Key Insights

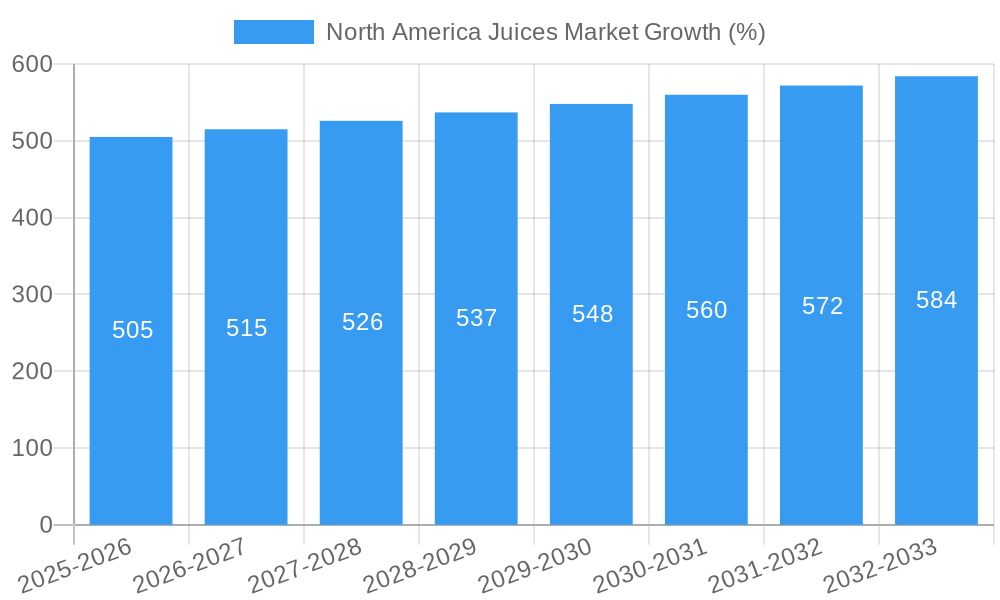

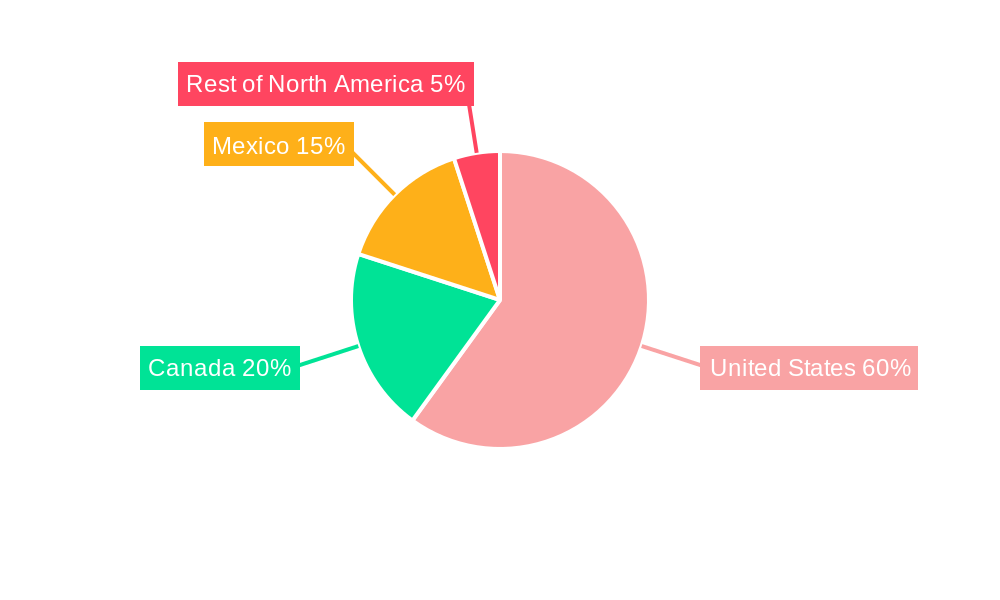

The North American juices market, valued at approximately $XX million in 2025, is projected to experience steady growth, exhibiting a compound annual growth rate (CAGR) of 2.51% from 2025 to 2033. This growth is fueled by several key factors. Increasing health consciousness among consumers is driving demand for 100% juice and juice drinks with higher juice content, particularly amongst health-conscious millennials and Gen Z. The rising popularity of convenient packaging formats like PET bottles and aseptic packages further contributes to market expansion. Furthermore, the increasing availability of functional juices infused with vitamins, minerals, and other health-boosting ingredients caters to the growing demand for nutritious and convenient beverage options. The market's segmentation reveals significant variations across different regions and distribution channels, with the United States representing the largest market share in North America. The off-trade channel (grocery stores, supermarkets) dominates distribution, although the on-trade (restaurants, cafes) segment is also expected to show growth, mirroring the expansion of juice options in food service establishments.

However, the market faces certain challenges. Fluctuations in raw material prices, particularly fruits and sugar, can impact production costs and pricing. Growing competition from other beverage categories, such as carbonated soft drinks and ready-to-drink teas, also poses a challenge. Furthermore, consumer concerns regarding added sugars and artificial ingredients in certain juice products could negatively impact market growth for those segments. Strategic initiatives by key players such as product diversification, expansion into new markets, and focus on premiumization and innovative product development are essential to navigate these challenges and capitalize on the ongoing market opportunities. Companies are increasingly investing in marketing campaigns highlighting the health benefits of juices, particularly emphasizing 100% juice options and those with added functional ingredients. This is critical in maintaining market share and attracting health-conscious consumers.

North America Juices Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America juices market, covering the period from 2019 to 2033. It offers valuable insights into market dynamics, competitive landscape, growth drivers, and future prospects, making it an essential resource for industry stakeholders, investors, and market researchers. The report encompasses detailed segmentation by country (United States, Canada, Mexico, Rest of North America), distribution channel (off-trade, on-trade), soft drink type (100% juice, juice drinks, juice concentrates, nectars), and packaging type (aseptic packages, disposable cups, glass bottles, metal cans, PET bottles). The base year for this report is 2025, with data covering the historical period (2019-2024), estimated year (2025), and forecast period (2025-2033). The market size is projected to reach xx Million by 2033.

North America Juices Market Market Structure & Competitive Dynamics

The North America juices market is characterized by a blend of large multinational corporations and smaller, regional players. Market concentration is moderate, with a few dominant players holding significant market share, while numerous smaller companies cater to niche segments. The competitive landscape is dynamic, with ongoing innovation, mergers & acquisitions (M&A), and intense competition based on pricing, product differentiation, and brand building.

- Market Concentration: The top 5 players account for approximately xx% of the total market share in 2025. This indicates a moderately consolidated market.

- Innovation Ecosystems: Companies are focusing on product innovation, particularly in functional juices, organic options, and convenient packaging. This is driven by evolving consumer preferences towards healthier and more convenient beverage options.

- Regulatory Frameworks: Regulations surrounding labeling, ingredients, and health claims significantly impact market dynamics. Compliance and adherence to these regulations are crucial for market participation.

- Product Substitutes: The market faces competition from other beverage categories such as bottled water, sports drinks, and ready-to-drink teas. These substitutes pose a competitive challenge, requiring juice producers to offer unique value propositions.

- End-User Trends: Health consciousness, convenience, and increasing demand for natural and organic juices are key trends shaping the market. Consumers are increasingly seeking functional beverages with added health benefits.

- M&A Activities: The market has witnessed several M&A activities in recent years, with larger players acquiring smaller companies to expand their product portfolios and market reach. The total value of M&A deals in the past five years is estimated at xx Million.

North America Juices Market Industry Trends & Insights

The North America juices market exhibits robust growth potential, driven by various factors. The market is projected to witness a CAGR of xx% during the forecast period (2025-2033). This growth is fueled by several key trends. Increased health consciousness among consumers is driving demand for 100% juices and products with added functional benefits. The rising adoption of convenient packaging formats like single-serve bottles and aseptic cartons is also contributing to market expansion. Furthermore, technological advancements in juice processing and packaging are enhancing product quality and shelf life. The market penetration of organic and functional juices is steadily increasing, representing a lucrative growth opportunity for manufacturers. However, the market also faces challenges such as intense competition, fluctuating raw material prices, and evolving consumer preferences. Competition is fierce among established brands and smaller, niche players, requiring companies to constantly innovate and differentiate their offerings.

Dominant Markets & Segments in North America Juices Market

The United States represents the largest market within North America, driven by high per capita consumption and diverse consumer preferences. Within the United States, the off-trade distribution channel dominates, reflecting the substantial sales through retail outlets. The 100% juice segment holds a significant market share, appealing to health-conscious consumers. PET bottles are the most widely used packaging type, offering convenience and cost-effectiveness.

Key Drivers for the US Market:

- Strong established retail infrastructure

- High disposable income

- Growing health consciousness

- Favorable government policies promoting healthy eating habits

Dominance Analysis: The dominance of the US market is due to its large population, high purchasing power, and well-developed distribution network. The preference for convenient packaging and the rising demand for healthier options fuel the dominance of PET bottles and the 100% juice segment.

North America Juices Market Product Innovations

Recent product launches highlight a clear trend toward functional and convenient juices. Companies are adding ingredients such as green coffee extract and L-Theanine for energy boosts, or creating blended juices with unique flavor combinations and increased nutritional value. The introduction of organic varieties also caters to the growing demand for natural and healthy options. This innovation strategy focuses on meeting the changing needs of health-conscious consumers seeking both taste and functional benefits in their beverages. Companies are also exploring sustainable packaging options to reduce their environmental footprint.

Report Segmentation & Scope

This report provides a comprehensive segmentation of the North America juices market across several key parameters:

- Country: United States, Canada, Mexico, Rest of North America (Growth projections and market sizes are available for each region).

- Distribution Channel: Off-trade (supermarkets, convenience stores), On-trade (restaurants, bars). (Market share and growth rates are detailed for each channel).

- Soft Drink Type: 100% Juice, Juice Drinks (up to 24% Juice), Juice concentrates, Nectars (25-99% Juice). (Market size and growth forecasts are provided for each type).

- Packaging Type: Aseptic packages, Disposable Cups, Glass Bottles, Metal Can, PET Bottles. (Detailed analysis of market share and trends for each packaging type).

Key Drivers of North America Juices Market Growth

The North America juices market is propelled by several key growth drivers:

- Growing Health Consciousness: Consumers are increasingly seeking healthier beverage options, boosting demand for 100% juices and functional beverages.

- Convenience: The ready-to-drink format and diverse packaging options are driving market expansion.

- Product Innovation: The introduction of new flavors, functional ingredients, and organic options is attracting new consumers.

- Favorable Economic Conditions (in select regions): Stronger economies in certain regions lead to increased disposable incomes and higher spending on premium beverages.

Challenges in the North America Juices Market Sector

The market faces several challenges:

- Intense Competition: The market is highly competitive, with numerous players vying for market share.

- Fluctuating Raw Material Prices: Changes in the prices of fruits and other ingredients affect production costs.

- Health and Wellness Trends: Maintaining consistency with evolving consumer demands for low sugar and healthier options.

- Sustainability Concerns: Growing demand for sustainable and eco-friendly packaging options.

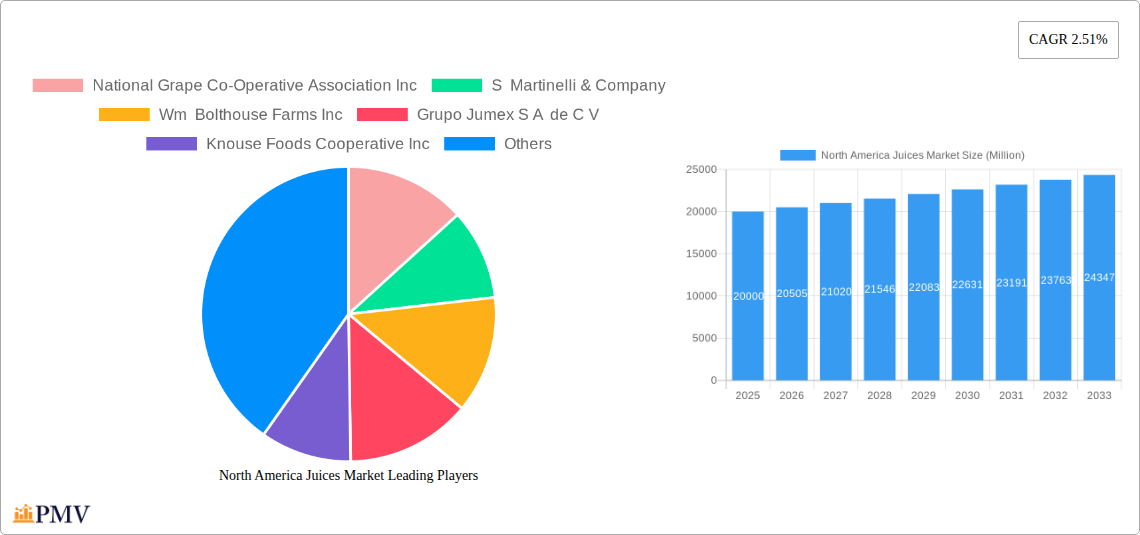

Leading Players in the North America Juices Market Market

- National Grape Co-Operative Association Inc

- S Martinelli & Company

- Wm Bolthouse Farms Inc

- Grupo Jumex S A de C V

- Knouse Foods Cooperative Inc

- PepsiCo Inc

- Keurig Dr Pepper Inc

- The Vita Coco Company Inc

- The Kraft Heinz Company

- Brynwood Partners

- Ocean Spray Cranberries Inc

- National Beverage Corp

- The Coca-Cola Company

- Langer Juice Company Inc

- Citrus World Inc

- Tropicana Brands Group

Key Developments in North America Juices Market Sector

- January 2023: Wm. Bolthouse Farms, Inc. launched three new product innovations under Bolthouse’s new "Energy" category.

- January 2023: Wm. Bolthouse Farms, Inc. expanded its line of feel-good nutrition with "Golden Goodness".

- April 2023: Martinelli's added an organic apple juice offering to its premium apple juice line.

Strategic North America Juices Market Market Outlook

The North America juices market presents significant growth opportunities, particularly in the functional beverages and organic segments. Strategic investments in product innovation, sustainable packaging, and efficient distribution networks will be crucial for success. Companies focusing on meeting the evolving needs of health-conscious consumers and leveraging technological advancements are poised to capture significant market share. The market's future growth will depend on adapting to changing consumer preferences and effectively addressing sustainability challenges.

North America Juices Market Segmentation

-

1. Soft Drink Type

- 1.1. 100% Juice

- 1.2. Juice Drinks (up to 24% Juice)

- 1.3. Juice concentrates

- 1.4. Nectars (25-99% Juice)

-

2. Packaging Type

- 2.1. Aseptic packages

- 2.2. Disposable Cups

- 2.3. Glass Bottles

- 2.4. Metal Can

- 2.5. PET Bottles

-

3. Distribution Channel

-

3.1. Off-trade

- 3.1.1. Convenience Stores

- 3.1.2. Online Retail

- 3.1.3. Supermarket/Hypermarket

- 3.1.4. Others

- 3.2. On-trade

-

3.1. Off-trade

North America Juices Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Juices Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.51% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Functional and Fortified Food; Multi-functionality and Wide Application of Riboflavin

- 3.3. Market Restrains

- 3.3.1. Low Stability of Riboflavin on Exposure to Light and Heat

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Juices Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 5.1.1. 100% Juice

- 5.1.2. Juice Drinks (up to 24% Juice)

- 5.1.3. Juice concentrates

- 5.1.4. Nectars (25-99% Juice)

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Aseptic packages

- 5.2.2. Disposable Cups

- 5.2.3. Glass Bottles

- 5.2.4. Metal Can

- 5.2.5. PET Bottles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Off-trade

- 5.3.1.1. Convenience Stores

- 5.3.1.2. Online Retail

- 5.3.1.3. Supermarket/Hypermarket

- 5.3.1.4. Others

- 5.3.2. On-trade

- 5.3.1. Off-trade

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 6. United States North America Juices Market Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Juices Market Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Juices Market Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Juices Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 National Grape Co-Operative Association Inc

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 S Martinelli & Company

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Wm Bolthouse Farms Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Grupo Jumex S A de C V

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Knouse Foods Cooperative Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 PepsiCo Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Keurig Dr Pepper Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 The Vita Coco Company Inc

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 The Kraft Heinz Company

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Brynwood Partners

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Ocean Spray Cranberries Inc

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 National Beverage Corp

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 The Coca-Cola Company

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 Langer Juice Company Inc

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.15 Citrus World Inc

- 10.2.15.1. Overview

- 10.2.15.2. Products

- 10.2.15.3. SWOT Analysis

- 10.2.15.4. Recent Developments

- 10.2.15.5. Financials (Based on Availability)

- 10.2.16 Tropicana Brands Group

- 10.2.16.1. Overview

- 10.2.16.2. Products

- 10.2.16.3. SWOT Analysis

- 10.2.16.4. Recent Developments

- 10.2.16.5. Financials (Based on Availability)

- 10.2.1 National Grape Co-Operative Association Inc

List of Figures

- Figure 1: North America Juices Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Juices Market Share (%) by Company 2024

List of Tables

- Table 1: North America Juices Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Juices Market Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 3: North America Juices Market Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 4: North America Juices Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: North America Juices Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Juices Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Juices Market Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 12: North America Juices Market Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 13: North America Juices Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 14: North America Juices Market Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Juices Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Juices Market?

The projected CAGR is approximately 2.51%.

2. Which companies are prominent players in the North America Juices Market?

Key companies in the market include National Grape Co-Operative Association Inc, S Martinelli & Company, Wm Bolthouse Farms Inc, Grupo Jumex S A de C V, Knouse Foods Cooperative Inc, PepsiCo Inc, Keurig Dr Pepper Inc, The Vita Coco Company Inc, The Kraft Heinz Company, Brynwood Partners, Ocean Spray Cranberries Inc, National Beverage Corp, The Coca-Cola Company, Langer Juice Company Inc, Citrus World Inc, Tropicana Brands Group.

3. What are the main segments of the North America Juices Market?

The market segments include Soft Drink Type, Packaging Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Functional and Fortified Food; Multi-functionality and Wide Application of Riboflavin.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Low Stability of Riboflavin on Exposure to Light and Heat.

8. Can you provide examples of recent developments in the market?

April 2023: Martinelli's is a manufacturer of premium apple juice and have recently added organic apple juice offering.January 2023: Wm. Bolthouse Farms, Inc. launched three new product innovations under Bolthouse’s new "Energy" category. Each bottle contains 3 ¾ servings of fruit and veg, anchored by the company’s signature carrot juice, plus balanced energy from natural green coffee bean extract and L-Theanine.January 2023: Wm. Bolthouse Farms, Inc. expanded its line of feel-good nutrition with "Golden Goodness". Golden is a blend of golden-hued fruits and vegetables, such as peach, banana, mango, and yellow carrots, with a hint of passion fruit for a new flavor experience.”

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Juices Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Juices Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Juices Market?

To stay informed about further developments, trends, and reports in the North America Juices Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence