Key Insights

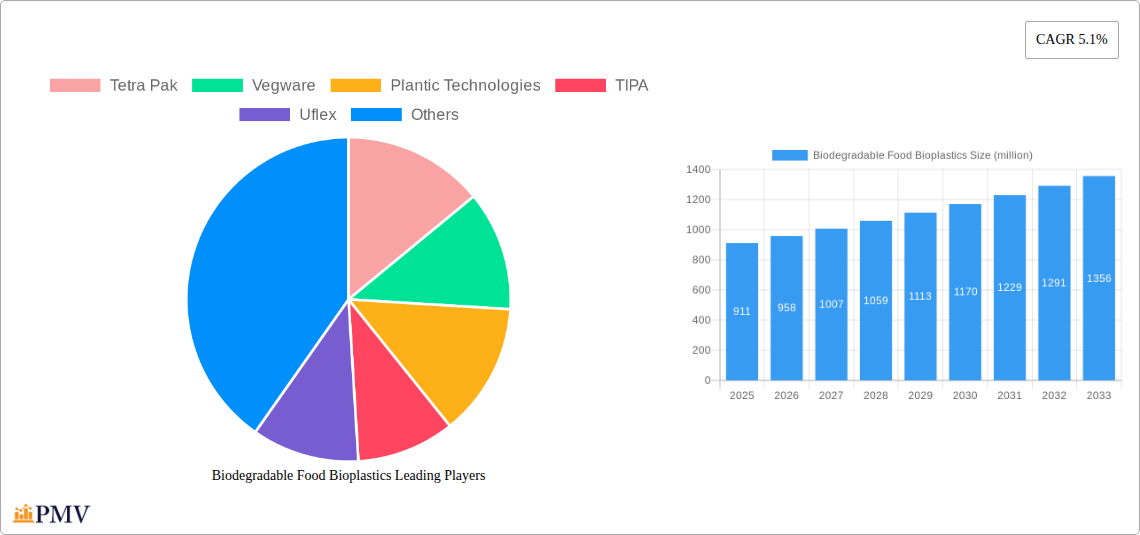

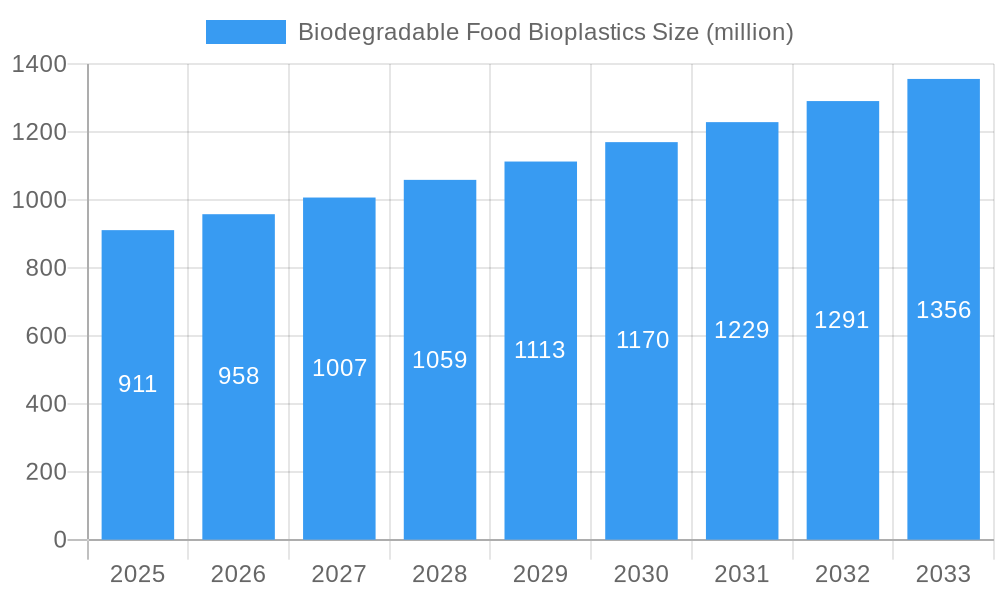

The global market for Biodegradable Food Bioplastics is poised for robust expansion, projected to reach an estimated \$911 million in 2025. Driven by a substantial Compound Annual Growth Rate (CAGR) of 5.1%, this market is set to witness sustained growth throughout the forecast period of 2025-2033. A primary catalyst for this upward trajectory is the increasing consumer and regulatory demand for sustainable packaging solutions, particularly within the food industry. Growing environmental consciousness, coupled with stringent government regulations aimed at curbing plastic pollution, is compelling food manufacturers to actively seek and adopt biodegradable alternatives. This shift is further amplified by advancements in bioplastic technologies, leading to improved performance characteristics, cost-effectiveness, and a wider array of applications, thereby addressing traditional concerns about durability and barrier properties. The industry is witnessing a pronounced trend towards innovation in material science, focusing on enhancing biodegradability across various environmental conditions, from photodegradation to more comprehensive biodegradation and photo-biological degradation processes.

Biodegradable Food Bioplastics Market Size (In Million)

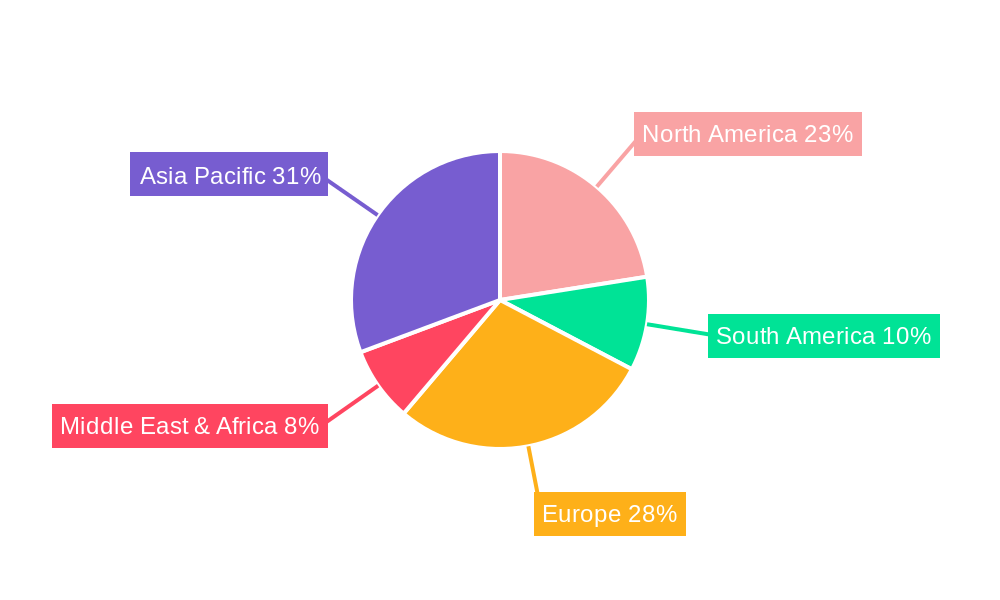

The market's growth is underpinned by significant applications in flexible packaging, stand-up pouches, trays, containers, and bottles, all of which are critical components of the food supply chain. The versatility and adaptability of biodegradable bioplastics are enabling their integration into a broad spectrum of food products, from fresh produce to processed goods. While the market exhibits strong growth potential, certain restraints, such as the initial higher cost of production compared to conventional plastics and the need for specialized composting infrastructure, remain points of consideration. However, ongoing research and development, coupled with economies of scale as adoption increases, are expected to mitigate these challenges. Leading companies like Amcor, Mondi Group, Tetra Pak, and DuPont are heavily investing in R&D and expanding their product portfolios to capture market share, further accelerating the adoption of biodegradable food bioplastics globally. Asia Pacific, particularly China and India, is emerging as a significant growth region due to rapid industrialization and increasing environmental awareness.

Biodegradable Food Bioplastics Company Market Share

Here is the SEO-optimized, detailed report description for Biodegradable Food Bioplastics, crafted without placeholders and ready for immediate use.

Biodegradable Food Bioplastics Market Structure & Competitive Dynamics

The global biodegradable food bioplastics market exhibits a moderately concentrated structure, with key players such as Tetra Pak, Vegware, Plantic Technologies, TIPA, Uflex, DuPont, Innovia Films, Huhtamaki Group, Amcor, and Mondi Group holding significant market shares, estimated to be over 60% combined. Innovation ecosystems are thriving, driven by increasing R&D investments exceeding $500 million annually, focusing on developing novel biopolymer formulations and enhanced degradation properties. Regulatory frameworks are evolving globally, with stringent mandates for sustainable packaging and waste reduction creating both opportunities and challenges. Product substitutes, primarily conventional petroleum-based plastics and traditional paper packaging, still pose competition, but the superior environmental profile of bioplastics is gaining traction. End-user trends demonstrate a clear shift towards eco-friendly solutions, with food and beverage manufacturers actively seeking biodegradable alternatives to meet consumer demand and corporate sustainability goals. Merger and acquisition (M&A) activities are on the rise, with deal values estimated to reach over $1.5 billion in the historical period (2019-2024) as larger companies seek to consolidate their market position and acquire innovative technologies.

Biodegradable Food Bioplastics Industry Trends & Insights

The biodegradable food bioplastics industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 9.5% during the forecast period (2025–2033). This surge is propelled by a confluence of compelling market growth drivers. Growing environmental consciousness among consumers worldwide is a paramount factor, compelling brands to adopt sustainable packaging solutions. Government initiatives and stringent regulations promoting the reduction of single-use plastics and encouraging the adoption of eco-friendly materials are also significantly influencing market dynamics. The technological disruption in biopolymer synthesis and processing is leading to improved performance characteristics, such as enhanced barrier properties, durability, and heat resistance, making biodegradable bioplastics viable for a wider range of food applications. For instance, advancements in PLA (Polylactic Acid) and PHA (Polyhydroxyalkanoates) technologies have unlocked new possibilities. Consumer preferences are clearly leaning towards products with a minimal environmental footprint, driving demand for packaging that is either compostable or biodegradable. Major food manufacturers are actively investing in research and development, seeking innovative bioplastic solutions that align with their sustainability commitments, thus increasing the market penetration of these materials. The market penetration of biodegradable food bioplastics is estimated to reach 25% by the end of the forecast period. Furthermore, the development of bio-based materials derived from renewable resources like corn starch, sugarcane, and potato starch is reducing reliance on fossil fuels. Companies are also exploring innovative bio-photodegradable and bio-compostable materials, further diversifying the product landscape and offering tailored solutions for specific food preservation needs. The increasing focus on circular economy principles is also accelerating the adoption of biodegradable bioplastics, as they can be integrated into biological recycling streams. The competitive landscape is intensifying, with established packaging giants and emerging bioplastic innovators vying for market share. Strategic partnerships and collaborations are becoming common, fostering innovation and accelerating market entry for new products.

Dominant Markets & Segments in Biodegradable Food Bioplastics

The biodegradable food bioplastics market is witnessing significant dominance in specific regions and segments, driven by a combination of economic policies, robust infrastructure, and consumer demand. Europe currently holds a leading position, largely due to its proactive environmental policies, ambitious waste management targets, and strong consumer awareness regarding sustainability. Countries like Germany, France, and the UK are at the forefront of adopting biodegradable packaging solutions. In terms of application, Flexible Packaging represents the largest and fastest-growing segment, projected to account for over 40% of the market share by 2033. This dominance is attributed to its versatility in packaging a wide array of food products, from snacks and confectioneries to dry goods and frozen foods. Within flexible packaging, Stand-up Pouches are experiencing exceptional growth due to their convenience, shelf appeal, and reduced material usage compared to traditional rigid packaging. The Biodegradation type segment is the most prominent, driven by a clear understanding and preference for materials that decompose naturally in existing composting facilities or the environment, with an estimated market share exceeding 55%. Key drivers for this dominance include:

- Government Incentives and Regulations: Supportive policies, such as extended producer responsibility (EPR) schemes and bans on certain single-use plastics, encourage the adoption of biodegradable alternatives.

- Consumer Demand for Sustainable Options: A growing segment of consumers actively seeks out products with eco-friendly packaging, influencing brand choices.

- Technological Advancements in Biodegradable Polymers: Continuous improvements in the performance and cost-effectiveness of biopolymers like PLA and PHA are making them more competitive.

- Focus on Reducing Plastic Waste: The global imperative to mitigate plastic pollution is a significant catalyst for the growth of biodegradable bioplastics.

The Trays and Containers segments also represent substantial market share, particularly for fresh produce, ready-to-eat meals, and dairy products, where barrier properties and food safety are critical. The Photodegradation and Photo-biological Degradation types are emerging segments with growing interest, especially for applications where controlled degradation is desired. The overall market value for biodegradable food bioplastics is estimated to reach over $25 billion by 2033.

Biodegradable Food Bioplastics Product Innovations

Recent product innovations in the biodegradable food bioplastics sector focus on enhancing performance and expanding application versatility. Companies are developing novel formulations that offer improved barrier properties against moisture and oxygen, extending food shelf life. Advancements in PHA-based bioplastics are yielding materials with enhanced flexibility and heat resistance, suitable for hot-fill applications. Furthermore, research into composite bioplastics, blending different biodegradable polymers and natural fibers, is creating materials with superior mechanical strength and biodegradability profiles, offering competitive advantages. These innovations cater to evolving market needs and stringent regulatory requirements, solidifying the position of biodegradable food bioplastics as a viable and attractive alternative to conventional plastics.

Report Segmentation & Scope

This report meticulously segments the biodegradable food bioplastics market to provide a comprehensive analysis. The Application segment is analyzed across Flexible Packaging, Stand-up Pouches, Trays, Containers, Bottles, and Other applications, with Flexible Packaging projected to dominate, reaching a market size of over $10 billion by 2033. The Types segment is divided into Photodegradation, Biodegradation, and Photo-biological Degradation, with Biodegradation expected to hold the largest market share, estimated at over $13 billion by 2033. The scope includes a detailed examination of market dynamics, growth projections, and competitive landscapes within each of these segments, offering granular insights for strategic decision-making.

Key Drivers of Biodegradable Food Bioplastics Growth

Several pivotal factors are propelling the biodegradable food bioplastics market. Primarily, stringent government regulations and ambitious environmental policies worldwide, such as those promoting a circular economy and plastic waste reduction, are creating a favorable regulatory environment. Growing consumer awareness and a strong preference for sustainable products are also significant drivers, compelling food manufacturers to adopt eco-friendly packaging. Technological advancements in biopolymer production, leading to improved material properties and cost competitiveness, are making biodegradable bioplastics a more viable option. Furthermore, the increasing corporate sustainability initiatives and commitments by major food and beverage companies to reduce their environmental footprint are substantial growth accelerators.

Challenges in the Biodegradable Food Bioplastics Sector

Despite its growth potential, the biodegradable food bioplastics sector faces notable challenges. Regulatory hurdles can be complex and vary significantly across regions, impacting market entry and adoption rates. Supply chain complexities, including the availability and cost of raw materials and the need for specialized manufacturing infrastructure, present significant barriers. Competitive pressures from established, lower-cost conventional plastics remain a concern. Furthermore, consumer education regarding proper disposal methods for biodegradable materials is crucial to ensure effective biodegradation and prevent contamination of recycling streams. The initial higher cost of some bioplastics compared to traditional options also remains a constraint.

Leading Players in the Biodegradable Food Bioplastics Market

- Tetra Pak

- Vegware

- Plantic Technologies

- TIPA

- Uflex

- DuPont

- Innovia Films

- Huhtamaki Group

- Amcor

- Mondi Group

- Be Green Packaging

- Biopak

- Biomass Packaging

- Eco-Products

Key Developments in Biodegradable Food Bioplastics Sector

- 2023 Q4: Launch of novel PHA-based films by [Company Name] offering enhanced compostability and flexibility.

- 2023 Q3: Strategic partnership between [Company A] and [Company B] to scale up production of biodegradable food containers.

- 2023 Q2: Introduction of certified compostable stand-up pouches by TIPA for the snack food industry.

- 2022: Huhtamaki Group invests in advanced bioplastic recycling technology to improve end-of-life solutions.

- 2021: Amcor acquires [Company X], strengthening its portfolio of sustainable packaging solutions.

Strategic Biodegradable Food Bioplastics Market Outlook

The strategic outlook for the biodegradable food bioplastics market is exceptionally positive, driven by a confluence of accelerating growth factors. The increasing demand for sustainable packaging solutions, amplified by consumer awareness and stringent environmental regulations, will continue to be the primary growth accelerator. Innovations in material science are leading to enhanced performance and cost-effectiveness, making biodegradable bioplastics more competitive for a wider range of applications, including high-barrier packaging. The growing emphasis on a circular economy and waste reduction will further incentivize the adoption of these eco-friendly materials. Opportunities lie in developing specialized bioplastics for niche food applications, expanding into emerging markets, and fostering collaborations across the value chain to overcome existing challenges and unlock the full potential of this dynamic sector. The market is projected to exceed $30 billion by 2033.

Biodegradable Food Bioplastics Segmentation

-

1. Application

- 1.1. Flexible Packaging

- 1.2. Stand-up Pouches

- 1.3. Trays

- 1.4. Containers

- 1.5. Bottles

- 1.6. Other

-

2. Types

- 2.1. Photodegradation

- 2.2. Biodegradation

- 2.3. Photo-biological Degradation

Biodegradable Food Bioplastics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Biodegradable Food Bioplastics Regional Market Share

Geographic Coverage of Biodegradable Food Bioplastics

Biodegradable Food Bioplastics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Flexible Packaging

- 5.1.2. Stand-up Pouches

- 5.1.3. Trays

- 5.1.4. Containers

- 5.1.5. Bottles

- 5.1.6. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Photodegradation

- 5.2.2. Biodegradation

- 5.2.3. Photo-biological Degradation

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Biodegradable Food Bioplastics Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Flexible Packaging

- 6.1.2. Stand-up Pouches

- 6.1.3. Trays

- 6.1.4. Containers

- 6.1.5. Bottles

- 6.1.6. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Photodegradation

- 6.2.2. Biodegradation

- 6.2.3. Photo-biological Degradation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Biodegradable Food Bioplastics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Flexible Packaging

- 7.1.2. Stand-up Pouches

- 7.1.3. Trays

- 7.1.4. Containers

- 7.1.5. Bottles

- 7.1.6. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Photodegradation

- 7.2.2. Biodegradation

- 7.2.3. Photo-biological Degradation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Biodegradable Food Bioplastics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Flexible Packaging

- 8.1.2. Stand-up Pouches

- 8.1.3. Trays

- 8.1.4. Containers

- 8.1.5. Bottles

- 8.1.6. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Photodegradation

- 8.2.2. Biodegradation

- 8.2.3. Photo-biological Degradation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Biodegradable Food Bioplastics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Flexible Packaging

- 9.1.2. Stand-up Pouches

- 9.1.3. Trays

- 9.1.4. Containers

- 9.1.5. Bottles

- 9.1.6. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Photodegradation

- 9.2.2. Biodegradation

- 9.2.3. Photo-biological Degradation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Biodegradable Food Bioplastics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Flexible Packaging

- 10.1.2. Stand-up Pouches

- 10.1.3. Trays

- 10.1.4. Containers

- 10.1.5. Bottles

- 10.1.6. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Photodegradation

- 10.2.2. Biodegradation

- 10.2.3. Photo-biological Degradation

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Biodegradable Food Bioplastics Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Flexible Packaging

- 11.1.2. Stand-up Pouches

- 11.1.3. Trays

- 11.1.4. Containers

- 11.1.5. Bottles

- 11.1.6. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Photodegradation

- 11.2.2. Biodegradation

- 11.2.3. Photo-biological Degradation

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Tetra Pak

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Vegware

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Plantic Technologies

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 TIPA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Uflex

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 DuPont

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Innovia Films

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Huhtamaki Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Amcor

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mondi Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Be Green Packaging

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Biopak

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Biomass Packaging

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Eco-Products

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Tetra Pak

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Biodegradable Food Bioplastics Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Biodegradable Food Bioplastics Revenue (million), by Application 2025 & 2033

- Figure 3: North America Biodegradable Food Bioplastics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Biodegradable Food Bioplastics Revenue (million), by Types 2025 & 2033

- Figure 5: North America Biodegradable Food Bioplastics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Biodegradable Food Bioplastics Revenue (million), by Country 2025 & 2033

- Figure 7: North America Biodegradable Food Bioplastics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Biodegradable Food Bioplastics Revenue (million), by Application 2025 & 2033

- Figure 9: South America Biodegradable Food Bioplastics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Biodegradable Food Bioplastics Revenue (million), by Types 2025 & 2033

- Figure 11: South America Biodegradable Food Bioplastics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Biodegradable Food Bioplastics Revenue (million), by Country 2025 & 2033

- Figure 13: South America Biodegradable Food Bioplastics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Biodegradable Food Bioplastics Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Biodegradable Food Bioplastics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Biodegradable Food Bioplastics Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Biodegradable Food Bioplastics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Biodegradable Food Bioplastics Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Biodegradable Food Bioplastics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Biodegradable Food Bioplastics Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Biodegradable Food Bioplastics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Biodegradable Food Bioplastics Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Biodegradable Food Bioplastics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Biodegradable Food Bioplastics Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Biodegradable Food Bioplastics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Biodegradable Food Bioplastics Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Biodegradable Food Bioplastics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Biodegradable Food Bioplastics Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Biodegradable Food Bioplastics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Biodegradable Food Bioplastics Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Biodegradable Food Bioplastics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Biodegradable Food Bioplastics Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Biodegradable Food Bioplastics Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Biodegradable Food Bioplastics Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Biodegradable Food Bioplastics Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Biodegradable Food Bioplastics Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Biodegradable Food Bioplastics Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Biodegradable Food Bioplastics Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Biodegradable Food Bioplastics Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Biodegradable Food Bioplastics Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Biodegradable Food Bioplastics Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Biodegradable Food Bioplastics Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Biodegradable Food Bioplastics Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Biodegradable Food Bioplastics Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Biodegradable Food Bioplastics Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Biodegradable Food Bioplastics Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Biodegradable Food Bioplastics Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Biodegradable Food Bioplastics Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Biodegradable Food Bioplastics Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Biodegradable Food Bioplastics Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Biodegradable Food Bioplastics?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Biodegradable Food Bioplastics?

Key companies in the market include Tetra Pak, Vegware, Plantic Technologies, TIPA, Uflex, DuPont, Innovia Films, Huhtamaki Group, Amcor, Mondi Group, Be Green Packaging, Biopak, Biomass Packaging, Eco-Products.

3. What are the main segments of the Biodegradable Food Bioplastics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 911 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Biodegradable Food Bioplastics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Biodegradable Food Bioplastics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Biodegradable Food Bioplastics?

To stay informed about further developments, trends, and reports in the Biodegradable Food Bioplastics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence