Key Insights

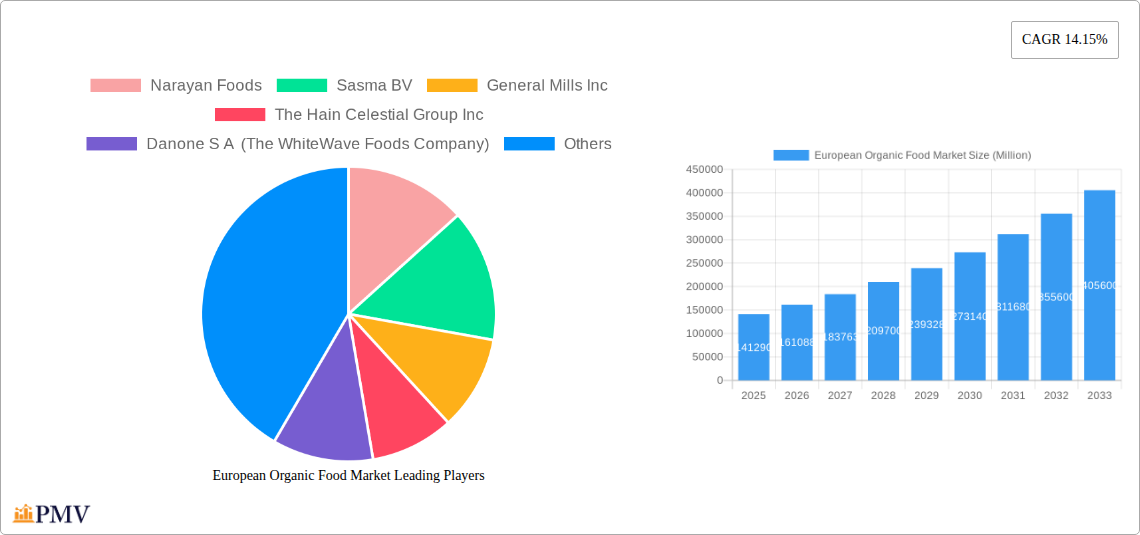

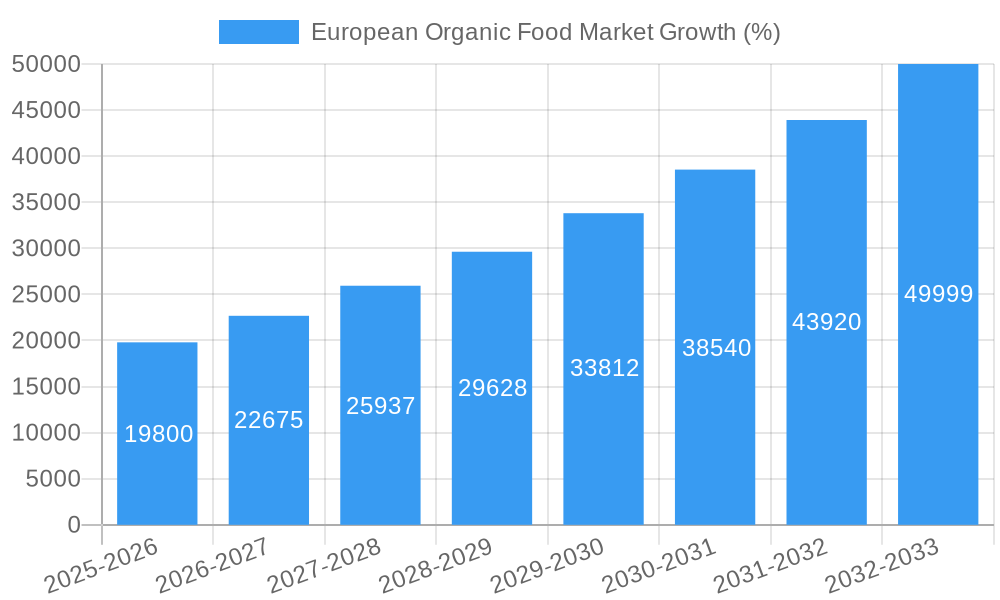

The European organic food market, valued at €141.29 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 14.15% from 2025 to 2033. This surge is driven by increasing consumer awareness of health and wellness, a rising preference for sustainably produced food, and stricter regulations promoting organic farming practices across major European nations. The market is segmented by product type (organic foods and organic beverages) and distribution channel (supermarkets/hypermarkets, convenience stores, specialist stores, and online retailing). Germany, France, Italy, the United Kingdom, and the Netherlands represent significant market shares within Europe, reflecting established consumer bases and robust retail infrastructure supporting organic product distribution. Growing demand for convenience and the increasing adoption of e-commerce platforms are driving the expansion of online organic food retailing, presenting new opportunities for market players.

The market's growth is further fueled by the increasing availability of a wider variety of organic products, encompassing both staple foods and specialized items catering to diverse dietary needs and preferences. However, challenges remain, including the higher price point of organic products compared to conventionally produced foods, which can limit accessibility for some consumer segments. Furthermore, ensuring consistent supply chain management and maintaining the integrity of organic certification across the entire production and distribution process are crucial for sustainable market development. Key players like Nestlé, Danone, General Mills, and smaller specialized brands are actively competing to capture market share, leveraging branding, innovation, and strategic partnerships to expand their presence within this dynamic and rapidly growing sector. Future growth will likely depend on addressing price sensitivity, improving supply chain resilience, and capitalizing on the burgeoning demand for convenient and accessible organic food options.

European Organic Food Market: A Comprehensive Report (2019-2033)

This comprehensive report provides a detailed analysis of the European organic food market, covering the period 2019-2033. With a base year of 2025 and a forecast period of 2025-2033, this report offers invaluable insights into market size, growth drivers, competitive dynamics, and future opportunities for businesses operating within this rapidly expanding sector. The study encompasses a wide range of key aspects, including market segmentation by product type (organic foods, organic beverages), distribution channels (supermarkets/hypermarkets, convenience stores, specialist stores, online retailing), and leading companies such as Narayan Foods, Sasma BV, General Mills Inc., and Nestlé S.A. The report utilizes data from the historical period (2019-2024) to provide a robust foundation for future projections, delivering actionable intelligence for strategic decision-making. The market is estimated to be worth xx Million in 2025.

European Organic Food Market Market Structure & Competitive Dynamics

The European organic food market exhibits a moderately concentrated structure, with several large multinational corporations holding significant market share alongside a diverse range of smaller, specialized players. Market share is dynamic, influenced by factors such as product innovation, brand recognition, and effective distribution strategies. Key players such as General Mills Inc. and Nestlé S.A. leverage their established brand presence and extensive distribution networks to maintain a strong competitive edge. However, smaller, niche players often specialize in specific product categories or regions, carving out valuable market segments.

The innovation ecosystem is robust, with ongoing research and development focused on improving product quality, expanding product lines, and enhancing sustainability practices. This includes advancements in organic farming techniques, packaging innovations, and the development of new and exciting organic food and beverage products. The regulatory landscape is increasingly stringent, with regulations focusing on labeling, certification, and traceability. These regulations influence market entry and competitiveness. Furthermore, the increasing availability of organic food substitutes and shifting consumer preferences toward healthier and more sustainable options influence the overall market dynamics. M&A activity has been significant, with deal values in the range of xx Million annually in recent years, often driven by strategic acquisitions aimed at expanding product portfolios and market reach. Examples include the partnerships between major players in the organic food sector and innovative companies like MeliBio.

- Market Concentration: Moderately concentrated, with large players commanding significant shares.

- Innovation Ecosystems: Active R&D in sustainable farming, packaging, and product development.

- Regulatory Frameworks: Stringent regulations impacting labeling, certification, and traceability.

- Product Substitutes: Competition from conventional food products and alternative healthy options.

- M&A Activity: Significant activity with deal values averaging xx Million annually.

European Organic Food Market Industry Trends & Insights

The European organic food market is experiencing robust growth, driven by several key factors. Increasing consumer awareness of health and environmental benefits fuels demand for organic products. The rising disposable incomes across several European countries, coupled with a shift towards healthier lifestyles, bolster market expansion. Technological advancements in organic farming and production have led to improved yields and efficiency, thereby driving down costs and enhancing accessibility. The compounded annual growth rate (CAGR) for the period 2025-2033 is projected at xx%, showcasing significant market expansion. Market penetration of organic products has increased steadily over the past years, reaching xx% in 2024 and expected to continue to rise, showing a strong consumer preference towards organic products in Europe. Consumer preferences are constantly evolving, with a growing demand for convenient, ready-to-eat organic meals and snacks. This trend fuels innovation within the food industry, leading to new product offerings tailored to consumer preferences. Competitive dynamics remain intensely competitive, pushing companies to innovate continually and optimize their supply chains to meet consumer demand.

Dominant Markets & Segments in European Organic Food Market

While the entire European market shows strong growth, certain regions and segments demonstrate particularly strong performance. Germany, France, and the UK remain leading markets, due to high consumer awareness, strong regulatory support, and established organic food infrastructure.

- Leading Regions: Germany, France, and the UK.

- Dominant Product Types: Organic Foods (xx Million market size in 2025) hold a larger market share compared to Organic Beverages (xx Million market size in 2025). This is driven by the broader range of products available and diverse consumer preferences.

- Leading Distribution Channels: Supermarkets/hypermarkets account for the largest share of the distribution channel, followed by online retailers, indicating significant opportunities for growth in e-commerce. Specialist stores and convenience stores show potential for future expansion.

Key Drivers for Dominance:

- Germany: Strong consumer demand, government support for organic farming, and established supply chains.

- France: Growing popularity of organic foods, particularly among health-conscious consumers, and a favorable regulatory environment.

- UK: High consumer spending power, increasing availability of organic products in major retailers and strong online retail market.

- Supermarkets/Hypermarkets: Wide reach and established distribution networks, catering to a large customer base.

- Online Retailing: Convenience and accessibility, providing an alternative to traditional brick-and-mortar stores.

European Organic Food Market Product Innovations

Recent years have seen significant innovation in the European organic food market. Companies are focusing on developing convenient, ready-to-eat meals and snacks, along with plant-based alternatives to traditional products. Technological advances in food processing and packaging enhance shelf life and product quality. These innovations cater to the evolving consumer demands for healthy, convenient, and sustainable food options, contributing to increased market growth. Examples include the launch of plant-based honey by MeliBio and the expansion of plant-based meal brands in supermarkets.

Report Segmentation & Scope

This report provides a comprehensive segmentation of the European organic food market based on Product Type and Distribution Channels.

Product Type:

Organic Foods: This segment includes a wide variety of organic food products like fruits, vegetables, grains, dairy, and meat. The growth of this segment is driven by increasing health consciousness, with a projected growth of xx% during the forecast period. Competitive dynamics are intense, with both large and small players vying for market share.

Organic Beverages: This segment comprises organic juices, teas, soft drinks, and alcoholic beverages. The segment’s growth is projected at xx% during the forecast period, driven by the increasing demand for healthier beverage options.

Distribution Channel:

Supermarkets/Hypermarkets: This channel dominates the market due to its extensive reach and established distribution network. This segment is expected to grow by xx% during the forecast period.

Convenience Stores: This segment exhibits moderate growth, driven by the increasing demand for convenient, on-the-go food options. The projected growth rate is xx%.

Specialist Stores: Growth in this segment is projected at xx%, driven by a focus on niche organic products.

Online Retailing: This channel shows substantial growth potential due to the rising popularity of e-commerce. The projected growth rate is xx%.

Key Drivers of European Organic Food Market Growth

Several key factors propel the growth of the European organic food market. Rising consumer awareness of health and environmental benefits, along with increased disposable incomes in many European countries, drives the demand for organic products. Government regulations and subsidies supporting organic farming increase production and availability. Technological improvements enhance efficiency and reduce costs. Moreover, the growing popularity of plant-based foods and the rise of conscious consumerism further fuel market expansion.

Challenges in the European Organic Food Market Sector

The European organic food market faces several challenges, including higher production costs compared to conventional farming, leading to higher prices that can limit accessibility for some consumers. Fluctuations in raw material prices and supply chain disruptions can impact profitability. Stringent regulations and certification processes can be costly and time-consuming for producers. Intense competition from both established and emerging players also poses a challenge for businesses.

Leading Players in the European Organic Food Market Market

- Narayan Foods

- Sasma BV

- General Mills Inc.

- The Hain Celestial Group Inc.

- Danone S.A. (The WhiteWave Foods Company)

- Clipper Teas

- Amy's Kitchen Inc

- Starbucks Corporation

- PureOrganic Drinks Limited

- Nestlé S.A.

Key Developments in European Organic Food Market Sector

- November 2022: Narayan Foods partners with MeliBio to launch plant-based honey in 75,000 European stores.

- November 2022: Ocado and Planet Organic introduce the allplants plant-based meal brand.

- July 2021: The Hain Celestial Group launches new organic snacks and teas in the European market.

Strategic European Organic Food Market Market Outlook

The European organic food market presents significant growth potential. Continued consumer demand for healthy and sustainable products, coupled with technological advancements and supportive government policies, will drive further expansion. Companies focusing on innovation, sustainability, and effective distribution strategies are well-positioned to capitalize on this growth. The market’s future hinges on addressing challenges like production costs and ensuring supply chain resilience to maintain sustainable growth and accessibility.

European Organic Food Market Segmentation

-

1. Product Type

-

1.1. Organic Foods

- 1.1.1. Fruit & Vegetables

- 1.1.2. Meat, Fish & Poultry

- 1.1.3. Dairy Products

- 1.1.4. Frozen & Processed Foods

- 1.1.5. Other Product Types

-

1.2. Organic Beverages

-

1.2.1. Alcoholic

- 1.2.1.1. Wine

- 1.2.1.2. Beer

- 1.2.1.3. Spirits

-

1.2.2. Non-alcoholic

- 1.2.2.1. Fruit and Vegetable Juices

- 1.2.2.2. Dairy Beverages

- 1.2.2.3. Coffee

- 1.2.2.4. Tea

- 1.2.2.5. Carbonated Beverages

- 1.2.2.6. Other Non-alcoholic Beverages

-

1.2.1. Alcoholic

-

1.1. Organic Foods

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Specialist Stores

- 2.4. Online Retailing

- 2.5. Other Distribution Channels

European Organic Food Market Segmentation By Geography

- 1. United Kingdom

- 2. France

- 3. Germany

- 4. Italy

- 5. Russia

- 6. Spain

- 7. Rest of Europe

European Organic Food Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 14.15% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Inclination Towards Reduced Sugar and Healthier Snacking Options; Surge in Demand for Organic Food Products

- 3.3. Market Restrains

- 3.3.1. Availability of Cheaper Snacking Options

- 3.4. Market Trends

- 3.4.1. Growing Demand for Clean-label Products

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Organic Foods

- 5.1.1.1. Fruit & Vegetables

- 5.1.1.2. Meat, Fish & Poultry

- 5.1.1.3. Dairy Products

- 5.1.1.4. Frozen & Processed Foods

- 5.1.1.5. Other Product Types

- 5.1.2. Organic Beverages

- 5.1.2.1. Alcoholic

- 5.1.2.1.1. Wine

- 5.1.2.1.2. Beer

- 5.1.2.1.3. Spirits

- 5.1.2.2. Non-alcoholic

- 5.1.2.2.1. Fruit and Vegetable Juices

- 5.1.2.2.2. Dairy Beverages

- 5.1.2.2.3. Coffee

- 5.1.2.2.4. Tea

- 5.1.2.2.5. Carbonated Beverages

- 5.1.2.2.6. Other Non-alcoholic Beverages

- 5.1.2.1. Alcoholic

- 5.1.1. Organic Foods

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Specialist Stores

- 5.2.4. Online Retailing

- 5.2.5. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. France

- 5.3.3. Germany

- 5.3.4. Italy

- 5.3.5. Russia

- 5.3.6. Spain

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United Kingdom European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Organic Foods

- 6.1.1.1. Fruit & Vegetables

- 6.1.1.2. Meat, Fish & Poultry

- 6.1.1.3. Dairy Products

- 6.1.1.4. Frozen & Processed Foods

- 6.1.1.5. Other Product Types

- 6.1.2. Organic Beverages

- 6.1.2.1. Alcoholic

- 6.1.2.1.1. Wine

- 6.1.2.1.2. Beer

- 6.1.2.1.3. Spirits

- 6.1.2.2. Non-alcoholic

- 6.1.2.2.1. Fruit and Vegetable Juices

- 6.1.2.2.2. Dairy Beverages

- 6.1.2.2.3. Coffee

- 6.1.2.2.4. Tea

- 6.1.2.2.5. Carbonated Beverages

- 6.1.2.2.6. Other Non-alcoholic Beverages

- 6.1.2.1. Alcoholic

- 6.1.1. Organic Foods

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Specialist Stores

- 6.2.4. Online Retailing

- 6.2.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. France European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Organic Foods

- 7.1.1.1. Fruit & Vegetables

- 7.1.1.2. Meat, Fish & Poultry

- 7.1.1.3. Dairy Products

- 7.1.1.4. Frozen & Processed Foods

- 7.1.1.5. Other Product Types

- 7.1.2. Organic Beverages

- 7.1.2.1. Alcoholic

- 7.1.2.1.1. Wine

- 7.1.2.1.2. Beer

- 7.1.2.1.3. Spirits

- 7.1.2.2. Non-alcoholic

- 7.1.2.2.1. Fruit and Vegetable Juices

- 7.1.2.2.2. Dairy Beverages

- 7.1.2.2.3. Coffee

- 7.1.2.2.4. Tea

- 7.1.2.2.5. Carbonated Beverages

- 7.1.2.2.6. Other Non-alcoholic Beverages

- 7.1.2.1. Alcoholic

- 7.1.1. Organic Foods

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets/Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Specialist Stores

- 7.2.4. Online Retailing

- 7.2.5. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Germany European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Organic Foods

- 8.1.1.1. Fruit & Vegetables

- 8.1.1.2. Meat, Fish & Poultry

- 8.1.1.3. Dairy Products

- 8.1.1.4. Frozen & Processed Foods

- 8.1.1.5. Other Product Types

- 8.1.2. Organic Beverages

- 8.1.2.1. Alcoholic

- 8.1.2.1.1. Wine

- 8.1.2.1.2. Beer

- 8.1.2.1.3. Spirits

- 8.1.2.2. Non-alcoholic

- 8.1.2.2.1. Fruit and Vegetable Juices

- 8.1.2.2.2. Dairy Beverages

- 8.1.2.2.3. Coffee

- 8.1.2.2.4. Tea

- 8.1.2.2.5. Carbonated Beverages

- 8.1.2.2.6. Other Non-alcoholic Beverages

- 8.1.2.1. Alcoholic

- 8.1.1. Organic Foods

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets/Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Specialist Stores

- 8.2.4. Online Retailing

- 8.2.5. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Italy European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Organic Foods

- 9.1.1.1. Fruit & Vegetables

- 9.1.1.2. Meat, Fish & Poultry

- 9.1.1.3. Dairy Products

- 9.1.1.4. Frozen & Processed Foods

- 9.1.1.5. Other Product Types

- 9.1.2. Organic Beverages

- 9.1.2.1. Alcoholic

- 9.1.2.1.1. Wine

- 9.1.2.1.2. Beer

- 9.1.2.1.3. Spirits

- 9.1.2.2. Non-alcoholic

- 9.1.2.2.1. Fruit and Vegetable Juices

- 9.1.2.2.2. Dairy Beverages

- 9.1.2.2.3. Coffee

- 9.1.2.2.4. Tea

- 9.1.2.2.5. Carbonated Beverages

- 9.1.2.2.6. Other Non-alcoholic Beverages

- 9.1.2.1. Alcoholic

- 9.1.1. Organic Foods

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets/Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Specialist Stores

- 9.2.4. Online Retailing

- 9.2.5. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Russia European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Organic Foods

- 10.1.1.1. Fruit & Vegetables

- 10.1.1.2. Meat, Fish & Poultry

- 10.1.1.3. Dairy Products

- 10.1.1.4. Frozen & Processed Foods

- 10.1.1.5. Other Product Types

- 10.1.2. Organic Beverages

- 10.1.2.1. Alcoholic

- 10.1.2.1.1. Wine

- 10.1.2.1.2. Beer

- 10.1.2.1.3. Spirits

- 10.1.2.2. Non-alcoholic

- 10.1.2.2.1. Fruit and Vegetable Juices

- 10.1.2.2.2. Dairy Beverages

- 10.1.2.2.3. Coffee

- 10.1.2.2.4. Tea

- 10.1.2.2.5. Carbonated Beverages

- 10.1.2.2.6. Other Non-alcoholic Beverages

- 10.1.2.1. Alcoholic

- 10.1.1. Organic Foods

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets/Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Specialist Stores

- 10.2.4. Online Retailing

- 10.2.5. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Organic Foods

- 11.1.1.1. Fruit & Vegetables

- 11.1.1.2. Meat, Fish & Poultry

- 11.1.1.3. Dairy Products

- 11.1.1.4. Frozen & Processed Foods

- 11.1.1.5. Other Product Types

- 11.1.2. Organic Beverages

- 11.1.2.1. Alcoholic

- 11.1.2.1.1. Wine

- 11.1.2.1.2. Beer

- 11.1.2.1.3. Spirits

- 11.1.2.2. Non-alcoholic

- 11.1.2.2.1. Fruit and Vegetable Juices

- 11.1.2.2.2. Dairy Beverages

- 11.1.2.2.3. Coffee

- 11.1.2.2.4. Tea

- 11.1.2.2.5. Carbonated Beverages

- 11.1.2.2.6. Other Non-alcoholic Beverages

- 11.1.2.1. Alcoholic

- 11.1.1. Organic Foods

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets/Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Specialist Stores

- 11.2.4. Online Retailing

- 11.2.5. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Europe European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Organic Foods

- 12.1.1.1. Fruit & Vegetables

- 12.1.1.2. Meat, Fish & Poultry

- 12.1.1.3. Dairy Products

- 12.1.1.4. Frozen & Processed Foods

- 12.1.1.5. Other Product Types

- 12.1.2. Organic Beverages

- 12.1.2.1. Alcoholic

- 12.1.2.1.1. Wine

- 12.1.2.1.2. Beer

- 12.1.2.1.3. Spirits

- 12.1.2.2. Non-alcoholic

- 12.1.2.2.1. Fruit and Vegetable Juices

- 12.1.2.2.2. Dairy Beverages

- 12.1.2.2.3. Coffee

- 12.1.2.2.4. Tea

- 12.1.2.2.5. Carbonated Beverages

- 12.1.2.2.6. Other Non-alcoholic Beverages

- 12.1.2.1. Alcoholic

- 12.1.1. Organic Foods

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Supermarkets/Hypermarkets

- 12.2.2. Convenience Stores

- 12.2.3. Specialist Stores

- 12.2.4. Online Retailing

- 12.2.5. Other Distribution Channels

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Germany European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 14. France European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 15. Italy European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 16. United Kingdom European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 17. Netherlands European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 18. Sweden European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 19. Rest of Europe European Organic Food Market Analysis, Insights and Forecast, 2019-2031

- 20. Competitive Analysis

- 20.1. Market Share Analysis 2024

- 20.2. Company Profiles

- 20.2.1 Narayan Foods

- 20.2.1.1. Overview

- 20.2.1.2. Products

- 20.2.1.3. SWOT Analysis

- 20.2.1.4. Recent Developments

- 20.2.1.5. Financials (Based on Availability)

- 20.2.2 Sasma BV

- 20.2.2.1. Overview

- 20.2.2.2. Products

- 20.2.2.3. SWOT Analysis

- 20.2.2.4. Recent Developments

- 20.2.2.5. Financials (Based on Availability)

- 20.2.3 General Mills Inc

- 20.2.3.1. Overview

- 20.2.3.2. Products

- 20.2.3.3. SWOT Analysis

- 20.2.3.4. Recent Developments

- 20.2.3.5. Financials (Based on Availability)

- 20.2.4 The Hain Celestial Group Inc

- 20.2.4.1. Overview

- 20.2.4.2. Products

- 20.2.4.3. SWOT Analysis

- 20.2.4.4. Recent Developments

- 20.2.4.5. Financials (Based on Availability)

- 20.2.5 Danone S A (The WhiteWave Foods Company)

- 20.2.5.1. Overview

- 20.2.5.2. Products

- 20.2.5.3. SWOT Analysis

- 20.2.5.4. Recent Developments

- 20.2.5.5. Financials (Based on Availability)

- 20.2.6 Clipper Teas

- 20.2.6.1. Overview

- 20.2.6.2. Products

- 20.2.6.3. SWOT Analysis

- 20.2.6.4. Recent Developments

- 20.2.6.5. Financials (Based on Availability)

- 20.2.7 Amy's Kitchen Inc

- 20.2.7.1. Overview

- 20.2.7.2. Products

- 20.2.7.3. SWOT Analysis

- 20.2.7.4. Recent Developments

- 20.2.7.5. Financials (Based on Availability)

- 20.2.8 Starbucks Corporation

- 20.2.8.1. Overview

- 20.2.8.2. Products

- 20.2.8.3. SWOT Analysis

- 20.2.8.4. Recent Developments

- 20.2.8.5. Financials (Based on Availability)

- 20.2.9 PureOrganic Drinks Limited*List Not Exhaustive

- 20.2.9.1. Overview

- 20.2.9.2. Products

- 20.2.9.3. SWOT Analysis

- 20.2.9.4. Recent Developments

- 20.2.9.5. Financials (Based on Availability)

- 20.2.10 Nestlé S A

- 20.2.10.1. Overview

- 20.2.10.2. Products

- 20.2.10.3. SWOT Analysis

- 20.2.10.4. Recent Developments

- 20.2.10.5. Financials (Based on Availability)

- 20.2.1 Narayan Foods

List of Figures

- Figure 1: European Organic Food Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European Organic Food Market Share (%) by Company 2024

List of Tables

- Table 1: European Organic Food Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European Organic Food Market Volume Tons Forecast, by Region 2019 & 2032

- Table 3: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 5: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 7: European Organic Food Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: European Organic Food Market Volume Tons Forecast, by Region 2019 & 2032

- Table 9: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 11: Germany European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Germany European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 13: France European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 15: Italy European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Italy European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 17: United Kingdom European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: United Kingdom European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 19: Netherlands European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Netherlands European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 21: Sweden European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Sweden European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 23: Rest of Europe European Organic Food Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe European Organic Food Market Volume (Tons) Forecast, by Application 2019 & 2032

- Table 25: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 26: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 27: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 28: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 29: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 30: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 31: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 32: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 33: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 34: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 35: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 36: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 37: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 38: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 39: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 40: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 41: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 42: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 43: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 44: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 45: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 46: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 47: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 48: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 49: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 50: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 51: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 52: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 53: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 54: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 55: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 56: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 57: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 58: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 59: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 60: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

- Table 61: European Organic Food Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 62: European Organic Food Market Volume Tons Forecast, by Product Type 2019 & 2032

- Table 63: European Organic Food Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 64: European Organic Food Market Volume Tons Forecast, by Distribution Channel 2019 & 2032

- Table 65: European Organic Food Market Revenue Million Forecast, by Country 2019 & 2032

- Table 66: European Organic Food Market Volume Tons Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Organic Food Market?

The projected CAGR is approximately 14.15%.

2. Which companies are prominent players in the European Organic Food Market?

Key companies in the market include Narayan Foods, Sasma BV, General Mills Inc, The Hain Celestial Group Inc, Danone S A (The WhiteWave Foods Company), Clipper Teas, Amy's Kitchen Inc, Starbucks Corporation, PureOrganic Drinks Limited*List Not Exhaustive, Nestlé S A.

3. What are the main segments of the European Organic Food Market?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 141.29 Million as of 2022.

5. What are some drivers contributing to market growth?

Inclination Towards Reduced Sugar and Healthier Snacking Options; Surge in Demand for Organic Food Products.

6. What are the notable trends driving market growth?

Growing Demand for Clean-label Products.

7. Are there any restraints impacting market growth?

Availability of Cheaper Snacking Options.

8. Can you provide examples of recent developments in the market?

In November 2022, in a partnership with Narayan Foods, a renowned player in organic foods, MeliBio, the first company that claims to produce real honey without bees, announced that it raised an extra USD 2.2 million in funding and planned to sell its products in 75,000 European stores. Through the partnership, Narayan Foods announced its plans to market MeliBio's plant-based honey under the Better Foodie brand, starting in early 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Organic Food Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Organic Food Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Organic Food Market?

To stay informed about further developments, trends, and reports in the European Organic Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence