Key Insights

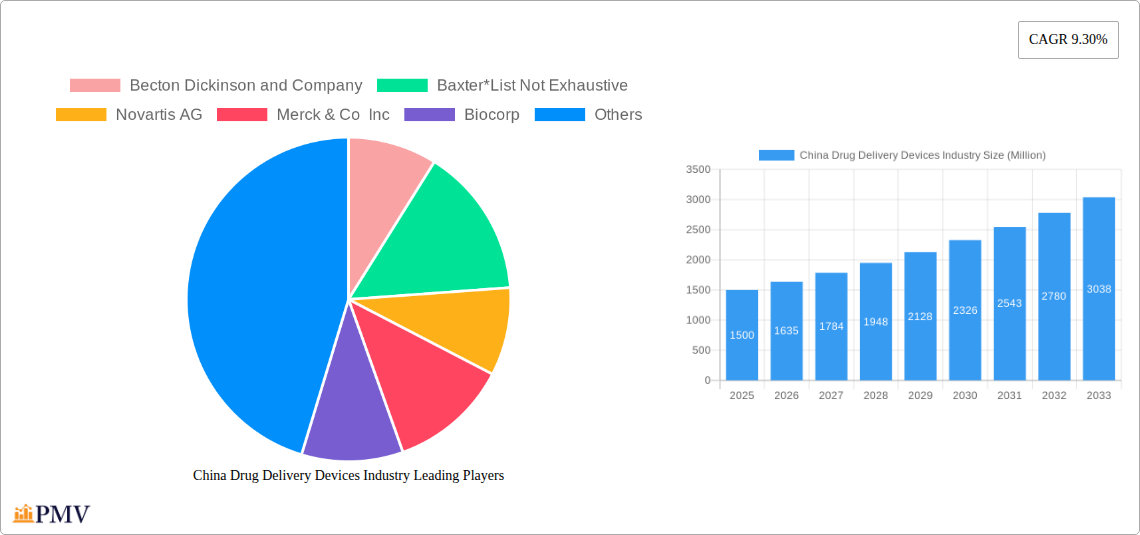

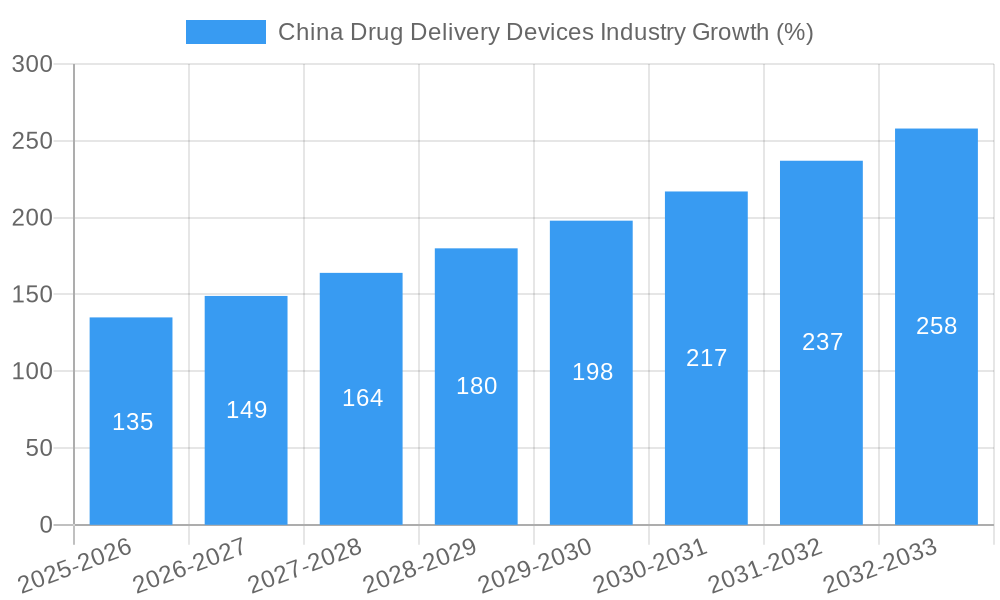

The China drug delivery devices market is experiencing robust growth, projected to reach a substantial size by 2033, driven by a confluence of factors. The market's Compound Annual Growth Rate (CAGR) of 9.30% from 2019 to 2024 indicates a strong upward trajectory. This expansion is fueled by several key drivers: a rising prevalence of chronic diseases like cardiovascular conditions, oncology, and autoimmune disorders, necessitating sophisticated drug delivery solutions; increasing demand for convenient and patient-friendly self-injectable devices; and growing investments in healthcare infrastructure and technological advancements within the pharmaceutical and medical device sectors in China. The market is segmented by sales channel (hospitals, pharmacies, others), device type (nasal, implantable, injectable, self-injectable including pre-filled syringes and auto-injectors, and others), and therapeutic application (cardiovascular, oncology, autoimmune disorders, pulmonary diseases, and others). The dominance of specific segments, like self-injectable devices within the broader injectable category, reflects changing patient preferences and the rising adoption of home healthcare. Leading players like Becton Dickinson, Baxter, Novartis, Merck, and others are actively shaping market dynamics through innovation, strategic partnerships, and product launches. Competition is fierce, driving innovation and efficiency.

However, challenges persist. Regulatory hurdles and stringent approval processes for new devices could pose a constraint on growth. Furthermore, pricing pressures and the need for cost-effective solutions may affect profitability for some market participants. Nevertheless, the long-term outlook remains positive, fueled by China's expanding healthcare ecosystem and its increasing focus on improving patient outcomes. This positive outlook is further strengthened by continuous technological advancements leading to more efficient and precise drug delivery systems, thereby improving treatment efficacy and patient adherence. The focus on personalized medicine is also expected to further propel the market growth by necessitating specific device types catering to individualized patient needs. The considerable market size and high CAGR suggest significant investment opportunities for companies operating in this dynamic sector.

China Drug Delivery Devices Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the China drug delivery devices market, offering valuable insights for stakeholders across the pharmaceutical and medical device industries. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report meticulously examines market size, growth drivers, competitive landscape, and future trends. The report covers a market valued at xx Million in 2025 and projects significant growth to xx Million by 2033, representing a robust CAGR.

China Drug Delivery Devices Industry Market Structure & Competitive Dynamics

The China drug delivery devices market exhibits a moderately concentrated structure, with both multinational corporations and domestic players vying for market share. Key players include Becton Dickinson and Company, Baxter, Novartis AG, Merck & Co Inc, Biocorp, Teva Pharmaceutical Industries Ltd, GSK plc, Teleflex Medical, Gerresheimer AG, and Pfizer Inc. However, the market also features numerous smaller, specialized companies focusing on niche therapeutic applications or innovative delivery technologies. The market share of the top 5 players is estimated at xx%, indicating room for both expansion by existing players and entry by new ones. Innovation ecosystems are evolving rapidly, driven by government initiatives promoting R&D and collaborations between academia, industry, and research institutions. The regulatory landscape is characterized by the stringent standards set by the National Medical Products Administration (NMPA), impacting product approvals and market entry strategies. Substitutes for drug delivery devices are limited, with the choice often dictated by the specific drug and therapeutic application. End-user trends favor minimally invasive, patient-friendly devices, impacting product development and marketing strategies. M&A activities have been relatively moderate in recent years, with deal values averaging xx Million per transaction, primarily driven by consolidation within specific segments, such as self-injectable devices.

China Drug Delivery Devices Industry Industry Trends & Insights

The China drug delivery devices market is witnessing substantial growth, driven by factors such as rising prevalence of chronic diseases, increasing demand for personalized medicine, and supportive government policies aimed at improving healthcare infrastructure. Technological advancements are significantly shaping market dynamics, with innovations in areas like smart inhalers, wearable drug delivery systems, and microneedle patches gaining traction. The market exhibits strong preference for user-friendly devices with improved efficacy and safety. Consumer preferences are increasingly influenced by factors such as convenience, ease of use, and reduced side effects. The rise of e-commerce and online pharmacies is also creating new sales channels and influencing consumer behavior. Competitive dynamics are characterized by both intense rivalry among established players and the emergence of innovative startups. This dynamic landscape drives continuous product development and fosters innovation in drug delivery technologies. The market penetration rate for advanced drug delivery devices remains relatively low, offering significant growth potential as awareness and affordability improve. The estimated CAGR for the forecast period is xx%.

Dominant Markets & Segments in China Drug Delivery Devices Industry

The China drug delivery devices market demonstrates diverse growth across various segments.

By Sales Channel: Hospitals currently dominate, accounting for xx% of market share, followed by pharmacies (xx%) and other sales channels (xx%). This dominance of hospitals is attributed to the established healthcare infrastructure and significant volume of drug administrations in hospital settings. However, the growth of pharmacies and other sales channels is noteworthy, fueled by rising healthcare expenditure, increasing patient preference for home-based treatments, and expanding private healthcare facilities.

By Device Type: Injectable devices maintain the largest market share (xx%), driven by the high prevalence of injectable medications. Self-injectable devices, such as prefilled syringes and auto-injectors (xx%), are exhibiting strong growth fueled by patient preference for convenience and improved self-management capabilities. Nasal drug delivery devices (xx%) are witnessing notable growth, propelled by the development of novel formulations and increased market acceptance. Implantable devices (xx%) are poised for significant growth in the forecast period.

By Therapeutic Application: Oncology (xx%) and cardiovascular (xx%) therapeutic applications represent the largest segments, reflecting the high prevalence of these diseases in China. Growth in other therapeutic areas such as autoimmune disorders and pulmonary diseases is also significant. This high demand is driven by growing awareness, improved diagnosis rates, and advancements in treatment options. Key drivers include favorable government policies incentivizing healthcare investment and improvement of medical infrastructure, particularly in underserved areas.

China Drug Delivery Devices Industry Product Innovations

Recent innovations in China's drug delivery devices market encompass advanced formulations for enhanced bioavailability, smart inhalers with digital monitoring capabilities, and the development of microneedle patches for minimally invasive drug administration. These innovations address unmet medical needs and enhance patient compliance and therapeutic efficacy. Technological trends favor miniaturization, personalized drug delivery, and connected devices enabling remote monitoring and data analysis. The market fit for these innovations is strong, driven by the increasing prevalence of chronic diseases, the rising demand for personalized medicine, and growing consumer preference for convenient and user-friendly devices.

Report Segmentation & Scope

This report segments the China drug delivery devices market comprehensively across various parameters.

By Sales Channel: Hospitals, Pharmacies, Other Sales Channels. Growth is projected to be highest in the other sales channels segment.

By Device Type: Nasal, Injectable, Implantable, Self-injectable (Prefilled Syringes, Auto-injectors, Other), Other Device Types. The self-injectable segment demonstrates the fastest growth.

By Therapeutic Application: Cardiovascular, Oncology, Autoimmune Disorders, Pulmonary Diseases, Other Therapeutic Applications. Oncology and Cardiovascular applications dominate market share. Each segment’s growth trajectory reflects the prevalence of the specific disease and the innovation pace within its associated drug delivery technologies. The competitive landscape varies across segments, with some dominated by a few major players while others showcase greater fragmentation.

Key Drivers of China Drug Delivery Devices Industry Growth

Growth in the China drug delivery devices market is driven by several factors: the rising prevalence of chronic diseases necessitates innovative drug delivery solutions; advancements in drug delivery technologies offer enhanced efficacy and patient compliance; government initiatives promoting healthcare infrastructure development and access to advanced therapies boost market expansion; increasing disposable incomes and rising healthcare expenditure fuel greater demand for sophisticated drug delivery systems.

Challenges in the China Drug Delivery Devices Industry Sector

The China drug delivery devices market faces challenges such as stringent regulatory requirements which increase approval times and costs; supply chain complexities which can disrupt product availability; intense competition from both domestic and international players; the pricing pressure from healthcare payers affects profitability. These challenges impact market expansion, particularly for smaller companies and innovative technologies.

Leading Players in the China Drug Delivery Devices Industry Market

- Becton Dickinson and Company

- Baxter

- Novartis AG

- Merck & Co Inc

- Biocorp

- Teva Pharmaceutical Industries Ltd

- GSK plc

- Teleflex Medical

- Gerresheimer AG

- Pfizer Inc

Key Developments in China Drug Delivery Devices Industry Sector

June 2022: EyePoint Pharmaceuticals, Inc. and OcuMension Therapeutics received NMPA approval for YUTIQ, expanding treatment options for chronic uveitis. This approval significantly impacts the implantable devices segment within the ophthalmology therapeutic area.

November 2022: DKSH and Nuance Pharma's agreement to market a nasal spray device in Hong Kong and Macau marks a commercial milestone for Nuance Pharma and signifies growth in the nasal drug delivery segment.

Strategic China Drug Delivery Devices Industry Market Outlook

The China drug delivery devices market is poised for substantial growth, driven by continued technological advancements, increasing healthcare expenditure, and supportive government policies. Strategic opportunities lie in focusing on innovative devices, tailoring offerings to specific therapeutic applications, and expanding distribution networks. The market's future potential is considerable, particularly in areas like personalized medicine and minimally invasive therapies, creating significant opportunities for existing players and new entrants alike.

China Drug Delivery Devices Industry Segmentation

-

1. Device Type

-

1.1. Nasal

- 1.1.1. Inhalers

- 1.1.2. Other Device Types

- 1.2. Implantable

-

1.3. Injectable

- 1.3.1. Conventional Drug Delivery Devices

-

1.3.2. Self-injectable Drug Delivery Devices

- 1.3.2.1. Prefilled Syringes

- 1.3.2.2. Auto-Injectors

- 1.3.2.3. Other Self-injectable Drug Delivery Devices

-

1.1. Nasal

-

2. Therapeutic Application

- 2.1. Cardiovascular

- 2.2. Oncology

- 2.3. Autoimmune Disorder

- 2.4. Pulmonary Disease

- 2.5. Other Therapeutic Applications

-

3. Sales Channel

- 3.1. Hospitals

- 3.2. Pharmacy

- 3.3. Other Sales Channels

China Drug Delivery Devices Industry Segmentation By Geography

- 1. China

China Drug Delivery Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 9.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Prevalence of Chronic Diseases; Advancement in Technology

- 3.3. Market Restrains

- 3.3.1. The High Cost of Development

- 3.4. Market Trends

- 3.4.1. Auto-Injectors Segment is Expected to Hold the Significant Market Share During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Drug Delivery Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Nasal

- 5.1.1.1. Inhalers

- 5.1.1.2. Other Device Types

- 5.1.2. Implantable

- 5.1.3. Injectable

- 5.1.3.1. Conventional Drug Delivery Devices

- 5.1.3.2. Self-injectable Drug Delivery Devices

- 5.1.3.2.1. Prefilled Syringes

- 5.1.3.2.2. Auto-Injectors

- 5.1.3.2.3. Other Self-injectable Drug Delivery Devices

- 5.1.1. Nasal

- 5.2. Market Analysis, Insights and Forecast - by Therapeutic Application

- 5.2.1. Cardiovascular

- 5.2.2. Oncology

- 5.2.3. Autoimmune Disorder

- 5.2.4. Pulmonary Disease

- 5.2.5. Other Therapeutic Applications

- 5.3. Market Analysis, Insights and Forecast - by Sales Channel

- 5.3.1. Hospitals

- 5.3.2. Pharmacy

- 5.3.3. Other Sales Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Becton Dickinson and Company

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Baxter*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Novartis AG

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Merck & Co Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Biocorp

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Teva Pharmaceutical Industries Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 GSK plc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Teleflex Medical

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Gerresheimer AG

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Pfizer Inc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Becton Dickinson and Company

List of Figures

- Figure 1: China Drug Delivery Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Drug Delivery Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: China Drug Delivery Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Drug Delivery Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 3: China Drug Delivery Devices Industry Revenue Million Forecast, by Therapeutic Application 2019 & 2032

- Table 4: China Drug Delivery Devices Industry Revenue Million Forecast, by Sales Channel 2019 & 2032

- Table 5: China Drug Delivery Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: China Drug Delivery Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China Drug Delivery Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 8: China Drug Delivery Devices Industry Revenue Million Forecast, by Therapeutic Application 2019 & 2032

- Table 9: China Drug Delivery Devices Industry Revenue Million Forecast, by Sales Channel 2019 & 2032

- Table 10: China Drug Delivery Devices Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Drug Delivery Devices Industry?

The projected CAGR is approximately 9.30%.

2. Which companies are prominent players in the China Drug Delivery Devices Industry?

Key companies in the market include Becton Dickinson and Company, Baxter*List Not Exhaustive, Novartis AG, Merck & Co Inc, Biocorp, Teva Pharmaceutical Industries Ltd, GSK plc, Teleflex Medical, Gerresheimer AG, Pfizer Inc.

3. What are the main segments of the China Drug Delivery Devices Industry?

The market segments include Device Type, Therapeutic Application, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Chronic Diseases; Advancement in Technology.

6. What are the notable trends driving market growth?

Auto-Injectors Segment is Expected to Hold the Significant Market Share During the Forecast Period.

7. Are there any restraints impacting market growth?

The High Cost of Development.

8. Can you provide examples of recent developments in the market?

November 2022: DKSH and Nuance Pharma agreed to market the nasal spray device in Hong Kong and Macau. Based in Shanghai, China, Nuance Pharma reached a major commercial milestone with an agreement to bring a novel nasal spray to market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Drug Delivery Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Drug Delivery Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Drug Delivery Devices Industry?

To stay informed about further developments, trends, and reports in the China Drug Delivery Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence