Key Insights

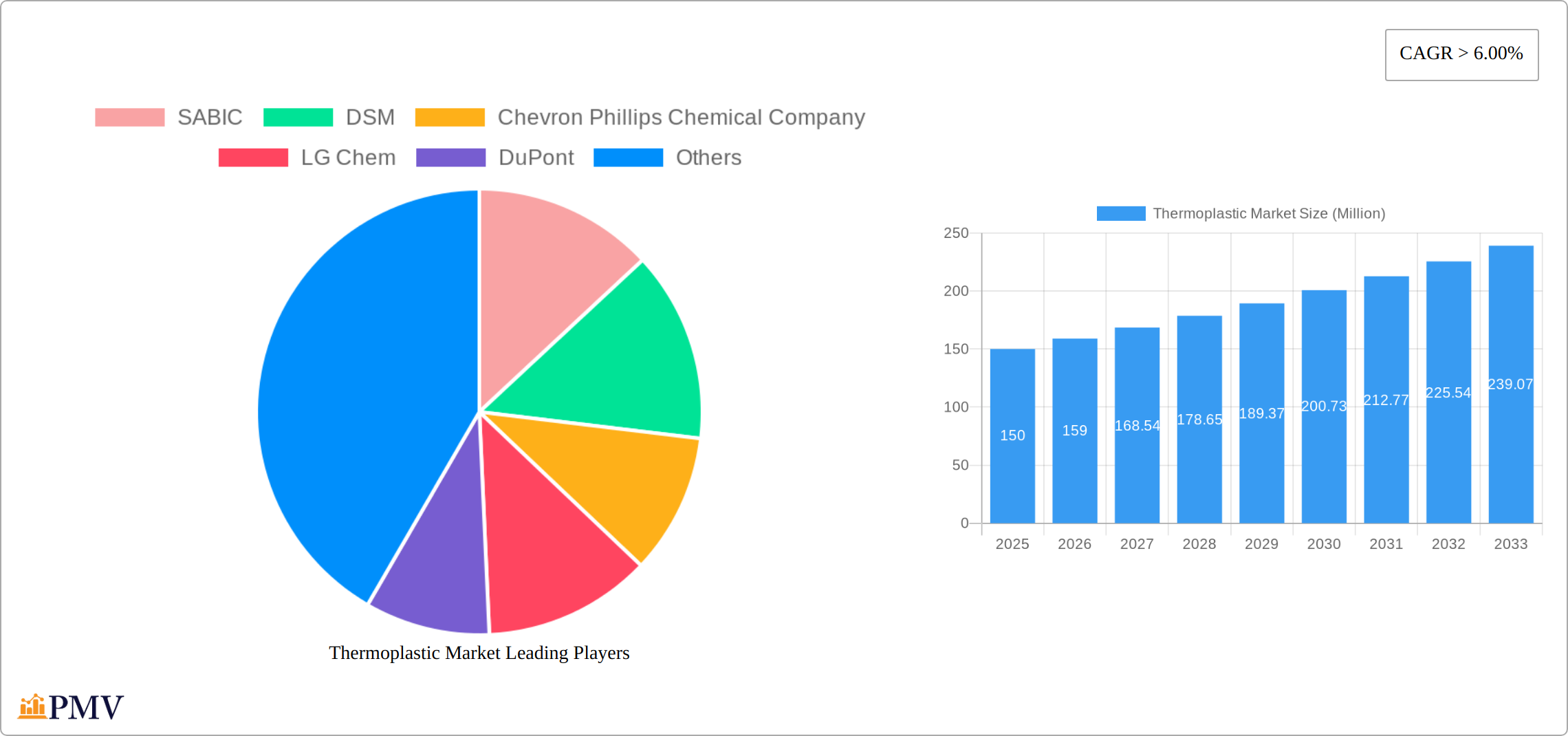

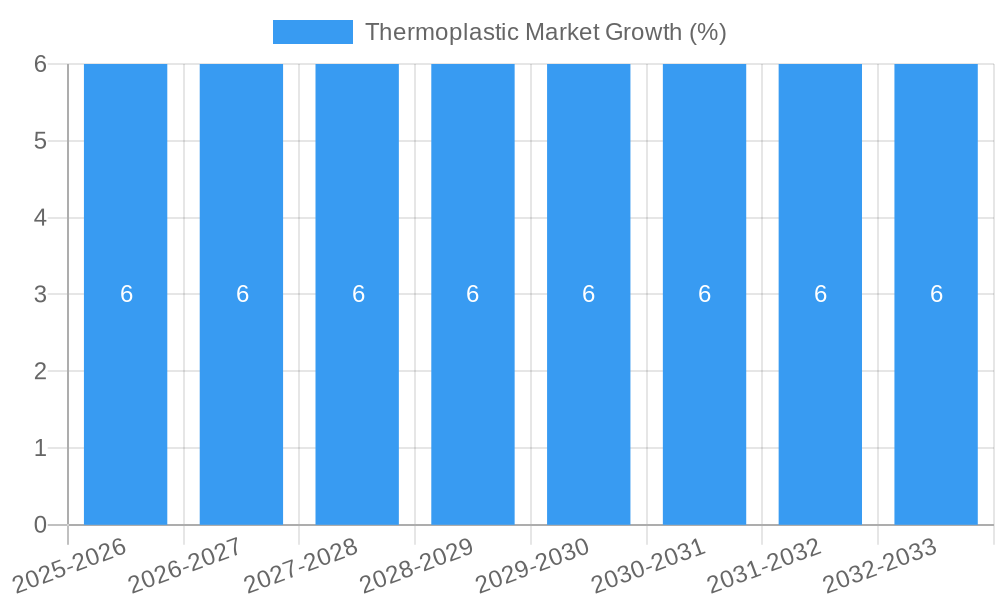

The global thermoplastic market is poised for significant growth, with an estimated market size of $150 billion in 2025 and a projected compound annual growth rate (CAGR) of over 6% from 2025 to 2033. Key drivers of this expansion include the increasing demand for lightweight and durable materials in automotive and transportation sectors, as well as the growing use of thermoplastics in the packaging industry due to their recyclability and cost-effectiveness. Major trends shaping the market include the shift towards high-performance engineering thermoplastics like polyimide (PI) and polystyrene (PS), which offer enhanced thermal and chemical resistance, and the integration of advanced materials in the electrical and electronics industry to meet the needs of modern technology.

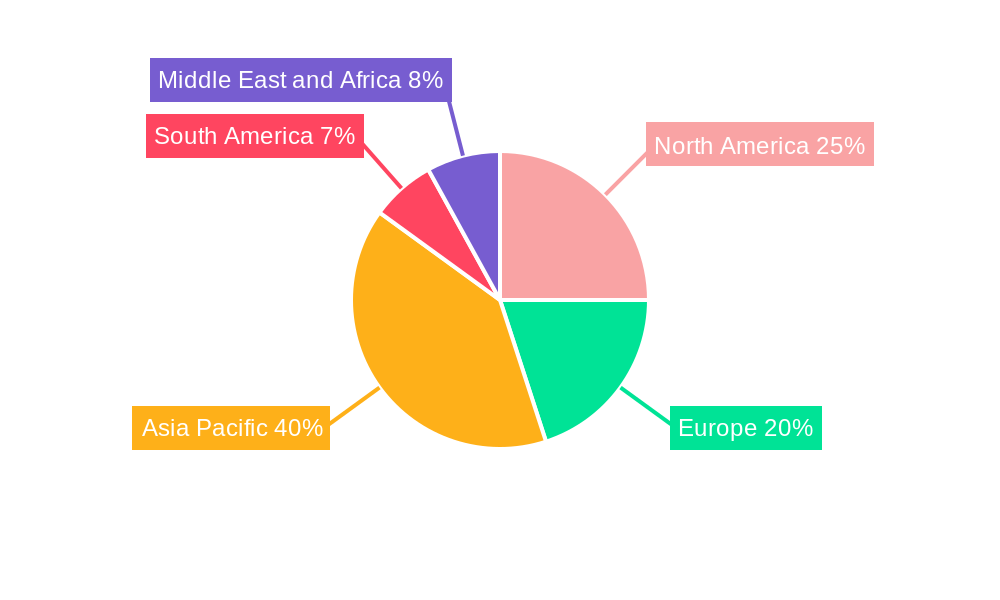

However, the market faces certain restraints such as fluctuating raw material prices and environmental concerns related to plastic waste. Despite these challenges, opportunities abound in segments such as building and construction, where thermoplastics are increasingly used for their versatility and sustainability. Regionally, Asia Pacific, particularly China and India, is expected to lead market growth due to rapid industrialization and urbanization. North America and Europe will also contribute significantly, driven by innovation and the presence of key industry players like SABIC, DSM, and DuPont. The competitive landscape is characterized by strategic collaborations and product innovations aimed at capturing a larger share of the burgeoning thermoplastic market.

Thermoplastic Market Market Structure & Competitive Dynamics

The thermoplastic market is a dynamic landscape shaped by intense competition and a thriving innovation ecosystem. Market concentration remains high, with a handful of multinational corporations dominating the global scene. Key players such as SABIC, DSM, and DuPont hold substantial market share, reflecting the industry's consolidated nature. SABIC, for instance, commands an estimated 15% of the global market. This concentration is further solidified by robust mergers and acquisitions (M&A) activity, exemplified by LyondellBasell's acquisition of A. Schulman for $2.25 billion in 2018. These strategic moves aim to broaden product portfolios, expand geographical reach, and enhance competitive positioning.

Driving innovation are significant R&D investments focused on developing high-performance and sustainable thermoplastic materials. This commitment to innovation is crucial in responding to evolving end-user demands and stringent regulatory frameworks, particularly within regions like Europe and North America. While emerging alternatives, including thermosets and bioplastics, are gaining traction, thermoplastics continue to hold a dominant position due to their versatility, cost-effectiveness, and established infrastructure. The competitive landscape is further nuanced by strategic alliances and collaborative partnerships, fostering technological advancements and facilitating market penetration into new and existing sectors.

End-user trends reveal a strong preference for sustainable and lightweight materials, especially within the rapidly growing automotive and electronics industries. These sectors are demanding high-performance thermoplastics that meet stringent performance and environmental criteria. The overall market dynamics are complex, reflecting the interplay of technological advancements, regulatory pressures, and shifting consumer preferences towards sustainable solutions.

- Market Concentration: Highly concentrated, with major players holding significant market share.

- Innovation Ecosystem: Robust R&D investment driving advancements in high-performance and sustainable materials.

- Regulatory Landscape: Stringent environmental regulations in key markets are accelerating the adoption of sustainable practices.

- Substitute Materials: Thermosets and bioplastics present competitive alternatives, but thermoplastics maintain market dominance.

- End-User Trends: Strong demand for sustainable and lightweight materials in key sectors such as automotive and electronics.

- M&A Activity: Significant consolidation through mergers and acquisitions, impacting market structure and competition.

- Strategic Alliances: Collaborative partnerships are facilitating technological advancements and market expansion.

Thermoplastic Market Industry Trends & Insights

The Thermoplastic Market is witnessing robust growth, driven by a compound annual growth rate (CAGR) of approximately 6% from 2025 to 2033. Technological disruptions are playing a pivotal role in shaping the industry, with advancements in polymer science leading to the development of high-performance thermoplastics that cater to specialized applications in aerospace, automotive, and electronics sectors. Consumer preferences are shifting towards eco-friendly materials, which has spurred the development of bio-based thermoplastics. This trend is particularly evident in Europe, where environmental regulations are stringent, and consumers are increasingly aware of sustainability.

Competitive dynamics are intense, with companies like SABIC and DuPont continuously innovating to maintain their market positions. The market penetration of thermoplastics in emerging economies like India and China is accelerating, driven by rapid industrialization and infrastructure development. The automotive sector remains a key growth driver, with thermoplastics being used to manufacture lightweight components that improve fuel efficiency. Additionally, the electrical and electronics industry is leveraging thermoplastics for their excellent insulation properties and durability.

The rise of 3D printing technologies has also opened new avenues for thermoplastics, allowing for rapid prototyping and customized production. This has led to increased market penetration in niche markets such as medical devices and consumer goods. The industry is also benefiting from the trend towards circular economy principles, with companies investing in recycling technologies to enhance the sustainability of their products. Overall, the Thermoplastic Market is poised for continued growth, supported by technological advancements, regulatory support, and evolving consumer demands.

Dominant Markets & Segments in Thermoplastic Market

The Thermoplastic Market showcases dominance across various segments and regions. In terms of product types, Polyimide (PI) and other high-performance engineering thermoplastics like PPE, PSU, PEI, PPS, ETFE, PFA, FEP, and PBI are leading due to their superior thermal and chemical resistance properties. These materials are particularly dominant in industries requiring high-performance materials, such as aerospace and electronics.

- Economic Policies: Favorable policies in regions like Asia-Pacific are driving growth in thermoplastic use.

- Infrastructure: Rapid infrastructure development in emerging markets like China and India boosts demand.

The end-user industry segment where thermoplastics dominate includes packaging, building and construction, and automotive and transportation. The automotive sector's dominance is fueled by the need for lightweight materials that enhance fuel efficiency. Thermoplastics like Commodity Thermoplastics and Polystyrene (PS) are widely used in packaging due to their cost-effectiveness and versatility.

- Packaging: Dominated by Commodity Thermoplastics due to their affordability and versatility.

- Automotive and Transportation: High demand for lightweight materials to improve fuel efficiency.

- Building and Construction: Thermoplastics are used for their durability and ease of processing.

In terms of geographical dominance, Asia-Pacific leads the Thermoplastic Market, driven by rapid industrialization and urbanization in countries like China and India. The region's economic policies, such as incentives for green technologies, are further propelling the market. Europe follows closely, with a focus on sustainability and high-performance applications in automotive and electronics.

- Asia-Pacific: Dominates due to rapid industrialization and favorable economic policies.

- Europe: Focus on sustainability and high-performance applications.

The dominance of these segments and regions is attributed to a combination of economic policies, infrastructure development, and specific industry needs. The market's growth is further supported by continuous innovation and strategic investments in R&D by key players.

Thermoplastic Market Product Innovations

Product innovations in the Thermoplastic Market are driven by technological advancements and the need for materials that meet specific industry requirements. Recent developments include SABIC's introduction of EXTEM™ and ULTEM™ thermo-optical resins, designed for advanced optical components in the electronics sector. These innovations support industry trends like co-packaged optics and single-mode fiber optic systems. Arkema's investment in increasing Pebax elastomer production capacity, including bio-circular Pebax Rnew, reflects a focus on sustainable materials. These product developments not only enhance competitive advantages but also align well with market demands for high-performance and eco-friendly thermoplastics.

Report Segmentation & Scope

The Thermoplastic Market report is segmented into various categories to provide a comprehensive analysis of market dynamics and growth potential.

Polyimide (PI) and Other Product Types (PPE, PSU, PEI, PPS, ETFE, PFA, FEP, PBI): These high-performance engineering thermoplastics are expected to grow at a CAGR of 7% from 2025 to 2033, driven by their use in aerospace and electronics. The market size for these segments is projected to reach $xx Million by 2033.

End-user Industry: The packaging segment is the largest, with a market size of $xx Million in 2025, expected to grow at a CAGR of 5%. Building and construction, automotive and transportation, and electrical and electronics are also significant, with growth rates of 6%, 7%, and 8% respectively. The medical and sports and leisure segments are niche but growing rapidly due to specialized applications.

Product Type: Commodity Thermoplastics are the most widely used, with a market size of $xx Million in 2025, expected to grow at a CAGR of 4%. Engineering Thermoplastics like Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN) and High-performance Engineering Thermoplastics are growing at a higher rate due to their specialized applications.

The competitive dynamics within these segments are intense, with companies like SABIC, DuPont, and Arkema leading in innovation and market share.

Key Drivers of Thermoplastic Market Growth

The Thermoplastic Market is propelled by several key drivers. Technological advancements in polymer science are enabling the development of high-performance materials that cater to specialized industries like aerospace and automotive. Economic factors, such as rapid industrialization in emerging economies, are increasing demand for thermoplastics in construction and packaging. Regulatory support for sustainable materials is driving the adoption of bio-based thermoplastics, particularly in Europe. These drivers collectively contribute to the market's robust growth trajectory.

Challenges in the Thermoplastic Market Sector

The Thermoplastic Market faces several challenges that could impede growth. Regulatory hurdles, particularly in regions with stringent environmental standards, can increase production costs and limit market expansion. Supply chain disruptions, exacerbated by global events like pandemics, pose significant risks to raw material availability and pricing. Competitive pressures are intense, with companies constantly needing to innovate to maintain market share. These challenges have quantifiable impacts, such as a potential 2-3% reduction in annual growth rate due to supply chain issues.

Leading Players in the Thermoplastic Market Market

- SABIC

- DSM

- Chevron Phillips Chemical Company

- LG Chem

- DuPont

- Arkema

- Eastman Chemical Company

- Daicel Corporation

- Mitsubishi Engineering-Plastics Corporation

- TEIJIN LIMITED

- Asahi Kasei Corporation

- INEOS AG

- Solvay

- Covestro AG

- Celanese Corporation

- Evonik Industries AG

- LyondellBasell Industries Holdings BV (incl A Schulman Inc)

- Polyplastics Co Ltd

- LANXESS

- 3M (incl Dyneon LLC)

- BASF SE

Key Developments in Thermoplastic Market Sector

- January 2023: SABIC announced that it will showcase its newest thermoplastic materials, known as EXTEM™ and ULTEM™ thermo-optical resins, well-suited for advanced optical components that support top industry trends, such as the migration to co-packaged optics and single-mode fiber optic systems at Photonics West 2023, at booth #5512. This development enhances SABIC's position in the high-performance thermoplastics market.

- January 2022: Arkema announced a 25% increase in its global Pebax elastomer production capacity by investing in Serquigny in France. This investment will notably enable increased production of the bio-circular Pebax, Rnew, and traditional Pebax ranges, aligning with the market's shift towards sustainable materials.

Strategic Thermoplastic Market Market Outlook

The Thermoplastic Market's strategic outlook is promising, with significant growth accelerators on the horizon. The increasing demand for lightweight and durable materials in the automotive and aerospace sectors will continue to drive market expansion. Technological advancements in 3D printing and sustainable materials are opening new avenues for innovation and market penetration. Strategic opportunities lie in the development of bio-based and recycled thermoplastics, aligning with global sustainability goals. The market's future potential is further bolstered by the ongoing industrialization in emerging economies and the continuous need for high-performance materials across various industries.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

Thermoplastic Market Segmentation

-

1. Product Type

-

1.1. Commodity Thermoplastics

- 1.1.1. Polyethylene (PE)

- 1.1.2. Polypropylene (PP)

- 1.1.3. Polyvinyl chloride (PVC)

- 1.1.4. Polystyrene (PS)

-

1.2. Engineering Thermoplastics

- 1.2.1. Polyamide (PA)

- 1.2.2. Polycarbonates (PC)

- 1.2.3. Polymethyl methacrylate (PMMA)

- 1.2.4. Polyoxymethylene (POM)

- 1.2.5. Polyethylene terephthalate (PET)

- 1.2.6. Polybutylene terephthalate (PBT)

- 1.2.7. Acryloni

-

1.3. High-performance Engineering Thermoplastics

- 1.3.1. Polyether Ether Ketone (PEEK)

- 1.3.2. Liquid Crystal Polymer (LCP)

- 1.3.3. Polytetrafluoroethylene (PTFE)

- 1.3.4. Polyimide (PI)

- 1.4. Other Pr

-

1.1. Commodity Thermoplastics

-

2. End-user Industry

- 2.1. Packaging

- 2.2. Building and Construction

- 2.3. Automotive and Transportation

- 2.4. Electrical and Electronics

- 2.5. Sports and Leisure

- 2.6. Medical

- 2.7. Other En

Thermoplastic Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Thermoplastic Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 6.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rapid Increase in Downstream Processing Capacity Additions; Growing Consumer Goods and Eelctronics Industries

- 3.3. Market Restrains

- 3.3.1. Environmental Concerns Related to thermoplastics; Other Restraints

- 3.4. Market Trends

- 3.4.1. Increasing Demand from Automotive and Transportation

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Commodity Thermoplastics

- 5.1.1.1. Polyethylene (PE)

- 5.1.1.2. Polypropylene (PP)

- 5.1.1.3. Polyvinyl chloride (PVC)

- 5.1.1.4. Polystyrene (PS)

- 5.1.2. Engineering Thermoplastics

- 5.1.2.1. Polyamide (PA)

- 5.1.2.2. Polycarbonates (PC)

- 5.1.2.3. Polymethyl methacrylate (PMMA)

- 5.1.2.4. Polyoxymethylene (POM)

- 5.1.2.5. Polyethylene terephthalate (PET)

- 5.1.2.6. Polybutylene terephthalate (PBT)

- 5.1.2.7. Acryloni

- 5.1.3. High-performance Engineering Thermoplastics

- 5.1.3.1. Polyether Ether Ketone (PEEK)

- 5.1.3.2. Liquid Crystal Polymer (LCP)

- 5.1.3.3. Polytetrafluoroethylene (PTFE)

- 5.1.3.4. Polyimide (PI)

- 5.1.4. Other Pr

- 5.1.1. Commodity Thermoplastics

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Packaging

- 5.2.2. Building and Construction

- 5.2.3. Automotive and Transportation

- 5.2.4. Electrical and Electronics

- 5.2.5. Sports and Leisure

- 5.2.6. Medical

- 5.2.7. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Asia Pacific Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Commodity Thermoplastics

- 6.1.1.1. Polyethylene (PE)

- 6.1.1.2. Polypropylene (PP)

- 6.1.1.3. Polyvinyl chloride (PVC)

- 6.1.1.4. Polystyrene (PS)

- 6.1.2. Engineering Thermoplastics

- 6.1.2.1. Polyamide (PA)

- 6.1.2.2. Polycarbonates (PC)

- 6.1.2.3. Polymethyl methacrylate (PMMA)

- 6.1.2.4. Polyoxymethylene (POM)

- 6.1.2.5. Polyethylene terephthalate (PET)

- 6.1.2.6. Polybutylene terephthalate (PBT)

- 6.1.2.7. Acryloni

- 6.1.3. High-performance Engineering Thermoplastics

- 6.1.3.1. Polyether Ether Ketone (PEEK)

- 6.1.3.2. Liquid Crystal Polymer (LCP)

- 6.1.3.3. Polytetrafluoroethylene (PTFE)

- 6.1.3.4. Polyimide (PI)

- 6.1.4. Other Pr

- 6.1.1. Commodity Thermoplastics

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Packaging

- 6.2.2. Building and Construction

- 6.2.3. Automotive and Transportation

- 6.2.4. Electrical and Electronics

- 6.2.5. Sports and Leisure

- 6.2.6. Medical

- 6.2.7. Other En

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Commodity Thermoplastics

- 7.1.1.1. Polyethylene (PE)

- 7.1.1.2. Polypropylene (PP)

- 7.1.1.3. Polyvinyl chloride (PVC)

- 7.1.1.4. Polystyrene (PS)

- 7.1.2. Engineering Thermoplastics

- 7.1.2.1. Polyamide (PA)

- 7.1.2.2. Polycarbonates (PC)

- 7.1.2.3. Polymethyl methacrylate (PMMA)

- 7.1.2.4. Polyoxymethylene (POM)

- 7.1.2.5. Polyethylene terephthalate (PET)

- 7.1.2.6. Polybutylene terephthalate (PBT)

- 7.1.2.7. Acryloni

- 7.1.3. High-performance Engineering Thermoplastics

- 7.1.3.1. Polyether Ether Ketone (PEEK)

- 7.1.3.2. Liquid Crystal Polymer (LCP)

- 7.1.3.3. Polytetrafluoroethylene (PTFE)

- 7.1.3.4. Polyimide (PI)

- 7.1.4. Other Pr

- 7.1.1. Commodity Thermoplastics

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Packaging

- 7.2.2. Building and Construction

- 7.2.3. Automotive and Transportation

- 7.2.4. Electrical and Electronics

- 7.2.5. Sports and Leisure

- 7.2.6. Medical

- 7.2.7. Other En

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Commodity Thermoplastics

- 8.1.1.1. Polyethylene (PE)

- 8.1.1.2. Polypropylene (PP)

- 8.1.1.3. Polyvinyl chloride (PVC)

- 8.1.1.4. Polystyrene (PS)

- 8.1.2. Engineering Thermoplastics

- 8.1.2.1. Polyamide (PA)

- 8.1.2.2. Polycarbonates (PC)

- 8.1.2.3. Polymethyl methacrylate (PMMA)

- 8.1.2.4. Polyoxymethylene (POM)

- 8.1.2.5. Polyethylene terephthalate (PET)

- 8.1.2.6. Polybutylene terephthalate (PBT)

- 8.1.2.7. Acryloni

- 8.1.3. High-performance Engineering Thermoplastics

- 8.1.3.1. Polyether Ether Ketone (PEEK)

- 8.1.3.2. Liquid Crystal Polymer (LCP)

- 8.1.3.3. Polytetrafluoroethylene (PTFE)

- 8.1.3.4. Polyimide (PI)

- 8.1.4. Other Pr

- 8.1.1. Commodity Thermoplastics

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Packaging

- 8.2.2. Building and Construction

- 8.2.3. Automotive and Transportation

- 8.2.4. Electrical and Electronics

- 8.2.5. Sports and Leisure

- 8.2.6. Medical

- 8.2.7. Other En

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. South America Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Commodity Thermoplastics

- 9.1.1.1. Polyethylene (PE)

- 9.1.1.2. Polypropylene (PP)

- 9.1.1.3. Polyvinyl chloride (PVC)

- 9.1.1.4. Polystyrene (PS)

- 9.1.2. Engineering Thermoplastics

- 9.1.2.1. Polyamide (PA)

- 9.1.2.2. Polycarbonates (PC)

- 9.1.2.3. Polymethyl methacrylate (PMMA)

- 9.1.2.4. Polyoxymethylene (POM)

- 9.1.2.5. Polyethylene terephthalate (PET)

- 9.1.2.6. Polybutylene terephthalate (PBT)

- 9.1.2.7. Acryloni

- 9.1.3. High-performance Engineering Thermoplastics

- 9.1.3.1. Polyether Ether Ketone (PEEK)

- 9.1.3.2. Liquid Crystal Polymer (LCP)

- 9.1.3.3. Polytetrafluoroethylene (PTFE)

- 9.1.3.4. Polyimide (PI)

- 9.1.4. Other Pr

- 9.1.1. Commodity Thermoplastics

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Packaging

- 9.2.2. Building and Construction

- 9.2.3. Automotive and Transportation

- 9.2.4. Electrical and Electronics

- 9.2.5. Sports and Leisure

- 9.2.6. Medical

- 9.2.7. Other En

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Commodity Thermoplastics

- 10.1.1.1. Polyethylene (PE)

- 10.1.1.2. Polypropylene (PP)

- 10.1.1.3. Polyvinyl chloride (PVC)

- 10.1.1.4. Polystyrene (PS)

- 10.1.2. Engineering Thermoplastics

- 10.1.2.1. Polyamide (PA)

- 10.1.2.2. Polycarbonates (PC)

- 10.1.2.3. Polymethyl methacrylate (PMMA)

- 10.1.2.4. Polyoxymethylene (POM)

- 10.1.2.5. Polyethylene terephthalate (PET)

- 10.1.2.6. Polybutylene terephthalate (PBT)

- 10.1.2.7. Acryloni

- 10.1.3. High-performance Engineering Thermoplastics

- 10.1.3.1. Polyether Ether Ketone (PEEK)

- 10.1.3.2. Liquid Crystal Polymer (LCP)

- 10.1.3.3. Polytetrafluoroethylene (PTFE)

- 10.1.3.4. Polyimide (PI)

- 10.1.4. Other Pr

- 10.1.1. Commodity Thermoplastics

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Packaging

- 10.2.2. Building and Construction

- 10.2.3. Automotive and Transportation

- 10.2.4. Electrical and Electronics

- 10.2.5. Sports and Leisure

- 10.2.6. Medical

- 10.2.7. Other En

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Asia Pacific Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 China

- 11.1.2 India

- 11.1.3 Japan

- 11.1.4 South Korea

- 11.1.5 Rest of Asia Pacific

- 12. North America Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United States

- 12.1.2 Canada

- 12.1.3 Mexico

- 13. Europe Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 Germany

- 13.1.2 United Kingdom

- 13.1.3 France

- 13.1.4 Italy

- 13.1.5 Rest of Europe

- 14. South America Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 Brazil

- 14.1.2 Argentina

- 14.1.3 Rest of South America

- 15. Middle East and Africa Thermoplastic Market Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Saudi Arabia

- 15.1.2 South Africa

- 15.1.3 Rest of Middle East and Africa

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 SABIC

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 DSM

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Chevron Phillips Chemical Company

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 LG Chem

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 DuPont

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Arkema

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Eastman Chemical Company

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Daicel Corporation

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Mitsubishi Engineering-Plastics Corporation

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 TEIJIN LIMITED*List Not Exhaustive

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Asahi Kasei Corporation

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 INEOS AG

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Solvay

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Covestro AG

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 Celanese Corporation

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.16 Evonik Industries AG

- 16.2.16.1. Overview

- 16.2.16.2. Products

- 16.2.16.3. SWOT Analysis

- 16.2.16.4. Recent Developments

- 16.2.16.5. Financials (Based on Availability)

- 16.2.17 LyondellBasell Industries Holdings BV (incl A Schulman Inc )

- 16.2.17.1. Overview

- 16.2.17.2. Products

- 16.2.17.3. SWOT Analysis

- 16.2.17.4. Recent Developments

- 16.2.17.5. Financials (Based on Availability)

- 16.2.18 Polyplastics Co Ltd

- 16.2.18.1. Overview

- 16.2.18.2. Products

- 16.2.18.3. SWOT Analysis

- 16.2.18.4. Recent Developments

- 16.2.18.5. Financials (Based on Availability)

- 16.2.19 LANXESS

- 16.2.19.1. Overview

- 16.2.19.2. Products

- 16.2.19.3. SWOT Analysis

- 16.2.19.4. Recent Developments

- 16.2.19.5. Financials (Based on Availability)

- 16.2.20 3M (incl Dyneon LLC)

- 16.2.20.1. Overview

- 16.2.20.2. Products

- 16.2.20.3. SWOT Analysis

- 16.2.20.4. Recent Developments

- 16.2.20.5. Financials (Based on Availability)

- 16.2.21 BASF SE

- 16.2.21.1. Overview

- 16.2.21.2. Products

- 16.2.21.3. SWOT Analysis

- 16.2.21.4. Recent Developments

- 16.2.21.5. Financials (Based on Availability)

- 16.2.1 SABIC

List of Figures

- Figure 1: Global Thermoplastic Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Asia Pacific Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 3: Asia Pacific Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 5: North America Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 6: Europe Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 7: Europe Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 9: South America Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 12: Asia Pacific Thermoplastic Market Revenue (Million), by Product Type 2024 & 2032

- Figure 13: Asia Pacific Thermoplastic Market Revenue Share (%), by Product Type 2024 & 2032

- Figure 14: Asia Pacific Thermoplastic Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 15: Asia Pacific Thermoplastic Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 16: Asia Pacific Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 17: Asia Pacific Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 18: North America Thermoplastic Market Revenue (Million), by Product Type 2024 & 2032

- Figure 19: North America Thermoplastic Market Revenue Share (%), by Product Type 2024 & 2032

- Figure 20: North America Thermoplastic Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 21: North America Thermoplastic Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 22: North America Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 23: North America Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 24: Europe Thermoplastic Market Revenue (Million), by Product Type 2024 & 2032

- Figure 25: Europe Thermoplastic Market Revenue Share (%), by Product Type 2024 & 2032

- Figure 26: Europe Thermoplastic Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 27: Europe Thermoplastic Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 28: Europe Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 29: Europe Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 30: South America Thermoplastic Market Revenue (Million), by Product Type 2024 & 2032

- Figure 31: South America Thermoplastic Market Revenue Share (%), by Product Type 2024 & 2032

- Figure 32: South America Thermoplastic Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 33: South America Thermoplastic Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 34: South America Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 35: South America Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Thermoplastic Market Revenue (Million), by Product Type 2024 & 2032

- Figure 37: Middle East and Africa Thermoplastic Market Revenue Share (%), by Product Type 2024 & 2032

- Figure 38: Middle East and Africa Thermoplastic Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 39: Middle East and Africa Thermoplastic Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 40: Middle East and Africa Thermoplastic Market Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East and Africa Thermoplastic Market Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Thermoplastic Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Thermoplastic Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: Global Thermoplastic Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Global Thermoplastic Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: India Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Japan Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: South Korea Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of Asia Pacific Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 12: United States Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Canada Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Mexico Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Germany Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: United Kingdom Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Europe Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Brazil Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Argentina Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of South America Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Saudi Arabia Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: South Africa Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Middle East and Africa Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Global Thermoplastic Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 30: Global Thermoplastic Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 31: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 32: China Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: India Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Japan Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: South Korea Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Rest of Asia Pacific Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Thermoplastic Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 38: Global Thermoplastic Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 39: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 40: United States Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Canada Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Mexico Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Global Thermoplastic Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 44: Global Thermoplastic Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 45: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 46: Germany Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: United Kingdom Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: France Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Italy Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Europe Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Global Thermoplastic Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 52: Global Thermoplastic Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 53: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 54: Brazil Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Argentina Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Rest of South America Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: Global Thermoplastic Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 58: Global Thermoplastic Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 59: Global Thermoplastic Market Revenue Million Forecast, by Country 2019 & 2032

- Table 60: Saudi Arabia Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: South Africa Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 62: Rest of Middle East and Africa Thermoplastic Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thermoplastic Market?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the Thermoplastic Market?

Key companies in the market include SABIC, DSM, Chevron Phillips Chemical Company, LG Chem, DuPont, Arkema, Eastman Chemical Company, Daicel Corporation, Mitsubishi Engineering-Plastics Corporation, TEIJIN LIMITED*List Not Exhaustive, Asahi Kasei Corporation, INEOS AG, Solvay, Covestro AG, Celanese Corporation, Evonik Industries AG, LyondellBasell Industries Holdings BV (incl A Schulman Inc ), Polyplastics Co Ltd, LANXESS, 3M (incl Dyneon LLC), BASF SE.

3. What are the main segments of the Thermoplastic Market?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Increase in Downstream Processing Capacity Additions; Growing Consumer Goods and Eelctronics Industries.

6. What are the notable trends driving market growth?

Increasing Demand from Automotive and Transportation.

7. Are there any restraints impacting market growth?

Environmental Concerns Related to thermoplastics; Other Restraints.

8. Can you provide examples of recent developments in the market?

January 2023: SABIC announced that it will showcase its newest thermoplastic materials, known as EXTEM™ and ULTEM™ thermo-optical resins, well-suited for advanced optical components that support top industry trends, such as the migration to co-packaged optics and single-mode fiber optic systems at Photonics West 2023, at booth #5512.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thermoplastic Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thermoplastic Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thermoplastic Market?

To stay informed about further developments, trends, and reports in the Thermoplastic Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence