Key Insights

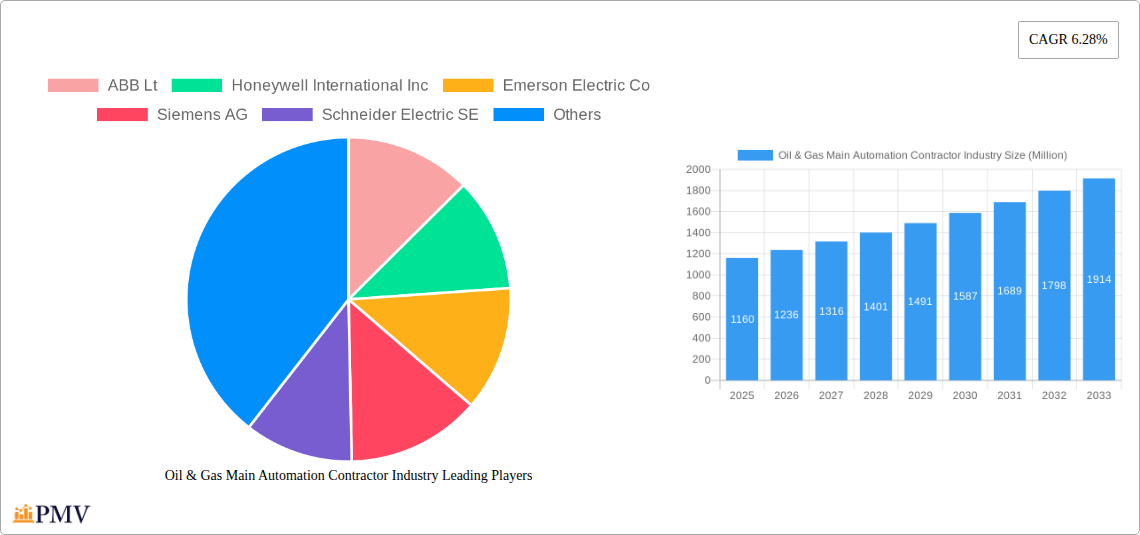

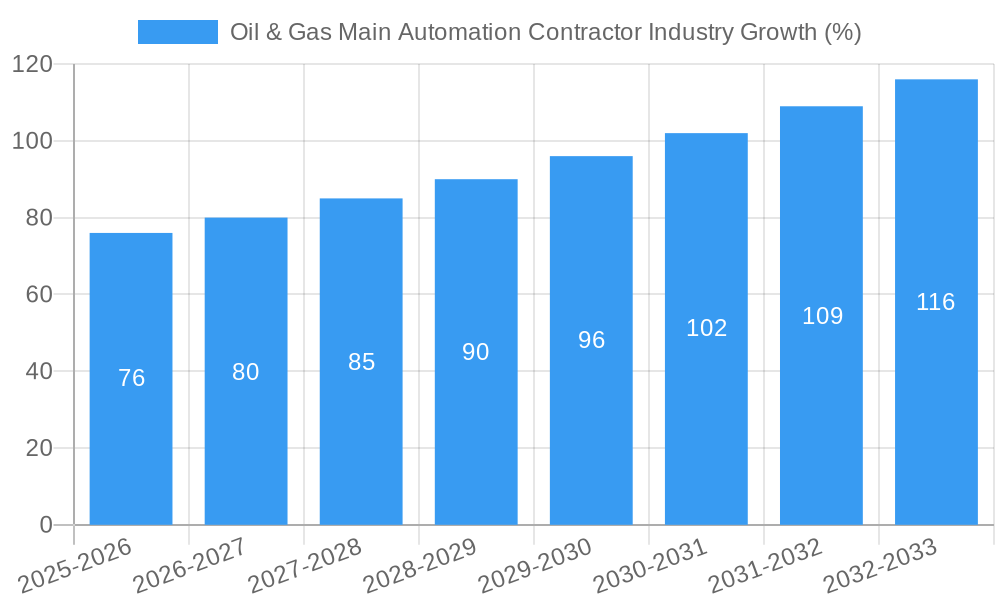

The Oil & Gas Main Automation Contractor industry is experiencing robust growth, projected to reach a market size of $1.16 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 6.28% from 2025 to 2033. This expansion is driven primarily by the increasing demand for enhanced operational efficiency, safety, and reduced operational expenditure within oil and gas operations globally. The industry is witnessing a significant push towards automation solutions to optimize production processes, improve resource allocation, and minimize human intervention in hazardous environments. Furthermore, stringent government regulations on emissions and safety are accelerating the adoption of advanced automation technologies, creating substantial growth opportunities for contractors specializing in upstream (offshore and onshore), midstream, and downstream applications. The market is segmented by project size, with large-scale projects (>$31 million) contributing significantly to overall revenue due to the higher complexity and technology integration involved. Leading players like ABB, Honeywell, Emerson Electric, Siemens, Schneider Electric, Rockwell Automation, and Yokogawa Electric are strategically investing in R&D and expanding their service portfolios to cater to the growing market demand.

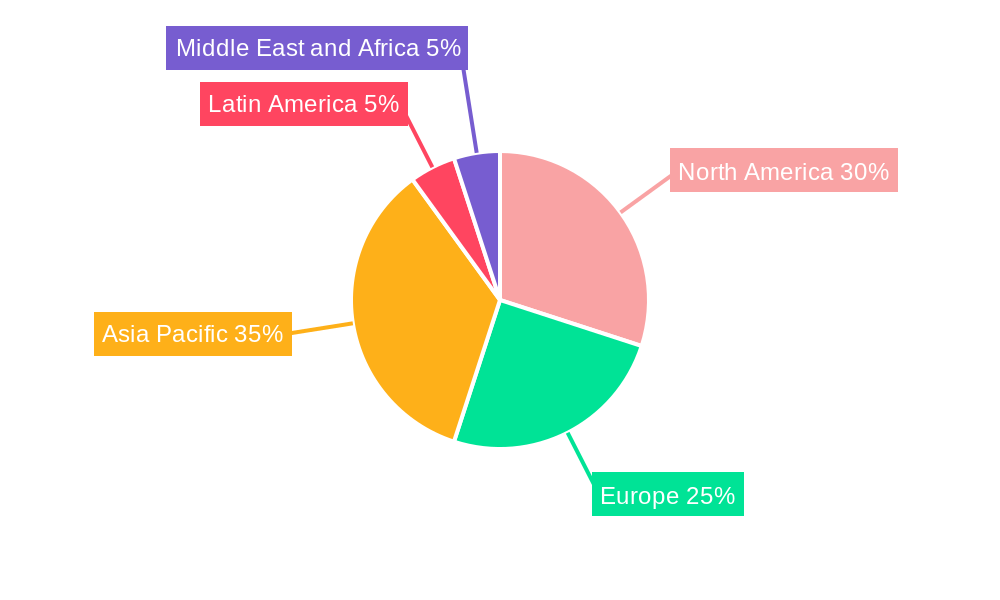

Growth is expected to be particularly strong in the Asia-Pacific region due to increasing energy demands and ongoing infrastructure development within the oil and gas sector. However, challenges remain, including fluctuating oil and gas prices, the complexity of integrating legacy systems with modern automation technologies, and the need for skilled workforce development to effectively manage and maintain sophisticated automation solutions. Despite these restraints, the long-term outlook for the Oil & Gas Main Automation Contractor industry remains positive, driven by ongoing technological advancements, stricter safety regulations, and the imperative for optimizing production efficiency across the entire oil and gas value chain. The industry's future hinges on its ability to adapt to evolving technological landscapes, develop innovative automation solutions tailored to specific operational needs, and address skilled labor shortages.

Oil & Gas Main Automation Contractor Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Oil & Gas Main Automation Contractor industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report delivers critical data on market size, segmentation, competitive landscape, and future growth prospects. The study incorporates key developments and industry trends, equipping readers with the knowledge needed for strategic decision-making.

Oil & Gas Main Automation Contractor Industry Market Structure & Competitive Dynamics

The Oil & Gas Main Automation Contractor industry exhibits a moderately concentrated market structure, with a handful of multinational corporations holding significant market share. Key players such as ABB Ltd, Honeywell International Inc, Emerson Electric Co, Siemens AG, Schneider Electric SE, Rockwell Automation Inc, and Yokogawa Electric Corporation, dominate the landscape, engaging in fierce competition through product innovation, strategic partnerships, and geographical expansion. Market concentration is estimated at xx%, reflecting the dominance of these major players. Innovation ecosystems are thriving, with continuous investment in Research & Development driving advancements in automation technologies. Regulatory frameworks, varying across regions, influence market access and operational practices. The industry is witnessing increasing M&A activity, with deal values exceeding USD xx Million in recent years. These activities aim to consolidate market share, expand technological capabilities, and access new markets. End-user trends favor integrated solutions, with oil and gas companies prioritizing automation to enhance efficiency, safety, and operational profitability. Substitutes for main automation contractors are limited, given the specialized nature of these services.

- Market Share (Estimated 2025): ABB Ltd (xx%), Honeywell International Inc (xx%), Emerson Electric Co (xx%), Siemens AG (xx%), Schneider Electric SE (xx%), Rockwell Automation Inc (xx%), Yokogawa Electric Corporation (xx%), Others (xx%).

- M&A Activity (2019-2024): Total deal value estimated at USD xx Million, with an average deal size of USD xx Million.

Oil & Gas Main Automation Contractor Industry Industry Trends & Insights

The Oil & Gas Main Automation Contractor industry is experiencing robust growth, driven by the increasing demand for automation solutions within the oil and gas sector. The market is projected to grow at a CAGR of xx% during the forecast period (2025-2033). Technological disruptions, including the rise of artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT), are reshaping the industry landscape. These technologies enable improved data analysis, predictive maintenance, and remote operations, leading to enhanced efficiency and reduced operational costs. Consumer preferences are shifting towards integrated automation systems offering comprehensive solutions that encompass multiple aspects of oil and gas operations. Competitive dynamics are characterized by intense rivalry amongst established players and the emergence of innovative start-ups. Market penetration of advanced automation technologies is steadily increasing, driven by regulatory pressures and operational needs. The industry's growth is also fueled by increasing investments in upstream, midstream, and downstream oil and gas projects globally, particularly in developing economies.

Dominant Markets & Segments in Oil & Gas Main Automation Contractor Industry

The Upstream sector (both onshore and offshore) currently represents the dominant segment in the Oil & Gas Main Automation Contractor industry, accounting for xx% of the total market in 2025. This dominance is attributed to the significant investments in exploration and production activities globally. The large project size segment (USD 31 million and above) also exhibits significant dominance, owing to the substantial capital expenditures associated with large-scale oil and gas projects.

- Key Drivers for Upstream Dominance:

- Extensive exploration and production activities.

- Stringent safety and regulatory requirements demanding advanced automation.

- High capital expenditure for offshore projects.

- Key Drivers for Large Project Size Dominance:

- Complex automation requirements demanding specialized expertise.

- Higher profitability margins.

- Increased willingness to invest in cutting-edge technologies.

The Middle East and North America are the leading geographic regions for this industry, propelled by robust oil and gas production, supportive government policies, and a well-established infrastructure.

Oil & Gas Main Automation Contractor Industry Product Innovations

Recent product innovations focus on enhancing safety, efficiency, and reducing operational costs through the integration of advanced technologies. This includes the development of AI-powered predictive maintenance systems, cloud-based control platforms, and cybersecurity solutions for enhanced data protection. These innovations offer competitive advantages through improved operational reliability, reduced downtime, and enhanced environmental performance. The market increasingly favors integrated solutions that seamlessly combine various automation technologies, enabling streamlined operations and improved data management.

Report Segmentation & Scope

This report segments the Oil & Gas Main Automation Contractor market by sector (Upstream – Offshore and Onshore, Midstream, Downstream) and project size (Small and Medium – USD 5 million to USD 30 million, Large – USD 31 million and Above). Each segment is analyzed in detail, providing insights into growth projections, market size, and competitive dynamics. The Upstream segment is expected to maintain its dominance, with substantial growth projected in both offshore and onshore sub-segments. The Midstream and Downstream segments are also expected to witness significant growth, driven by increasing investments in refining and processing capacity. The Large project size segment will retain its lead in terms of revenue generation, but the Small and Medium project size segment is expected to show promising growth.

Key Drivers of Oil & Gas Main Automation Contractor Industry Growth

Several factors contribute to the industry's robust growth. Technological advancements, particularly in AI, ML, and IoT, are driving demand for sophisticated automation solutions. Stringent safety regulations and the growing need for improved operational efficiency are compelling oil and gas companies to invest in advanced automation technologies. Furthermore, increasing global energy demand and exploration activities in emerging markets fuel the expansion of the oil and gas sector, consequently increasing the demand for main automation contractors.

Challenges in the Oil & Gas Main Automation Contractor Industry Sector

The industry faces challenges including fluctuating oil and gas prices, which directly impact investment levels. Supply chain disruptions can lead to project delays and increased costs. Intense competition among established players and the emergence of new entrants pose a continuous threat. Regulatory compliance requirements, particularly in relation to environmental protection and safety, can present significant hurdles. These factors collectively impact the profitability and sustainability of the Oil & Gas Main Automation Contractor industry, affecting project timelines and costs by an estimated xx%.

Leading Players in the Oil & Gas Main Automation Contractor Industry Market

- ABB Ltd

- Honeywell International Inc

- Emerson Electric Co

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc

- Yokogawa Electric Corporation

Key Developments in Oil & Gas Main Automation Contractor Industry Sector

June 2022: Honeywell and Anchorage Investments Ltd signed a Memorandum of Understanding (MoU) to make Honeywell the Integrated Main Automation Contractor (IMAC) for the Anchor Benitoite Petrochemicals Complex in Egypt. This signifies a major step towards the adoption of Honeywell's autonomous technologies within the oil and gas sector.

January 2022: Honeywell inaugurated a new production facility in Saudi Arabia dedicated to oil and gas projects. This expansion reinforces Honeywell’s commitment to the Middle Eastern market and enhances its capacity to deliver advanced automation solutions.

Strategic Oil & Gas Main Automation Contractor Industry Market Outlook

The Oil & Gas Main Automation Contractor industry is poised for continued growth, driven by sustained demand for enhanced operational efficiency, safety, and sustainability. Strategic opportunities lie in leveraging advanced technologies like AI and IoT to deliver integrated, data-driven solutions. Expansion into emerging markets and strategic partnerships with oil and gas companies offer significant potential for growth. Companies focusing on innovation, technological integration, and strong client relationships are best positioned to capitalize on future market opportunities and secure a leading position within this competitive landscape.

Oil & Gas Main Automation Contractor Industry Segmentation

-

1. Sector

- 1.1. Upstream (Offshore and Onshore)

- 1.2. Midstream

- 1.3. Downstream

-

2. Project Size

- 2.1. Small and Medium (USD 5 million to USD 30 million)

- 2.2. Large (USD 31 million and Above)

Oil & Gas Main Automation Contractor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Oil & Gas Main Automation Contractor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.28% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Preference of Oil and Gas Companies for a MAC Approach to Avoid Project Management and Integration Complexities

- 3.3. Market Restrains

- 3.3.1. Additional Costs Associated with Machine Safety Systems

- 3.4. Market Trends

- 3.4.1. Upstream Segment to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream (Offshore and Onshore)

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Project Size

- 5.2.1. Small and Medium (USD 5 million to USD 30 million)

- 5.2.2. Large (USD 31 million and Above)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. North America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream (Offshore and Onshore)

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.2. Market Analysis, Insights and Forecast - by Project Size

- 6.2.1. Small and Medium (USD 5 million to USD 30 million)

- 6.2.2. Large (USD 31 million and Above)

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Europe Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 7.1.1. Upstream (Offshore and Onshore)

- 7.1.2. Midstream

- 7.1.3. Downstream

- 7.2. Market Analysis, Insights and Forecast - by Project Size

- 7.2.1. Small and Medium (USD 5 million to USD 30 million)

- 7.2.2. Large (USD 31 million and Above)

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 8. Asia Pacific Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 8.1.1. Upstream (Offshore and Onshore)

- 8.1.2. Midstream

- 8.1.3. Downstream

- 8.2. Market Analysis, Insights and Forecast - by Project Size

- 8.2.1. Small and Medium (USD 5 million to USD 30 million)

- 8.2.2. Large (USD 31 million and Above)

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 9. Latin America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 9.1.1. Upstream (Offshore and Onshore)

- 9.1.2. Midstream

- 9.1.3. Downstream

- 9.2. Market Analysis, Insights and Forecast - by Project Size

- 9.2.1. Small and Medium (USD 5 million to USD 30 million)

- 9.2.2. Large (USD 31 million and Above)

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 10. Middle East and Africa Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 10.1.1. Upstream (Offshore and Onshore)

- 10.1.2. Midstream

- 10.1.3. Downstream

- 10.2. Market Analysis, Insights and Forecast - by Project Size

- 10.2.1. Small and Medium (USD 5 million to USD 30 million)

- 10.2.2. Large (USD 31 million and Above)

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 11. North America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East and Africa Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 ABB Lt

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Honeywell International Inc

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Emerson Electric Co

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Siemens AG

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Schneider Electric SE

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Rockwell Automation Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Yokogawa Electric Corporation

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.1 ABB Lt

List of Figures

- Figure 1: Global Oil & Gas Main Automation Contractor Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2024 & 2032

- Figure 13: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 14: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2024 & 2032

- Figure 15: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2024 & 2032

- Figure 16: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2024 & 2032

- Figure 19: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 20: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2024 & 2032

- Figure 21: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2024 & 2032

- Figure 22: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2024 & 2032

- Figure 25: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 26: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2024 & 2032

- Figure 27: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2024 & 2032

- Figure 28: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2024 & 2032

- Figure 31: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 32: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2024 & 2032

- Figure 33: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2024 & 2032

- Figure 34: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2024 & 2032

- Figure 37: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 38: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2024 & 2032

- Figure 39: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2024 & 2032

- Figure 40: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2019 & 2032

- Table 4: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Oil & Gas Main Automation Contractor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Oil & Gas Main Automation Contractor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Oil & Gas Main Automation Contractor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Oil & Gas Main Automation Contractor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Oil & Gas Main Automation Contractor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 16: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2019 & 2032

- Table 17: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 19: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2019 & 2032

- Table 20: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 22: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2019 & 2032

- Table 23: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 25: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2019 & 2032

- Table 26: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 28: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2019 & 2032

- Table 29: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil & Gas Main Automation Contractor Industry?

The projected CAGR is approximately 6.28%.

2. Which companies are prominent players in the Oil & Gas Main Automation Contractor Industry?

Key companies in the market include ABB Lt, Honeywell International Inc, Emerson Electric Co, Siemens AG, Schneider Electric SE, Rockwell Automation Inc, Yokogawa Electric Corporation.

3. What are the main segments of the Oil & Gas Main Automation Contractor Industry?

The market segments include Sector, Project Size.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.16 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Preference of Oil and Gas Companies for a MAC Approach to Avoid Project Management and Integration Complexities.

6. What are the notable trends driving market growth?

Upstream Segment to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Additional Costs Associated with Machine Safety Systems.

8. Can you provide examples of recent developments in the market?

June 2022: In a significant development, Honeywell and Anchorage Investments Ltd inked a memorandum of understanding (MoU), opening the door for Honeywell's cutting-edge industrial autonomous technologies to be incorporated into the advanced Anchor Benitoite Petrochemicals Complex, located within Egypt's Suez Canal Economic Zone. As per the terms of the MoU, both companies will commence initial deliberations to appoint Honeywell Process Solutions (HPS) as the integrated main automation contractor (IMAC) for the facility.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil & Gas Main Automation Contractor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil & Gas Main Automation Contractor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil & Gas Main Automation Contractor Industry?

To stay informed about further developments, trends, and reports in the Oil & Gas Main Automation Contractor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence