Key Insights

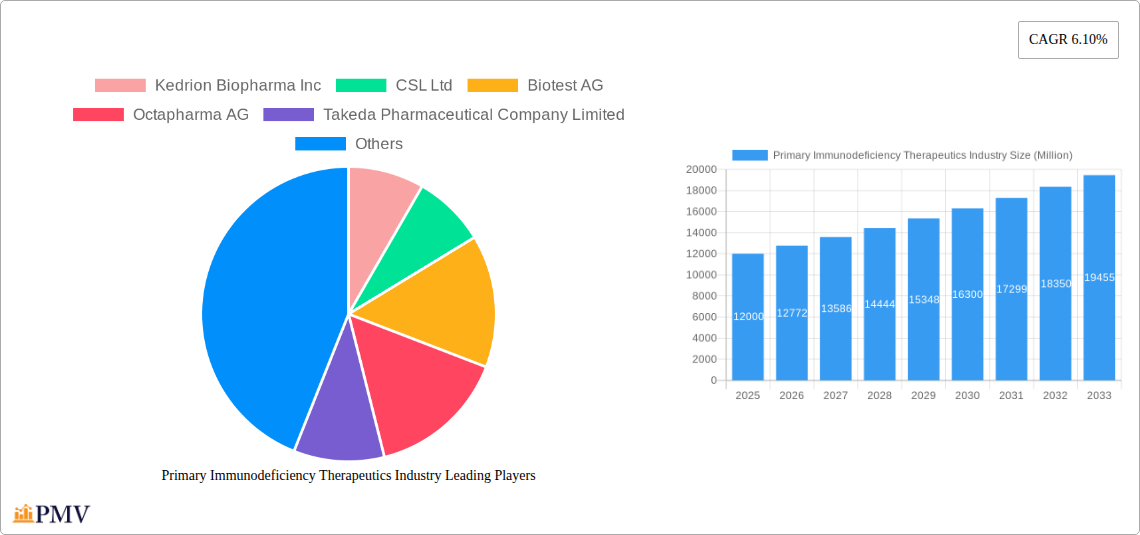

The Primary Immunodeficiency Therapeutics market is experiencing robust growth, projected to reach a substantial size driven by increasing prevalence of primary immunodeficiencies (PIDs), advancements in therapeutic modalities, and rising healthcare expenditure globally. The market's Compound Annual Growth Rate (CAGR) of 6.10% from 2019 to 2024 suggests a consistently expanding market. This growth is fueled by several factors. The development of novel therapies, including gene therapy and improved immunoglobulin replacement therapies, offers more effective treatment options leading to increased patient survival and improved quality of life. Furthermore, heightened awareness of PIDs among healthcare professionals and patients is resulting in earlier diagnosis and improved treatment initiation. The market is segmented by product type (Immunoglobulin Replacement Therapy, Stem Cell/Bone Marrow Transplantation, Antibiotic Therapy, Gene Therapy, Others) and disease type (Antibody Deficiency, Cellular Immunodeficiency, Innate Immune Disorders, Others). Immunoglobulin Replacement Therapy currently holds a significant market share, but the rapid advancement and adoption of gene therapy is anticipated to significantly impact market dynamics in the coming years. Geographic distribution shows North America and Europe as currently dominant regions, reflecting higher healthcare infrastructure and spending. However, growing awareness and improved healthcare accessibility in Asia-Pacific and other emerging markets are expected to drive future growth in these regions. The market faces certain challenges including the high cost of advanced therapies and the complexities associated with gene therapy development and administration. Nevertheless, the overall outlook remains positive, indicating substantial growth potential within the forecast period (2025-2033).

The competitive landscape is characterized by a mix of large pharmaceutical companies and specialized biotechnology firms. Key players such as Kedrion Biopharma Inc, CSL Ltd, Biotest AG, Octapharma AG, Takeda Pharmaceutical Company Limited, and others are actively involved in research and development, market expansion, and strategic partnerships to strengthen their positions within this dynamic market. The future of the Primary Immunodeficiency Therapeutics market is closely tied to ongoing clinical trials, regulatory approvals, and the continued development of innovative therapies that address the unmet needs of patients with PIDs. The market is expected to witness continued consolidation and strategic alliances as companies strive to enhance their product portfolios and broaden their global reach. The focus will likely remain on developing more effective and accessible therapies, reducing treatment costs, and improving patient outcomes.

Primary Immunodeficiency Therapeutics Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Primary Immunodeficiency Therapeutics market, offering invaluable insights for stakeholders across the industry. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report meticulously examines market dynamics, competitive landscapes, and future growth potential. The report leverages extensive data analysis to provide actionable intelligence and strategic recommendations. The market size is projected to reach xx Million by 2033, exhibiting a robust CAGR of xx% during the forecast period.

Primary Immunodeficiency Therapeutics Industry Market Structure & Competitive Dynamics

This section analyzes the competitive landscape of the Primary Immunodeficiency Therapeutics market, examining market concentration, innovation ecosystems, regulatory frameworks, and M&A activities. The market is moderately consolidated, with key players such as Kedrion Biopharma Inc, CSL Ltd, Biotest AG, Octapharma AG, Takeda Pharmaceutical Company Limited, Lupin Pharmaceuticals, Grifols S A, LFB group, Baxter international Inc, and Bio Products Laboratory Limited holding significant market share. However, the emergence of smaller, innovative companies is increasing competition.

Market share data for 2024 suggests that the top 5 players hold approximately xx% of the overall market, while the remaining companies share the remaining xx%. M&A activity has been moderate in recent years, with deal values ranging from a few Million to over xx Million. Innovation is primarily driven by advancements in gene therapy and other novel therapeutic approaches. Regulatory frameworks vary across geographies, influencing market access and product approvals. The primary substitutes are existing treatments for related immune deficiencies, though these often have limited efficacy for specific primary immunodeficiencies. End-user trends show a growing demand for more effective and targeted therapies with improved safety profiles.

Primary Immunodeficiency Therapeutics Industry Industry Trends & Insights

The Primary Immunodeficiency Therapeutics market is experiencing significant growth, driven by several key factors. The increasing prevalence of primary immunodeficiency diseases, coupled with advancements in diagnostic technologies, is expanding the addressable market. Technological disruptions, such as the development of novel gene therapies and immunotherapies, are transforming treatment paradigms. Consumer preferences are shifting towards personalized medicine and improved treatment outcomes. Furthermore, strategic collaborations, licensing agreements, and product launches by major players are fueling market expansion. The market’s CAGR from 2025 to 2033 is projected to be xx%, with market penetration expected to reach xx% by 2033 in key markets. Competitive dynamics are characterized by intense R&D investments, strategic partnerships, and increasing competition from both established players and emerging biotech companies.

Dominant Markets & Segments in Primary Immunodeficiency Therapeutics Industry

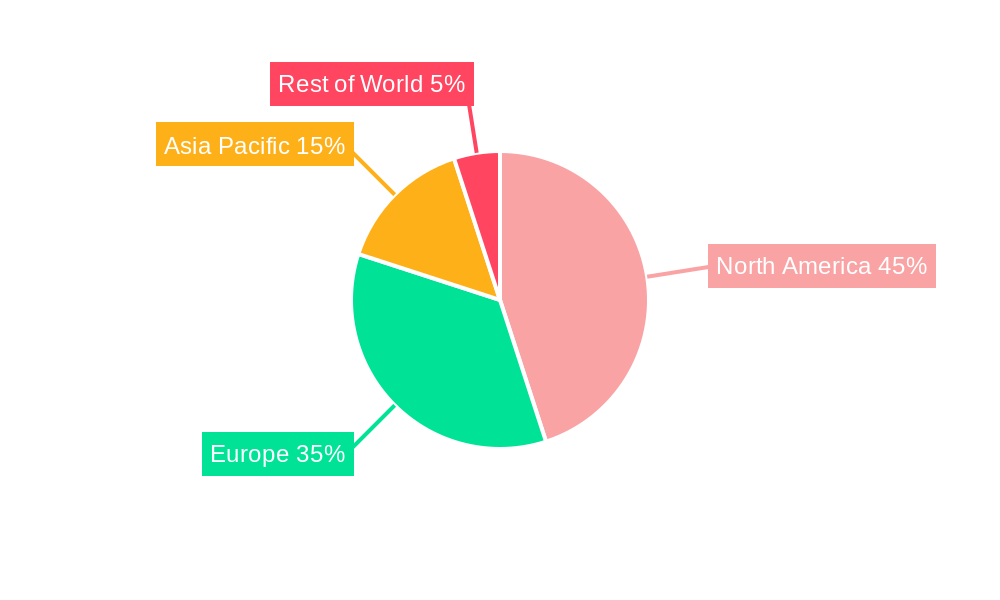

The North American region currently dominates the Primary Immunodeficiency Therapeutics market, followed by Europe. This dominance is driven by factors such as high healthcare expenditure, advanced healthcare infrastructure, and a robust regulatory environment. However, emerging markets in Asia-Pacific are demonstrating rapid growth potential.

By Product Type:

- Immunoglobulin Replacement Therapy: This segment holds the largest market share due to its established role in treating various immunodeficiencies. Growth is driven by the availability of high-purity products and improvements in delivery methods.

- Stem Cell/Bone Marrow Transplantation: This segment is growing steadily, driven by advancements in stem cell technology and increasing success rates.

- Antibiotic Therapy: This segment is a significant part of managing infections associated with immunodeficiency, but its long-term growth may be limited by the rise of antibiotic resistance.

- Gene Therapy: This rapidly growing segment shows huge potential, offering the possibility of curative treatment, although access and cost are major challenges.

- Others: This includes supportive therapies that may play a part in management but do not drive the majority of the market.

By Disease Type:

- Antibody Deficiency: This is a major segment due to the high prevalence of these disorders and the availability of replacement therapies.

- Cellular Immunodeficiency: This is a rapidly developing segment due to increasing understanding and therapeutic developments in cell-based therapies.

- Innate Immune Disorders: This segment is expanding with the development of therapies targeting the innate immune system.

- Others: A smaller group of less common primary immunodeficiencies.

Primary Immunodeficiency Therapeutics Industry Product Innovations

Significant advancements in gene therapy and novel immunotherapies are revolutionizing the treatment landscape of primary immunodeficiencies. These innovations offer more targeted and potentially curative therapies, compared to traditional treatments such as immunoglobulin replacement therapy. Improved delivery methods and targeted approaches enhance efficacy and reduce side effects. The market is witnessing a shift towards personalized medicine, with therapies tailored to specific patient needs and genetic profiles.

Report Segmentation & Scope

This report provides a granular segmentation of the Primary Immunodeficiency Therapeutics market by product type (Immunoglobulin Replacement Therapy, Stem Cell/Bone Marrow Transplantation, Antibiotic Therapy, Gene Therapy, Others) and by disease type (Antibody Deficiency, Cellular Immunodeficiency, Innate Immune Disorders, Others). Each segment's growth projections, market size, and competitive dynamics are analyzed. The report provides detailed analysis of historical data (2019-2024), current market estimations (2025), and detailed market projections (2025-2033).

Key Drivers of Primary Immunodeficiency Therapeutics Industry Growth

The growth of this market is propelled by several factors: rising prevalence of primary immunodeficiencies, increased awareness and improved diagnostic capabilities leading to early diagnosis and treatment, technological advancements in gene therapy and immunotherapy providing more effective treatment options, and supportive regulatory frameworks facilitating drug development and market access. Increased investment in R&D by major pharmaceutical companies is also contributing to market growth.

Challenges in the Primary Immunodeficiency Therapeutics Industry Sector

The industry faces several challenges, including the high cost of novel therapies limiting accessibility for many patients. Regulatory hurdles and lengthy approval processes can delay market entry for new drugs, and the complexity of managing these diseases often requires multidisciplinary care, which can be challenging to coordinate. Supply chain disruptions and the potential for shortages of critical raw materials can also create instability in the market. The competitive landscape necessitates robust R&D and marketing strategies for maintaining market share.

Leading Players in the Primary Immunodeficiency Therapeutics Industry Market

- Kedrion Biopharma Inc

- CSL Ltd

- Biotest AG

- Octapharma AG

- Takeda Pharmaceutical Company Limited

- Lupin Pharmaceuticals

- Grifols S A

- LFB group

- Baxter international Inc

- Bio Products Laboratory Limited

Key Developments in Primary Immunodeficiency Therapeutics Industry Sector

- September 2022: Lactiga Therapeutics raised USD 1.6 Million in oversubscribed pre-seed financing for developing therapeutics for patients with primary immunodeficiency diseases. This signifies investor confidence in the potential of novel therapies in this area.

- April 2022: Pharming Group N.V. presented positive data from the pivotal Phase II/III trial of leniolisib for the treatment of activated phosphoinositide 3-kinase delta (PI3Kδ) syndrome (APDS), a primary immunodeficiency. This highlights significant progress in developing targeted therapies for specific primary immunodeficiencies.

Strategic Primary Immunodeficiency Therapeutics Industry Market Outlook

The future of the Primary Immunodeficiency Therapeutics market looks promising, driven by continued technological advancements, increased investment in R&D, and the growing awareness of primary immunodeficiencies. Strategic opportunities lie in developing novel therapies, expanding market access in emerging economies, and forging strategic collaborations to accelerate innovation and bring life-saving treatments to patients. The focus on personalized medicine and the development of curative therapies will shape future market dynamics.

Primary Immunodeficiency Therapeutics Industry Segmentation

-

1. Disease Type

- 1.1. Antibody Deficiency

- 1.2. Cellular Immunodeficiency

- 1.3. Innate Immune Disorders

- 1.4. Others

-

2. Product Type

- 2.1. Immunoglobulin Replacement Therapy

- 2.2. Stem Cell/Bone Marrow Transplantation

- 2.3. Antibiotic Therapy

- 2.4. Gene Therapy

- 2.5. Others

Primary Immunodeficiency Therapeutics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Primary Immunodeficiency Therapeutics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.10% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Prevalence of Immunodeficiency diseases; Technological Advancements in Genetic Therapy

- 3.3. Market Restrains

- 3.3.1. High Cost of the Therapies; Side Effects Associated with the Treatment

- 3.4. Market Trends

- 3.4.1. Gene Therapy Segment is Expected to Hold a Major Market Share in the Primary Immunodeficiency Therapeutics Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 5.1.1. Antibody Deficiency

- 5.1.2. Cellular Immunodeficiency

- 5.1.3. Innate Immune Disorders

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Immunoglobulin Replacement Therapy

- 5.2.2. Stem Cell/Bone Marrow Transplantation

- 5.2.3. Antibiotic Therapy

- 5.2.4. Gene Therapy

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Disease Type

- 6. North America Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 6.1.1. Antibody Deficiency

- 6.1.2. Cellular Immunodeficiency

- 6.1.3. Innate Immune Disorders

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Immunoglobulin Replacement Therapy

- 6.2.2. Stem Cell/Bone Marrow Transplantation

- 6.2.3. Antibiotic Therapy

- 6.2.4. Gene Therapy

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Disease Type

- 7. Europe Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 7.1.1. Antibody Deficiency

- 7.1.2. Cellular Immunodeficiency

- 7.1.3. Innate Immune Disorders

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Immunoglobulin Replacement Therapy

- 7.2.2. Stem Cell/Bone Marrow Transplantation

- 7.2.3. Antibiotic Therapy

- 7.2.4. Gene Therapy

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Disease Type

- 8. Asia Pacific Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 8.1.1. Antibody Deficiency

- 8.1.2. Cellular Immunodeficiency

- 8.1.3. Innate Immune Disorders

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Immunoglobulin Replacement Therapy

- 8.2.2. Stem Cell/Bone Marrow Transplantation

- 8.2.3. Antibiotic Therapy

- 8.2.4. Gene Therapy

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Disease Type

- 9. Middle East and Africa Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 9.1.1. Antibody Deficiency

- 9.1.2. Cellular Immunodeficiency

- 9.1.3. Innate Immune Disorders

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Immunoglobulin Replacement Therapy

- 9.2.2. Stem Cell/Bone Marrow Transplantation

- 9.2.3. Antibiotic Therapy

- 9.2.4. Gene Therapy

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Disease Type

- 10. South America Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 10.1.1. Antibody Deficiency

- 10.1.2. Cellular Immunodeficiency

- 10.1.3. Innate Immune Disorders

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Immunoglobulin Replacement Therapy

- 10.2.2. Stem Cell/Bone Marrow Transplantation

- 10.2.3. Antibiotic Therapy

- 10.2.4. Gene Therapy

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Disease Type

- 11. North America Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America Primary Immunodeficiency Therapeutics Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Kedrion Biopharma Inc

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 CSL Ltd

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Biotest AG

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Octapharma AG

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Takeda Pharmaceutical Company Limited

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Lupin Pharmaceuticals*List Not Exhaustive

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Grifols S A

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 LFB group

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Baxter international Inc

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Bio Products Laboratory Limited

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Kedrion Biopharma Inc

List of Figures

- Figure 1: Global Primary Immunodeficiency Therapeutics Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Disease Type 2024 & 2032

- Figure 13: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2024 & 2032

- Figure 14: North America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 15: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 16: North America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Disease Type 2024 & 2032

- Figure 19: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2024 & 2032

- Figure 20: Europe Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 21: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 22: Europe Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Disease Type 2024 & 2032

- Figure 25: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2024 & 2032

- Figure 26: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 27: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 28: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Disease Type 2024 & 2032

- Figure 31: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2024 & 2032

- Figure 32: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 33: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 34: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: South America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Disease Type 2024 & 2032

- Figure 37: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Disease Type 2024 & 2032

- Figure 38: South America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 39: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 40: South America Primary Immunodeficiency Therapeutics Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: South America Primary Immunodeficiency Therapeutics Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Disease Type 2019 & 2032

- Table 3: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Germany Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Australia Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: GCC Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Brazil Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Argentina Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of South America Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Disease Type 2019 & 2032

- Table 32: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 33: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United States Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Canada Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Mexico Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Disease Type 2019 & 2032

- Table 38: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 39: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 40: Germany Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: United Kingdom Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: France Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Italy Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Spain Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Rest of Europe Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Disease Type 2019 & 2032

- Table 47: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 48: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 49: China Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Japan Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: India Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Australia Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: South Korea Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Rest of Asia Pacific Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Disease Type 2019 & 2032

- Table 56: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 57: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: GCC Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: South Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Rest of Middle East and Africa Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Disease Type 2019 & 2032

- Table 62: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 63: Global Primary Immunodeficiency Therapeutics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 64: Brazil Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Argentina Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Rest of South America Primary Immunodeficiency Therapeutics Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Primary Immunodeficiency Therapeutics Industry?

The projected CAGR is approximately 6.10%.

2. Which companies are prominent players in the Primary Immunodeficiency Therapeutics Industry?

Key companies in the market include Kedrion Biopharma Inc, CSL Ltd, Biotest AG, Octapharma AG, Takeda Pharmaceutical Company Limited, Lupin Pharmaceuticals*List Not Exhaustive, Grifols S A, LFB group, Baxter international Inc, Bio Products Laboratory Limited.

3. What are the main segments of the Primary Immunodeficiency Therapeutics Industry?

The market segments include Disease Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Immunodeficiency diseases; Technological Advancements in Genetic Therapy.

6. What are the notable trends driving market growth?

Gene Therapy Segment is Expected to Hold a Major Market Share in the Primary Immunodeficiency Therapeutics Market.

7. Are there any restraints impacting market growth?

High Cost of the Therapies; Side Effects Associated with the Treatment.

8. Can you provide examples of recent developments in the market?

In September 2022, Lactiga Therapeutics raised USD 1.6 million in oversubscribed pre-seed financing for developing therapeutics for patients with primary immunodeficiency diseases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Primary Immunodeficiency Therapeutics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Primary Immunodeficiency Therapeutics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Primary Immunodeficiency Therapeutics Industry?

To stay informed about further developments, trends, and reports in the Primary Immunodeficiency Therapeutics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence