroelectronics NV

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Qualcomm Incorporated

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 ON Semiconductor Corporatio

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Renesas Electronics Corporation

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 SK Hynix Inc

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Advanced Semiconductor Engineering Inc

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 Nvidia Corporation

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 Intel Corporation

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.20 Fujitsu Semiconductor Ltd

- 6.2.20.1. Overview

- 6.2.20.2. Products

- 6.2.20.3. SWOT Analysis

- 6.2.20.4. Recent Developments

- 6.2.20.5. Financials (Based on Availability)

- 6.2.1 Infineon Technologies AG

List of Figures

- Figure 1: China Semiconductor Device Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Semiconductor Device Market Share (%) by Company 2024

List of Tables

- Table 1: China Semiconductor Device Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Semiconductor Device Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 3: China Semiconductor Device Market Revenue Million Forecast, by End-User Vertical 2019 & 2032

- Table 4: China Semiconductor Device Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: China Semiconductor Device Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China Semiconductor Device Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 7: China Semiconductor Device Market Revenue Million Forecast, by End-User Vertical 2019 & 2032

- Table 8: China Semiconductor Device Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Semiconductor Device Market?

The projected CAGR is approximately 9.32%.

2. Which companies are prominent players in the China Semiconductor Device Market?

Key companies in the market include Infineon Technologies AG, Rohm Co Ltd, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Kyocera Corporation, Xilinx Inc, Texas Instruments Inc, Samsung Electronics Co Ltd, Broadcom Inc, STMicroelectronics NV, Qualcomm Incorporated, ON Semiconductor Corporatio, Renesas Electronics Corporation, SK Hynix Inc, Advanced Semiconductor Engineering Inc, Nvidia Corporation, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Intel Corporation, Fujitsu Semiconductor Ltd.

3. What are the main segments of the China Semiconductor Device Market?

The market segments include Device Type, End-User Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 237.24 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Technologies like IoT and AI; Increased Deployment of 5G and Rising Demand for 5G Smartphones.

6. What are the notable trends driving market growth?

Automotive Sector is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Supply Chain Disruptions Resulting in Semiconductor Chip Shortage.

8. Can you provide examples of recent developments in the market?

April 2023: Renesas Electronics Corp. has produced its first microcontroller (MCU) based on advanced 22-nm process technology. By employing state-of-the-art process technology, Renesas provides MCUs with higher performance at lower power consumption based on reduced core voltages. The process technology enables the integration of a feature set that includes functions such as radio frequency (RF). The advanced process node also uses a smaller die area, resulting in more minor chips with improved peripheral and memory integration.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Semiconductor Device Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Semiconductor Device Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Semiconductor Device Market?

To stay informed about further developments, trends, and reports in the China Semiconductor Device Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence