Key Insights

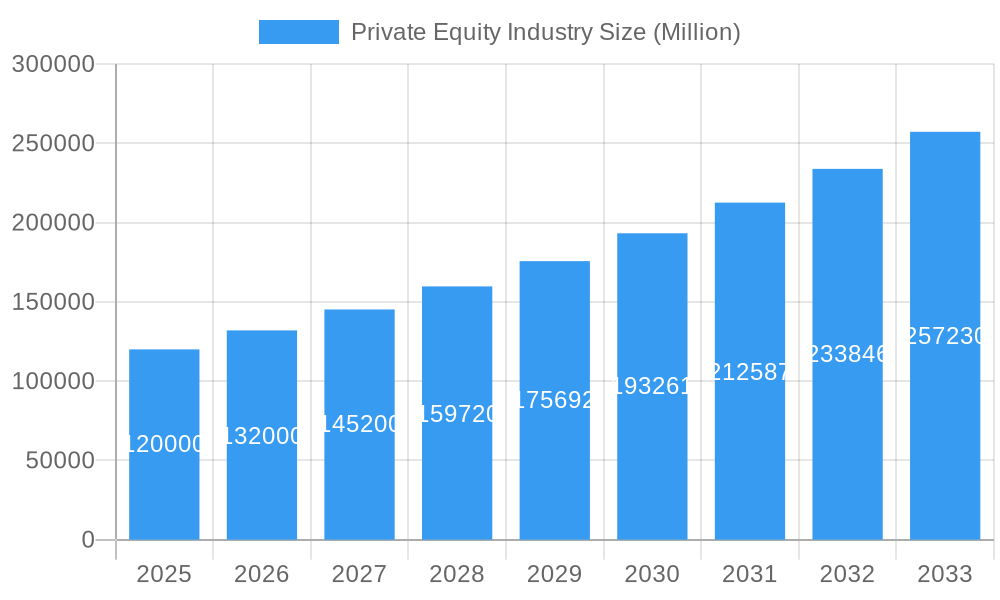

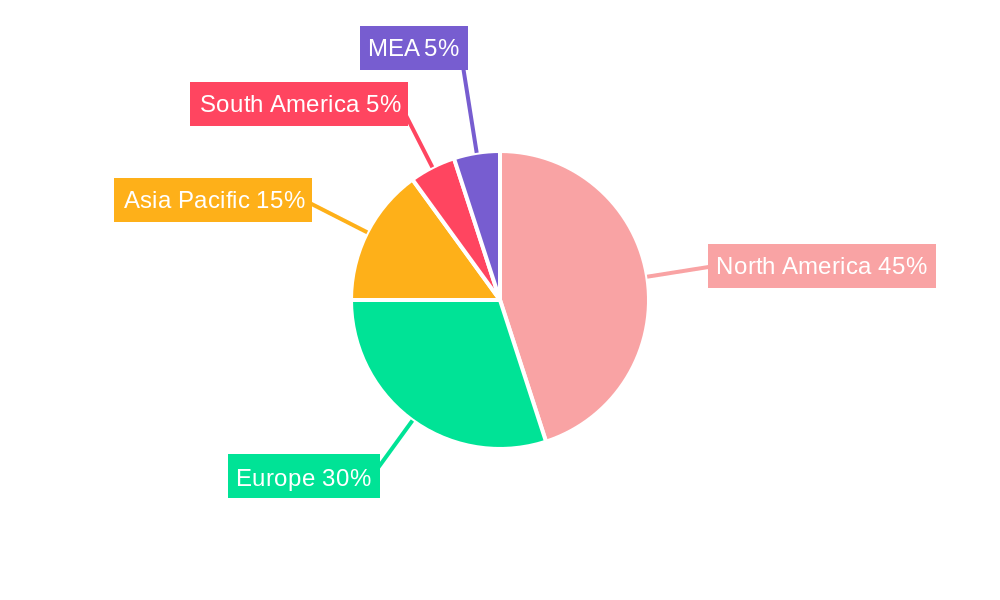

The Private Equity (PE) industry, boasting a market size exceeding $XX million in 2025 and exhibiting a Compound Annual Growth Rate (CAGR) of over 10%, is experiencing robust expansion. This growth is fueled by several key drivers, including increasing institutional investor participation seeking higher returns than traditional asset classes, abundant liquidity in global capital markets, and a favorable regulatory environment in many regions. The trend towards consolidation within industries, driven by technological advancements and evolving consumer preferences, further propels PE investment activity. Significant investments are concentrated in sectors like Technology (Software), Healthcare, and Real Estate, reflecting their high growth potential and resilience to economic downturns. While macroeconomic uncertainties and rising interest rates pose potential restraints, the adaptable nature of PE strategies and the continued search for alpha amongst investors suggest the industry's upward trajectory will likely persist throughout the forecast period (2025-2033). The diverse range of PE strategies, encompassing buyouts, venture capital, real estate, and infrastructure investments across various market caps (Large Cap, Upper Middle Market, Lower Middle Market), underscores the industry's depth and broad appeal. Geographical distribution of investments reveals strong activity in North America and Europe, with Asia-Pacific emerging as a significant and rapidly growing market.

Private Equity Industry Market Size (In Billion)

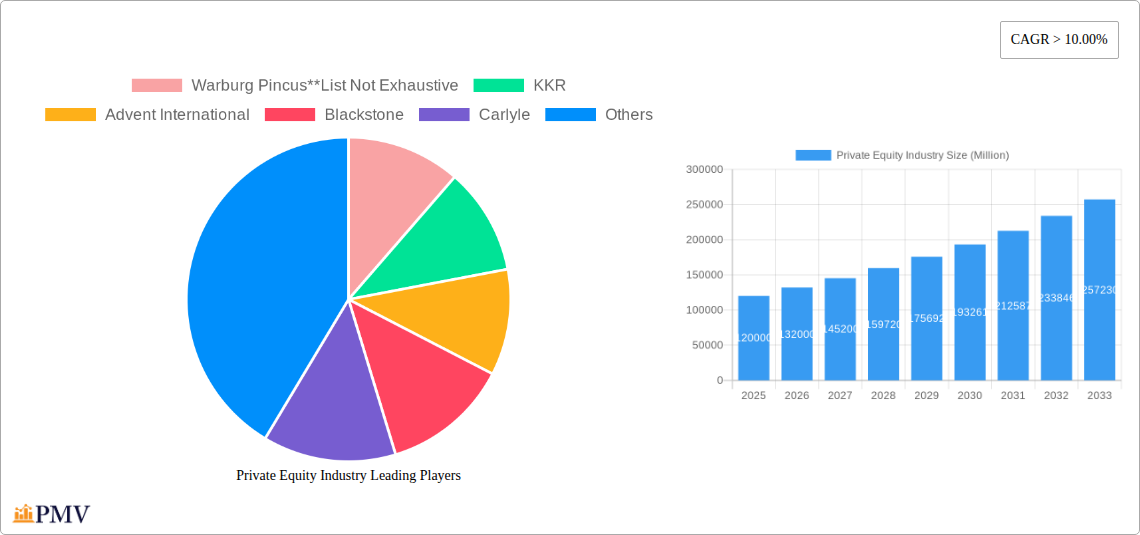

The dominance of established PE giants like Warburg Pincus, KKR, Advent International, Blackstone, Carlyle, and others highlights the competitive landscape. However, the industry also sees increased participation from emerging players, particularly in niche sectors and geographic regions. The forecast period of 2025-2033 anticipates continued expansion, though the exact pace will depend on factors such as global economic conditions, geopolitical stability, and technological disruption. Segmentation by fund type, sector, and investment size offers crucial insights into the market's dynamics, allowing for targeted strategies and investment decisions. While the "Other" segment (Distressed PE, Direct Lending, etc.) represents a significant, albeit less specified, portion of the market, it is expected to contribute substantially to overall growth. The data suggests a strong performance throughout the historical period (2019-2024), providing a robust foundation for future projections.

Private Equity Industry Company Market Share

Private Equity Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the Private Equity industry, covering market structure, competitive dynamics, key trends, dominant segments, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and an estimated and forecast period of 2025-2033, this report offers invaluable insights for investors, industry professionals, and strategic decision-makers. The report leverages extensive data analysis covering Buyout, Venture Capital (VCs), Real Estate, Infrastructure, and other alternative investment strategies, across sectors including Technology, Healthcare, Financial Services, and more. Millions of dollars in deal values and market sizes are analyzed, providing a realistic view of current market conditions and projections.

Private Equity Industry Market Structure & Competitive Dynamics

The Private Equity industry is characterized by a dynamic and evolving market structure. While a select group of large, established firms command significant influence and market share, the landscape is also populated by a diverse and innovative ecosystem of smaller, specialized funds. This dual nature fosters robust competition and drives innovation across deal sourcing, portfolio management, and exit strategies. Global regulatory frameworks are continuously adapting, generally aiming to foster private equity investment while addressing areas like transparency and investor protection. These regulations can vary considerably across different jurisdictions, presenting both opportunities and compliance complexities for market participants. Direct product substitutes for private equity's core function of acquiring, transforming, and divesting businesses are limited. However, other alternative investment vehicles, such as hedge funds and venture capital, compete for investor capital and may offer similar return profiles. End-user demand for private equity investments remains strong, propelled by the ongoing search for alpha in a low-yield environment and the attractive growth prospects offered by private markets. M&A activity is not only a defining characteristic but also a primary engine for value creation and realization within the industry.

- Market Concentration: While a few mega-firms dominate, the top 10 firms represent a substantial portion, approximately XX%, of total global deal value, highlighting the influence of scale.

- M&A Deal Values: In 2024, the total M&A deal value within the private equity sector reached an estimated $XX Billion, with the average deal size hovering around $XX Million, indicating a broad spectrum of transaction sizes.

- Innovation Ecosystems: The industry benefits from a strong and growing presence of specialized firms focusing on niche sectors, emerging technologies, and innovative investment strategies. This fuels continuous advancements in data analytics for deal sourcing, operational improvements in portfolio companies, and sophisticated exit planning.

- Regulatory Frameworks: The patchwork of evolving regulations across key global markets creates a complex operating environment. Firms must navigate diverse compliance requirements, influencing investment strategies, deal structuring, and geographical focus.

Private Equity Industry Industry Trends & Insights

The Private Equity industry is experiencing robust growth, driven by several key factors. Favorable macroeconomic conditions, including low interest rates and abundant liquidity, have fueled investment activity. Technological disruptions, particularly in areas like data analytics and artificial intelligence, are transforming deal sourcing, due diligence, and portfolio management. These advancements allow for more efficient and data-driven decision-making. Shifting consumer preferences toward sustainable and ethical investing have influenced private equity's investment strategies with a greater focus on ESG factors. The competitive landscape remains dynamic, with ongoing consolidation through mergers and acquisitions among private equity firms themselves.

- CAGR: The industry is projected to register a CAGR of xx% during the forecast period (2025-2033).

- Market Penetration: The penetration of private equity investments into various sectors is expected to increase significantly, particularly in technology, healthcare, and renewable energy.

Dominant Markets & Segments in Private Equity Industry

The North American private equity market currently holds the largest market share, driven by a robust economy, abundant capital, and a favorable regulatory environment. Within the sector, the technology (software) and healthcare sectors are showing particularly strong growth. Within fund types, Buyouts and Venture Capital continue to dominate, representing over xx% of total investment volume. Large-cap deals remain prominent, but the upper middle market offers significant opportunities for smaller firms.

Key Drivers (North America):

- Strong entrepreneurial ecosystem

- Availability of capital

- Developed financial infrastructure

- Favorable regulatory environment

Dominant Segments:

- Fund Type: Buyout (xx% market share), Venture Capital (xx% market share)

- Sector: Technology (Software) and Healthcare demonstrate the highest growth rate and investment volume.

- Investments: Large Cap investments account for a substantial majority of the total investment volume.

Private Equity Industry Product Innovations

Recent innovations in the private equity industry focus on enhancing efficiency and effectiveness across the investment lifecycle. Data analytics and artificial intelligence are being leveraged for improved deal sourcing, portfolio monitoring, and risk management. The rise of specialized funds concentrating on specific sectors or strategies reflects a move towards greater focus and expertise. These innovations are driving higher returns and improved portfolio company performance, while also enhancing the value proposition for limited partners.

Report Segmentation & Scope

This comprehensive report offers a granular analysis of the private equity market, segmented across critical dimensions to provide deep insights into its various facets. Each segment is examined for its market size, growth trajectory, and unique competitive dynamics.

- Fund Type: The analysis includes Buyout funds, Venture Capital (VCs), Real Estate funds, Infrastructure funds, and Other specialized strategies such as Distressed Private Equity and Direct Lending. Projections for each fund type's growth, market penetration, and competitive landscape are detailed.

- Sector: We delve into key industries including Technology (with a focus on Software), Healthcare, Real Estate & Services, Financial Services, Industrials, Consumer & Retail, Energy & Power, Media & Entertainment, and Telecommunications, alongside a broad "Others" category encompassing sectors like Transportation. Growth projections are informed by sector-specific trends, technological disruptions, and macroeconomic factors.

- Investments: The report further categorizes the market by investment size and type, analyzing Large Cap, Upper Middle Market, Lower Middle Market, and Real Estate investments. The competitive landscape and market sizing for each investment stratum are meticulously evaluated.

Key Drivers of Private Equity Industry Growth

The sustained and robust growth of the private equity industry is underpinned by a confluence of powerful drivers. Technological advancements are revolutionizing operational efficiencies within portfolio companies and enhancing data-driven decision-making throughout the investment lifecycle. Favorable macroeconomic conditions, characterized by persistently low interest rates and ample global liquidity, continue to incentivize private equity investment as investors seek higher risk-adjusted returns. Additionally, supportive government policies and evolving regulatory environments in many key regions are facilitating capital formation, streamlining operational aspects for portfolio companies, and generally encouraging inbound investment. The increasing maturity and growth of a significant number of high-potential companies, particularly in burgeoning technology and healthcare sectors, are creating a rich pipeline of attractive investment opportunities, further fueling capital deployment and deal activity.

Challenges in the Private Equity Industry Sector

Despite its impressive growth trajectory, the private equity sector navigates a landscape fraught with significant challenges. Heightened regulatory scrutiny and increasingly complex compliance demands, particularly in areas like environmental, social, and governance (ESG) factors, are leading to elevated operational costs and a greater need for specialized expertise. Intensifying competition among an expanding pool of private equity firms, including both established players and agile new entrants, is exerting downward pressure on deal valuations and potential returns. Furthermore, global economic uncertainties and disruptions, such as ongoing supply chain volatilities impacting portfolio companies across various industries, present considerable risks to achieving projected investment outcomes. The severity and nature of these challenges can differ substantially based on geographical focus and the specific industry segments in which firms operate.

Leading Players in the Private Equity Industry Market

- Warburg Pincus

- KKR

- Advent International

- Blackstone

- Carlyle

- EnCap Investments

- CVC Capital Partners

- TPG Capital

- Neuberger Berman

- Apollo Global Management

Key Developments in Private Equity Industry Sector

- September 2022: Nonantum Capital Partners acquired LJP Waste Solutions, expanding its presence in the waste management sector.

- August 2022: Prosus Ventures and PayU India acquired BillDesk in a USD 4.7 Billion deal, representing the largest acquisition in India's digital payments space.

Strategic Private Equity Industry Market Outlook

The private equity industry is poised for continued growth, driven by increasing demand for alternative investments, technological advancements, and evolving investor preferences. Strategic opportunities abound in sectors like technology, healthcare, and renewable energy. Focusing on ESG factors and deploying innovative investment strategies will be critical for success in the coming years. The industry will witness further consolidation, with larger firms acquiring smaller ones to achieve greater scale and market share. This evolution underscores a promising future, marked by continued innovation and substantial expansion.

Private Equity Industry Segmentation

-

1. Fund Type

- 1.1. Buyout

- 1.2. Venture Capital (VCs)

- 1.3. Real Estate

- 1.4. Infrastructure

- 1.5. Other (Distressed PE, Direct Lending, etc.)

-

2. Sector

- 2.1. Technology (Software)

- 2.2. Healthcare

- 2.3. Real Estate and Services

- 2.4. Financial Services

- 2.5. Industrials

- 2.6. Consumer & Retail

- 2.7. Energy & Power

- 2.8. Media & Entertainment

- 2.9. Telecom

- 2.10. Others (Transportation, etc.)

-

3. Investments

- 3.1. Large Cap

- 3.2. Upper Middle Market

- 3.3. Lower Middle Market

- 3.4. Real Estate

Private Equity Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Private Equity Industry Regional Market Share

Geographic Coverage of Private Equity Industry

Private Equity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 10.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fund Type

- 5.1.1. Buyout

- 5.1.2. Venture Capital (VCs)

- 5.1.3. Real Estate

- 5.1.4. Infrastructure

- 5.1.5. Other (Distressed PE, Direct Lending, etc.)

- 5.2. Market Analysis, Insights and Forecast - by Sector

- 5.2.1. Technology (Software)

- 5.2.2. Healthcare

- 5.2.3. Real Estate and Services

- 5.2.4. Financial Services

- 5.2.5. Industrials

- 5.2.6. Consumer & Retail

- 5.2.7. Energy & Power

- 5.2.8. Media & Entertainment

- 5.2.9. Telecom

- 5.2.10. Others (Transportation, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Investments

- 5.3.1. Large Cap

- 5.3.2. Upper Middle Market

- 5.3.3. Lower Middle Market

- 5.3.4. Real Estate

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Fund Type

- 6. Global Private Equity Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fund Type

- 6.1.1. Buyout

- 6.1.2. Venture Capital (VCs)

- 6.1.3. Real Estate

- 6.1.4. Infrastructure

- 6.1.5. Other (Distressed PE, Direct Lending, etc.)

- 6.2. Market Analysis, Insights and Forecast - by Sector

- 6.2.1. Technology (Software)

- 6.2.2. Healthcare

- 6.2.3. Real Estate and Services

- 6.2.4. Financial Services

- 6.2.5. Industrials

- 6.2.6. Consumer & Retail

- 6.2.7. Energy & Power

- 6.2.8. Media & Entertainment

- 6.2.9. Telecom

- 6.2.10. Others (Transportation, etc.)

- 6.3. Market Analysis, Insights and Forecast - by Investments

- 6.3.1. Large Cap

- 6.3.2. Upper Middle Market

- 6.3.3. Lower Middle Market

- 6.3.4. Real Estate

- 6.1. Market Analysis, Insights and Forecast - by Fund Type

- 7. North America Private Equity Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fund Type

- 7.1.1. Buyout

- 7.1.2. Venture Capital (VCs)

- 7.1.3. Real Estate

- 7.1.4. Infrastructure

- 7.1.5. Other (Distressed PE, Direct Lending, etc.)

- 7.2. Market Analysis, Insights and Forecast - by Sector

- 7.2.1. Technology (Software)

- 7.2.2. Healthcare

- 7.2.3. Real Estate and Services

- 7.2.4. Financial Services

- 7.2.5. Industrials

- 7.2.6. Consumer & Retail

- 7.2.7. Energy & Power

- 7.2.8. Media & Entertainment

- 7.2.9. Telecom

- 7.2.10. Others (Transportation, etc.)

- 7.3. Market Analysis, Insights and Forecast - by Investments

- 7.3.1. Large Cap

- 7.3.2. Upper Middle Market

- 7.3.3. Lower Middle Market

- 7.3.4. Real Estate

- 7.1. Market Analysis, Insights and Forecast - by Fund Type

- 8. Europe Private Equity Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fund Type

- 8.1.1. Buyout

- 8.1.2. Venture Capital (VCs)

- 8.1.3. Real Estate

- 8.1.4. Infrastructure

- 8.1.5. Other (Distressed PE, Direct Lending, etc.)

- 8.2. Market Analysis, Insights and Forecast - by Sector

- 8.2.1. Technology (Software)

- 8.2.2. Healthcare

- 8.2.3. Real Estate and Services

- 8.2.4. Financial Services

- 8.2.5. Industrials

- 8.2.6. Consumer & Retail

- 8.2.7. Energy & Power

- 8.2.8. Media & Entertainment

- 8.2.9. Telecom

- 8.2.10. Others (Transportation, etc.)

- 8.3. Market Analysis, Insights and Forecast - by Investments

- 8.3.1. Large Cap

- 8.3.2. Upper Middle Market

- 8.3.3. Lower Middle Market

- 8.3.4. Real Estate

- 8.1. Market Analysis, Insights and Forecast - by Fund Type

- 9. Asia Pacific Private Equity Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fund Type

- 9.1.1. Buyout

- 9.1.2. Venture Capital (VCs)

- 9.1.3. Real Estate

- 9.1.4. Infrastructure

- 9.1.5. Other (Distressed PE, Direct Lending, etc.)

- 9.2. Market Analysis, Insights and Forecast - by Sector

- 9.2.1. Technology (Software)

- 9.2.2. Healthcare

- 9.2.3. Real Estate and Services

- 9.2.4. Financial Services

- 9.2.5. Industrials

- 9.2.6. Consumer & Retail

- 9.2.7. Energy & Power

- 9.2.8. Media & Entertainment

- 9.2.9. Telecom

- 9.2.10. Others (Transportation, etc.)

- 9.3. Market Analysis, Insights and Forecast - by Investments

- 9.3.1. Large Cap

- 9.3.2. Upper Middle Market

- 9.3.3. Lower Middle Market

- 9.3.4. Real Estate

- 9.1. Market Analysis, Insights and Forecast - by Fund Type

- 10. Latin America Private Equity Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fund Type

- 10.1.1. Buyout

- 10.1.2. Venture Capital (VCs)

- 10.1.3. Real Estate

- 10.1.4. Infrastructure

- 10.1.5. Other (Distressed PE, Direct Lending, etc.)

- 10.2. Market Analysis, Insights and Forecast - by Sector

- 10.2.1. Technology (Software)

- 10.2.2. Healthcare

- 10.2.3. Real Estate and Services

- 10.2.4. Financial Services

- 10.2.5. Industrials

- 10.2.6. Consumer & Retail

- 10.2.7. Energy & Power

- 10.2.8. Media & Entertainment

- 10.2.9. Telecom

- 10.2.10. Others (Transportation, etc.)

- 10.3. Market Analysis, Insights and Forecast - by Investments

- 10.3.1. Large Cap

- 10.3.2. Upper Middle Market

- 10.3.3. Lower Middle Market

- 10.3.4. Real Estate

- 10.1. Market Analysis, Insights and Forecast - by Fund Type

- 11. Middle East Private Equity Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Fund Type

- 11.1.1. Buyout

- 11.1.2. Venture Capital (VCs)

- 11.1.3. Real Estate

- 11.1.4. Infrastructure

- 11.1.5. Other (Distressed PE, Direct Lending, etc.)

- 11.2. Market Analysis, Insights and Forecast - by Sector

- 11.2.1. Technology (Software)

- 11.2.2. Healthcare

- 11.2.3. Real Estate and Services

- 11.2.4. Financial Services

- 11.2.5. Industrials

- 11.2.6. Consumer & Retail

- 11.2.7. Energy & Power

- 11.2.8. Media & Entertainment

- 11.2.9. Telecom

- 11.2.10. Others (Transportation, etc.)

- 11.3. Market Analysis, Insights and Forecast - by Investments

- 11.3.1. Large Cap

- 11.3.2. Upper Middle Market

- 11.3.3. Lower Middle Market

- 11.3.4. Real Estate

- 11.1. Market Analysis, Insights and Forecast - by Fund Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Warburg Pincus**List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 KKR

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Advent International

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Blackstone

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Carlyle

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 EnCap Investments

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 CVC Capital Partners

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 TPG Capital

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Neuberger Berman

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Apollo Global Management

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Warburg Pincus**List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Private Equity Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Private Equity Industry Revenue (Million), by Fund Type 2025 & 2033

- Figure 3: North America Private Equity Industry Revenue Share (%), by Fund Type 2025 & 2033

- Figure 4: North America Private Equity Industry Revenue (Million), by Sector 2025 & 2033

- Figure 5: North America Private Equity Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 6: North America Private Equity Industry Revenue (Million), by Investments 2025 & 2033

- Figure 7: North America Private Equity Industry Revenue Share (%), by Investments 2025 & 2033

- Figure 8: North America Private Equity Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Private Equity Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Private Equity Industry Revenue (Million), by Fund Type 2025 & 2033

- Figure 11: Europe Private Equity Industry Revenue Share (%), by Fund Type 2025 & 2033

- Figure 12: Europe Private Equity Industry Revenue (Million), by Sector 2025 & 2033

- Figure 13: Europe Private Equity Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 14: Europe Private Equity Industry Revenue (Million), by Investments 2025 & 2033

- Figure 15: Europe Private Equity Industry Revenue Share (%), by Investments 2025 & 2033

- Figure 16: Europe Private Equity Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Private Equity Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Private Equity Industry Revenue (Million), by Fund Type 2025 & 2033

- Figure 19: Asia Pacific Private Equity Industry Revenue Share (%), by Fund Type 2025 & 2033

- Figure 20: Asia Pacific Private Equity Industry Revenue (Million), by Sector 2025 & 2033

- Figure 21: Asia Pacific Private Equity Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 22: Asia Pacific Private Equity Industry Revenue (Million), by Investments 2025 & 2033

- Figure 23: Asia Pacific Private Equity Industry Revenue Share (%), by Investments 2025 & 2033

- Figure 24: Asia Pacific Private Equity Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Private Equity Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Private Equity Industry Revenue (Million), by Fund Type 2025 & 2033

- Figure 27: Latin America Private Equity Industry Revenue Share (%), by Fund Type 2025 & 2033

- Figure 28: Latin America Private Equity Industry Revenue (Million), by Sector 2025 & 2033

- Figure 29: Latin America Private Equity Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 30: Latin America Private Equity Industry Revenue (Million), by Investments 2025 & 2033

- Figure 31: Latin America Private Equity Industry Revenue Share (%), by Investments 2025 & 2033

- Figure 32: Latin America Private Equity Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America Private Equity Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East Private Equity Industry Revenue (Million), by Fund Type 2025 & 2033

- Figure 35: Middle East Private Equity Industry Revenue Share (%), by Fund Type 2025 & 2033

- Figure 36: Middle East Private Equity Industry Revenue (Million), by Sector 2025 & 2033

- Figure 37: Middle East Private Equity Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 38: Middle East Private Equity Industry Revenue (Million), by Investments 2025 & 2033

- Figure 39: Middle East Private Equity Industry Revenue Share (%), by Investments 2025 & 2033

- Figure 40: Middle East Private Equity Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East Private Equity Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Private Equity Industry Revenue Million Forecast, by Fund Type 2020 & 2033

- Table 2: Global Private Equity Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 3: Global Private Equity Industry Revenue Million Forecast, by Investments 2020 & 2033

- Table 4: Global Private Equity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Private Equity Industry Revenue Million Forecast, by Fund Type 2020 & 2033

- Table 6: Global Private Equity Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 7: Global Private Equity Industry Revenue Million Forecast, by Investments 2020 & 2033

- Table 8: Global Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Private Equity Industry Revenue Million Forecast, by Fund Type 2020 & 2033

- Table 10: Global Private Equity Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 11: Global Private Equity Industry Revenue Million Forecast, by Investments 2020 & 2033

- Table 12: Global Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Private Equity Industry Revenue Million Forecast, by Fund Type 2020 & 2033

- Table 14: Global Private Equity Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 15: Global Private Equity Industry Revenue Million Forecast, by Investments 2020 & 2033

- Table 16: Global Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Private Equity Industry Revenue Million Forecast, by Fund Type 2020 & 2033

- Table 18: Global Private Equity Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 19: Global Private Equity Industry Revenue Million Forecast, by Investments 2020 & 2033

- Table 20: Global Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Private Equity Industry Revenue Million Forecast, by Fund Type 2020 & 2033

- Table 22: Global Private Equity Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 23: Global Private Equity Industry Revenue Million Forecast, by Investments 2020 & 2033

- Table 24: Global Private Equity Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Private Equity Industry?

The projected CAGR is approximately > 10.00%.

2. Which companies are prominent players in the Private Equity Industry?

Key companies in the market include Warburg Pincus**List Not Exhaustive, KKR, Advent International, Blackstone, Carlyle, EnCap Investments, CVC Capital Partners, TPG Capital, Neuberger Berman, Apollo Global Management.

3. What are the main segments of the Private Equity Industry?

The market segments include Fund Type, Sector, Investments.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Innovative Tracking Technologies.

6. What are the notable trends driving market growth?

Growth Investments Have Become Larger and More Complex.

7. Are there any restraints impacting market growth?

Rising Competition of Banks with Fintech and Financial Services.

8. Can you provide examples of recent developments in the market?

September 2022: Nonantum Capital Partners, a middle-market private equity firm, today announced the acquisition of LJP Waste Solutions ("LJP") from Aperion Management. LJP is a leading regional provider of non-hazardous solid waste and recycling services specializing in zero landfill and waste-to-energy solutions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Private Equity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Private Equity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Private Equity Industry?

To stay informed about further developments, trends, and reports in the Private Equity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence