Key Insights

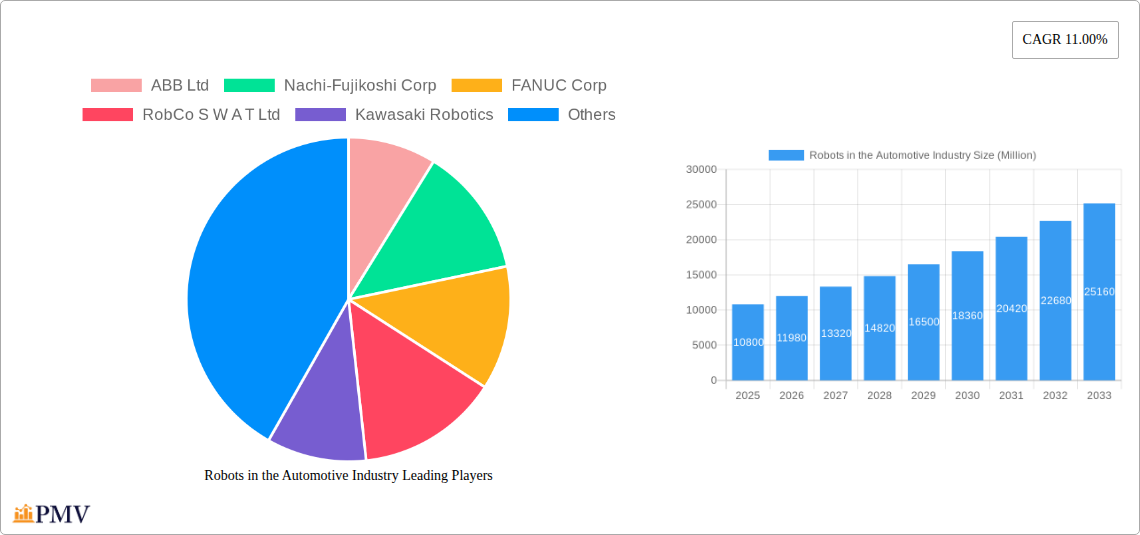

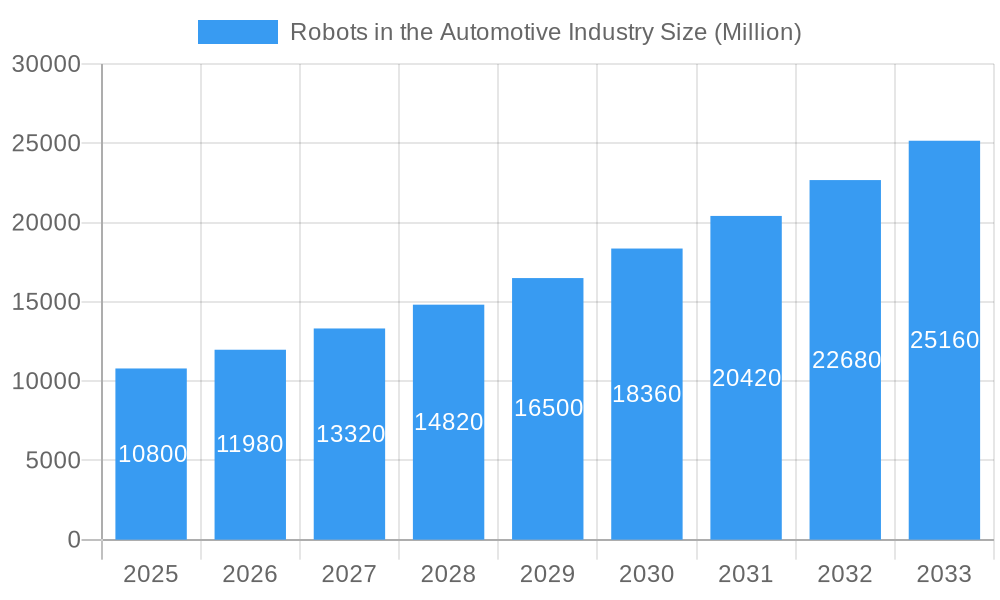

The global automotive robotics market, valued at $10.80 billion in 2025, is projected to experience robust growth, driven by increasing automation in vehicle manufacturing and the rising demand for higher production efficiency and improved product quality. A Compound Annual Growth Rate (CAGR) of 11% from 2025 to 2033 signifies a substantial expansion, reaching an estimated market size exceeding $30 billion by 2033. This growth is fueled by several key factors: the escalating adoption of advanced robotic technologies like collaborative robots (cobots) for enhanced flexibility and human-robot collaboration; the increasing integration of sophisticated sensor systems and artificial intelligence (AI) for improved precision and adaptability in robotic tasks; and the growing need to address labor shortages and rising labor costs within the automotive industry. Specific market segments like articulated robots, used extensively in assembly and welding, and those serving vehicle and component manufacturers, are experiencing particularly strong growth. While regulatory compliance and high initial investment costs present some challenges, the long-term benefits of automation far outweigh these concerns, continuously driving market expansion.

Robots in the Automotive Industry Market Size (In Billion)

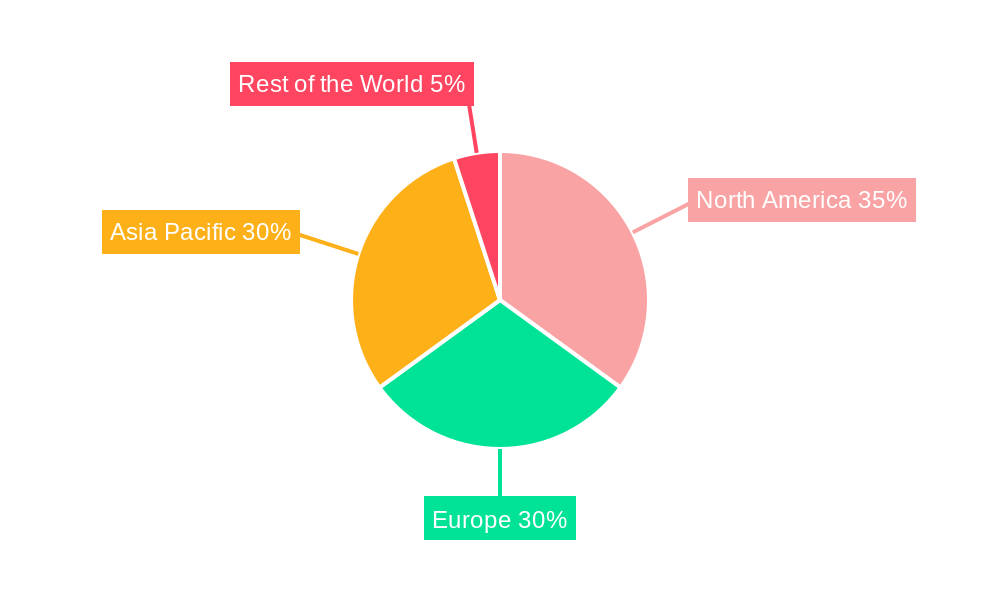

The geographical distribution of the market shows significant regional variations. North America and Europe currently hold substantial market shares, driven by established automotive manufacturing hubs and technological advancements. However, the Asia-Pacific region, particularly China and India, is anticipated to witness the most rapid growth due to increasing domestic automotive production and significant foreign direct investment in the sector. This shift reflects a global trend toward decentralization of manufacturing and the emergence of new automotive production powerhouses. The competitive landscape is shaped by a range of established industry players like ABB, FANUC, and KUKA, alongside emerging companies specializing in niche robotic technologies. This dynamic environment fosters innovation and competition, accelerating the overall development and adoption of automotive robotics.

Robots in the Automotive Industry Company Market Share

Robots in the Automotive Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Robots in the Automotive Industry market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. With a detailed study period spanning 2019-2033 (base year 2025, forecast period 2025-2033), this report leverages extensive market research and data analysis to present a clear picture of current market dynamics and future growth prospects. The global market is projected to reach xx Million by 2033, exhibiting a robust CAGR of xx% during the forecast period. Key players profiled include ABB Ltd, Nachi-Fujikoshi Corp, FANUC Corp, RobCo S W A T Ltd, Kawasaki Robotics, Omron Adept Robotics, KUKA Robotics, Honda Motor Co Ltd, Harmonic Drive System, and Yaskawa Electric Corporation.

Robots in the Automotive Industry Market Structure & Competitive Dynamics

The automotive robotics market is characterized by a moderately concentrated structure, with a handful of major players commanding significant market share. The competitive landscape is shaped by intense R&D investments driving innovation in areas like collaborative robots (cobots), AI-powered automation, and advanced sensor technologies. Regulatory frameworks, particularly concerning safety and environmental regulations, play a significant role in shaping market dynamics. Product substitutes, such as specialized automation equipment, pose a moderate threat, while the growing adoption of automation across various automotive manufacturing processes is a major growth driver. Furthermore, the market has witnessed significant M&A activity in recent years, with deal values exceeding xx Million in 2024 alone, reflecting the consolidation trend within the sector.

- Market Concentration: Top 5 players hold approximately xx% of the market share.

- Innovation Ecosystems: Collaborative partnerships between robotics companies and automotive OEMs are driving rapid innovation.

- Regulatory Frameworks: Stringent safety and environmental regulations influence technology adoption and market entry.

- M&A Activity: High deal volumes and values indicate a trend of consolidation and expansion among major players. Examples include recent acquisitions valued at xx Million in the past year.

- End-User Trends: Increasing demand for electric vehicles and autonomous driving features are driving the need for advanced robotics solutions.

Robots in the Automotive Industry Industry Trends & Insights

The automotive robotics market is experiencing robust and accelerating growth, propelled by the unwavering pursuit of enhanced automation by vehicle manufacturers and their component suppliers worldwide. A primary catalyst for this expansion is the escalating demand for manufacturing processes that deliver superior quality, cost-effectiveness, and unparalleled efficiency. The integration of cutting-edge technologies, notably Artificial Intelligence (AI) and Machine Learning (ML), is revolutionizing robotic capabilities, unlocking new applications and optimizing existing ones. Furthermore, evolving consumer preferences for vehicles equipped with advanced features, coupled with the significant surge in the production of electric vehicles (EVs), are substantial contributors to the market's upward trajectory. A notable shift within the industry is the increasing adoption of more agile and collaborative robots. These advanced systems minimize the need for extensive safety infrastructure, fostering a more integrated and productive human-robot collaboration environment. The competitive landscape is characterized by substantial investments in Research and Development (R&D), strategic alliances, and a dynamic M&A environment aimed at consolidating market position and technological leadership. The global market size, valued at approximately [Insert Specific Value Here] Million in 2024, is projected for substantial expansion, with a significant increase in market penetration expected by 2033.

Dominant Markets & Segments in Robots in the Automotive Industry

The automotive robotics market is exhibiting strong growth across a diverse range of geographical regions, with Asia-Pacific currently leading the charge. This dominance is largely attributed to the presence of extensive manufacturing hubs in key countries such as China, Japan, and South Korea, which are at the forefront of automotive production. Within specific market segments, the following trends are observed:

- By Component Type: Robotic arms continue to command the largest market share, a testament to their indispensable role in a multitude of automotive manufacturing processes. The demand for controllers and advanced sensors is also experiencing significant upward momentum.

- By Product Type: Articulated robots remain the most prevalent, their inherent versatility and adaptability making them ideal for a wide spectrum of applications. SCARA robots are also finding extensive use, particularly in intricate assembly operations.

- By Function Type: Welding robots represent a substantial portion of the market, followed closely by robots dedicated to painting and assembly tasks.

- By End-user Type: Vehicle manufacturers are the primary consumers of automotive robots, with automotive component manufacturers emerging as a critically important and rapidly expanding segment.

Key Drivers for Dominant Segments:

- Asia-Pacific Dominance: Fueled by a robust automotive manufacturing ecosystem and supportive government policies encouraging industrial automation.

- Robotic Arms: Sustained high demand driven by their critical role in welding, painting, and assembly operations, which are core to vehicle production.

- Articulated Robots: Their exceptional versatility and ability to adapt to diverse and complex manufacturing environments are key to their widespread adoption.

- Welding Robots: Considered foundational for the precise and efficient construction of automotive body structures.

- Vehicle Manufacturers: Demonstrating a strong commitment to adopting automation across their entire production lines to achieve efficiency and quality targets.

Robots in the Automotive Industry Product Innovations

Recent groundbreaking advancements in automotive robotics are sharply focused on elevating precision, accelerating operational speeds, and enhancing manufacturing flexibility. The pervasive integration of sophisticated AI and Machine Learning algorithms is empowering robots to intelligently adapt to dynamic production environments and execute complex tasks with an unprecedented degree of autonomy. Collaborative robots (cobots) are rapidly gaining traction, their inherent safety features allowing them to work seamlessly alongside human personnel, thereby significantly boosting overall productivity and efficiency. New robot designs are increasingly emphasizing compact footprints and superior energy efficiency. These innovations directly address the automotive industry's critical needs for shorter production cycles, enhanced quality control measures, and substantial cost reductions. Furthermore, the market is witnessing the development of highly specialized robots tailored for specific emerging tasks, such as the intricate assembly of battery packs for electric vehicles.

Report Segmentation & Scope

This report offers a detailed segmentation of the automotive robotics market, analyzed across various parameters:

- By Component Type: Controllers, Robotic Arms, End Effectors, Drive and Sensors (Growth projections, market size, and competitive dynamics are provided for each segment.)

- By Product Type: Cartesian Robots, SCARA Robots, Articulated Robots, Other Product Types (Market size and growth forecasts are presented, with an analysis of the competitive landscape.)

- By Function Type: Welding Robots, Painting Robots, Assembling and Disassembling Robots, Cutting and Milling Robots (This section analyzes the market share and growth potential of each functional robot type.)

- By End-user Type: Vehicle Manufacturers, Automotive Component Manufacturers (Detailed analysis of market size and growth projections for each end-user category.)

Key Drivers of Robots in the Automotive Industry Growth

The sustained and impressive growth of the automotive robotics market is underpinned by a confluence of powerful factors. Foremost among these is the escalating demand for sophisticated automation solutions within automotive manufacturing, aimed at optimizing operational efficiency and driving down production costs. Continuous technological breakthroughs, particularly in AI and Machine Learning, are significantly expanding the capabilities of robots, enabling them to perform more complex and nuanced tasks. Supportive government initiatives and policies that actively promote industrial automation across various sectors are further accelerating market penetration. The burgeoning adoption of electric vehicles and the rapid advancement of autonomous driving technologies are concurrently creating entirely new avenues and demand for specialized robotic applications, especially in areas like battery production and advanced vehicle assembly.

Challenges in the Robots in the Automotive Industry Sector

Despite significant growth potential, the automotive robotics industry faces challenges. High initial investment costs and the complexity of integrating robots into existing production lines can be barriers to adoption for some companies. Supply chain disruptions, especially for critical components like sensors and controllers, can impact production. Furthermore, intense competition and the need for continuous innovation to stay ahead of the curve pose significant challenges for market participants.

Leading Players in the Robots in the Automotive Industry Market

- ABB Ltd

- Nachi-Fujikoshi Corp

- FANUC Corp

- RobCo S W A T Ltd

- Kawasaki Robotics

- Omron Adept Robotics

- KUKA Robotics

- Honda Motor Co Ltd

- Harmonic Drive System

- Yaskawa Electric Corporation

Key Developments in Robots in the Automotive Industry Sector

- November 2023: ABB Robotics expanded its industrial SCARA robot portfolio with the IRB 930, offering three variants with 12 kg and 22 kg payload capacities. This expands ABB's reach in the growing SCARA market.

- August 2023: Kia, collaborating with Boston Dynamics, announced plans to launch a new automotive robot in 2024, signaling a move towards more advanced robotics in vehicle production.

- September 2023: OTTO Motors launched the OTTO 1200, a high-performing, heavy-duty mobile robot for compact environments, showcasing advancements in autonomous mobile robots (AMRs) for material handling within automotive facilities.

Strategic Robots in the Automotive Industry Market Outlook

The future of the automotive robotics market appears bright, with continued growth fueled by technological advancements, rising automation demands, and the expansion of electric and autonomous vehicle production. Strategic opportunities lie in developing innovative robotic solutions tailored to specific automotive manufacturing needs, such as battery assembly and precision component handling. Collaboration between robotics companies and automotive manufacturers will be crucial for driving innovation and market expansion. The market's focus on sustainability and efficiency will also present opportunities for energy-efficient robotic solutions and intelligent automation systems.

Robots in the Automotive Industry Segmentation

-

1. End-user Type

- 1.1. Vehicle Manufacturers

- 1.2. Automotive Component Manufacturers

-

2. Component Type

- 2.1. Controllers

- 2.2. Robotic Arms

- 2.3. End Effectors

- 2.4. Drive and Sensors

-

3. Product Type

- 3.1. Cartesian Robots

- 3.2. SCARA Robots

- 3.3. Articulated Robots

- 3.4. Other Product Types

-

4. Function Type

- 4.1. Welding Robots

- 4.2. Painting Robots

- 4.3. Assembling and Disassembling Robots

- 4.4. Cutting and Milling Robots

Robots in the Automotive Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Robots in the Automotive Industry Regional Market Share

Geographic Coverage of Robots in the Automotive Industry

Robots in the Automotive Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user Type

- 5.1.1. Vehicle Manufacturers

- 5.1.2. Automotive Component Manufacturers

- 5.2. Market Analysis, Insights and Forecast - by Component Type

- 5.2.1. Controllers

- 5.2.2. Robotic Arms

- 5.2.3. End Effectors

- 5.2.4. Drive and Sensors

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Cartesian Robots

- 5.3.2. SCARA Robots

- 5.3.3. Articulated Robots

- 5.3.4. Other Product Types

- 5.4. Market Analysis, Insights and Forecast - by Function Type

- 5.4.1. Welding Robots

- 5.4.2. Painting Robots

- 5.4.3. Assembling and Disassembling Robots

- 5.4.4. Cutting and Milling Robots

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by End-user Type

- 6. Global Robots in the Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user Type

- 6.1.1. Vehicle Manufacturers

- 6.1.2. Automotive Component Manufacturers

- 6.2. Market Analysis, Insights and Forecast - by Component Type

- 6.2.1. Controllers

- 6.2.2. Robotic Arms

- 6.2.3. End Effectors

- 6.2.4. Drive and Sensors

- 6.3. Market Analysis, Insights and Forecast - by Product Type

- 6.3.1. Cartesian Robots

- 6.3.2. SCARA Robots

- 6.3.3. Articulated Robots

- 6.3.4. Other Product Types

- 6.4. Market Analysis, Insights and Forecast - by Function Type

- 6.4.1. Welding Robots

- 6.4.2. Painting Robots

- 6.4.3. Assembling and Disassembling Robots

- 6.4.4. Cutting and Milling Robots

- 6.1. Market Analysis, Insights and Forecast - by End-user Type

- 7. North America Robots in the Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End-user Type

- 7.1.1. Vehicle Manufacturers

- 7.1.2. Automotive Component Manufacturers

- 7.2. Market Analysis, Insights and Forecast - by Component Type

- 7.2.1. Controllers

- 7.2.2. Robotic Arms

- 7.2.3. End Effectors

- 7.2.4. Drive and Sensors

- 7.3. Market Analysis, Insights and Forecast - by Product Type

- 7.3.1. Cartesian Robots

- 7.3.2. SCARA Robots

- 7.3.3. Articulated Robots

- 7.3.4. Other Product Types

- 7.4. Market Analysis, Insights and Forecast - by Function Type

- 7.4.1. Welding Robots

- 7.4.2. Painting Robots

- 7.4.3. Assembling and Disassembling Robots

- 7.4.4. Cutting and Milling Robots

- 7.1. Market Analysis, Insights and Forecast - by End-user Type

- 8. Europe Robots in the Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End-user Type

- 8.1.1. Vehicle Manufacturers

- 8.1.2. Automotive Component Manufacturers

- 8.2. Market Analysis, Insights and Forecast - by Component Type

- 8.2.1. Controllers

- 8.2.2. Robotic Arms

- 8.2.3. End Effectors

- 8.2.4. Drive and Sensors

- 8.3. Market Analysis, Insights and Forecast - by Product Type

- 8.3.1. Cartesian Robots

- 8.3.2. SCARA Robots

- 8.3.3. Articulated Robots

- 8.3.4. Other Product Types

- 8.4. Market Analysis, Insights and Forecast - by Function Type

- 8.4.1. Welding Robots

- 8.4.2. Painting Robots

- 8.4.3. Assembling and Disassembling Robots

- 8.4.4. Cutting and Milling Robots

- 8.1. Market Analysis, Insights and Forecast - by End-user Type

- 9. Asia Pacific Robots in the Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End-user Type

- 9.1.1. Vehicle Manufacturers

- 9.1.2. Automotive Component Manufacturers

- 9.2. Market Analysis, Insights and Forecast - by Component Type

- 9.2.1. Controllers

- 9.2.2. Robotic Arms

- 9.2.3. End Effectors

- 9.2.4. Drive and Sensors

- 9.3. Market Analysis, Insights and Forecast - by Product Type

- 9.3.1. Cartesian Robots

- 9.3.2. SCARA Robots

- 9.3.3. Articulated Robots

- 9.3.4. Other Product Types

- 9.4. Market Analysis, Insights and Forecast - by Function Type

- 9.4.1. Welding Robots

- 9.4.2. Painting Robots

- 9.4.3. Assembling and Disassembling Robots

- 9.4.4. Cutting and Milling Robots

- 9.1. Market Analysis, Insights and Forecast - by End-user Type

- 10. Rest of the World Robots in the Automotive Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End-user Type

- 10.1.1. Vehicle Manufacturers

- 10.1.2. Automotive Component Manufacturers

- 10.2. Market Analysis, Insights and Forecast - by Component Type

- 10.2.1. Controllers

- 10.2.2. Robotic Arms

- 10.2.3. End Effectors

- 10.2.4. Drive and Sensors

- 10.3. Market Analysis, Insights and Forecast - by Product Type

- 10.3.1. Cartesian Robots

- 10.3.2. SCARA Robots

- 10.3.3. Articulated Robots

- 10.3.4. Other Product Types

- 10.4. Market Analysis, Insights and Forecast - by Function Type

- 10.4.1. Welding Robots

- 10.4.2. Painting Robots

- 10.4.3. Assembling and Disassembling Robots

- 10.4.4. Cutting and Milling Robots

- 10.1. Market Analysis, Insights and Forecast - by End-user Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 ABB Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Nachi-Fujikoshi Corp

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 FANUC Corp

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 RobCo S W A T Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Kawasaki Robotics

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Omron Adept Robotics

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 KUKA Robotics

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Honda Motor Co Ltd

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Harmonic Drive System

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Yaskawa Electric Corporation

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 ABB Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Robots in the Automotive Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Robots in the Automotive Industry Revenue (Million), by End-user Type 2025 & 2033

- Figure 3: North America Robots in the Automotive Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 4: North America Robots in the Automotive Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 5: North America Robots in the Automotive Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 6: North America Robots in the Automotive Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 7: North America Robots in the Automotive Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: North America Robots in the Automotive Industry Revenue (Million), by Function Type 2025 & 2033

- Figure 9: North America Robots in the Automotive Industry Revenue Share (%), by Function Type 2025 & 2033

- Figure 10: North America Robots in the Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Robots in the Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Robots in the Automotive Industry Revenue (Million), by End-user Type 2025 & 2033

- Figure 13: Europe Robots in the Automotive Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 14: Europe Robots in the Automotive Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 15: Europe Robots in the Automotive Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 16: Europe Robots in the Automotive Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 17: Europe Robots in the Automotive Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Europe Robots in the Automotive Industry Revenue (Million), by Function Type 2025 & 2033

- Figure 19: Europe Robots in the Automotive Industry Revenue Share (%), by Function Type 2025 & 2033

- Figure 20: Europe Robots in the Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Robots in the Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Robots in the Automotive Industry Revenue (Million), by End-user Type 2025 & 2033

- Figure 23: Asia Pacific Robots in the Automotive Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 24: Asia Pacific Robots in the Automotive Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 25: Asia Pacific Robots in the Automotive Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 26: Asia Pacific Robots in the Automotive Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 27: Asia Pacific Robots in the Automotive Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Asia Pacific Robots in the Automotive Industry Revenue (Million), by Function Type 2025 & 2033

- Figure 29: Asia Pacific Robots in the Automotive Industry Revenue Share (%), by Function Type 2025 & 2033

- Figure 30: Asia Pacific Robots in the Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Robots in the Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Rest of the World Robots in the Automotive Industry Revenue (Million), by End-user Type 2025 & 2033

- Figure 33: Rest of the World Robots in the Automotive Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 34: Rest of the World Robots in the Automotive Industry Revenue (Million), by Component Type 2025 & 2033

- Figure 35: Rest of the World Robots in the Automotive Industry Revenue Share (%), by Component Type 2025 & 2033

- Figure 36: Rest of the World Robots in the Automotive Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 37: Rest of the World Robots in the Automotive Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Rest of the World Robots in the Automotive Industry Revenue (Million), by Function Type 2025 & 2033

- Figure 39: Rest of the World Robots in the Automotive Industry Revenue Share (%), by Function Type 2025 & 2033

- Figure 40: Rest of the World Robots in the Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Rest of the World Robots in the Automotive Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Robots in the Automotive Industry Revenue Million Forecast, by End-user Type 2020 & 2033

- Table 2: Global Robots in the Automotive Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 3: Global Robots in the Automotive Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: Global Robots in the Automotive Industry Revenue Million Forecast, by Function Type 2020 & 2033

- Table 5: Global Robots in the Automotive Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Robots in the Automotive Industry Revenue Million Forecast, by End-user Type 2020 & 2033

- Table 7: Global Robots in the Automotive Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 8: Global Robots in the Automotive Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 9: Global Robots in the Automotive Industry Revenue Million Forecast, by Function Type 2020 & 2033

- Table 10: Global Robots in the Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of North America Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Robots in the Automotive Industry Revenue Million Forecast, by End-user Type 2020 & 2033

- Table 15: Global Robots in the Automotive Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 16: Global Robots in the Automotive Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 17: Global Robots in the Automotive Industry Revenue Million Forecast, by Function Type 2020 & 2033

- Table 18: Global Robots in the Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Germany Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: United Kingdom Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Rest of Europe Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Global Robots in the Automotive Industry Revenue Million Forecast, by End-user Type 2020 & 2033

- Table 24: Global Robots in the Automotive Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 25: Global Robots in the Automotive Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 26: Global Robots in the Automotive Industry Revenue Million Forecast, by Function Type 2020 & 2033

- Table 27: Global Robots in the Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: China Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: India Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Japan Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: South Korea Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Rest of Asia Pacific Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Global Robots in the Automotive Industry Revenue Million Forecast, by End-user Type 2020 & 2033

- Table 34: Global Robots in the Automotive Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 35: Global Robots in the Automotive Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 36: Global Robots in the Automotive Industry Revenue Million Forecast, by Function Type 2020 & 2033

- Table 37: Global Robots in the Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 38: South America Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Middle East and Africa Robots in the Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Robots in the Automotive Industry?

The projected CAGR is approximately 11.00%.

2. Which companies are prominent players in the Robots in the Automotive Industry?

Key companies in the market include ABB Ltd, Nachi-Fujikoshi Corp, FANUC Corp, RobCo S W A T Ltd, Kawasaki Robotics, Omron Adept Robotics, KUKA Robotics, Honda Motor Co Ltd, Harmonic Drive System, Yaskawa Electric Corporation.

3. What are the main segments of the Robots in the Automotive Industry?

The market segments include End-user Type, Component Type, Product Type, Function Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.80 Million as of 2022.

5. What are some drivers contributing to market growth?

Exponential Increase in Automotive Sector.

6. What are the notable trends driving market growth?

Welding Robots Hold the Highest Share.

7. Are there any restraints impacting market growth?

High Cost of Installation Related to Industrial Robots.

8. Can you provide examples of recent developments in the market?

September 2023: OTTO Motors announced the OTTO 1200, which it claimed is the highest-performing, heavy-duty mobile robot for compact environments. It can safely move payloads of up to 1,200 kg (2,650 lb). The autonomous mobile robot (AMR) is equipped with patented adaptive fieldset technology to quickly and safely maneuver around people in narrow spaces, as claimed by OTTO Motors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Robots in the Automotive Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Robots in the Automotive Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Robots in the Automotive Industry?

To stay informed about further developments, trends, and reports in the Robots in the Automotive Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence