Key Insights

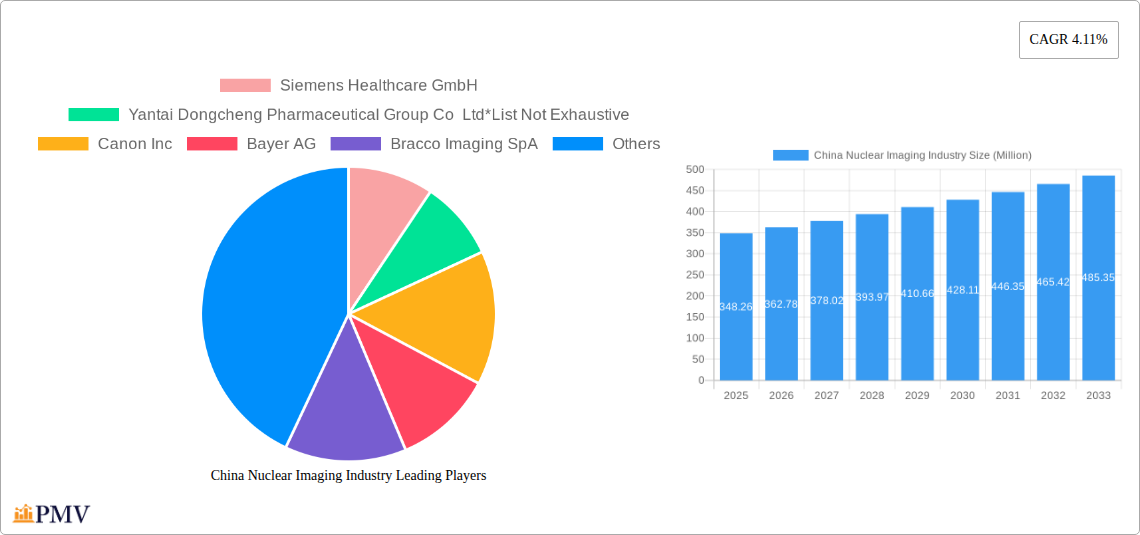

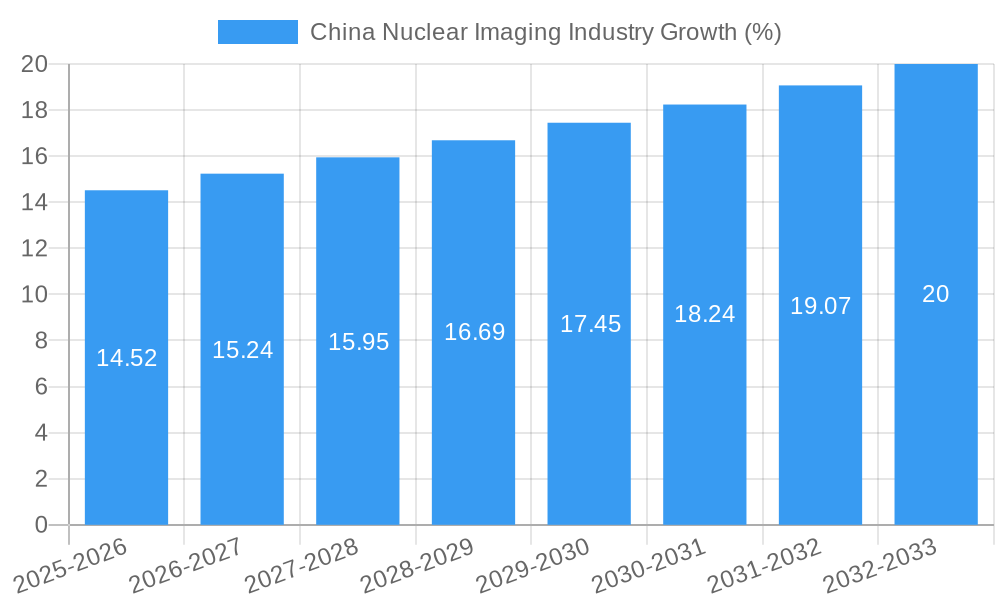

The China nuclear imaging market, valued at $348.26 million in 2025, is projected to experience robust growth, driven by a rising prevalence of chronic diseases like cancer and cardiovascular ailments necessitating advanced diagnostic tools. The market's Compound Annual Growth Rate (CAGR) of 4.11% from 2025 to 2033 indicates a steady expansion, fueled by increasing government healthcare expenditure, growing adoption of minimally invasive procedures, and technological advancements in imaging equipment. Specifically, the demand for PET and SPECT radioisotopes is expected to significantly contribute to market growth, particularly Technetium-99m (Tc-99m) which holds the largest share within the SPECT segment due to its widespread use in various diagnostic applications. The segment encompassing PET applications will likely see above-average growth, driven by the superior image resolution and functional information provided by PET scans compared to conventional imaging techniques. Leading players like Siemens Healthcare, Canon, and Philips are strategically investing in research and development, focusing on improving image quality, reducing radiation exposure, and expanding their product portfolio. The competitive landscape is characterized by a mix of global and domestic companies, with domestic players benefiting from government support and growing domestic demand.

The market's growth is however, subject to certain restraints. These include stringent regulatory approvals for new imaging technologies and the high cost associated with both the equipment and the radioisotopes. Nevertheless, the increasing awareness of the advantages of nuclear imaging among healthcare professionals and patients, combined with the government's focus on improving healthcare infrastructure, is expected to mitigate these challenges and fuel consistent market expansion over the forecast period. Expansion into rural areas and the development of more affordable imaging solutions could further accelerate market penetration and benefit a wider patient population. Specific growth drivers within individual segments may vary based on technological improvements and government funding schemes.

This comprehensive report provides an in-depth analysis of the China Nuclear Imaging Industry, covering market size, segmentation, competitive landscape, and future growth prospects. The report utilizes data from the historical period (2019-2024), the base year (2025), and projects forecasts to 2033. The study period is 2019-2033, and the estimated year is 2025. This report is crucial for businesses, investors, and stakeholders seeking to understand and capitalize on opportunities within this rapidly evolving market.

China Nuclear Imaging Industry Market Structure & Competitive Dynamics

The China nuclear imaging market exhibits a moderately concentrated structure, with several multinational corporations and domestic players vying for market share. Market concentration is influenced by factors such as regulatory approvals, technological advancements, and strategic partnerships. The market is characterized by a dynamic innovation ecosystem, with ongoing research and development efforts focused on enhancing imaging technologies and expanding their applications. Stringent regulatory frameworks govern the production, distribution, and use of radioisotopes and imaging equipment, influencing market entry and operations. Product substitutes, such as MRI and ultrasound, pose some competitive pressure, though nuclear imaging holds a distinct advantage for specific diagnostic applications. End-user trends favor increased adoption of advanced imaging techniques for improved diagnostic accuracy and personalized medicine. M&A activities have played a significant role in shaping the market landscape, with several high-value deals reshaping the competitive dynamics. For example, a recent deal between xx and xx was valued at xx Million. While precise market share data is proprietary, it's estimated that the top five players collectively account for approximately xx% of the market.

China Nuclear Imaging Industry Industry Trends & Insights

The China nuclear imaging market is experiencing robust growth, driven by factors such as increasing prevalence of chronic diseases, rising healthcare expenditure, and growing government support for healthcare infrastructure development. Technological advancements, particularly in PET and SPECT imaging, are fueling market expansion, offering enhanced image quality, faster scanning times, and improved diagnostic capabilities. Consumer preferences are shifting towards minimally invasive procedures and personalized treatment plans, increasing the demand for advanced nuclear imaging technologies. The market is witnessing heightened competition, leading to the development of innovative products, competitive pricing strategies, and strategic alliances. The market's compound annual growth rate (CAGR) from 2025 to 2033 is estimated to be approximately xx%, signifying substantial growth potential. Market penetration of advanced nuclear imaging technologies is steadily increasing, particularly in urban areas with better healthcare infrastructure.

Dominant Markets & Segments in China Nuclear Imaging Industry

The eastern coastal regions of China, including major cities such as Beijing, Shanghai, and Guangzhou, dominate the nuclear imaging market due to higher healthcare spending, better healthcare infrastructure, and a large concentration of specialized hospitals.

- Key Drivers:

- Robust economic growth leading to increased healthcare expenditure.

- Favorable government policies supporting healthcare infrastructure development.

- Growing awareness of the benefits of early disease detection.

Within segments:

- By Product: Equipment holds a larger market share compared to radioisotopes due to the higher cost of advanced imaging equipment. However, the radioisotope segment is expected to experience significant growth due to the increasing demand for advanced nuclear medicine applications.

- By Application: PET applications are rapidly expanding due to their superior diagnostic capabilities in oncology, while SPECT applications remain significant in cardiology and neurology.

- SPECT Radioisotopes: Technetium-99m (Tc-99m) dominates the SPECT market due to its widespread use in various diagnostic procedures.

- PET Radioisotopes: Fluorine-18 (F-18) accounts for a large portion of PET radioisotope usage owing to its importance in oncology imaging.

The dominance is primarily attributed to higher patient volumes, greater concentration of healthcare professionals and specialized centers, and a stronger regulatory environment supporting the adoption of advanced nuclear imaging techniques.

China Nuclear Imaging Industry Product Innovations

Recent advancements include the development of more sensitive detectors, improved image reconstruction algorithms, and the introduction of new radiotracers for improved diagnostic accuracy and specificity. These innovations are improving image quality, reducing radiation exposure, and expanding the clinical applications of nuclear imaging. Furthermore, the integration of AI and machine learning is enhancing diagnostic workflow, improving the interpretation of images, and enabling more efficient diagnosis. Companies are focusing on developing compact and portable imaging systems to improve accessibility in underserved areas.

Report Segmentation & Scope

This report segments the China nuclear imaging market by product (equipment and radioisotopes) and application (SPECT and PET).

- Equipment: This segment includes SPECT and PET scanners, gamma cameras, and related accessories. Growth is driven by technological advancements and an increasing number of diagnostic centers. The market is highly competitive, with both multinational and domestic players.

- Radioisotopes: This segment encompasses SPECT and PET radioisotopes, with Technetium-99m and Fluorine-18 holding the largest market share. Growth is linked to an increased demand for nuclear medicine procedures. The market is characterized by several key players, including both multinational companies and domestic manufacturers.

- SPECT Applications: Primarily focused on cardiology and neurology.

- PET Applications: Predominantly used in oncology for cancer detection and staging. Growth is projected to be the fastest due to increasing cancer incidence.

Key Drivers of China Nuclear Imaging Industry Growth

The industry's growth is spurred by: (1) rising prevalence of chronic diseases like cancer and cardiovascular illnesses demanding advanced diagnostics; (2) substantial investments in healthcare infrastructure, creating more centers equipped for nuclear imaging; and (3) supportive government policies encouraging the adoption of advanced medical technologies.

Challenges in the China Nuclear Imaging Industry Sector

Challenges include: (1) high initial investment costs for equipment acquisition; (2) stringent regulatory approvals and licensing processes which create significant barriers to market entry; and (3) managing the supply chain for radioisotopes due to limited domestic production capabilities leading to a reliance on imports in certain segments. These factors could hinder market growth if not properly addressed.

Leading Players in the China Nuclear Imaging Industry Market

- Siemens Healthcare GmbH

- Yantai Dongcheng Pharmaceutical Group Co Ltd

- Canon Inc

- Bayer AG

- Bracco Imaging SpA

- Cardinal Health Inc

- Global Medical Solutions Ltd

- China Isotope & Radiation Corporation (CIRC)

- Koninklijke Philips NV

- Curium Pharma

- General Electric Company (GE HealthCare)

Key Developments in China Nuclear Imaging Industry Sector

- August 2022: IBA's collaboration with CNRT for Cyclone IKON installation signifies advancements in PET and SPECT isotope production capacity within China, boosting domestic supply and potentially reducing reliance on imports.

- January 2022: ImaginAb and DongCheng Pharmaceutical Group's partnership for ImmunoPET agent introduction indicates the growing interest in novel radiopharmaceuticals and personalized medicine within the Chinese market.

Strategic China Nuclear Imaging Industry Market Outlook

The China nuclear imaging market is poised for continued expansion, driven by favorable demographics, technological progress, and government support. Strategic opportunities exist in developing innovative products, expanding into underserved regions, and forging strategic partnerships to capitalize on market growth. Investment in research and development, along with collaborations between domestic and international companies, will play a vital role in shaping the future of this dynamic industry.

China Nuclear Imaging Industry Segmentation

-

1. Product

- 1.1. Equipment

-

1.2. Radioisotope

-

1.2.1. SPECT Radioisotopes

- 1.2.1.1. Technetium-99m (TC-99m)

- 1.2.1.2. Thallium-201 (TI-201)

- 1.2.1.3. Gallium (Ga-67)

- 1.2.1.4. Iodine (I-123)

- 1.2.1.5. Other SPECT Radioisotopes

-

1.2.2. PET Radioisotopes

- 1.2.2.1. Fluorine-18 (F-18)

- 1.2.2.2. Rubidium-82 (RB-82)

- 1.2.2.3. Other PET Radioisotopes

-

1.2.1. SPECT Radioisotopes

-

2. Application

-

2.1. SPECT Applications

- 2.1.1. Neurology

- 2.1.2. Cardiology

- 2.1.3. Thyroid

- 2.1.4. Other SPECT Applications

-

2.2. PET Applications

- 2.2.1. Oncology

- 2.2.2. Other PET Applications

-

2.1. SPECT Applications

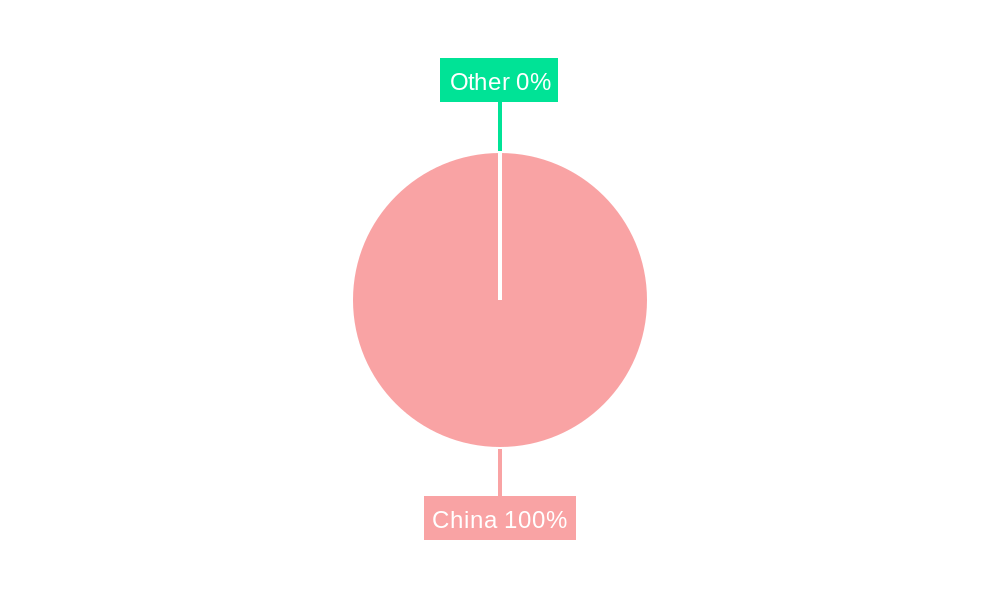

China Nuclear Imaging Industry Segmentation By Geography

- 1. China

China Nuclear Imaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.11% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Burden of Chronic Diseases; Increasing Technological Advancements with Growth in Applications of Nuclear Imaging

- 3.3. Market Restrains

- 3.3.1. High Cost of the Techniques; Short Half-life of Radiopharmaceuticals

- 3.4. Market Trends

- 3.4.1. Neurology Under SPECT Application Segment is Expected to Grow with a Significant CAGR Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Nuclear Imaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Equipment

- 5.1.2. Radioisotope

- 5.1.2.1. SPECT Radioisotopes

- 5.1.2.1.1. Technetium-99m (TC-99m)

- 5.1.2.1.2. Thallium-201 (TI-201)

- 5.1.2.1.3. Gallium (Ga-67)

- 5.1.2.1.4. Iodine (I-123)

- 5.1.2.1.5. Other SPECT Radioisotopes

- 5.1.2.2. PET Radioisotopes

- 5.1.2.2.1. Fluorine-18 (F-18)

- 5.1.2.2.2. Rubidium-82 (RB-82)

- 5.1.2.2.3. Other PET Radioisotopes

- 5.1.2.1. SPECT Radioisotopes

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. SPECT Applications

- 5.2.1.1. Neurology

- 5.2.1.2. Cardiology

- 5.2.1.3. Thyroid

- 5.2.1.4. Other SPECT Applications

- 5.2.2. PET Applications

- 5.2.2.1. Oncology

- 5.2.2.2. Other PET Applications

- 5.2.1. SPECT Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Siemens Healthcare GmbH

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Yantai Dongcheng Pharmaceutical Group Co Ltd*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Canon Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Bayer AG

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Bracco Imaging SpA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Cardinal Health Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Global Medical Solutions Ltd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 China Isotope & Radiation Corporation (CIRC)

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Koninklijke Philips NV

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Curium Pharma

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 General Electric Company (GE HealthCare)

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 Siemens Healthcare GmbH

List of Figures

- Figure 1: China Nuclear Imaging Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Nuclear Imaging Industry Share (%) by Company 2024

List of Tables

- Table 1: China Nuclear Imaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Nuclear Imaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: China Nuclear Imaging Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: China Nuclear Imaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: China Nuclear Imaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China Nuclear Imaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 7: China Nuclear Imaging Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 8: China Nuclear Imaging Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Nuclear Imaging Industry?

The projected CAGR is approximately 4.11%.

2. Which companies are prominent players in the China Nuclear Imaging Industry?

Key companies in the market include Siemens Healthcare GmbH, Yantai Dongcheng Pharmaceutical Group Co Ltd*List Not Exhaustive, Canon Inc, Bayer AG, Bracco Imaging SpA, Cardinal Health Inc, Global Medical Solutions Ltd, China Isotope & Radiation Corporation (CIRC), Koninklijke Philips NV, Curium Pharma, General Electric Company (GE HealthCare).

3. What are the main segments of the China Nuclear Imaging Industry?

The market segments include Product, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 348.26 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Burden of Chronic Diseases; Increasing Technological Advancements with Growth in Applications of Nuclear Imaging.

6. What are the notable trends driving market growth?

Neurology Under SPECT Application Segment is Expected to Grow with a Significant CAGR Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of the Techniques; Short Half-life of Radiopharmaceuticals.

8. Can you provide examples of recent developments in the market?

August 2022: IBA (Ion Beam Applications S.A), a provider of radiopharmaceutical production solutions, signed a collaboration agreement with Chengdu New Radiomedicine Technology Co. Ltd (CNRT) to install a Cyclone IKON in Chengdu, Sichuan Province, China. The Cyclone IKON is IBA's new high-energy and high-capacity cyclotron which offers the largest energy spectrum for PET and SPECT isotopes from 13 MeV to 30 MeV. CNRT is a Chinese manufacturer and provider of medical isotopes used for oncology diagnosis and therapy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Nuclear Imaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Nuclear Imaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Nuclear Imaging Industry?

To stay informed about further developments, trends, and reports in the China Nuclear Imaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence