Key Insights

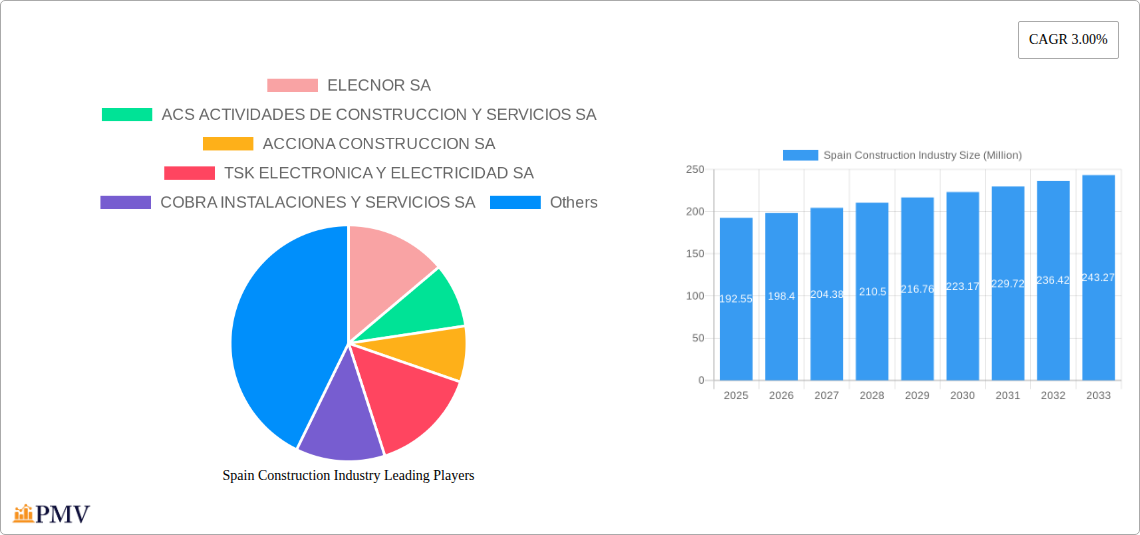

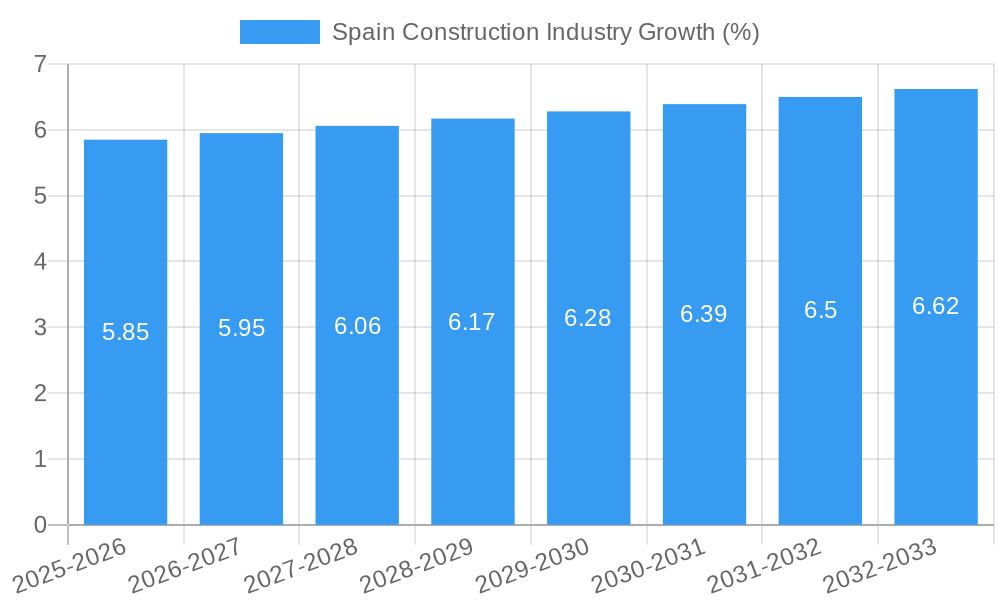

The Spanish construction industry, valued at €192.55 million in 2025, is projected to experience steady growth, driven by several key factors. Government infrastructure investments, particularly in transportation projects like high-speed rail expansion (evidenced by the presence of ADIF Alta Velocidad in the list of companies), and renewable energy initiatives within the Energy and Utilities sector are major contributors to this positive outlook. The residential segment, fueled by population growth and increasing urbanization, also provides significant impetus. However, the industry faces headwinds including potential material cost inflation and skilled labor shortages, which could temper growth rates. The commercial sector's performance will depend on economic conditions and investment in new office spaces and retail developments. The industrial sector's growth is closely tied to broader economic activity and manufacturing output. Companies like ELECNOR SA, ACS Actividades de Construccion y Servicios SA, and Acciona Construcción SA, represent significant players, indicating a competitive yet consolidated market landscape. While the 3.00% CAGR suggests moderate growth, the actual rate will depend on effective management of these challenges and the success of government policies supporting infrastructure development and sustainable construction practices.

The forecast period (2025-2033) anticipates a continuation of these trends. Maintaining a 3% CAGR, the market size is projected to reach approximately €250 million by 2033. This estimation accounts for potential fluctuations in economic activity and assumes the ongoing support for infrastructure and renewable energy projects. The relative growth across different sectors will likely reflect variations in government investment priorities and overall economic performance. Companies will need to adopt innovative approaches to address material cost issues, utilize advanced technologies to enhance efficiency, and implement robust sustainability measures to maintain competitiveness and contribute to a responsible growth trajectory for the Spanish construction market. Further analysis of specific regional variations within Spain would provide a more granular understanding of market dynamics and growth potential.

Spain Construction Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Spain construction industry, offering valuable insights for investors, industry professionals, and strategic decision-makers. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report unveils the market's structure, dynamics, trends, and future outlook. The analysis incorporates data from the historical period (2019-2024) and projects future growth, offering crucial information on key players, market segments, and growth drivers. Estimated market values are presented in Millions.

Spain Construction Industry Market Structure & Competitive Dynamics

The Spanish construction market exhibits a moderately concentrated structure, dominated by a few large players alongside numerous smaller firms. Key players such as ACS Actividades de Construcción y Servicios SA, Acciona Construcción SA, and Ferrovial Agroman SA hold significant market share, influencing pricing and innovation. The industry's innovation ecosystem is evolving, driven by government initiatives promoting sustainable building practices and technological advancements like BIM (Building Information Modeling). The regulatory framework, including building codes and environmental regulations, plays a significant role, impacting project timelines and costs. Product substitutes, such as prefabricated building components, are gaining traction, while end-user trends toward sustainable and energy-efficient construction are shaping demand. M&A activity has been relatively robust in recent years, with deal values exceeding €xx Million in 2024. Specific examples include (but are not limited to):

- ACS Actividades de Construcción y Servicios SA's acquisition of [Company Name] for €xx Million in 2023.

- Acciona Construcción SA's strategic partnership with [Company Name] to develop sustainable infrastructure projects.

Market Share (Estimated 2025):

- ACS Actividades de Construcción y Servicios SA: xx%

- Acciona Construcción SA: xx%

- Ferrovial Agroman SA: xx%

- Others: xx%

Spain Construction Industry Industry Trends & Insights

The Spain construction industry is experiencing a period of transformation, driven by several key trends. The market exhibits a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Government investments in infrastructure projects, particularly in transportation and renewable energy, are a major growth driver, boosting demand for construction services. Technological disruptions, such as the adoption of BIM and advanced construction technologies, are enhancing efficiency and productivity. Consumer preferences are shifting toward sustainable and energy-efficient buildings, influencing material choices and construction techniques. Furthermore, increasing urbanization and a growing population are fueling demand for residential and commercial construction. Market penetration of sustainable building materials is increasing at a rate of xx% annually, while the adoption of BIM in major projects has reached approximately xx%. Competitive dynamics are intensifying, with companies focusing on specialization, innovation, and strategic partnerships to gain a competitive edge.

Dominant Markets & Segments in Spain Construction Industry

The Infrastructure (Transportation) segment currently dominates the Spanish construction market, driven by substantial government investments in high-speed rail projects and road improvements. Major cities such as Madrid and Barcelona are experiencing significant growth in commercial and residential construction, though the infrastructure sector remains most influential overall.

Key Drivers for Infrastructure Dominance:

- Significant government investment in high-speed rail (AVE) expansion.

- Modernization of existing road networks and port infrastructure.

- EU funding for sustainable transport projects.

- Growing demand for logistics and distribution centers.

The dominance of the Infrastructure (Transportation) sector is supported by continuous government spending in this area. This segment is expected to maintain its leading position throughout the forecast period due to ongoing investment plans and population growth driving increased demand for efficient transportation networks. Other segments, like residential and commercial, show consistent growth, but are less impactful than the Infrastructure sector due to project scale and government involvement.

Spain Construction Industry Product Innovations

The Spanish construction industry is witnessing a surge in product innovation, driven by the need for sustainable, efficient, and cost-effective solutions. The adoption of Building Information Modeling (BIM) is streamlining project management and reducing errors. Prefabricated building components are gaining popularity, speeding up construction times and improving precision. The use of sustainable materials, such as recycled concrete and timber, is growing, reflecting a broader industry focus on environmental responsibility. Innovative construction techniques, such as 3D printing, are also starting to emerge, promising to revolutionize the industry in the long term. These innovations enhance efficiency, reduce costs, and improve the sustainability of construction projects, making them more competitive in the market.

Report Segmentation & Scope

This report segments the Spanish construction industry by sector:

Residential: This segment encompasses the construction of single-family homes, multi-family dwellings, and residential complexes. The market is projected to grow at a CAGR of xx% during the forecast period, driven by population growth and increasing urbanization. Competitive dynamics are shaped by land availability, building regulations, and consumer preferences.

Commercial: This segment includes the construction of office buildings, retail spaces, shopping malls, and hotels. The market is expected to grow at a CAGR of xx% during the forecast period, driven by economic growth and increasing investment in commercial real estate. Competition is intense, with firms specializing in different building types.

Industrial: This segment covers the construction of factories, warehouses, and industrial parks. The market is projected to experience a CAGR of xx% during the forecast period, fueled by industrial growth and expansion. Competition in this segment is largely based on cost-effectiveness and specialized expertise.

Infrastructure (Transportation): This segment includes the construction of roads, bridges, railways, airports, and other transportation infrastructure. It is projected to register a CAGR of xx% driven by significant government investment. Competitive dynamics are influenced by large-scale projects and government tenders.

Energy and Utilities: This segment encompasses the construction of power plants, renewable energy facilities, and utility infrastructure. The market is anticipated to grow at a CAGR of xx% due to increased focus on renewable energy and grid modernization. The industry is marked by specialized expertise and stringent safety regulations.

Key Drivers of Spain Construction Industry Growth

Several factors are driving the growth of the Spanish construction industry. Government spending on infrastructure projects, particularly in transportation and renewable energy, is a major catalyst. Economic growth and increased urbanization are boosting demand for residential and commercial construction. Technological advancements, such as BIM and prefabrication, are enhancing efficiency and productivity. Finally, supportive government policies, including tax incentives and streamlined permitting processes, are creating a favorable environment for investment and development.

Challenges in the Spain Construction Industry Sector

The Spanish construction industry faces several challenges. Regulatory hurdles, including complex permitting processes and environmental regulations, can delay projects and increase costs. Supply chain disruptions, particularly regarding the availability of certain materials, can impact project timelines and profitability. Intense competition, especially among larger firms, can lead to price pressures and reduced profit margins. These challenges impact industry profitability and require proactive strategies for mitigation. For example, lengthy permit approvals delay projects by an average of xx months, costing the industry an estimated €xx Million annually.

Leading Players in the Spain Construction Industry Market

- Acciona Construcción SA

- ACS Actividades de Construcción y Servicios SA

- ELECNOR SA

- Ferrovial Agroman SA

- Cobra Instalaciones y Servicios SA

- Dragados Sociedad Anónima

- Obrascón Huarte Lain SA

- Administrador de Infraestructuras Ferroviarias

- FCC Construction SA

- Sacyr Construcción SAU

- TSK Electrónica y Electricidad SA

- ADIF Alta Velocidad

Key Developments in Spain Construction Industry Sector

- 2023 Q3: Government announces €xx Million investment in renewable energy infrastructure.

- 2024 Q1: ACS Actividades de Construcción y Servicios SA merges with [Company Name].

- 2024 Q4: New building code implemented, focusing on sustainable construction practices.

Strategic Spain Construction Industry Market Outlook

The Spanish construction industry is poised for continued growth in the coming years. Government investments in infrastructure, coupled with increasing urbanization and economic growth, will drive demand for construction services. Technological advancements and a focus on sustainable construction practices will shape the industry's evolution. Strategic opportunities exist for companies that can adapt to changing market conditions, embrace technological innovations, and offer sustainable solutions. The long-term outlook is positive, with the market expected to reach €xx Million by 2033, presenting lucrative prospects for both established and emerging players.

Spain Construction Industry Segmentation

-

1. Sector

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

- 1.4. Infrastructure (Transportation)

- 1.5. Energy and Utilities

Spain Construction Industry Segmentation By Geography

- 1. Spain

Spain Construction Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing demand for Housing; Increasing demand for transportation infrastructure

- 3.3. Market Restrains

- 3.3.1. High Cost of Labour; Rising material costs

- 3.4. Market Trends

- 3.4.1. Increase in housing construction drives the market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Construction Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.1.4. Infrastructure (Transportation)

- 5.1.5. Energy and Utilities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 ELECNOR SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 ACS ACTIVIDADES DE CONSTRUCCION Y SERVICIOS SA

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 ACCIONA CONSTRUCCION SA

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 TSK ELECTRONICA Y ELECTRICIDAD SA

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 COBRA INSTALACIONES Y SERVICIOS SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 ADIF ALTA VELOCIDAD

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 SACYR CONSTRUCCION SAU**List Not Exhaustive

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 FERROVIAL AGROMAN SA

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 DRAGADOS SOCIEDAD ANONIMA

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 OBRASCON HUARTE LAIN SA

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 ADMINISTRADOR DE INFRAESTRUCTURAS FERROVIARIAS

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 FCC CONSTRUCTION SA

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 ELECNOR SA

List of Figures

- Figure 1: Spain Construction Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain Construction Industry Share (%) by Company 2024

List of Tables

- Table 1: Spain Construction Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain Construction Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Spain Construction Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Spain Construction Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Spain Construction Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 6: Spain Construction Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Construction Industry?

The projected CAGR is approximately 3.00%.

2. Which companies are prominent players in the Spain Construction Industry?

Key companies in the market include ELECNOR SA, ACS ACTIVIDADES DE CONSTRUCCION Y SERVICIOS SA, ACCIONA CONSTRUCCION SA, TSK ELECTRONICA Y ELECTRICIDAD SA, COBRA INSTALACIONES Y SERVICIOS SA, ADIF ALTA VELOCIDAD, SACYR CONSTRUCCION SAU**List Not Exhaustive, FERROVIAL AGROMAN SA, DRAGADOS SOCIEDAD ANONIMA, OBRASCON HUARTE LAIN SA, ADMINISTRADOR DE INFRAESTRUCTURAS FERROVIARIAS, FCC CONSTRUCTION SA.

3. What are the main segments of the Spain Construction Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 192.55 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing demand for Housing; Increasing demand for transportation infrastructure.

6. What are the notable trends driving market growth?

Increase in housing construction drives the market.

7. Are there any restraints impacting market growth?

High Cost of Labour; Rising material costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Construction Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Construction Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Construction Industry?

To stay informed about further developments, trends, and reports in the Spain Construction Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence