Key Insights

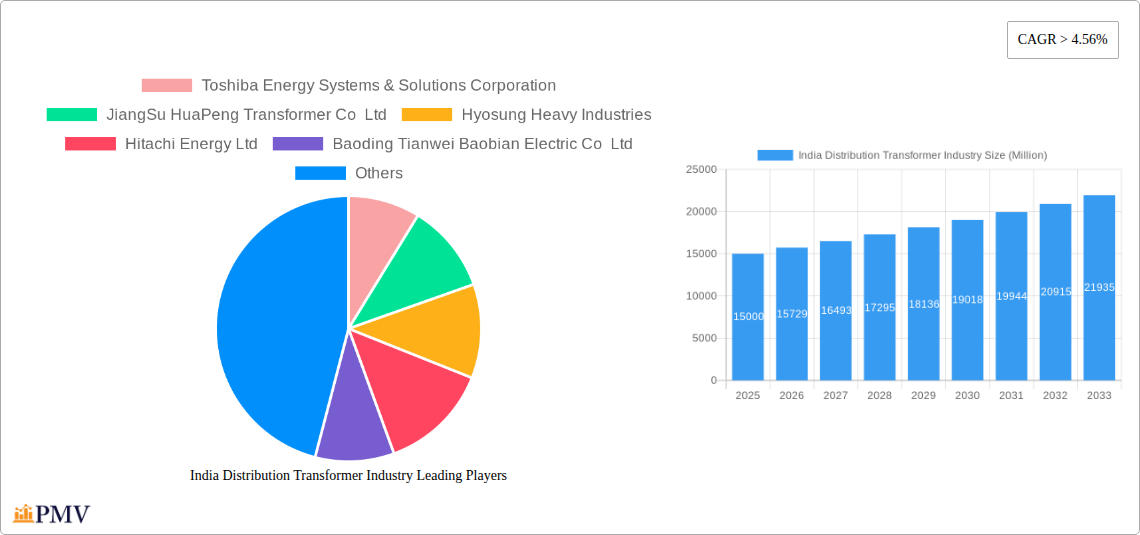

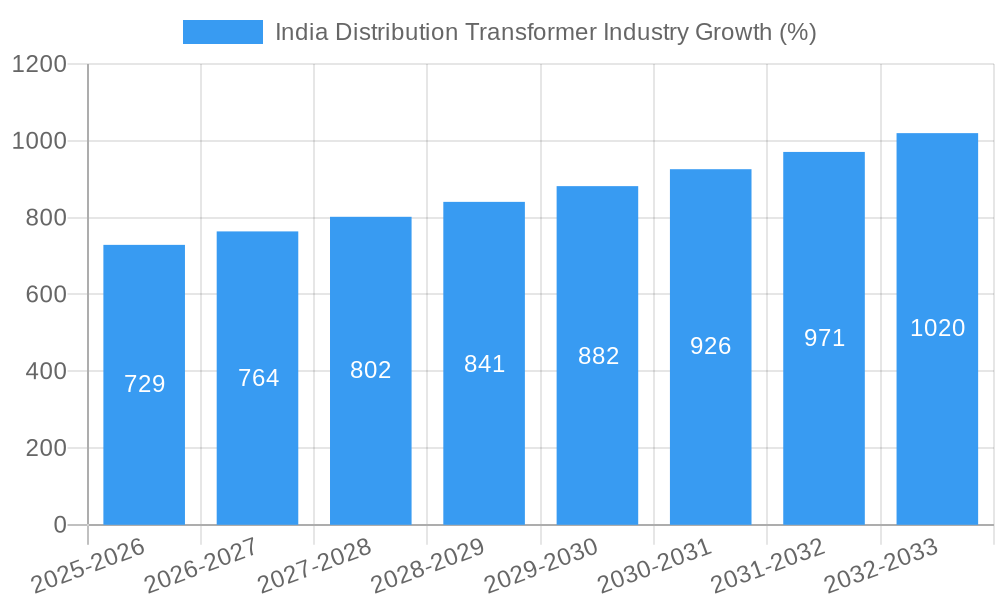

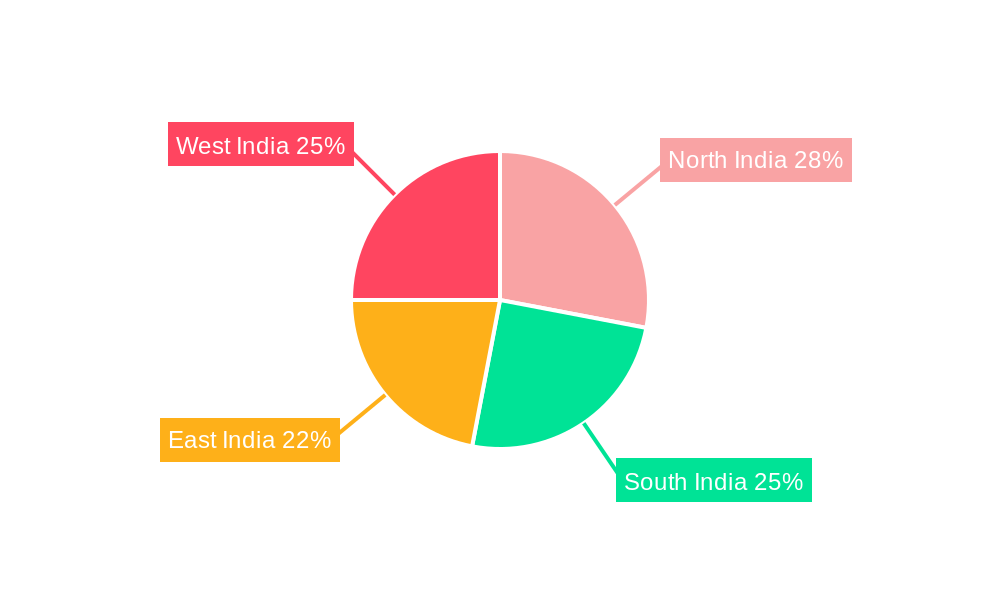

The Indian distribution transformer market, valued at approximately ₹15000 million (estimated) in 2025, is experiencing robust growth, projected to expand at a CAGR exceeding 4.56% from 2025 to 2033. This growth is fueled by several key factors. The burgeoning electricity demand driven by rapid urbanization and industrialization across India, particularly in regions like North and West India, is a primary driver. Government initiatives promoting renewable energy integration and smart grid development further stimulate market expansion. The increasing adoption of dry-type transformers, known for their enhanced efficiency and environmental friendliness, is a significant trend. However, challenges remain, including fluctuating raw material prices, intense competition among numerous domestic and international players, and the need for robust grid infrastructure improvements in certain regions. The market segmentation reveals a significant portion dominated by transformers with capacities between 500 kVA and 2500 kVA, catering to the prevalent needs of distribution networks. Three-phase transformers hold a larger market share compared to single-phase units, reflecting the broader electrification demands. Pad-mounted transformers enjoy higher preference than pole-mounted ones due to installation and maintenance advantages. Key players like Toshiba, Jiangsu HuaPeng, Hyosung, and others are actively competing, leveraging technological advancements and strategic partnerships to secure market share. The market is expected to witness significant consolidation in the coming years as companies strive for greater scale and efficiency.

The forecast period (2025-2033) anticipates continued growth, driven by ongoing infrastructure development, particularly in the southern and eastern regions of India. The market will witness increasing adoption of advanced technologies, including digital monitoring and predictive maintenance to improve grid reliability and efficiency. Further government policies incentivizing energy efficiency and renewable integration are expected to further enhance the growth trajectory. The competitive landscape will likely see strategic alliances and mergers & acquisitions as companies aim to capitalize on growth opportunities and expand their market reach. The demand for higher capacity transformers (above 2500 kVA) is expected to increase gradually, reflecting the need for enhanced power distribution capacity in rapidly developing urban areas.

India Distribution Transformer Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the India distribution transformer industry, offering invaluable insights for stakeholders, investors, and industry professionals. Covering the period from 2019 to 2033, with a base year of 2025, this report forecasts market trends, identifies key players, and analyzes growth drivers and challenges. The report segments the market by capacity (Below 500 kVA, 500 kVA - 2500 kVA, Above 2500 kVA), type (Oil-filled, Dry Type), mounting type (Pad-mounted, Pole-mounted), and phase (Single Phase, Three Phase).

India Distribution Transformer Industry Market Structure & Competitive Dynamics

The Indian distribution transformer market exhibits a moderately concentrated structure, with both domestic and multinational players vying for market share. Key players like Toshiba Energy Systems & Solutions Corporation, Jiangsu HuaPeng Transformer Co Ltd, Hyosung Heavy Industries, Hitachi Energy Ltd, Baoding Tianwei Baobian Electric Co Ltd, Mitsubishi Electric Corporation, Schneider Electric SE, Siemens Energy AG, CG Power and Industrial Solutions Ltd, and Bharat Heavy Electricals Limited hold significant market share, though the exact figures are proprietary to this report. However, the market also features several smaller, regional players.

The industry's innovation ecosystem is developing, driven by the need for energy efficiency and smart grid technologies. Regulatory frameworks, including those related to energy efficiency standards and grid modernization initiatives, significantly influence market dynamics. Product substitutes, primarily focusing on improved energy efficiency and reduced environmental impact, are emerging. End-user trends are shifting towards smart grid solutions and increased automation, impacting the demand for advanced distribution transformers. Recent M&A activities have been moderate, with deal values estimated at xx Million USD in the past five years (2019-2024). The report contains a detailed breakdown of market share for key players and a comprehensive analysis of M&A activity.

India Distribution Transformer Industry Industry Trends & Insights

The Indian distribution transformer market is experiencing robust growth, driven by increasing urbanization, industrialization, and the government's focus on rural electrification. The Compound Annual Growth Rate (CAGR) during the historical period (2019-2024) is estimated at xx%, with projections indicating continued growth at xx% during the forecast period (2025-2033). Technological disruptions, particularly in the areas of smart grids, energy storage, and digitalization, are significantly reshaping the industry landscape. Consumer preferences are increasingly shifting towards energy-efficient and technologically advanced transformers. Intense competition, coupled with government initiatives to promote renewable energy integration, is further influencing market trends. Market penetration of advanced transformer technologies, such as dry-type transformers and smart transformers, is steadily increasing, though remaining below xx% of the total market in 2024, projected to reach xx% by 2033.

Dominant Markets & Segments in India Distribution Transformer Industry

The report identifies the northern and western regions of India as the dominant markets for distribution transformers, primarily driven by robust industrial activity and expanding infrastructure projects.

- Capacity: The 500 kVA - 2500 kVA segment currently holds the largest market share, driven by significant demand from industrial and commercial applications.

- Type: Oil-filled transformers continue to dominate the market due to their established technology and lower initial cost. However, dry-type transformers are gaining traction due to their enhanced safety features and environmental benefits.

- Mounting Type: Pad-mounted transformers are the most widely used type, owing to their ease of installation and maintenance.

- Phase: Three-phase transformers dominate the market due to their applicability in industrial and commercial settings.

Key drivers for the dominance of these segments include favorable government policies promoting infrastructure development, increasing electricity demand, and robust economic growth in these regions. Detailed analysis of regional and segment-specific growth drivers, including economic policies and infrastructure development, is provided within the full report.

India Distribution Transformer Industry Product Innovations

Recent product innovations include the development of more energy-efficient transformers with advanced cooling systems and digital monitoring capabilities. The increasing adoption of dry-type transformers, offering superior safety and environmental benefits, is another significant trend. These advancements are aimed at enhancing reliability, improving efficiency, and reducing environmental impact. Market fit is driven by customer demand for improved performance, safety, and environmental sustainability.

Report Segmentation & Scope

The report segments the market comprehensively across capacity (Below 500 kVA, 500 kVA - 2500 kVA, Above 2500 kVA), type (Oil-filled, Dry Type), mounting type (Pad-mounted, Pole-mounted), and phase (Single Phase, Three Phase). Each segment is analyzed individually, providing detailed growth projections, market size estimations, and competitive dynamics. The report also provides a detailed overview of each segment, including its current market size, projected growth rate, and competitive landscape.

Key Drivers of India Distribution Transformer Industry Growth

The growth of the India distribution transformer industry is propelled by several factors: increasing electricity demand fueled by economic growth and rising urbanization; government initiatives aimed at improving the country's power infrastructure; expansion of the rural electrification program; and the increasing adoption of renewable energy sources requiring efficient distribution infrastructure. Further, technological advancements leading to the development of smart transformers enhance grid efficiency and reliability.

Challenges in the India Distribution Transformer Industry Sector

The industry faces challenges including: the fluctuating price of raw materials; potential supply chain disruptions; intense competition from both domestic and international players; and the need to meet stringent regulatory compliance requirements and energy efficiency standards. These challenges, along with their quantifiable impact on market growth, are discussed extensively in the report.

Leading Players in the India Distribution Transformer Industry Market

- Toshiba Energy Systems & Solutions Corporation

- Jiangsu HuaPeng Transformer Co Ltd

- Hyosung Heavy Industries

- Hitachi Energy Ltd

- Baoding Tianwei Baobian Electric Co Ltd

- Mitsubishi Electric Corporation

- Schneider Electric SE

- Siemens Energy AG

- CG Power and Industrial Solutions Ltd

- Bharat Heavy Electricals Limited

- *List Not Exhaustive

Key Developments in India Distribution Transformer Industry Sector

- December 2021: The Transformers & Rectifiers India Ltd. secured orders worth INR 72 crore (approximately xx Million USD) for various transformers, including distribution transformers, from Gujarat Energy Transmission Corporation (GETCO). This highlights strong demand from the power transmission sector.

- December 2021: Tata Power Delhi Distribution Ltd (DDL), in collaboration with Toshiba Transmission & Distribution Systems (India) Pvt. Ltd., installed a 630 kVA submersible distribution transformer, showcasing innovation in power distribution infrastructure.

Strategic India Distribution Transformer Industry Market Outlook

The Indian distribution transformer market presents significant growth potential, driven by sustained infrastructure development, government investments in renewable energy, and increasing industrialization. Strategic opportunities exist for companies focused on energy-efficient, smart grid-compatible solutions. The market is expected to witness further consolidation, with larger players acquiring smaller companies to expand their market share and technological capabilities. The future outlook is promising, with the industry poised for significant expansion in the coming years.

India Distribution Transformer Industry Segmentation

-

1. Capacity

- 1.1. Below 500 kVA

- 1.2. 500 kVA - 2500 kVA

- 1.3. Above 2500 kVA

-

2. Type

- 2.1. Oil-filled

- 2.2. Dry Type

-

3. Mounting Type

- 3.1. Pad-mounted

- 3.2. Pole-mounted

-

4. Phase

- 4.1. Single Phase

- 4.2. Three Phase

India Distribution Transformer Industry Segmentation By Geography

- 1. India

India Distribution Transformer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 4.56% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; High Electricity Demand from Industries4.; Enhancement in Economic Activities

- 3.3. Market Restrains

- 3.3.1. 4.; The Complex Maintenance Process of Components And the Emergence of Toxic Wastes that Affect the Environment

- 3.4. Market Trends

- 3.4.1. Below 500 kVA Capacity to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Distribution Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Below 500 kVA

- 5.1.2. 500 kVA - 2500 kVA

- 5.1.3. Above 2500 kVA

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Oil-filled

- 5.2.2. Dry Type

- 5.3. Market Analysis, Insights and Forecast - by Mounting Type

- 5.3.1. Pad-mounted

- 5.3.2. Pole-mounted

- 5.4. Market Analysis, Insights and Forecast - by Phase

- 5.4.1. Single Phase

- 5.4.2. Three Phase

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. India

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. North India India Distribution Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India Distribution Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India Distribution Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India Distribution Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Toshiba Energy Systems & Solutions Corporation

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 JiangSu HuaPeng Transformer Co Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Hyosung Heavy Industries

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Hitachi Energy Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Baoding Tianwei Baobian Electric Co Ltd

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Mitsubishi Electric Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Schneider Electric SE

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Siemens Energy AG

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 CG Power and Industrial Solutions Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Bharat Heavy Electricals Limited*List Not Exhaustive

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Toshiba Energy Systems & Solutions Corporation

List of Figures

- Figure 1: India Distribution Transformer Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Distribution Transformer Industry Share (%) by Company 2024

List of Tables

- Table 1: India Distribution Transformer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Distribution Transformer Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 3: India Distribution Transformer Industry Revenue Million Forecast, by Capacity 2019 & 2032

- Table 4: India Distribution Transformer Industry Volume K Units Forecast, by Capacity 2019 & 2032

- Table 5: India Distribution Transformer Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 6: India Distribution Transformer Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 7: India Distribution Transformer Industry Revenue Million Forecast, by Mounting Type 2019 & 2032

- Table 8: India Distribution Transformer Industry Volume K Units Forecast, by Mounting Type 2019 & 2032

- Table 9: India Distribution Transformer Industry Revenue Million Forecast, by Phase 2019 & 2032

- Table 10: India Distribution Transformer Industry Volume K Units Forecast, by Phase 2019 & 2032

- Table 11: India Distribution Transformer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 12: India Distribution Transformer Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 13: India Distribution Transformer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: India Distribution Transformer Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 15: North India India Distribution Transformer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: North India India Distribution Transformer Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 17: South India India Distribution Transformer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: South India India Distribution Transformer Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 19: East India India Distribution Transformer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: East India India Distribution Transformer Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 21: West India India Distribution Transformer Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: West India India Distribution Transformer Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 23: India Distribution Transformer Industry Revenue Million Forecast, by Capacity 2019 & 2032

- Table 24: India Distribution Transformer Industry Volume K Units Forecast, by Capacity 2019 & 2032

- Table 25: India Distribution Transformer Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 26: India Distribution Transformer Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 27: India Distribution Transformer Industry Revenue Million Forecast, by Mounting Type 2019 & 2032

- Table 28: India Distribution Transformer Industry Volume K Units Forecast, by Mounting Type 2019 & 2032

- Table 29: India Distribution Transformer Industry Revenue Million Forecast, by Phase 2019 & 2032

- Table 30: India Distribution Transformer Industry Volume K Units Forecast, by Phase 2019 & 2032

- Table 31: India Distribution Transformer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: India Distribution Transformer Industry Volume K Units Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Distribution Transformer Industry?

The projected CAGR is approximately > 4.56%.

2. Which companies are prominent players in the India Distribution Transformer Industry?

Key companies in the market include Toshiba Energy Systems & Solutions Corporation, JiangSu HuaPeng Transformer Co Ltd, Hyosung Heavy Industries, Hitachi Energy Ltd, Baoding Tianwei Baobian Electric Co Ltd, Mitsubishi Electric Corporation, Schneider Electric SE, Siemens Energy AG, CG Power and Industrial Solutions Ltd, Bharat Heavy Electricals Limited*List Not Exhaustive.

3. What are the main segments of the India Distribution Transformer Industry?

The market segments include Capacity, Type, Mounting Type, Phase.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; High Electricity Demand from Industries4.; Enhancement in Economic Activities.

6. What are the notable trends driving market growth?

Below 500 kVA Capacity to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; The Complex Maintenance Process of Components And the Emergence of Toxic Wastes that Affect the Environment.

8. Can you provide examples of recent developments in the market?

In December 2021, The Transformers & Rectifiers India Ltd. was awarded orders of various transformers, including distribution transformers, for the total contract value of INR 72 crore from Gujarat Energy Transmission Corporation (GETCO).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Distribution Transformer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Distribution Transformer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Distribution Transformer Industry?

To stay informed about further developments, trends, and reports in the India Distribution Transformer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence