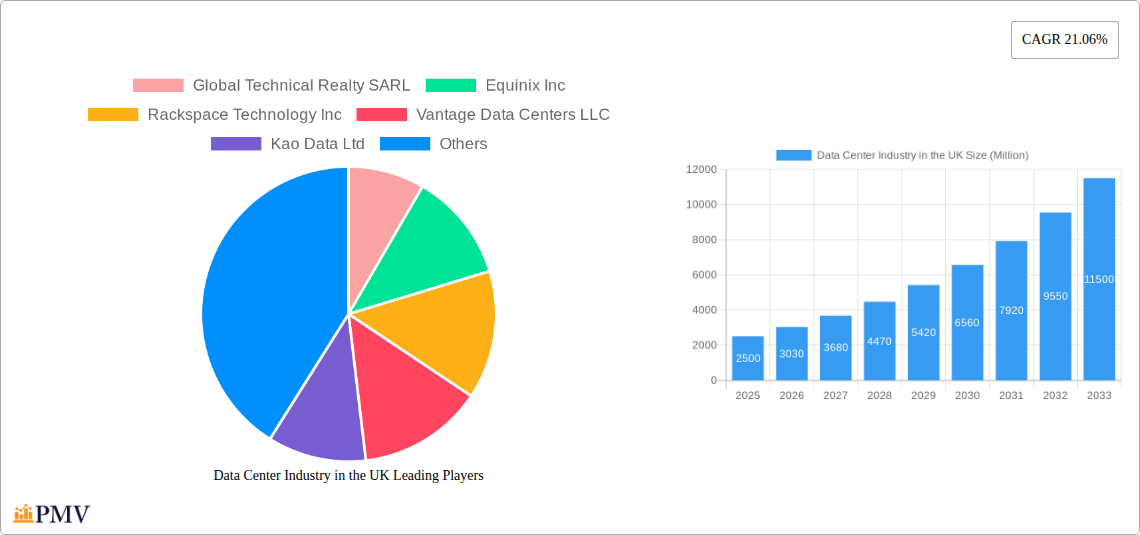

Key Insights

The UK data center market is experiencing robust growth, driven by the increasing adoption of cloud computing, the expansion of digital services, and the burgeoning demand for high-speed internet connectivity. A compound annual growth rate (CAGR) of 21.06% from 2019-2024 suggests a significant market expansion. This growth is fueled by several key trends, including the rising adoption of edge computing to reduce latency and improve responsiveness for applications, the increasing need for data sovereignty and compliance regulations, and the ongoing digital transformation initiatives across various sectors, particularly finance and technology. The market is segmented by tier type (Tier 1, Tier 2, Tier 3, Tier 4), utilization (utilized, non-utilized), end-user (other), hotspot regions (London, Rest of UK), and data center size (small, medium, mega, massive, large). London, as a major financial and technological hub, dominates the market, though significant growth is also evident across other UK regions. While challenges exist, including potential infrastructure limitations and energy costs, the overall market outlook remains highly positive. The presence of major players like Equinix, Digital Realty, and Global Switch, alongside several smaller but significant regional providers, demonstrates the market's maturity and competitive intensity. The continued investment in infrastructure and technological advancements indicates strong future prospects for UK data centers.

The significant investment from both domestic and international players points to a sustained period of growth. The market's segmentation offers opportunities for specialized providers to cater to specific client needs and further accelerate expansion. For example, the growth of edge data centers is expected to drive demand for smaller, strategically located facilities, while the expansion of cloud service providers will continue to drive demand for larger hyperscale data centers. Companies are adopting innovative solutions such as AI-powered optimization and sustainable energy sources to improve operational efficiency and meet environmental concerns. The robust growth trajectory is underpinned by the UK's supportive regulatory environment, skilled workforce, and strategic geographical location, ensuring a competitive edge in the global data center landscape. Continued focus on infrastructure development and digital innovation will be key to sustaining this growth trajectory throughout the forecast period (2025-2033).

Data Center Industry in the UK: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the UK data center market, encompassing market size, segmentation, competitive landscape, key trends, and future growth prospects. The study period covers 2019-2033, with 2025 serving as the base and estimated year. The report leverages extensive primary and secondary research to deliver actionable insights for stakeholders across the data center ecosystem. Market values are expressed in Millions.

Data Center Industry in the UK Market Structure & Competitive Dynamics

The UK data center market exhibits a moderately concentrated structure, with a handful of major players vying for market share. The competitive landscape is characterized by intense rivalry, driven by factors such as capacity expansion, technological advancements, and strategic acquisitions. Market concentration is further influenced by the presence of both global giants like Equinix and Digital Realty and smaller, agile providers specializing in niche segments. Regulatory frameworks, though generally supportive of digital infrastructure development, pose certain challenges, particularly regarding energy consumption and environmental impact. Product substitutes, while limited, include cloud computing services, which exerts indirect pressure on traditional data center operations. End-user trends favor hyperscale deployments, driving demand for large, high-capacity facilities. The M&A landscape has witnessed significant activity in recent years, with deal values reaching into the hundreds of Millions, reflecting consolidation within the sector.

- Market Share (2024 Estimate): Equinix (xx%), Digital Realty (xx%), Global Switch (xx%), Others (xx%).

- M&A Deal Value (2019-2024): £xx Million

Data Center Industry in the UK Industry Trends & Insights

The UK data center market is experiencing robust growth, propelled by a convergence of factors. Increased digitalization across sectors, fueled by the rise of cloud computing, big data analytics, and the Internet of Things (IoT), is a primary growth driver. The demand for low-latency connectivity and robust infrastructure is further supporting market expansion. Technological advancements, such as the adoption of AI and edge computing, are reshaping the industry landscape, driving innovation and creating new opportunities. Consumer preferences are shifting toward highly secure, resilient, and sustainable data center solutions. The compound annual growth rate (CAGR) during the forecast period (2025-2033) is projected to be xx%, with market penetration rates steadily increasing. Competitive dynamics remain intense, with providers focusing on differentiation through service offerings, operational efficiency, and strategic partnerships.

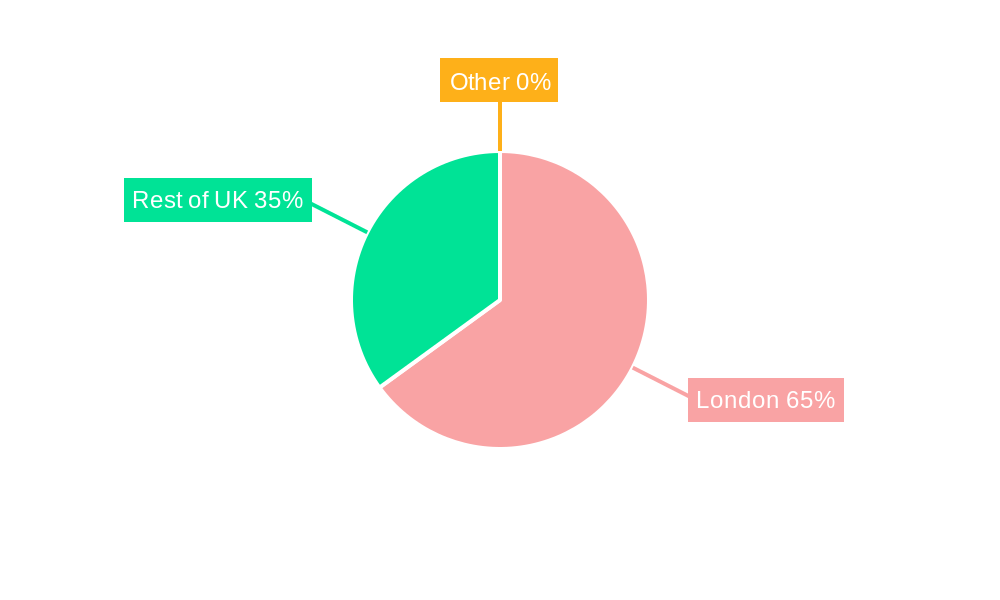

Dominant Markets & Segments in Data Center Industry in the UK

London remains the undisputed hotspot for data center activity in the UK, driven by its highly developed digital infrastructure, skilled workforce, and strong connectivity. However, other regions are emerging as key players, capitalizing on factors like lower operational costs and available land. The large and mega data center segments are experiencing significant growth, fueled by hyperscale deployments.

- Key Drivers of London's Dominance:

- Superior connectivity and network infrastructure.

- Concentration of major businesses and digital enterprises.

- Established talent pool in the technology sector.

- Government support for digital infrastructure development.

- Other Significant Regions: The rest of the UK is experiencing growth driven by regional business expansion and investment in digital infrastructure.

- Data Center Size: The demand for large and mega data centers is surging, with small and medium facilities catering to specific niche markets. Utilization rates are high, reflecting robust demand and limited available capacity. Non-utilized capacity represents a smaller portion of the total, indicative of a healthy, rapidly evolving market.

- Tier Type: Tier 1 and Tier 3 facilities are predominantly dominant, meeting the stringent requirements of large enterprises and hyperscalers.

Data Center Industry in the UK Product Innovations

Significant product innovations are reshaping the UK data center market. This includes advancements in cooling technologies aimed at improving energy efficiency, the adoption of modular data center designs to enhance scalability and reduce deployment times, and the increasing integration of renewable energy sources to address sustainability concerns. These innovations are enhancing the overall market competitiveness by offering greater efficiency, flexibility, and reduced environmental impact. The adoption of such technologies caters to the growing demands of energy-conscious customers and strengthens the long-term sustainability of the UK data center industry.

Report Segmentation & Scope

This report segments the UK data center market based on several key parameters:

- Tier Type: Tier 1, Tier 2, Tier 3, Tier 4 (Growth projections and market sizes are provided for each tier in the full report.)

- Absorption: Utilized and Non-Utilized capacity (Analysis of utilization rates and market trends for each segment.)

- End-User: Hyperscalers, enterprises, colocation providers (Competitive dynamics and market share for each end-user group.)

- Hotspot: London and Rest of the UK (Regional market analysis, highlighting key growth drivers and challenges.)

- Data Center Size: Small, Medium, Mega, Large, Massive (Market size and growth prospects for each size category.)

Key Drivers of Data Center Industry in the UK Growth

The growth of the UK data center industry is propelled by several key factors:

- Technological advancements: Adoption of AI, cloud computing, and IoT is creating massive demand for data storage and processing capabilities.

- Economic growth: Increased digitalization across various sectors is boosting investment in data center infrastructure.

- Government policies: Supportive regulations and incentives promote the development of digital infrastructure.

Challenges in the Data Center Industry in the UK Sector

Despite significant growth potential, several challenges exist:

- Energy costs: High electricity prices impact operational costs and profitability.

- Land availability: Finding suitable sites for large-scale data center deployments can be challenging.

- Competition: Intense competition necessitates continuous innovation and efficiency improvements.

Leading Players in the Data Center Industry in the UK Market

- Global Technical Realty SARL

- Equinix Inc

- Rackspace Technology Inc

- Vantage Data Centers LLC

- Kao Data Ltd

- Colt Technology Services

- Digital Realty Trust Inc

- CyrusOne Inc

- Telehouse (KDDI Corporation)

- Virtus Data Centres Properties Ltd (STT GDC)

- Global Switch Holdings Limited

- NTT Ltd

Key Developments in Data Center Industry in the UK Sector

- October 2022: CyrusOne announced plans for a new 90MW data center in Iver Heath, Buckinghamshire. This significantly expands capacity in the region.

- August 2022: Colt opened a new 50MW data center campus ('London 4') in Hayes, West London, tripling its UK footprint. This reinforces London's position as a major hub.

- March 2022: Kao Data began construction on a second 10MW facility in Harlow, expanding its presence outside London. This demonstrates growth beyond the capital city.

Strategic Data Center Industry in the UK Market Outlook

The UK data center market is poised for sustained growth, driven by ongoing digital transformation and increasing demand for high-performance computing. Strategic opportunities exist for providers who can effectively leverage technological advancements, optimize operational efficiency, and address the growing need for sustainable infrastructure solutions. The market will likely see further consolidation, with larger players acquiring smaller companies to gain scale and market share. Focus on edge computing, AI, and hyperscale deployments will shape future growth.

Data Center Industry in the UK Segmentation

-

1. Hotspot

- 1.1. London

- 1.2. Rest of United Kingdom

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

5. Colocation Type

- 5.1. Hyperscale

- 5.2. Retail

- 5.3. Wholesale

-

6. End User

- 6.1. BFSI

- 6.2. Cloud

- 6.3. E-Commerce

- 6.4. Government

- 6.5. Manufacturing

- 6.6. Media & Entertainment

- 6.7. Telecom

- 6.8. Other End User

Data Center Industry in the UK Segmentation By Geography

- 1. United Kingdom

Data Center Industry in the UK REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 21.06% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rise of E-Commerce; Flourishing Startup Culture

- 3.3. Market Restrains

- 3.3.1. Slow Penetration Rate in Developing Countries

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Data Center Industry in the UK Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. London

- 5.1.2. Rest of United Kingdom

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.5. Market Analysis, Insights and Forecast - by Colocation Type

- 5.5.1. Hyperscale

- 5.5.2. Retail

- 5.5.3. Wholesale

- 5.6. Market Analysis, Insights and Forecast - by End User

- 5.6.1. BFSI

- 5.6.2. Cloud

- 5.6.3. E-Commerce

- 5.6.4. Government

- 5.6.5. Manufacturing

- 5.6.6. Media & Entertainment

- 5.6.7. Telecom

- 5.6.8. Other End User

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. England Data Center Industry in the UK Analysis, Insights and Forecast, 2019-2031

- 7. Wales Data Center Industry in the UK Analysis, Insights and Forecast, 2019-2031

- 8. Scotland Data Center Industry in the UK Analysis, Insights and Forecast, 2019-2031

- 9. Northern Data Center Industry in the UK Analysis, Insights and Forecast, 2019-2031

- 10. Ireland Data Center Industry in the UK Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Global Technical Realty SARL

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Equinix Inc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Rackspace Technology Inc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Vantage Data Centers LLC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kao Data Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Colt Technology Services

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Digital Realty Trust Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 CyrusOne Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Telehouse (KDDI Corporation)

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Virtus Data Centres Properties Ltd (STT GDC)5 4 LIST OF COMPANIES STUDIE

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Global Switch Holdings Limited

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 NTT Ltd

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Global Technical Realty SARL

List of Figures

- Figure 1: Data Center Industry in the UK Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Data Center Industry in the UK Share (%) by Company 2024

List of Tables

- Table 1: Data Center Industry in the UK Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Data Center Industry in the UK Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 3: Data Center Industry in the UK Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 4: Data Center Industry in the UK Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 5: Data Center Industry in the UK Revenue Million Forecast, by Absorption 2019 & 2032

- Table 6: Data Center Industry in the UK Revenue Million Forecast, by Colocation Type 2019 & 2032

- Table 7: Data Center Industry in the UK Revenue Million Forecast, by End User 2019 & 2032

- Table 8: Data Center Industry in the UK Revenue Million Forecast, by Region 2019 & 2032

- Table 9: Data Center Industry in the UK Revenue Million Forecast, by Country 2019 & 2032

- Table 10: England Data Center Industry in the UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Wales Data Center Industry in the UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Scotland Data Center Industry in the UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Northern Data Center Industry in the UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Ireland Data Center Industry in the UK Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Data Center Industry in the UK Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 16: Data Center Industry in the UK Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 17: Data Center Industry in the UK Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 18: Data Center Industry in the UK Revenue Million Forecast, by Absorption 2019 & 2032

- Table 19: Data Center Industry in the UK Revenue Million Forecast, by Colocation Type 2019 & 2032

- Table 20: Data Center Industry in the UK Revenue Million Forecast, by End User 2019 & 2032

- Table 21: Data Center Industry in the UK Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Data Center Industry in the UK?

The projected CAGR is approximately 21.06%.

2. Which companies are prominent players in the Data Center Industry in the UK?

Key companies in the market include Global Technical Realty SARL, Equinix Inc, Rackspace Technology Inc, Vantage Data Centers LLC, Kao Data Ltd, Colt Technology Services, Digital Realty Trust Inc, CyrusOne Inc, Telehouse (KDDI Corporation), Virtus Data Centres Properties Ltd (STT GDC)5 4 LIST OF COMPANIES STUDIE, Global Switch Holdings Limited, NTT Ltd.

3. What are the main segments of the Data Center Industry in the UK?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption, Colocation Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-Commerce; Flourishing Startup Culture.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Slow Penetration Rate in Developing Countries.

8. Can you provide examples of recent developments in the market?

October 2022: CyrusOne announced that they proposed a new data center in Iver Heath, Buckinghamshire, UK. The site will have 10 data halls supporting around 90MW of capacity and the project would include a new on-site substation.August 2022: Coltannounced to open a new data center in Hayes, West London, that would more than triple its existing footprint in the UK capital. It will deliver a new purpose-built of 50MW in 2.1-hectare data center campus known as 'London 4'.March 2022: Kao Data announced plans for a second building for its Harlow campus in the UK. The company says construction is now underway on its second 10 MW facility outside London.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Data Center Industry in the UK," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Data Center Industry in the UK report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Data Center Industry in the UK?

To stay informed about further developments, trends, and reports in the Data Center Industry in the UK, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence