Key Insights

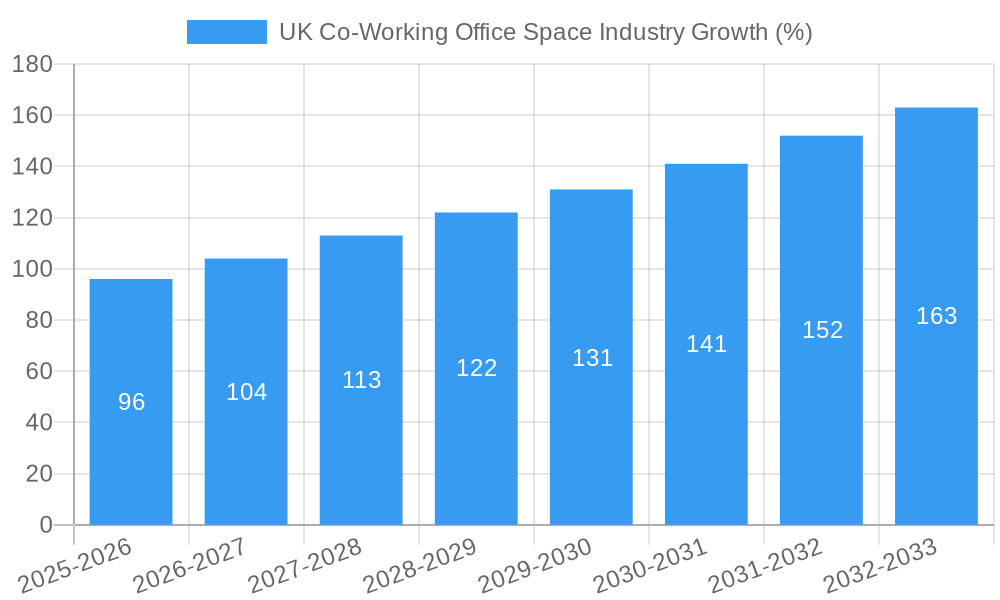

The UK co-working office space industry is experiencing robust growth, driven by the increasing preference for flexible work arrangements among freelancers, startups, and established businesses alike. The market, valued at £1.34 billion in 2025, exhibits a Compound Annual Growth Rate (CAGR) of 7.11%, projecting significant expansion through 2033. This growth is fueled by several factors. The rising popularity of remote work and hybrid work models, especially post-pandemic, has led to a surge in demand for flexible, shared workspaces. Furthermore, co-working spaces offer cost-effective solutions compared to traditional leased offices, eliminating upfront capital expenditure and long-term commitments. Technological advancements, such as improved booking systems and virtual office solutions, are further enhancing the appeal and accessibility of co-working spaces. The industry is segmented by end-user type, with personal users, small-scale companies, and large-scale companies comprising the majority of the market. Competition is intensifying, with established players like Regus and The Office Group facing competition from smaller, niche providers focusing on specific industries or demographics. While economic downturns could potentially restrain growth, the inherent flexibility and adaptability of the co-working model suggest sustained demand even during economic uncertainty. Regional variations exist across England, Wales, Scotland, and Northern Ireland, with London likely dominating the market due to its concentration of businesses and professionals.

The continued expansion of the UK co-working office space market hinges on several key trends. The increasing adoption of sustainability initiatives by co-working providers is attracting environmentally conscious businesses. Furthermore, the integration of community-building initiatives and networking opportunities within these spaces is becoming a significant differentiator, attracting clients seeking collaborative work environments. However, challenges persist. Securing suitable locations with competitive rental costs remains crucial for operators, while maintaining profitability in a competitive market requires efficient management and operational strategies. Government regulations related to workspace safety and accessibility also play a significant role in shaping the industry's landscape. Future growth will depend on the industry's ability to innovate, adapt to evolving work patterns, and offer value-added services that cater to the diverse needs of its clientele. The long-term outlook for the UK co-working office space market remains positive, indicating a significant opportunity for growth and investment.

UK Co-Working Office Space Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the UK co-working office space industry, covering market structure, competitive dynamics, key trends, and future growth prospects from 2019 to 2033. The report utilizes data from the historical period (2019-2024), base year (2025), and estimated year (2025) to forecast market trends until 2033. The analysis incorporates insights from major players such as The Office Group, Regus, WeWork, and many others, providing a 360° view of this dynamic sector. This report is essential for investors, industry professionals, and businesses seeking to understand and capitalize on opportunities within the UK co-working market. The total market value is predicted to reach xx Million by 2033.

UK Co-Working Office Space Industry Market Structure & Competitive Dynamics

The UK co-working office space market presents a dynamic landscape characterized by moderate concentration, with a few major players holding a substantial market share alongside a multitude of smaller, localized operators. While the top three players commanded an estimated 35% of the market share in 2025, this concentration is tempered by a vibrant and innovative ecosystem. High initial capital investment and ongoing operational costs create significant barriers to entry, yet companies continuously introduce cutting-edge technologies and tailored service offerings to differentiate themselves and attract a diverse clientele. This ongoing innovation is a key driver of the industry's evolution.

The regulatory environment significantly influences the market, impacting everything from building codes and safety regulations to lease agreements and operational compliance. The burgeoning trend of flexible work arrangements and the increasing preference for collaborative workspaces are powerful growth catalysts. Although traditional leased offices and home offices remain viable alternatives, the unique value proposition of co-working spaces—namely, fostering networking opportunities and offering flexible, scalable solutions—continues to fuel strong demand. The sector also displays notable M&A activity, primarily driven by consolidation and expansion strategies. In 2024, the total value of these transactions reached approximately xx Million, reflecting the ongoing industry reshaping.

- Market Concentration: Top 3 players held approximately 35% market share (2025), indicating a moderately consolidated market.

- Innovation: Continuous technological advancements and service diversification are key competitive differentiators.

- Regulatory Landscape: Compliance with building codes, safety regulations, and lease agreements is crucial for operational success.

- M&A Activity: Significant consolidation and expansion through mergers and acquisitions, totaling approximately xx Million in 2024.

- Substitutes: Traditional leased offices and home offices represent key competitive alternatives.

UK Co-Working Office Space Industry Industry Trends & Insights

The UK co-working office space industry has experienced robust growth, driven by several key factors. The increasing adoption of flexible work models, fueled by the rise of remote work and the gig economy, has significantly contributed to this expansion. Technological advancements, such as smart building technologies and integrated workspace management systems, are improving efficiency and enhancing the user experience. Consumer preferences are shifting towards more collaborative and flexible work environments, fostering demand for co-working spaces.

The industry is also characterized by intense competition, with established players and new entrants continuously vying for market share. This competitive landscape drives innovation and keeps prices competitive. The Compound Annual Growth Rate (CAGR) for the market is projected to be xx% during the forecast period (2025-2033), indicating substantial growth potential. Market penetration has increased significantly, particularly among small and medium-sized enterprises (SMEs), who are drawn to the affordability and flexibility of co-working spaces. However, economic fluctuations and changing business landscapes could influence the trajectory of growth.

Dominant Markets & Segments in UK Co-Working Office Space Industry

London remains the undisputed leader in the UK co-working market, fueled by its high concentration of businesses, a large pool of skilled professionals, and a robust infrastructure that supports a thriving business ecosystem. London's strong economic policies and diverse talent pool further solidify its position as the industry's central hub. Regarding end-user segments, small-scale companies constitute the largest market share, drawn to the cost-effectiveness and scalability offered by co-working spaces. However, large-scale companies are increasingly adopting co-working solutions for specific projects or teams, indicating a broadening appeal across business sizes.

- Key Drivers of London's Dominance:

- High concentration of businesses and professionals.

- Robust and well-developed infrastructure.

- Supportive economic policies fostering business growth.

- A vast and diverse talent pool.

- Largest End-User Segment: Small-scale companies, attracted by affordability and flexibility.

- Growing Segment: Large-scale companies utilizing co-working for specific projects or teams, representing an emerging opportunity.

UK Co-Working Office Space Industry Product Innovations

Recent innovations within the UK co-working industry reflect a focus on enhanced user experience and operational efficiency. These include the integration of smart building technologies to improve energy efficiency and workspace management; the development of specialized spaces catering to niche industry needs, such as tech startups or creative agencies; and the creation of flexible membership plans offering tailored services and amenities. These advancements are crucial for providers seeking to enhance value propositions and maintain a competitive edge in a rapidly evolving market. The adoption of technological solutions is becoming increasingly vital for success.

Report Segmentation & Scope

This report segments the UK co-working office space market by end-user type:

Personal Users: Including freelancers, independent contractors, and individuals, this segment projects xx% growth from 2025 to 2033. Competition is primarily driven by pricing and the availability of attractive amenities.

Small-Scale Companies: Encompassing startups, SMEs, and small businesses, this key segment projects xx% growth from 2025 to 2033. The market is highly competitive, with providers focusing on attracting this significant demographic.

Large-Scale Companies: This segment includes corporations and large enterprises utilizing co-working for specific projects or teams, with projected growth of xx% from 2025 to 2033. Competition hinges on superior service quality and premium offerings.

Other End Users: Including educational institutions and government agencies, this segment projects xx% growth from 2025 to 2033 and represents a relatively less developed area compared to others.

Key Drivers of UK Co-Working Office Space Industry Growth

Several factors propel the growth of the UK co-working office space industry: the rise of the gig economy and remote work, increasing demand for flexible work arrangements, technological advancements improving workspace efficiency, and government initiatives promoting entrepreneurship and innovation. The ongoing shift towards activity-based working models also fuels demand for flexible, collaborative spaces.

Challenges in the UK Co-Working Office Space Industry Sector

The UK co-working industry faces several key challenges, including intense competition, economic volatility impacting demand, rising operating costs, and the difficulty of securing suitable locations in prime areas. The lingering effects of the pandemic—initially depressing the market but recently contributing to a resurgence—continue to influence growth projections and operational strategies. These factors highlight the need for ongoing adaptability and innovative solutions within the sector.

Leading Players in the UK Co-Working Office Space Industry Market

- Jactin House

- The Skiff

- Work Well Offices

- Soho Works

- The Brew

- Wimbletech CIC

- The Hoxton

- Mare Street Market

- Southbank Centre

- The Office Group

- Regus

- Huckle Tree

- Creative Works

- Labs

- Foyles

- Icon Offices

Key Developments in UK Co-Working Office Space Industry Sector

May 2023: Amazon leased 70,000 sq. ft of WeWork office space in London, signifying the continued attractiveness of co-working spaces for large corporations.

July 2023: WeWork announced a franchise partnership with Garnier & Garnier in Costa Rica, expanding its global footprint and indicating the growing international interest in the co-working model.

Strategic UK Co-Working Office Space Industry Market Outlook

The UK co-working office space market presents significant growth potential driven by ongoing trends in flexible work arrangements, technological advancements, and the increasing demand for collaborative work environments. Strategic opportunities exist for providers who can effectively adapt to evolving market needs, leverage technology, and offer innovative solutions that cater to the specific requirements of diverse user segments. The market is expected to continue its expansion, driven by both established players and new entrants, creating a dynamic and competitive landscape.

UK Co-Working Office Space Industry Segmentation

-

1. End User

- 1.1. Personal User

- 1.2. Small Scale Company

- 1.3. Large Scale Company

- 1.4. Other End Users

-

2. Geography

- 2.1. London

- 2.2. Manchester

- 2.3. Birmingham

- 2.4. Leeds

- 2.5. Other UK Cities

-

3. Type

- 3.1. Flexible Managed Office

- 3.2. Serviced Office

-

4. Application

- 4.1. Information Technology (IT and ITES)

- 4.2. Legal Services

- 4.3. BFSI (Banking, Financial Services, and Insurance)

- 4.4. Consulting

- 4.5. Other Applications

UK Co-Working Office Space Industry Segmentation By Geography

- 1. London

- 2. Manchester

- 3. Birmingham

- 4. Leeds

- 5. Other UK Cities

UK Co-Working Office Space Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.11% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Shift Toward Co-working Spaces is Driving the Market4.; Increasing Focus on Sustainability is Driving the Market

- 3.3. Market Restrains

- 3.3.1. 4.; Economic Uncertainty is Affecting the Market

- 3.4. Market Trends

- 3.4.1. The Demand for Landlord-Fitted Office Space Surges Amid Rising Costs and Shrinking Availability

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Personal User

- 5.1.2. Small Scale Company

- 5.1.3. Large Scale Company

- 5.1.4. Other End Users

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. London

- 5.2.2. Manchester

- 5.2.3. Birmingham

- 5.2.4. Leeds

- 5.2.5. Other UK Cities

- 5.3. Market Analysis, Insights and Forecast - by Type

- 5.3.1. Flexible Managed Office

- 5.3.2. Serviced Office

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Information Technology (IT and ITES)

- 5.4.2. Legal Services

- 5.4.3. BFSI (Banking, Financial Services, and Insurance)

- 5.4.4. Consulting

- 5.4.5. Other Applications

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. London

- 5.5.2. Manchester

- 5.5.3. Birmingham

- 5.5.4. Leeds

- 5.5.5. Other UK Cities

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. London UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by End User

- 6.1.1. Personal User

- 6.1.2. Small Scale Company

- 6.1.3. Large Scale Company

- 6.1.4. Other End Users

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. London

- 6.2.2. Manchester

- 6.2.3. Birmingham

- 6.2.4. Leeds

- 6.2.5. Other UK Cities

- 6.3. Market Analysis, Insights and Forecast - by Type

- 6.3.1. Flexible Managed Office

- 6.3.2. Serviced Office

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Information Technology (IT and ITES)

- 6.4.2. Legal Services

- 6.4.3. BFSI (Banking, Financial Services, and Insurance)

- 6.4.4. Consulting

- 6.4.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by End User

- 7. Manchester UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by End User

- 7.1.1. Personal User

- 7.1.2. Small Scale Company

- 7.1.3. Large Scale Company

- 7.1.4. Other End Users

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. London

- 7.2.2. Manchester

- 7.2.3. Birmingham

- 7.2.4. Leeds

- 7.2.5. Other UK Cities

- 7.3. Market Analysis, Insights and Forecast - by Type

- 7.3.1. Flexible Managed Office

- 7.3.2. Serviced Office

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. Information Technology (IT and ITES)

- 7.4.2. Legal Services

- 7.4.3. BFSI (Banking, Financial Services, and Insurance)

- 7.4.4. Consulting

- 7.4.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by End User

- 8. Birmingham UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by End User

- 8.1.1. Personal User

- 8.1.2. Small Scale Company

- 8.1.3. Large Scale Company

- 8.1.4. Other End Users

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. London

- 8.2.2. Manchester

- 8.2.3. Birmingham

- 8.2.4. Leeds

- 8.2.5. Other UK Cities

- 8.3. Market Analysis, Insights and Forecast - by Type

- 8.3.1. Flexible Managed Office

- 8.3.2. Serviced Office

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. Information Technology (IT and ITES)

- 8.4.2. Legal Services

- 8.4.3. BFSI (Banking, Financial Services, and Insurance)

- 8.4.4. Consulting

- 8.4.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by End User

- 9. Leeds UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by End User

- 9.1.1. Personal User

- 9.1.2. Small Scale Company

- 9.1.3. Large Scale Company

- 9.1.4. Other End Users

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. London

- 9.2.2. Manchester

- 9.2.3. Birmingham

- 9.2.4. Leeds

- 9.2.5. Other UK Cities

- 9.3. Market Analysis, Insights and Forecast - by Type

- 9.3.1. Flexible Managed Office

- 9.3.2. Serviced Office

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. Information Technology (IT and ITES)

- 9.4.2. Legal Services

- 9.4.3. BFSI (Banking, Financial Services, and Insurance)

- 9.4.4. Consulting

- 9.4.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by End User

- 10. Other UK Cities UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by End User

- 10.1.1. Personal User

- 10.1.2. Small Scale Company

- 10.1.3. Large Scale Company

- 10.1.4. Other End Users

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. London

- 10.2.2. Manchester

- 10.2.3. Birmingham

- 10.2.4. Leeds

- 10.2.5. Other UK Cities

- 10.3. Market Analysis, Insights and Forecast - by Type

- 10.3.1. Flexible Managed Office

- 10.3.2. Serviced Office

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. Information Technology (IT and ITES)

- 10.4.2. Legal Services

- 10.4.3. BFSI (Banking, Financial Services, and Insurance)

- 10.4.4. Consulting

- 10.4.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by End User

- 11. England UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 12. Wales UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 13. Scotland UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 14. Northern UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 15. Ireland UK Co-Working Office Space Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Jactin House

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 The Skiff

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Work Well Offices

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Soho Works

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 The Brew

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Wimbletech CIC

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 The Hoxton

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Mare Street Market

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Southbank Centre**List Not Exhaustive 6 3 Other Companie

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 The Office Group

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Regus

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Huckle Tree

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Creative Works

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Labs

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 Foyles

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.16 Icon Offices

- 16.2.16.1. Overview

- 16.2.16.2. Products

- 16.2.16.3. SWOT Analysis

- 16.2.16.4. Recent Developments

- 16.2.16.5. Financials (Based on Availability)

- 16.2.1 Jactin House

List of Figures

- Figure 1: UK Co-Working Office Space Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: UK Co-Working Office Space Industry Share (%) by Company 2024

List of Tables

- Table 1: UK Co-Working Office Space Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: UK Co-Working Office Space Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 3: UK Co-Working Office Space Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 4: UK Co-Working Office Space Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 5: UK Co-Working Office Space Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 6: UK Co-Working Office Space Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 7: UK Co-Working Office Space Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: England UK Co-Working Office Space Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Wales UK Co-Working Office Space Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Scotland UK Co-Working Office Space Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Northern UK Co-Working Office Space Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Ireland UK Co-Working Office Space Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: UK Co-Working Office Space Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 14: UK Co-Working Office Space Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 15: UK Co-Working Office Space Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: UK Co-Working Office Space Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: UK Co-Working Office Space Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: UK Co-Working Office Space Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 19: UK Co-Working Office Space Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 20: UK Co-Working Office Space Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 21: UK Co-Working Office Space Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 22: UK Co-Working Office Space Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: UK Co-Working Office Space Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 24: UK Co-Working Office Space Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 25: UK Co-Working Office Space Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 26: UK Co-Working Office Space Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 27: UK Co-Working Office Space Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: UK Co-Working Office Space Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 29: UK Co-Working Office Space Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 30: UK Co-Working Office Space Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 31: UK Co-Working Office Space Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 32: UK Co-Working Office Space Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 33: UK Co-Working Office Space Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 34: UK Co-Working Office Space Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 35: UK Co-Working Office Space Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 36: UK Co-Working Office Space Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 37: UK Co-Working Office Space Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Co-Working Office Space Industry?

The projected CAGR is approximately 7.11%.

2. Which companies are prominent players in the UK Co-Working Office Space Industry?

Key companies in the market include Jactin House, The Skiff, Work Well Offices, Soho Works, The Brew, Wimbletech CIC, The Hoxton, Mare Street Market, Southbank Centre**List Not Exhaustive 6 3 Other Companie, The Office Group, Regus, Huckle Tree, Creative Works, Labs, Foyles, Icon Offices.

3. What are the main segments of the UK Co-Working Office Space Industry?

The market segments include End User, Geography, Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.34 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Shift Toward Co-working Spaces is Driving the Market4.; Increasing Focus on Sustainability is Driving the Market.

6. What are the notable trends driving market growth?

The Demand for Landlord-Fitted Office Space Surges Amid Rising Costs and Shrinking Availability.

7. Are there any restraints impacting market growth?

4.; Economic Uncertainty is Affecting the Market.

8. Can you provide examples of recent developments in the market?

May 2023: Amazon took over WeWork Cos.' 70,000 sq. ft office space in London. The tech giant will take over WeWork's refurbished Moore Place office building, which is estimated to house around 1,000 employees.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Co-Working Office Space Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Co-Working Office Space Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Co-Working Office Space Industry?

To stay informed about further developments, trends, and reports in the UK Co-Working Office Space Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence