Key Insights

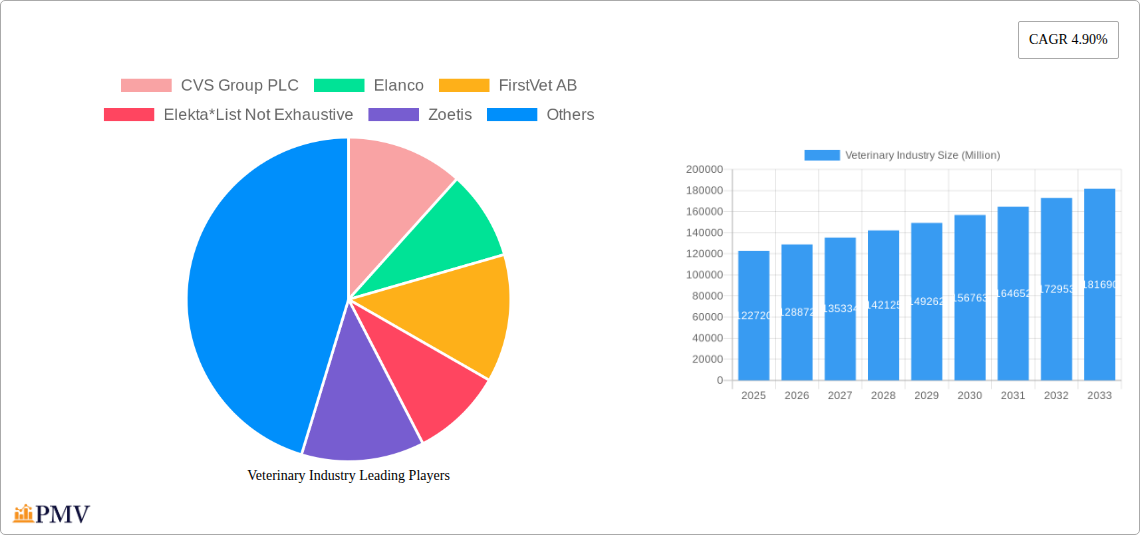

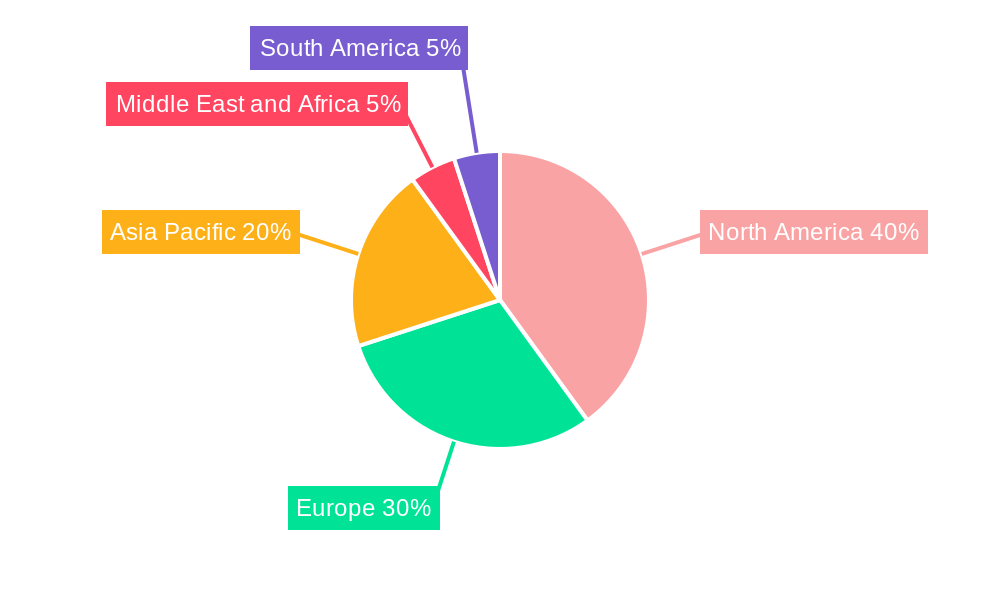

The global veterinary market, valued at $122.72 billion in 2025, is projected to experience robust growth, driven by several key factors. Rising pet ownership worldwide, coupled with increasing humanization of pets and a corresponding willingness to spend on their healthcare, significantly fuels market expansion. Advancements in veterinary diagnostic technologies, including sophisticated imaging techniques and genetic testing, contribute to improved animal health outcomes and increased demand for specialized services. The growing prevalence of chronic diseases in animals, mirroring human health trends, necessitates ongoing care and treatment, further boosting market revenue. The market is segmented by service (surgery, diagnostics, monitoring, other) and animal type (companion, farm), with companion animals currently dominating due to higher owner spending. The increasing adoption of telemedicine and remote monitoring solutions is reshaping service delivery, offering convenience and accessibility to pet owners, particularly in rural areas. However, factors such as the high cost of advanced veterinary treatments and the economic disparities impacting access to care act as market restraints. Geographic expansion is expected, with North America and Europe maintaining significant market shares due to established veterinary infrastructure and high pet ownership rates. Rapid growth is, however, anticipated in emerging economies of Asia Pacific, driven by rising disposable incomes and increasing pet ownership in these regions.

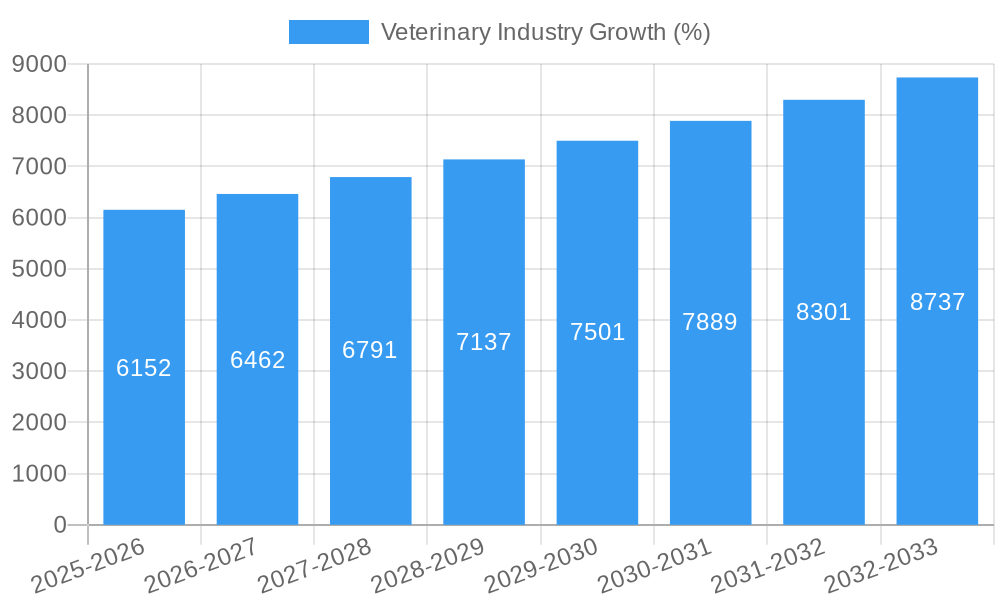

The forecast period (2025-2033) suggests a continued upward trajectory, with the 4.90% CAGR indicating substantial growth potential. Competitive pressures among established players like Zoetis, Idexx Laboratories, and Mars Inc., alongside the emergence of innovative startups, will shape market dynamics. Strategic mergers and acquisitions are likely to further consolidate the market, leading to improved service offerings and a more integrated approach to animal healthcare. The increasing focus on preventive care and wellness programs, alongside the development of specialized veterinary pharmaceuticals and therapeutics, will continue to drive market segmentation and innovation. Regulatory frameworks and ethical considerations surrounding animal welfare will play a crucial role in shaping the future of the veterinary market. Ultimately, the market's success hinges on addressing the evolving needs of pet owners and farmers, while ensuring accessibility and affordability of vital animal healthcare services.

Comprehensive Report: Veterinary Industry Market Analysis, 2019-2033

This comprehensive report provides an in-depth analysis of the global veterinary industry, projecting a market value exceeding $XX Million by 2033. The study covers the period 2019-2033, with 2025 as the base and estimated year. This report is crucial for investors, industry stakeholders, and veterinary professionals seeking actionable insights into market trends, competitive landscapes, and future growth opportunities. The report incorporates data from key players including CVS Group PLC, Elanco, FirstVet AB, Elekta, Zoetis, CityVet Inc, Kremer Veterinary Services, Ethos Veterinary Health, Torigen Pharmaceuticals Inc, Karyopharm Therapeutics Inc, ELIAS Animal Health, Greencross Limited, Armor Animal Health (Animart), Mars Inc, and Idexx laboratories.

Veterinary Industry Market Structure & Competitive Dynamics

The global veterinary market is characterized by a moderately concentrated structure, with a few large multinational corporations dominating alongside numerous smaller regional players. Market share is influenced by factors such as geographic reach, product portfolio diversification (including pharmaceuticals, diagnostics, and services), and technological innovation. The market exhibits a dynamic competitive landscape, with ongoing mergers and acquisitions (M&A) significantly shaping market dynamics. Deal values in recent years have ranged from tens to hundreds of Millions of dollars, reflecting the industry's consolidation trend and the pursuit of economies of scale. Innovation ecosystems are driven by technological advancements in diagnostics, therapeutics, and data analytics, fostering the development of advanced veterinary products and services. Stringent regulatory frameworks govern the approval and distribution of veterinary pharmaceuticals and medical devices, impacting market entry and competition. Substitute products and services are limited due to the specialized nature of veterinary care, but the rise of telehealth and remote monitoring technologies is gradually altering the delivery landscape. End-user trends, characterized by increasing pet ownership and growing awareness of animal welfare, are driving demand for higher-quality veterinary care.

- Market Concentration: Moderately concentrated, with top players holding significant market share.

- M&A Activity: High, with deals valued at tens to hundreds of Millions of dollars annually driving consolidation.

- Regulatory Framework: Stringent regulations impacting product approval and market access.

- Innovation Ecosystem: Driven by technological advances in diagnostics, therapeutics, and data analytics.

Veterinary Industry Industry Trends & Insights

The veterinary industry is experiencing robust growth driven by multiple factors, including the increasing humanization of pets, rising pet ownership globally, escalating consumer spending on animal healthcare, and advancements in veterinary medicine and technology. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is estimated to be XX%, indicating substantial market expansion. Technological disruptions, particularly in diagnostics (e.g., advanced imaging techniques and point-of-care testing) and therapeutics (e.g., personalized medicine and gene therapy), are transforming veterinary practice. Consumer preferences are shifting towards proactive and preventative healthcare, driving demand for wellness services and personalized care. Competitive dynamics are influenced by the entry of new players, technological innovation, and ongoing M&A activity, shaping the industry's landscape. Market penetration of advanced diagnostic tools and therapeutic modalities remains relatively low, offering significant opportunities for growth.

Dominant Markets & Segments in Veterinary Industry

The companion animal segment dominates the veterinary industry, driven by high pet ownership rates and increasing expenditure on pet healthcare. Geographically, North America and Europe currently lead the market, but Asia-Pacific is emerging as a key growth region.

- By Service: Diagnostic Tests and Imaging displays highest growth potential due to increasing adoption of advanced technologies. Surgery remains a significant segment driven by the high incidence of surgical interventions in companion animals.

- By Animal Type: Companion animals (dogs and cats) constitute the largest segment due to increasing pet ownership and consumer spending on pet health. The farm animal segment shows promising growth driven by increasing demand for animal protein and rising focus on animal health and productivity in agriculture.

Key Drivers for Dominant Segments:

- Companion Animal: High pet ownership rates, increasing human-animal bond, rising disposable incomes.

- Diagnostic Tests & Imaging: Technological advancements, early disease detection, improved treatment outcomes.

- North America & Europe: High per capita income, advanced veterinary infrastructure, established regulatory frameworks.

Veterinary Industry Product Innovations

Recent product innovations in the veterinary sector include advanced diagnostic tools such as high-resolution ultrasound and MRI systems, minimally invasive surgical techniques, personalized medicine approaches based on genetic testing, and telemedicine platforms for remote patient monitoring. These advancements enhance diagnostic accuracy, improve treatment efficacy, and expand access to veterinary care.

Report Segmentation & Scope

This report segments the veterinary market by service type (Surgery, Diagnostic Tests and Imaging, Physical Health Monitoring, Other Services) and animal type (Companion Animal, Farm Animal). Each segment's growth projections, market sizes, and competitive dynamics are analyzed, providing a detailed understanding of the market's structure and trends.

Key Drivers of Veterinary Industry Growth

Several key factors drive growth in the veterinary industry. These include technological advancements leading to improved diagnostics and treatments, rising pet ownership rates and increased humanization of pets, and growing consumer spending on pet healthcare, fueled by rising disposable incomes and increased awareness of animal welfare. Furthermore, supportive government policies and initiatives, such as the launch of mobile veterinary clinics in certain regions (as seen with the Andhra Pradesh initiative), also contribute to enhanced market access and growth.

Challenges in the Veterinary Industry Sector

Challenges within the veterinary industry include high costs of advanced diagnostic equipment and treatments, which could create barriers to access for some pet owners. Supply chain disruptions for veterinary pharmaceuticals and medical devices can also impact service provision. Increased regulatory scrutiny and competition among established and emerging players further pose challenges to market participants.

Leading Players in the Veterinary Industry Market

- CVS Group PLC

- Elanco

- FirstVet AB

- Elekta

- Zoetis

- CityVet Inc

- Kremer Veterinary Services

- Ethos Veterinary Health

- Torigen Pharmaceuticals Inc

- Karyopharm Therapeutics Inc

- ELIAS Animal Health

- Greencross Limited

- Armor Animal Health (Animart)

- Mars Inc

- Idexx laboratories

Key Developments in Veterinary Industry Sector

- May 2022: Launch of 175 Mobile Ambulatory Veterinary Clinics (MAVCs) in Andhra Pradesh, India, with a planned expansion to 340 clinics. This initiative significantly improves access to veterinary services in underserved rural areas.

- March 2022: Hacarus Inc. and DS Pharma Animal Health launched an ECG platform for early detection of canine cardiac disease. This innovative technology improves diagnostic capabilities and potentially improves treatment outcomes.

Strategic Veterinary Industry Market Outlook

The veterinary industry presents a promising outlook, with sustained growth anticipated due to continued technological advancements, rising pet ownership, and increasing consumer spending. Strategic opportunities exist for companies focused on innovation, expansion into emerging markets, and the development of integrated veterinary healthcare solutions combining advanced diagnostics, therapeutics, and telehealth capabilities. The ongoing integration of technology and data analytics will further transform the industry, paving the way for personalized medicine and preventive care strategies.

Veterinary Industry Segmentation

-

1. Service

- 1.1. Surgery

- 1.2. Diagnostic Tests and Imaging

- 1.3. Physical Health Monitoring

- 1.4. Other Services

-

2. Animal Type

- 2.1. Companion Animal

- 2.2. Farm Animal

Veterinary Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Veterinary Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.90% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Prevalence of Various Diseases in Animals; Rising Adoption of Animals; Growing Expenditure on Animals/Pets

- 3.3. Market Restrains

- 3.3.1. Shortage of Skilled Personnel; Increasing Cost of Veterinary Services

- 3.4. Market Trends

- 3.4.1. The Companion Animal Segment is Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Surgery

- 5.1.2. Diagnostic Tests and Imaging

- 5.1.3. Physical Health Monitoring

- 5.1.4. Other Services

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Companion Animal

- 5.2.2. Farm Animal

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. North America Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Surgery

- 6.1.2. Diagnostic Tests and Imaging

- 6.1.3. Physical Health Monitoring

- 6.1.4. Other Services

- 6.2. Market Analysis, Insights and Forecast - by Animal Type

- 6.2.1. Companion Animal

- 6.2.2. Farm Animal

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Europe Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Service

- 7.1.1. Surgery

- 7.1.2. Diagnostic Tests and Imaging

- 7.1.3. Physical Health Monitoring

- 7.1.4. Other Services

- 7.2. Market Analysis, Insights and Forecast - by Animal Type

- 7.2.1. Companion Animal

- 7.2.2. Farm Animal

- 7.1. Market Analysis, Insights and Forecast - by Service

- 8. Asia Pacific Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Service

- 8.1.1. Surgery

- 8.1.2. Diagnostic Tests and Imaging

- 8.1.3. Physical Health Monitoring

- 8.1.4. Other Services

- 8.2. Market Analysis, Insights and Forecast - by Animal Type

- 8.2.1. Companion Animal

- 8.2.2. Farm Animal

- 8.1. Market Analysis, Insights and Forecast - by Service

- 9. Middle East and Africa Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Service

- 9.1.1. Surgery

- 9.1.2. Diagnostic Tests and Imaging

- 9.1.3. Physical Health Monitoring

- 9.1.4. Other Services

- 9.2. Market Analysis, Insights and Forecast - by Animal Type

- 9.2.1. Companion Animal

- 9.2.2. Farm Animal

- 9.1. Market Analysis, Insights and Forecast - by Service

- 10. South America Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Service

- 10.1.1. Surgery

- 10.1.2. Diagnostic Tests and Imaging

- 10.1.3. Physical Health Monitoring

- 10.1.4. Other Services

- 10.2. Market Analysis, Insights and Forecast - by Animal Type

- 10.2.1. Companion Animal

- 10.2.2. Farm Animal

- 10.1. Market Analysis, Insights and Forecast - by Service

- 11. North America Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America Veterinary Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 CVS Group PLC

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Elanco

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 FirstVet AB

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Elekta*List Not Exhaustive

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Zoetis

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 CityVet Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Kremer Veterinary Services

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Ethos Veterinary Health

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Torigen Pharmaceuticals Inc

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Karyopharm Therapeutics Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 ELIAS Animal Health

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Greencross Limited

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Armor Animal Health (Animart)

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Mars Inc

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 Idexx laboratories

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.1 CVS Group PLC

List of Figures

- Figure 1: Global Veterinary Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Veterinary Industry Revenue (Million), by Service 2024 & 2032

- Figure 13: North America Veterinary Industry Revenue Share (%), by Service 2024 & 2032

- Figure 14: North America Veterinary Industry Revenue (Million), by Animal Type 2024 & 2032

- Figure 15: North America Veterinary Industry Revenue Share (%), by Animal Type 2024 & 2032

- Figure 16: North America Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Veterinary Industry Revenue (Million), by Service 2024 & 2032

- Figure 19: Europe Veterinary Industry Revenue Share (%), by Service 2024 & 2032

- Figure 20: Europe Veterinary Industry Revenue (Million), by Animal Type 2024 & 2032

- Figure 21: Europe Veterinary Industry Revenue Share (%), by Animal Type 2024 & 2032

- Figure 22: Europe Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Veterinary Industry Revenue (Million), by Service 2024 & 2032

- Figure 25: Asia Pacific Veterinary Industry Revenue Share (%), by Service 2024 & 2032

- Figure 26: Asia Pacific Veterinary Industry Revenue (Million), by Animal Type 2024 & 2032

- Figure 27: Asia Pacific Veterinary Industry Revenue Share (%), by Animal Type 2024 & 2032

- Figure 28: Asia Pacific Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa Veterinary Industry Revenue (Million), by Service 2024 & 2032

- Figure 31: Middle East and Africa Veterinary Industry Revenue Share (%), by Service 2024 & 2032

- Figure 32: Middle East and Africa Veterinary Industry Revenue (Million), by Animal Type 2024 & 2032

- Figure 33: Middle East and Africa Veterinary Industry Revenue Share (%), by Animal Type 2024 & 2032

- Figure 34: Middle East and Africa Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa Veterinary Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: South America Veterinary Industry Revenue (Million), by Service 2024 & 2032

- Figure 37: South America Veterinary Industry Revenue Share (%), by Service 2024 & 2032

- Figure 38: South America Veterinary Industry Revenue (Million), by Animal Type 2024 & 2032

- Figure 39: South America Veterinary Industry Revenue Share (%), by Animal Type 2024 & 2032

- Figure 40: South America Veterinary Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: South America Veterinary Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Veterinary Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Veterinary Industry Revenue Million Forecast, by Service 2019 & 2032

- Table 3: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 4: Global Veterinary Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Germany Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Australia Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Asia Pacific Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: GCC Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Africa Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East and Africa Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Brazil Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Argentina Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of South America Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Veterinary Industry Revenue Million Forecast, by Service 2019 & 2032

- Table 32: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 33: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United States Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Canada Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Mexico Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Veterinary Industry Revenue Million Forecast, by Service 2019 & 2032

- Table 38: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 39: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 40: Germany Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: United Kingdom Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: France Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Italy Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Spain Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Rest of Europe Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global Veterinary Industry Revenue Million Forecast, by Service 2019 & 2032

- Table 47: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 48: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 49: China Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Japan Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: India Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Australia Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: South Korea Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Rest of Asia Pacific Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Global Veterinary Industry Revenue Million Forecast, by Service 2019 & 2032

- Table 56: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 57: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: GCC Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: South Africa Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Rest of Middle East and Africa Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Global Veterinary Industry Revenue Million Forecast, by Service 2019 & 2032

- Table 62: Global Veterinary Industry Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 63: Global Veterinary Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 64: Brazil Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Argentina Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Rest of South America Veterinary Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Industry?

The projected CAGR is approximately 4.90%.

2. Which companies are prominent players in the Veterinary Industry?

Key companies in the market include CVS Group PLC, Elanco, FirstVet AB, Elekta*List Not Exhaustive, Zoetis, CityVet Inc, Kremer Veterinary Services, Ethos Veterinary Health, Torigen Pharmaceuticals Inc, Karyopharm Therapeutics Inc, ELIAS Animal Health, Greencross Limited, Armor Animal Health (Animart), Mars Inc, Idexx laboratories.

3. What are the main segments of the Veterinary Industry?

The market segments include Service, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 122.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Various Diseases in Animals; Rising Adoption of Animals; Growing Expenditure on Animals/Pets.

6. What are the notable trends driving market growth?

The Companion Animal Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Shortage of Skilled Personnel; Increasing Cost of Veterinary Services.

8. Can you provide examples of recent developments in the market?

May 2022: The Chief Minister of Andhra Pradesh, Sri YS Jagan Mohan Reddy, officially launched 175 Mobile Ambulatory Veterinary Clinics (MAVCs) with an investment of Rs 278 crore. The state government planned to establish 340 Dr. YSR Sanchaara Pasu Aarogya Seva, or Mobile Ambulatory Veterinary Clinics (MAVC), in the state to improve the service delivery system and ensure that the veterinary services provided by the animal husbandry department are more easily accessible to the public.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Industry?

To stay informed about further developments, trends, and reports in the Veterinary Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence