Key Insights

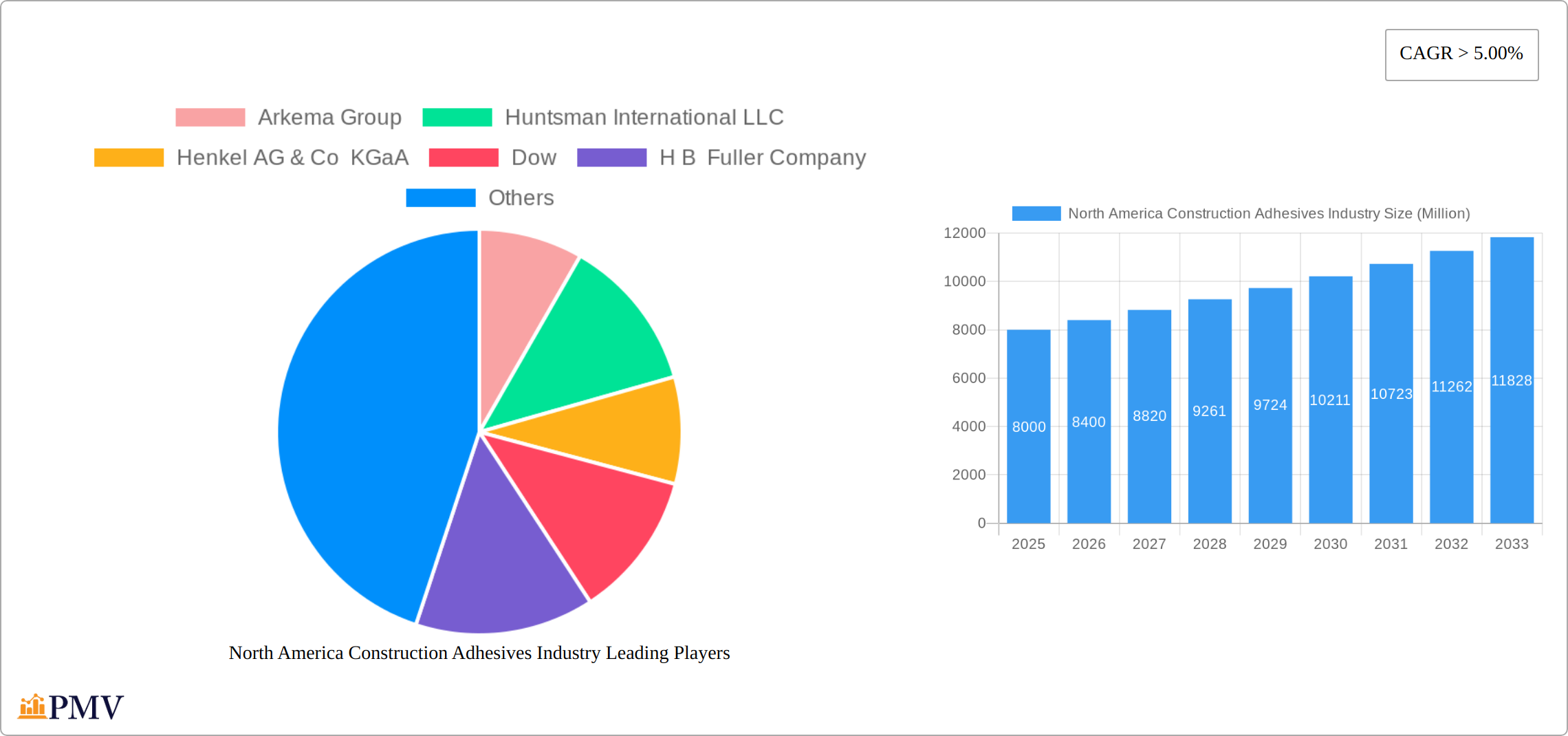

The North American construction adhesives market, valued at approximately $8 billion in 2025, is experiencing robust growth, projected to maintain a CAGR exceeding 5% through 2033. This expansion is fueled by several key drivers. The ongoing surge in residential and commercial construction activities, particularly in major metropolitan areas, is a primary factor. Government infrastructure investments, including road and bridge repairs and new constructions, further bolster demand. Moreover, the increasing preference for sustainable and high-performance building materials that utilize advanced adhesive technologies contributes significantly to market growth. Specific trends include the rising adoption of water-borne adhesives due to their environmental friendliness and the increasing demand for specialized adhesives tailored to specific construction applications, such as high-strength structural adhesives and those designed for extreme weather conditions. While the industry faces challenges like fluctuating raw material prices and potential supply chain disruptions, the overall market outlook remains positive, driven by the robust construction sector and ongoing technological advancements.

Market segmentation reveals that acrylics, epoxies, and polyurethanes dominate the resin type segment, reflecting their versatility and performance characteristics. The water-borne technology segment is also exhibiting rapid growth, reflecting the growing environmental consciousness within the construction industry. The residential segment leads in terms of end-use application, owing to the large volume of residential construction projects. However, the commercial and infrastructure segments are also showing significant growth potential, fueled by increasing urbanisation and infrastructure development projects. Key players in the market, including Arkema, Huntsman, Henkel, Dow, and 3M, are actively engaged in research and development to introduce innovative products that cater to the evolving needs of the construction industry. Their strategic initiatives such as mergers, acquisitions, and new product launches contribute significantly to the market's dynamism and growth trajectory.

North America Construction Adhesives Industry: 2019-2033 Market Report

This comprehensive report provides an in-depth analysis of the North America construction adhesives market, offering invaluable insights for businesses, investors, and industry professionals. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report dissects market trends, competitive dynamics, and growth opportunities within this vital sector. The report values are in Millions.

North America Construction Adhesives Industry Market Structure & Competitive Dynamics

The North American construction adhesives market presents a moderately consolidated structure, characterized by several key players commanding significant market share. Prominent competitors include Arkema Group, Huntsman International LLC, Henkel AG & Co KGaA, Dow, H.B. Fuller Company, Sika AG, 3M, Avery Dennison Corporation, RPM International Inc., Wacker Chemie AG, Parker Hannifin Corp., and Ashland. These industry giants compete fiercely, leveraging strategies focused on product innovation, competitive pricing, and robust distribution networks. The collective market share of the top five players is estimated at [Insert Updated Percentage]% in 2025, indicating a significant level of market concentration. Driving innovation are robust ecosystems fueled by continuous advancements in resin technology and application methodologies. Furthermore, the regulatory landscape, encompassing stringent environmental regulations and comprehensive safety standards, significantly influences product development and market access. The presence of product substitutes, such as mechanical fasteners, introduces additional competitive pressures and shapes market dynamics. The past five years have witnessed considerable merger and acquisition (M&A) activity, with an estimated total deal value of [Insert Updated Value] million USD. Notable examples include [Insert Specific Examples of M&A Activity with brief descriptions and impact]. Finally, the prevailing end-user trend toward sustainable and high-performance construction materials is profoundly reshaping demand patterns, pushing the industry to adapt and innovate.

- Market Concentration: Moderately consolidated, with top 5 players holding [Insert Updated Percentage]% market share (2025).

- Innovation Ecosystems: Robust, driven by advancements in resin technology and application methods.

- Regulatory Frameworks: Significant influence on product development, market access, and material composition.

- Product Substitutes: Mechanical fasteners represent a notable competitive pressure.

- M&A Activity: Significant activity with estimated deal values of [Insert Updated Value] million USD in the past five years.

North America Construction Adhesives Industry Industry Trends & Insights

The North American construction adhesives market is experiencing robust growth, driven by factors such as increasing construction activity across residential, commercial, and infrastructure sectors. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Technological disruptions, such as the adoption of more sustainable and high-performance adhesives, are transforming the industry. Consumer preferences are shifting towards eco-friendly and easy-to-use products, impacting demand for specific adhesive types. The increasing adoption of water-borne adhesives, fueled by environmental concerns, is noteworthy. Market penetration of water-borne adhesives in the residential sector is projected to reach xx% by 2033. Competitive dynamics are characterized by ongoing innovation, strategic partnerships, and mergers and acquisitions. The growing focus on improving energy efficiency in buildings is also boosting the demand for specialized construction adhesives. Government initiatives aimed at improving infrastructure further propel market growth. The increasing adoption of prefabricated construction methods is also anticipated to enhance the market growth during the projected period.

Dominant Markets & Segments in North America Construction Adhesives Industry

The residential sector currently holds the dominant position in the North American construction adhesives market, fueled by robust housing demand and a steady increase in renovation and repair projects. However, significant growth potential lies within the infrastructure sector, projected to experience the fastest expansion during the forecast period. This accelerated growth is driven by substantial government investments in large-scale infrastructure development projects. Analyzing resin types, acrylics command the largest market share due to their versatility, cost-effectiveness, and broad applicability across various construction segments. Concurrently, water-borne technology maintains market dominance, largely attributed to its environmentally friendly properties and compliance with increasingly stringent environmental regulations.

Key Market Drivers:

- Residential Construction: Strong housing market, encompassing new construction, renovations, and repairs.

- Commercial Construction: Growth in non-residential construction projects, including office buildings, retail spaces, and hospitality facilities.

- Infrastructure Development: Government investments in highway projects, public works, and transportation infrastructure.

- Industrial Construction: Demand from manufacturing facilities, warehouses, and industrial plants.

- Acrylics (Resin Type): Versatility, cost-effectiveness, and suitability for diverse applications.

- Water-borne Technology: Environmental friendliness and adherence to regulatory compliance.

North America Construction Adhesives Industry Product Innovations

The construction adhesives sector is witnessing a surge in innovative product development. Recent breakthroughs include high-performance, eco-friendly adhesives boasting enhanced durability and superior bonding strength. These advancements directly address the rising demand for sustainable and energy-efficient construction practices. Furthermore, improvements in application methods, such as pre-applied adhesives and automated dispensing systems, are boosting productivity and reducing labor costs. The introduction of specialized adhesives with properties like fire resistance or acoustic dampening caters to specific needs across diverse construction applications. These innovations collectively reshape the competitive landscape, offering enhanced performance and cost advantages, ultimately driving market growth.

Report Segmentation & Scope

This report provides a comprehensive segmentation of the North America construction adhesives market, categorized by resin type (Acrylics, Epoxy, Polyurethanes, Polyvinyl Acetate (PVA), Silicones, Other Resin Types), technology (Water-borne, Reactive, Hot-melt, Other Technologies), and end-use sector (Residential, Commercial, Infrastructure, Industrial). Each segment undergoes detailed analysis, encompassing market size, growth projections, and competitive dynamics. Market size data is presented for the historical period (2019-2024), the base year (2025), and the forecast period (2025-2033). [Detailed analysis of each segment with specific data would follow here.]

Key Drivers of North America Construction Adhesives Industry Growth

The growth of the North American construction adhesives market is fueled by several key factors. Increased construction activity across all sectors is a major driver. Government investments in infrastructure projects and initiatives promoting sustainable construction practices contribute significantly. Technological advancements leading to higher-performance and more eco-friendly adhesives also boost demand. The growing preference for prefabricated construction methods further enhances market expansion.

Challenges in the North America Construction Adhesives Industry Sector

The North American construction adhesives industry faces several challenges. Fluctuations in raw material prices and supply chain disruptions impact profitability and production. Stringent environmental regulations and safety standards necessitate significant investments in R&D and compliance. Intense competition from established players and the emergence of new entrants create pressure on pricing and margins. Economic downturns and reduced construction activity can significantly affect market demand.

Leading Players in the North America Construction Adhesives Industry Market

- Arkema Group

- Huntsman International LLC

- Henkel AG & Co KGaA

- Dow

- H B Fuller Company

- Sika AG

- 3M

- AVERY DENNISON CORPORATION

- RPM International Inc

- Wacker Chemie AG

- Parker Hannifin Corp

- Ashland

Key Developments in North America Construction Adhesives Industry Sector

- [Insert specific developments with year/month and impact on market dynamics. Examples: New product launches (with details), mergers and acquisitions (with details and impact), regulatory changes (with details and impact), significant investments in R&D, partnerships and collaborations, etc.]

Strategic North America Construction Adhesives Industry Market Outlook

The North American construction adhesives market presents significant growth opportunities, driven by continued expansion in the construction sector and technological advancements. Strategic focus on developing sustainable and high-performance products, expanding into new market segments, and investing in innovative application methods will be crucial for success. Companies that leverage digital technologies to optimize supply chains and enhance customer engagement will gain a competitive advantage. The market is poised for considerable growth in the coming years, offering attractive investment prospects for both established players and new entrants.

North America Construction Adhesives Industry Segmentation

-

1. Resin Type

- 1.1. Acrylics

- 1.2. Epoxy

- 1.3. Polyurethanes

- 1.4. Polyvinyl Acetate (PVA)

- 1.5. Silicones

- 1.6. Other Resin Types

-

2. Technology

- 2.1. Water-borne

- 2.2. Reactive

- 2.3. Hot-melt

- 2.4. Other Technologies

-

3. End-use Sector

- 3.1. Residential

- 3.2. Commercial

- 3.3. Infrastructure

- 3.4. Industrial

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

North America Construction Adhesives Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Construction Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Growing Demand for Residential Construction in the United States

- 3.3. Market Restrains

- 3.3.1. ; Limited Usage in High End Applications; Other Restraints

- 3.4. Market Trends

- 3.4.1. Waterborne Technology to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Acrylics

- 5.1.2. Epoxy

- 5.1.3. Polyurethanes

- 5.1.4. Polyvinyl Acetate (PVA)

- 5.1.5. Silicones

- 5.1.6. Other Resin Types

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Water-borne

- 5.2.2. Reactive

- 5.2.3. Hot-melt

- 5.2.4. Other Technologies

- 5.3. Market Analysis, Insights and Forecast - by End-use Sector

- 5.3.1. Residential

- 5.3.2. Commercial

- 5.3.3. Infrastructure

- 5.3.4. Industrial

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. United States North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Acrylics

- 6.1.2. Epoxy

- 6.1.3. Polyurethanes

- 6.1.4. Polyvinyl Acetate (PVA)

- 6.1.5. Silicones

- 6.1.6. Other Resin Types

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Water-borne

- 6.2.2. Reactive

- 6.2.3. Hot-melt

- 6.2.4. Other Technologies

- 6.3. Market Analysis, Insights and Forecast - by End-use Sector

- 6.3.1. Residential

- 6.3.2. Commercial

- 6.3.3. Infrastructure

- 6.3.4. Industrial

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. Canada North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 7.1.1. Acrylics

- 7.1.2. Epoxy

- 7.1.3. Polyurethanes

- 7.1.4. Polyvinyl Acetate (PVA)

- 7.1.5. Silicones

- 7.1.6. Other Resin Types

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Water-borne

- 7.2.2. Reactive

- 7.2.3. Hot-melt

- 7.2.4. Other Technologies

- 7.3. Market Analysis, Insights and Forecast - by End-use Sector

- 7.3.1. Residential

- 7.3.2. Commercial

- 7.3.3. Infrastructure

- 7.3.4. Industrial

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Resin Type

- 8. Mexico North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 8.1.1. Acrylics

- 8.1.2. Epoxy

- 8.1.3. Polyurethanes

- 8.1.4. Polyvinyl Acetate (PVA)

- 8.1.5. Silicones

- 8.1.6. Other Resin Types

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Water-borne

- 8.2.2. Reactive

- 8.2.3. Hot-melt

- 8.2.4. Other Technologies

- 8.3. Market Analysis, Insights and Forecast - by End-use Sector

- 8.3.1. Residential

- 8.3.2. Commercial

- 8.3.3. Infrastructure

- 8.3.4. Industrial

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Resin Type

- 9. United States North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Construction Adhesives Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Arkema Group

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Huntsman International LLC

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Henkel AG & Co KGaA

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Dow

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 H B Fuller Company

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Sika AG

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 3M

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 AVERY DENNISON CORPORATION

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 RPM International Inc *List Not Exhaustive

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Wacker Chemie AG

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Parker Hannifin Corp

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Ashland

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 Arkema Group

List of Figures

- Figure 1: North America Construction Adhesives Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Construction Adhesives Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Construction Adhesives Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Construction Adhesives Industry Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 3: North America Construction Adhesives Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 4: North America Construction Adhesives Industry Revenue Million Forecast, by End-use Sector 2019 & 2032

- Table 5: North America Construction Adhesives Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 6: North America Construction Adhesives Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: North America Construction Adhesives Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States North America Construction Adhesives Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada North America Construction Adhesives Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Mexico North America Construction Adhesives Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Rest of North America North America Construction Adhesives Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: North America Construction Adhesives Industry Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 13: North America Construction Adhesives Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 14: North America Construction Adhesives Industry Revenue Million Forecast, by End-use Sector 2019 & 2032

- Table 15: North America Construction Adhesives Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 16: North America Construction Adhesives Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: North America Construction Adhesives Industry Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 18: North America Construction Adhesives Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 19: North America Construction Adhesives Industry Revenue Million Forecast, by End-use Sector 2019 & 2032

- Table 20: North America Construction Adhesives Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: North America Construction Adhesives Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: North America Construction Adhesives Industry Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 23: North America Construction Adhesives Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 24: North America Construction Adhesives Industry Revenue Million Forecast, by End-use Sector 2019 & 2032

- Table 25: North America Construction Adhesives Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Construction Adhesives Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Construction Adhesives Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the North America Construction Adhesives Industry?

Key companies in the market include Arkema Group, Huntsman International LLC, Henkel AG & Co KGaA, Dow, H B Fuller Company, Sika AG, 3M, AVERY DENNISON CORPORATION, RPM International Inc *List Not Exhaustive, Wacker Chemie AG, Parker Hannifin Corp, Ashland.

3. What are the main segments of the North America Construction Adhesives Industry?

The market segments include Resin Type, Technology, End-use Sector, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand for Residential Construction in the United States.

6. What are the notable trends driving market growth?

Waterborne Technology to Dominate the Market.

7. Are there any restraints impacting market growth?

; Limited Usage in High End Applications; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Construction Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Construction Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Construction Adhesives Industry?

To stay informed about further developments, trends, and reports in the North America Construction Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence