Key Insights

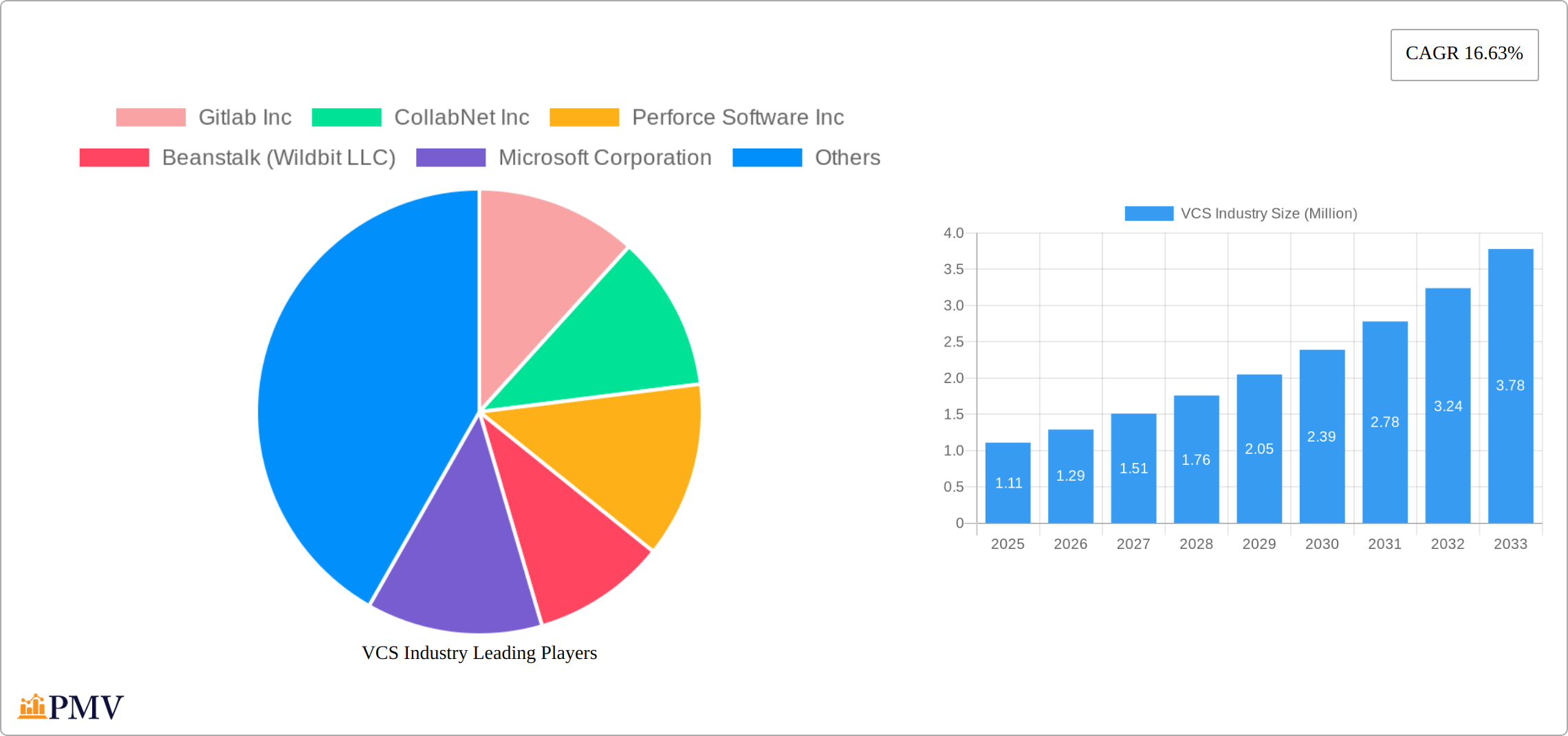

The Version Control System (VCS) market is poised for significant growth, with a projected market size of $1.11 million in 2025 and an impressive Compound Annual Growth Rate (CAGR) of 16.63% from 2025 to 2033. The VCS industry is driven by the increasing need for efficient software development and collaboration tools across various sectors, including IT and Telecom, Retail & E-commerce, Healthcare and Life Sciences, BFSI, and others such as Media and Entertainment, Travel and Tourism, and Educational Institutions. Key players like Gitlab Inc, Microsoft Corporation, and Github Inc are continuously innovating to meet the growing demand for both distributed and centralized VCS solutions. The deployment modes are split between on-premise and on-cloud, catering to diverse organizational needs and preferences.

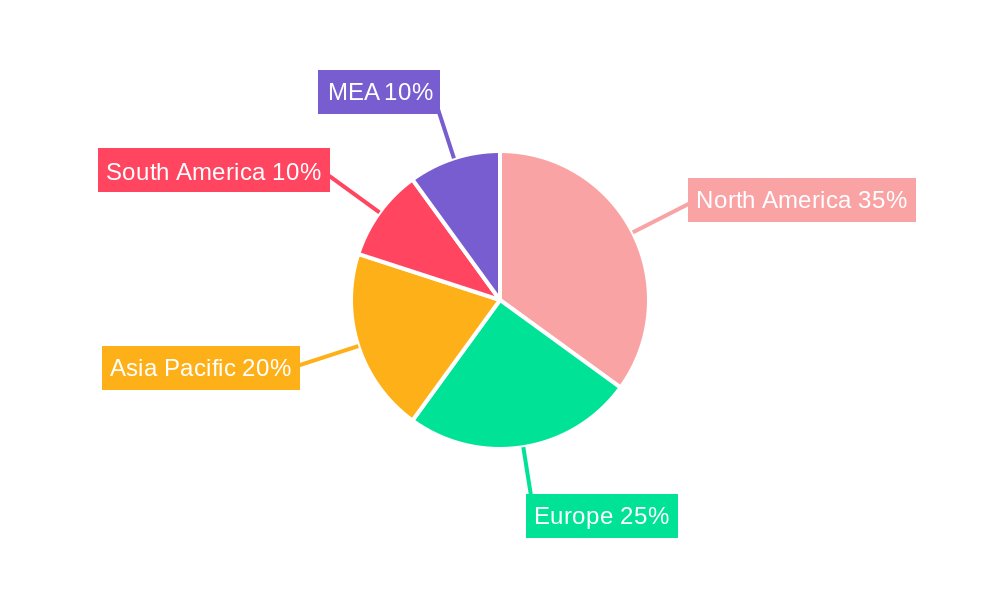

Geographically, North America holds a significant share of the VCS market, with the United States, Canada, and Mexico leading the region. Europe follows closely, with major contributions from Germany, the United Kingdom, and France. The Asia Pacific region is also witnessing rapid growth, driven by technological advancements in countries like China, Japan, and India. The market's expansion is further fueled by trends such as the adoption of DevOps practices, the rise of remote work, and the increasing complexity of software projects, all of which necessitate robust version control systems. However, challenges such as security concerns and the need for skilled professionals may restrain growth, though these are being addressed through continuous improvements and training initiatives.

VCS Industry Market Structure & Competitive Dynamics

The Version Control System (VCS) industry presents a dynamic competitive landscape blending established tech giants and specialized software providers. Market concentration is moderate, with key players like GitLab Inc, Microsoft Corporation, and Amazon Web Services Inc commanding significant market shares—estimated at 25%, 20%, and 15%, respectively. These industry leaders fuel innovation through continuous product improvements and strategic collaborations, fostering a robust ecosystem.

The regulatory environment surrounding VCS is relatively permissive, prioritizing data protection and intellectual property rights. This fosters a climate ripe for innovation, especially in the area of distributed VCS solutions. While manual version tracking and less sophisticated software exist as alternatives, the efficiency and scalability advantages of modern VCS solutions remain unparalleled, ensuring continued market dominance.

Significant end-user demand is evident, particularly within the IT and Telecom sectors, exhibiting a remarkable 10% annual adoption rate increase. The BFSI (Banking, Financial Services, and Insurance) sector closely follows, utilizing VCS for enhanced compliance and comprehensive audit trails. The industry also witnesses frequent mergers and acquisitions, with transactions reaching up to $500 million in 2022, reflecting strategic moves to expand product portfolios and market penetration.

- Market Share Leaders: GitLab Inc, Microsoft Corporation, Amazon Web Services Inc, GitHub, Bitbucket (increasingly significant)

- Regulatory Focus: Data protection, intellectual property rights, data privacy (GDPR, CCPA, etc. – increasingly important)

- End-user Demand Growth: IT and Telecom (10% annually), BFSI, Healthcare, Life Sciences (rapidly growing)

- M&A Deal Values: Up to $500 Million in 2022 (potential for larger deals in the future)

VCS Industry Industry Trends & Insights

The VCS industry demonstrates robust and sustained growth, driven by several key factors. A projected compound annual growth rate (CAGR) of 8% from 2025 to 2033 underscores the increasing reliance on version control across software development and other sectors. Technological advancements, such as the proliferation of cloud-based solutions and the integration of AI and machine learning capabilities, are fundamentally reshaping the market landscape.

User preferences increasingly favor collaborative and flexible VCS options, as demonstrated by the substantial market penetration of distributed VCS systems, now accounting for 60% of the market. Competition intensifies, with companies like Bitbucket and GitHub continuously introducing innovative features to elevate user experience and functionality.

The expanding adoption of VCS across non-traditional sectors, including healthcare and life sciences, is noteworthy, driven by the need for secure and efficient data management in these highly regulated fields. Supportive economic policies promoting digital transformation, coupled with substantial investments in cloud infrastructure, provide a solid foundation for continued VCS expansion.

- CAGR Projection: 8% (2025-2033) – potential for upward revision depending on market dynamics

- Market Penetration: Distributed VCS (60%) – expected to increase further

- Non-traditional Sectors: Healthcare and Life Sciences, Education, Government (emerging markets)

- Supporting Factors: Economic policies, cloud infrastructure, increasing awareness of VCS benefits

Dominant Markets & Segments in VCS Industry

The IT and Telecom sector stands out as the dominant end-user industry for VCS solutions, driven by the sector's inherent need for robust software development and maintenance tools. The demand is further fueled by economic policies promoting digitalization and the availability of advanced IT infrastructure.

- Economic Policies: Government incentives for digital transformation

- Infrastructure: Advanced IT networks and cloud services

In terms of type, distributed VCS has emerged as the leader, offering greater flexibility and scalability compared to centralized systems. This dominance is particularly pronounced in regions with a high concentration of tech companies, such as Silicon Valley.

- Type Leadership: Distributed VCS

- Regional Dominance: Silicon Valley

The deployment mode of VCS solutions also plays a critical role, with on-cloud deployments gaining traction due to their cost-effectiveness and scalability. This trend is especially evident in the BFSI sector, where cloud-based VCS solutions facilitate compliance with regulatory requirements and enhance operational efficiency.

- Deployment Mode: On-Cloud

- Sector-Specific: BFSI

VCS Industry Product Innovations

Recent product innovations in the VCS industry focus on enhancing collaboration and integration capabilities. Microsoft's introduction of Git version control for canvas apps exemplifies this trend, allowing multiple users to work simultaneously without conflicts. Similarly, GitHub's hosting of the WebKit project highlights the shift towards leveraging large developer communities and automation tools. These innovations align well with market demands for more efficient and scalable VCS solutions.

Report Segmentation & Scope

This VCS industry report segments the market comprehensively to provide a detailed analysis. End-user industries include IT and Telecom, Retail & E-commerce, Healthcare and Life Sciences, BFSI, and other sectors such as Media and Entertainment, Travel and Tourism, and Educational Institutions. Growth projections vary across segments, with IT and Telecom leading at a projected CAGR of 10% by 2033.

VCS types are categorized as Distributed VCS and Centralized VCS, with distributed systems anticipated to reach a market size of $2 Billion by 2033. Deployment modes encompass On-Premise and On-Cloud, with the latter projected to maintain market dominance due to inherent scalability and cost-effectiveness advantages.

- End-user Industry: IT and Telecom (CAGR 10%), BFSI, Healthcare and Life Sciences (high growth potential)

- Type: Distributed VCS ($2 Billion by 2033) – potential for exceeding this projection

- Deployment Mode: On-Cloud (dominant) – driven by cloud adoption trends

Key Drivers of VCS Industry Growth

The VCS industry's growth is propelled by a confluence of key drivers. Technological advancements, such as the integration of AI and machine learning into VCS platforms, significantly enhance automation and overall efficiency. Economically, the widespread adoption of digital transformation initiatives across diverse industries fuels the demand for robust version control solutions. Furthermore, regulatory factors, such as stringent data protection laws, necessitate secure and auditable VCS systems, driving further adoption.

- Technological: AI and machine learning integration, improved user interfaces, enhanced security features

- Economic: Digital transformation initiatives, increasing software development complexity, cost optimization through efficiency gains

- Regulatory: Data protection requirements (GDPR, CCPA, etc.), compliance mandates, industry-specific regulations

Challenges in the VCS Industry Sector

The VCS industry faces several challenges that could impede growth. Regulatory hurdles, particularly around data privacy, can complicate VCS deployment in sensitive sectors like healthcare. Supply chain issues, such as software licensing and distribution, can delay product rollouts. Competitive pressures are intense, with new entrants offering innovative solutions that could disrupt established players.

- Regulatory Hurdles: Data privacy compliance

- Supply Chain Issues: Software licensing and distribution

- Competitive Pressures: New market entrants

Leading Players in the VCS Industry Market

- GitLab Inc

- CollabNet Inc

- Perforce Software Inc

- Beanstalk (Wildbit LLC)

- Microsoft Corporation

- Bitbucket (Atlassian Corporation Plc)

- Amazon Web Services Inc

- Apache Software Foundation

- GitHub Inc

- Dynamsoft Corporation

Key Developments in VCS Industry Sector

- September 2023: Accenture and Workday expanded their partnership to develop data-led finance solutions, impacting the software and technology, retail, and media industries by enhancing agility and responsiveness. This indirectly boosts demand for efficient VCS.

- December 2022: Microsoft introduced a Git version control feature for canvas apps, addressing simultaneous editing challenges and improving collaboration in distributed development environments.

- September 2022: The WebKit project migrated to GitHub, leveraging its extensive developer community and automation capabilities to enhance open-source collaboration and development efficiency. This highlights GitHub's influence in the industry.

- [Add more recent key developments here for up-to-date information]

Strategic VCS Industry Market Outlook

- September 2023: Accenture and Workday expanded their partnership to develop data-led finance solutions, impacting the software and technology, retail, and media industries by enhancing agility and responsiveness. This indirectly boosts demand for efficient VCS.

- December 2022: Microsoft introduced a Git version control feature for canvas apps, addressing simultaneous editing challenges and improving collaboration in distributed development environments.

- September 2022: The WebKit project migrated to GitHub, leveraging its extensive developer community and automation capabilities to enhance open-source collaboration and development efficiency. This highlights GitHub's influence in the industry.

- [Add more recent key developments here for up-to-date information]

Strategic VCS Industry Market Outlook

The VCS industry is poised for significant growth, driven by technological advancements and increasing demand across various sectors. Strategic opportunities lie in expanding into emerging markets, particularly in Asia-Pacific, where digital transformation is accelerating. Companies that focus on enhancing collaboration features and integrating with emerging technologies like AI will be well-positioned to capitalize on future market potential.

VCS Industry Segmentation

-

1. Deployment Mode

- 1.1. On-Premise

- 1.2. On-Cloud

-

2. End-user Industry

- 2.1. IT and Telecom

- 2.2. Retail & E-commerce

- 2.3. Healthcare and Life Sciences

- 2.4. BFSI

- 2.5. Other

-

3. Type

- 3.1. Distributed VCS

- 3.2. Centralized VCS

VCS Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

VCS Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 16.63% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Digitization of Business Processes Leading to Adoption of Software; Increasing Demand for Reduced Complexities in Software Development and Cost Optimization

- 3.3. Market Restrains

- 3.3.1. Use of Diversified Software Applications in Organizations; Growing Complexity Due to Massive Data Generation

- 3.4. Market Trends

- 3.4.1. BFSI Industry Expected to Hold Significant Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global VCS Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 5.1.1. On-Premise

- 5.1.2. On-Cloud

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. IT and Telecom

- 5.2.2. Retail & E-commerce

- 5.2.3. Healthcare and Life Sciences

- 5.2.4. BFSI

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Type

- 5.3.1. Distributed VCS

- 5.3.2. Centralized VCS

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 6. North America VCS Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 6.1.1. On-Premise

- 6.1.2. On-Cloud

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. IT and Telecom

- 6.2.2. Retail & E-commerce

- 6.2.3. Healthcare and Life Sciences

- 6.2.4. BFSI

- 6.2.5. Other

- 6.3. Market Analysis, Insights and Forecast - by Type

- 6.3.1. Distributed VCS

- 6.3.2. Centralized VCS

- 6.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 7. Europe VCS Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 7.1.1. On-Premise

- 7.1.2. On-Cloud

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. IT and Telecom

- 7.2.2. Retail & E-commerce

- 7.2.3. Healthcare and Life Sciences

- 7.2.4. BFSI

- 7.2.5. Other

- 7.3. Market Analysis, Insights and Forecast - by Type

- 7.3.1. Distributed VCS

- 7.3.2. Centralized VCS

- 7.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 8. Asia Pacific VCS Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 8.1.1. On-Premise

- 8.1.2. On-Cloud

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. IT and Telecom

- 8.2.2. Retail & E-commerce

- 8.2.3. Healthcare and Life Sciences

- 8.2.4. BFSI

- 8.2.5. Other

- 8.3. Market Analysis, Insights and Forecast - by Type

- 8.3.1. Distributed VCS

- 8.3.2. Centralized VCS

- 8.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 9. Latin America VCS Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 9.1.1. On-Premise

- 9.1.2. On-Cloud

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. IT and Telecom

- 9.2.2. Retail & E-commerce

- 9.2.3. Healthcare and Life Sciences

- 9.2.4. BFSI

- 9.2.5. Other

- 9.3. Market Analysis, Insights and Forecast - by Type

- 9.3.1. Distributed VCS

- 9.3.2. Centralized VCS

- 9.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 10. Middle East and Africa VCS Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 10.1.1. On-Premise

- 10.1.2. On-Cloud

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. IT and Telecom

- 10.2.2. Retail & E-commerce

- 10.2.3. Healthcare and Life Sciences

- 10.2.4. BFSI

- 10.2.5. Other

- 10.3. Market Analysis, Insights and Forecast - by Type

- 10.3.1. Distributed VCS

- 10.3.2. Centralized VCS

- 10.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 11. North America VCS Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe VCS Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Spain

- 12.1.5 Italy

- 12.1.6 Spain

- 12.1.7 Belgium

- 12.1.8 Netherland

- 12.1.9 Nordics

- 12.1.10 Rest of Europe

- 13. Asia Pacific VCS Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 South Korea

- 13.1.5 Southeast Asia

- 13.1.6 Australia

- 13.1.7 Indonesia

- 13.1.8 Phillipes

- 13.1.9 Singapore

- 13.1.10 Thailandc

- 13.1.11 Rest of Asia Pacific

- 14. South America VCS Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 Brazil

- 14.1.2 Argentina

- 14.1.3 Peru

- 14.1.4 Chile

- 14.1.5 Colombia

- 14.1.6 Ecuador

- 14.1.7 Venezuela

- 14.1.8 Rest of South America

- 15. North America VCS Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 United States

- 15.1.2 Canada

- 15.1.3 Mexico

- 16. MEA VCS Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1 United Arab Emirates

- 16.1.2 Saudi Arabia

- 16.1.3 South Africa

- 16.1.4 Rest of Middle East and Africa

- 17. Competitive Analysis

- 17.1. Global Market Share Analysis 2024

- 17.2. Company Profiles

- 17.2.1 Gitlab Inc

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 CollabNet Inc

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 Perforce Software Inc

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 Beanstalk (Wildbit LLC)

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 Microsoft Corporation

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.6 Bitbucket org (Atlassian Corporation Plc)

- 17.2.6.1. Overview

- 17.2.6.2. Products

- 17.2.6.3. SWOT Analysis

- 17.2.6.4. Recent Developments

- 17.2.6.5. Financials (Based on Availability)

- 17.2.7 Amazon Web Services Inc

- 17.2.7.1. Overview

- 17.2.7.2. Products

- 17.2.7.3. SWOT Analysis

- 17.2.7.4. Recent Developments

- 17.2.7.5. Financials (Based on Availability)

- 17.2.8 APAChe Software Foundation

- 17.2.8.1. Overview

- 17.2.8.2. Products

- 17.2.8.3. SWOT Analysis

- 17.2.8.4. Recent Developments

- 17.2.8.5. Financials (Based on Availability)

- 17.2.9 Github Inc

- 17.2.9.1. Overview

- 17.2.9.2. Products

- 17.2.9.3. SWOT Analysis

- 17.2.9.4. Recent Developments

- 17.2.9.5. Financials (Based on Availability)

- 17.2.10 Dynamsoft Corporatio

- 17.2.10.1. Overview

- 17.2.10.2. Products

- 17.2.10.3. SWOT Analysis

- 17.2.10.4. Recent Developments

- 17.2.10.5. Financials (Based on Availability)

- 17.2.1 Gitlab Inc

List of Figures

- Figure 1: Global VCS Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: South America VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: North America VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: MEA VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 13: MEA VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America VCS Industry Revenue (Million), by Deployment Mode 2024 & 2032

- Figure 15: North America VCS Industry Revenue Share (%), by Deployment Mode 2024 & 2032

- Figure 16: North America VCS Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 17: North America VCS Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 18: North America VCS Industry Revenue (Million), by Type 2024 & 2032

- Figure 19: North America VCS Industry Revenue Share (%), by Type 2024 & 2032

- Figure 20: North America VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 21: North America VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: Europe VCS Industry Revenue (Million), by Deployment Mode 2024 & 2032

- Figure 23: Europe VCS Industry Revenue Share (%), by Deployment Mode 2024 & 2032

- Figure 24: Europe VCS Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 25: Europe VCS Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 26: Europe VCS Industry Revenue (Million), by Type 2024 & 2032

- Figure 27: Europe VCS Industry Revenue Share (%), by Type 2024 & 2032

- Figure 28: Europe VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Europe VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Asia Pacific VCS Industry Revenue (Million), by Deployment Mode 2024 & 2032

- Figure 31: Asia Pacific VCS Industry Revenue Share (%), by Deployment Mode 2024 & 2032

- Figure 32: Asia Pacific VCS Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 33: Asia Pacific VCS Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 34: Asia Pacific VCS Industry Revenue (Million), by Type 2024 & 2032

- Figure 35: Asia Pacific VCS Industry Revenue Share (%), by Type 2024 & 2032

- Figure 36: Asia Pacific VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 37: Asia Pacific VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 38: Latin America VCS Industry Revenue (Million), by Deployment Mode 2024 & 2032

- Figure 39: Latin America VCS Industry Revenue Share (%), by Deployment Mode 2024 & 2032

- Figure 40: Latin America VCS Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 41: Latin America VCS Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 42: Latin America VCS Industry Revenue (Million), by Type 2024 & 2032

- Figure 43: Latin America VCS Industry Revenue Share (%), by Type 2024 & 2032

- Figure 44: Latin America VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 45: Latin America VCS Industry Revenue Share (%), by Country 2024 & 2032

- Figure 46: Middle East and Africa VCS Industry Revenue (Million), by Deployment Mode 2024 & 2032

- Figure 47: Middle East and Africa VCS Industry Revenue Share (%), by Deployment Mode 2024 & 2032

- Figure 48: Middle East and Africa VCS Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 49: Middle East and Africa VCS Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 50: Middle East and Africa VCS Industry Revenue (Million), by Type 2024 & 2032

- Figure 51: Middle East and Africa VCS Industry Revenue Share (%), by Type 2024 & 2032

- Figure 52: Middle East and Africa VCS Industry Revenue (Million), by Country 2024 & 2032

- Figure 53: Middle East and Africa VCS Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global VCS Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global VCS Industry Revenue Million Forecast, by Deployment Mode 2019 & 2032

- Table 3: Global VCS Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Global VCS Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 5: Global VCS Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Germany VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United Kingdom VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: France VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Italy VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Spain VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Belgium VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Netherland VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Nordics VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Europe VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: China VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Japan VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: India VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Korea VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Southeast Asia VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Australia VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Indonesia VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Phillipes VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Singapore VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Thailandc VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Rest of Asia Pacific VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: Brazil VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Argentina VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Peru VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Chile VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Colombia VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Ecuador VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Venezuela VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Rest of South America VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 43: United States VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Canada VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Mexico VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 47: United Arab Emirates VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Saudi Arabia VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: South Africa VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Middle East and Africa VCS Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global VCS Industry Revenue Million Forecast, by Deployment Mode 2019 & 2032

- Table 52: Global VCS Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 53: Global VCS Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 54: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 55: Global VCS Industry Revenue Million Forecast, by Deployment Mode 2019 & 2032

- Table 56: Global VCS Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 57: Global VCS Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 58: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 59: Global VCS Industry Revenue Million Forecast, by Deployment Mode 2019 & 2032

- Table 60: Global VCS Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 61: Global VCS Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 62: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 63: Global VCS Industry Revenue Million Forecast, by Deployment Mode 2019 & 2032

- Table 64: Global VCS Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 65: Global VCS Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 66: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 67: Global VCS Industry Revenue Million Forecast, by Deployment Mode 2019 & 2032

- Table 68: Global VCS Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 69: Global VCS Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 70: Global VCS Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the VCS Industry?

The projected CAGR is approximately 16.63%.

2. Which companies are prominent players in the VCS Industry?

Key companies in the market include Gitlab Inc, CollabNet Inc, Perforce Software Inc, Beanstalk (Wildbit LLC), Microsoft Corporation, Bitbucket org (Atlassian Corporation Plc), Amazon Web Services Inc, APAChe Software Foundation, Github Inc, Dynamsoft Corporatio.

3. What are the main segments of the VCS Industry?

The market segments include Deployment Mode, End-user Industry, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Digitization of Business Processes Leading to Adoption of Software; Increasing Demand for Reduced Complexities in Software Development and Cost Optimization.

6. What are the notable trends driving market growth?

BFSI Industry Expected to Hold Significant Share.

7. Are there any restraints impacting market growth?

Use of Diversified Software Applications in Organizations; Growing Complexity Due to Massive Data Generation.

8. Can you provide examples of recent developments in the market?

September 2023 - Accenture and Workday have expanded their partnership to assist organizations in reinventing their finance functions to be more agile, data-driven, and customer-centric. The companies are collaborating to develop a suite of data-led, composable finance solutions that can be configured and reconfigured to help clients in the software and technology, retail, and media industries be more responsive to changing business requirements.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "VCS Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the VCS Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the VCS Industry?

To stay informed about further developments, trends, and reports in the VCS Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence