Key Insights

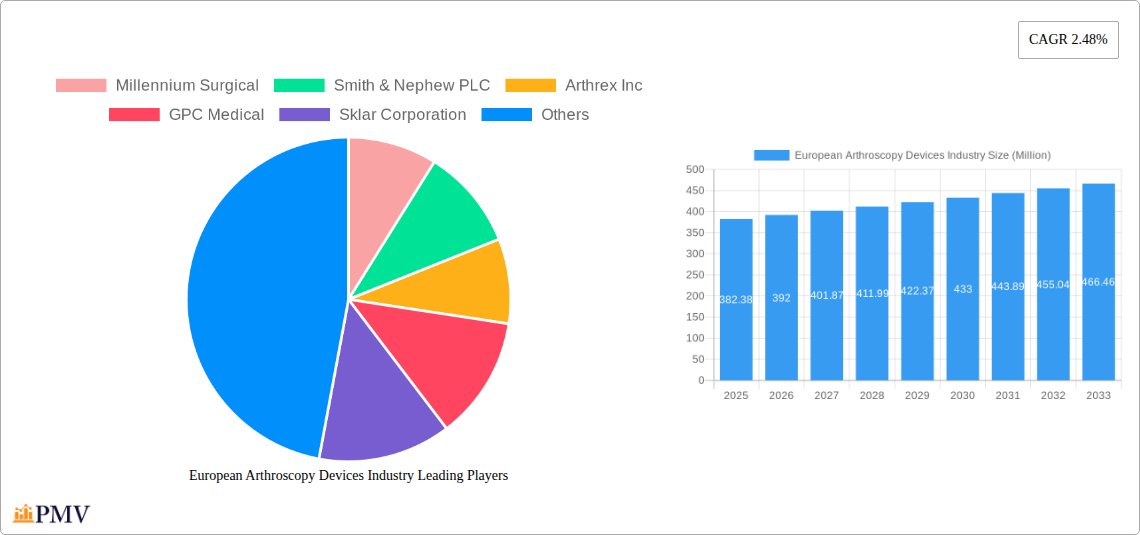

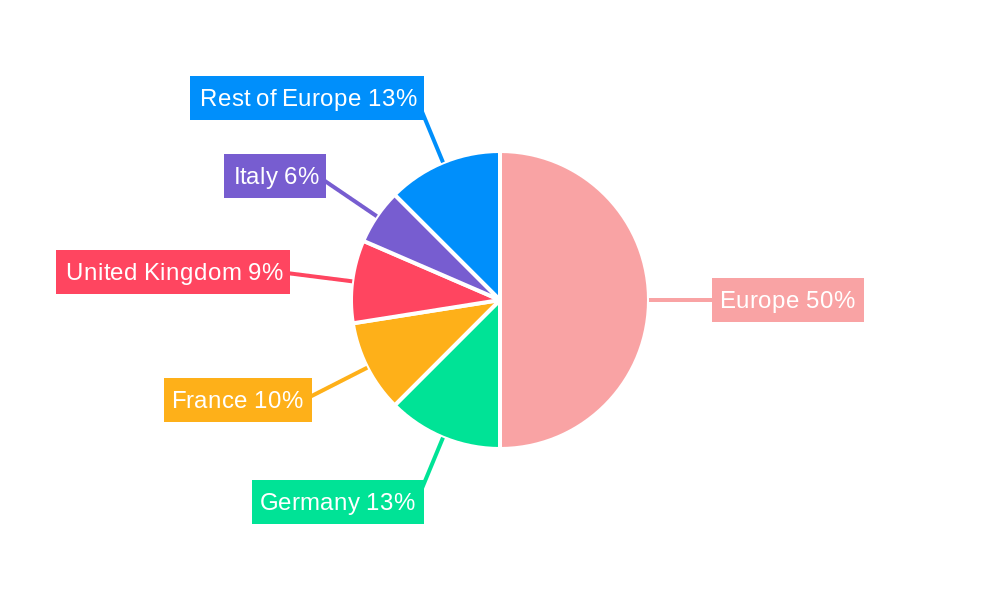

The European arthroscopy devices market, valued at €382.38 million in 2025, is projected to experience steady growth, driven by a rising geriatric population susceptible to osteoarthritis and other joint-related conditions requiring arthroscopic procedures. Increased prevalence of sports injuries, particularly among younger demographics, further fuels demand for minimally invasive arthroscopic surgeries. Technological advancements in arthroscopic instruments, such as improved visualization systems and smaller, more precise instruments, enhance surgical precision and patient outcomes, contributing to market expansion. The market segmentation reveals a strong demand across various applications, with knee arthroscopy likely dominating due to the high incidence of knee osteoarthritis. Hip, shoulder, and elbow arthroscopy segments also contribute significantly, reflecting the prevalence of injuries and degenerative conditions affecting these joints. The product segment is characterized by a diverse range of devices, including arthroscopes, implants, fluid management systems, and visualization systems, each contributing to the overall market value. Germany, France, and the United Kingdom are expected to be the largest national markets within Europe, reflecting their advanced healthcare infrastructure and higher prevalence of arthroscopic procedures. However, growth across smaller European markets like the Netherlands and Sweden is also anticipated due to improving healthcare access and increasing awareness of arthroscopy as a viable treatment option.

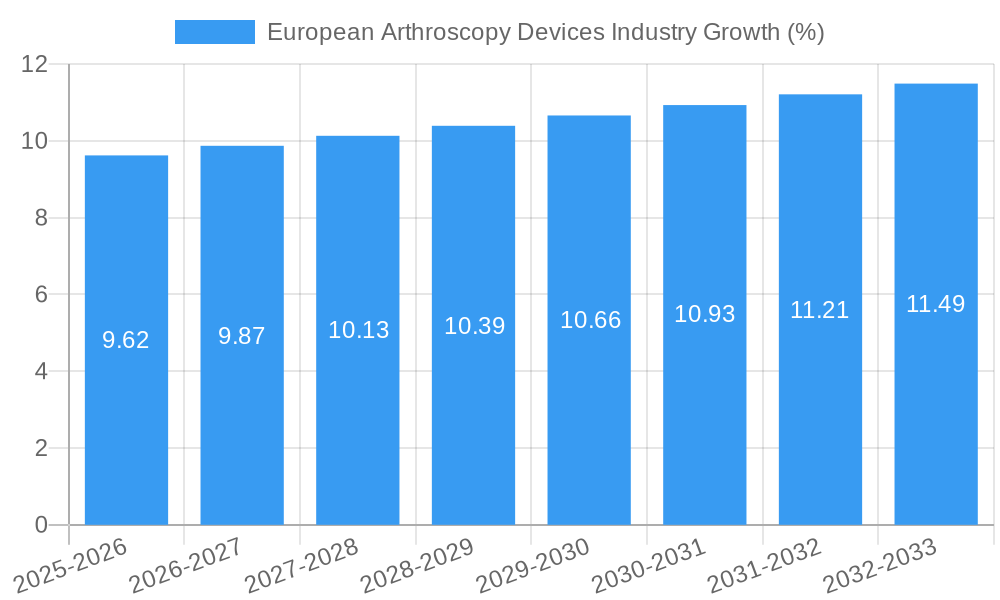

The forecast period (2025-2033) anticipates a continued, albeit moderate, expansion of the European arthroscopy devices market. While the 2.48% CAGR suggests a steady growth trajectory, market dynamics suggest potential for acceleration. Factors influencing future growth include the ongoing development of innovative arthroscopic techniques (e.g., robotic-assisted arthroscopy), increased adoption of value-based healthcare models focusing on cost-effectiveness, and the potential for new applications expanding beyond the currently dominant procedures. However, restraints like the high cost of advanced arthroscopic devices, stringent regulatory approvals, and the potential for alternative treatment methods may slightly temper growth. Competition within the market is intense, with both established multinational corporations and specialized smaller companies vying for market share. Strategic partnerships, technological innovation, and a focus on providing comprehensive solutions are expected to be key factors for success in this competitive landscape.

European Arthroscopy Devices Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the European arthroscopy devices market, covering market structure, competitive dynamics, industry trends, dominant segments, product innovations, and future growth prospects. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period extends from 2025 to 2033, while the historical period encompasses 2019-2024. The report offers actionable insights for stakeholders across the value chain, including manufacturers, distributors, and healthcare providers. The market size in 2025 is estimated at xx Million, projected to reach xx Million by 2033.

European Arthroscopy Devices Industry Market Structure & Competitive Dynamics

The European arthroscopy devices market exhibits a moderately concentrated structure, with several multinational corporations and specialized companies vying for market share. Market leaders such as Smith & Nephew PLC, Arthrex Inc, and Medtronic PLC hold significant portions of the market, while smaller, specialized players focus on niche segments. The market's innovation ecosystem is robust, driven by continuous advancements in surgical techniques, imaging technology, and implant design. Regulatory frameworks, primarily governed by the European Union's Medical Device Regulation (MDR), heavily influence market access and product development. Substitute products, such as open surgery techniques, exist, but the minimally invasive nature and faster recovery times associated with arthroscopy are fueling strong market growth. End-user trends, including an aging population and increasing prevalence of musculoskeletal disorders, are key drivers. Recent M&A activity in the sector has been moderate, with deal values primarily in the range of xx Million to xx Million, aiming to expand product portfolios and geographic reach.

- Market Concentration: Moderately Concentrated

- Top 3 Players Market Share (2025 est.): xx%

- Average M&A Deal Value (2019-2024): xx Million

European Arthroscopy Devices Industry Industry Trends & Insights

The European arthroscopy devices market is experiencing robust growth, driven by several key factors. The aging population across Europe is leading to increased incidence of osteoarthritis and other musculoskeletal conditions requiring arthroscopic procedures. Technological advancements, such as the development of more sophisticated arthroscopes, implants, and visualization systems, are enhancing the precision and effectiveness of arthroscopic surgeries, boosting market demand. Consumer preferences are shifting towards minimally invasive procedures due to shorter recovery times and reduced hospital stays. The rise of ambulatory surgery centers is further fueling the growth of arthroscopy. Competitive dynamics are shaping the market, with companies investing heavily in R&D to introduce innovative products and gain a competitive edge. Market growth is also being driven by rising healthcare expenditure and increasing insurance coverage for arthroscopic procedures. The CAGR for the forecast period (2025-2033) is estimated to be xx%, with market penetration expected to reach xx% by 2033.

Dominant Markets & Segments in European Arthroscopy Devices Industry

Within the European arthroscopy devices market, Germany and the United Kingdom are the leading national markets, driven by factors such as strong healthcare infrastructure, high incidence of musculoskeletal disorders, and advanced medical technology adoption. The Knee Arthroscopy segment dominates the application-based market, owing to its high prevalence among the aging population. Within the product category, Arthroscopes and Arthroscopic Implants constitute the largest market segments.

- Key Drivers for Leading Markets:

- Germany & UK: Well-established healthcare infrastructure, high prevalence of osteoarthritis, robust reimbursement policies.

- Knee Arthroscopy: High incidence of knee injuries and osteoarthritis.

- Arthroscopes & Implants: Essential components of any arthroscopic procedure.

European Arthroscopy Devices Industry Product Innovations

Recent years have witnessed significant advancements in arthroscopy devices, driven by the pursuit of enhanced precision, minimally invasive procedures, and improved patient outcomes. Innovations include the development of smaller, more flexible arthroscopes with improved visualization capabilities, next-generation implants with enhanced biocompatibility and durability, and advanced fluid management systems. These advancements are improving the efficiency and effectiveness of arthroscopic surgeries, leading to faster recovery times and reduced complications, further propelling market growth. The incorporation of robotic assistance and AI-powered imaging analysis is also transforming the field.

Report Segmentation & Scope

This report segments the European arthroscopy devices market across various parameters:

Application: Knee Arthroscopy (largest market share, xx Million in 2025, projected growth of xx% CAGR), Hip Arthroscopy, Spine Arthroscopy, Shoulder and Elbow Arthroscopy, Other Arthroscopy Applications. Each application segment is analyzed considering its specific market size, growth drivers, and competitive landscape.

Product: Arthroscope, Arthroscopic Implant, Fluid Management System, Radiofrequency (RF) System, Visualization System, Other Products. Similar in-depth analysis is provided for each product segment, including market size, growth trajectory, and competitive dynamics. The market for visualization systems is experiencing rapid growth due to technological advancements.

Key Drivers of European Arthroscopy Devices Industry Growth

The European arthroscopy devices market's growth is fueled by a confluence of factors. The aging population necessitates more arthroscopic procedures. Technological advancements, like improved imaging and minimally invasive instruments, increase efficiency and demand. Stronger reimbursement policies and favorable healthcare infrastructure in many European countries support market expansion. The rising prevalence of sports-related injuries also contributes to growth.

Challenges in the European Arthroscopy Devices Industry Sector

The European arthroscopy devices market faces challenges such as stringent regulatory approvals (MDR) impacting product launches and increasing costs. Supply chain disruptions and price pressures from generic competitors can also affect profitability. The intense competition among established players and new entrants requires ongoing innovation and strategic partnerships to succeed.

Leading Players in the European Arthroscopy Devices Industry Market

- Millennium Surgical

- Smith & Nephew PLC

- Arthrex Inc

- GPC Medical

- Sklar Corporation

- Henke Sass Wolf GmbH

- Medtronic PLC

- B Braun Melsungen AG

- Richard Wolf GmbH

- Karl Storz GmbH & Co KG

- Conmed Corporation

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet Holdings Inc

Key Developments in European Arthroscopy Devices Industry Sector

April 2022: Smith & Nephew PLC launched the JOURNEY II Unicompartmental Knee (UK) System, featuring advanced designs and customized sizing. This launch strengthened their position in the knee arthroscopy market.

September 2022: Olympus Corporation launched the VISERA ELITE III surgical visualization platform, enhancing imaging capabilities and impacting the visualization system segment. This improved visualization significantly benefits arthroscopic procedures across all applications.

Strategic European Arthroscopy Devices Industry Market Outlook

The European arthroscopy devices market exhibits significant growth potential over the forecast period. Continuous technological advancements, coupled with the rising prevalence of musculoskeletal disorders and an aging population, will drive demand. Strategic opportunities lie in developing innovative products, focusing on minimally invasive techniques, and expanding into underserved markets. Companies should also focus on strategic partnerships and collaborations to enhance their market position.

European Arthroscopy Devices Industry Segmentation

-

1. Application

- 1.1. Knee Arthroscopy

- 1.2. Hip Arthroscopy

- 1.3. Spine Arthroscopy

- 1.4. Shoulder and Elbow Arthroscopy

- 1.5. Other Arthroscopy Applications

-

2. Product

- 2.1. Arthroscope

- 2.2. Arthroscopic Implant

- 2.3. Fluid Management System

- 2.4. Radiofrequency (RF) System

- 2.5. Visualization System

- 2.6. Other Products

European Arthroscopy Devices Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

European Arthroscopy Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.48% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Incidences of Sports Injuries; Rising Geriatric Population; Technological Advancements in Arthroscopic Implants

- 3.3. Market Restrains

- 3.3.1. Lack of Skilled Surgeons; Stringent Regulatory Requirements

- 3.4. Market Trends

- 3.4.1. Knee Arthroscopy is Expected to Witness a Significant Growth Over the Forecast Period.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Knee Arthroscopy

- 5.1.2. Hip Arthroscopy

- 5.1.3. Spine Arthroscopy

- 5.1.4. Shoulder and Elbow Arthroscopy

- 5.1.5. Other Arthroscopy Applications

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Arthroscope

- 5.2.2. Arthroscopic Implant

- 5.2.3. Fluid Management System

- 5.2.4. Radiofrequency (RF) System

- 5.2.5. Visualization System

- 5.2.6. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Spain

- 5.3.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Germany European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Knee Arthroscopy

- 6.1.2. Hip Arthroscopy

- 6.1.3. Spine Arthroscopy

- 6.1.4. Shoulder and Elbow Arthroscopy

- 6.1.5. Other Arthroscopy Applications

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Arthroscope

- 6.2.2. Arthroscopic Implant

- 6.2.3. Fluid Management System

- 6.2.4. Radiofrequency (RF) System

- 6.2.5. Visualization System

- 6.2.6. Other Products

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. United Kingdom European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Knee Arthroscopy

- 7.1.2. Hip Arthroscopy

- 7.1.3. Spine Arthroscopy

- 7.1.4. Shoulder and Elbow Arthroscopy

- 7.1.5. Other Arthroscopy Applications

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Arthroscope

- 7.2.2. Arthroscopic Implant

- 7.2.3. Fluid Management System

- 7.2.4. Radiofrequency (RF) System

- 7.2.5. Visualization System

- 7.2.6. Other Products

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. France European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Knee Arthroscopy

- 8.1.2. Hip Arthroscopy

- 8.1.3. Spine Arthroscopy

- 8.1.4. Shoulder and Elbow Arthroscopy

- 8.1.5. Other Arthroscopy Applications

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Arthroscope

- 8.2.2. Arthroscopic Implant

- 8.2.3. Fluid Management System

- 8.2.4. Radiofrequency (RF) System

- 8.2.5. Visualization System

- 8.2.6. Other Products

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Italy European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Knee Arthroscopy

- 9.1.2. Hip Arthroscopy

- 9.1.3. Spine Arthroscopy

- 9.1.4. Shoulder and Elbow Arthroscopy

- 9.1.5. Other Arthroscopy Applications

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Arthroscope

- 9.2.2. Arthroscopic Implant

- 9.2.3. Fluid Management System

- 9.2.4. Radiofrequency (RF) System

- 9.2.5. Visualization System

- 9.2.6. Other Products

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Spain European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Knee Arthroscopy

- 10.1.2. Hip Arthroscopy

- 10.1.3. Spine Arthroscopy

- 10.1.4. Shoulder and Elbow Arthroscopy

- 10.1.5. Other Arthroscopy Applications

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Arthroscope

- 10.2.2. Arthroscopic Implant

- 10.2.3. Fluid Management System

- 10.2.4. Radiofrequency (RF) System

- 10.2.5. Visualization System

- 10.2.6. Other Products

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Rest of Europe European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Knee Arthroscopy

- 11.1.2. Hip Arthroscopy

- 11.1.3. Spine Arthroscopy

- 11.1.4. Shoulder and Elbow Arthroscopy

- 11.1.5. Other Arthroscopy Applications

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Arthroscope

- 11.2.2. Arthroscopic Implant

- 11.2.3. Fluid Management System

- 11.2.4. Radiofrequency (RF) System

- 11.2.5. Visualization System

- 11.2.6. Other Products

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Europe European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1. undefined

- 13. Germany European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1. undefined

- 14. France European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1. undefined

- 15. United Kingdom European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1. undefined

- 16. Netherlands European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1. undefined

- 17. Sweden European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 17.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 17.1.1. undefined

- 18. United Kingdom European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 18.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 18.1.1. undefined

- 19. Italy European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 19.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 19.1.1. undefined

- 20. Competitive Analysis

- 20.1. Market Share Analysis 2024

- 20.2. Company Profiles

- 20.2.1 Millennium Surgical

- 20.2.1.1. Overview

- 20.2.1.2. Products

- 20.2.1.3. SWOT Analysis

- 20.2.1.4. Recent Developments

- 20.2.1.5. Financials (Based on Availability)

- 20.2.2 Smith & Nephew PLC

- 20.2.2.1. Overview

- 20.2.2.2. Products

- 20.2.2.3. SWOT Analysis

- 20.2.2.4. Recent Developments

- 20.2.2.5. Financials (Based on Availability)

- 20.2.3 Arthrex Inc

- 20.2.3.1. Overview

- 20.2.3.2. Products

- 20.2.3.3. SWOT Analysis

- 20.2.3.4. Recent Developments

- 20.2.3.5. Financials (Based on Availability)

- 20.2.4 GPC Medical

- 20.2.4.1. Overview

- 20.2.4.2. Products

- 20.2.4.3. SWOT Analysis

- 20.2.4.4. Recent Developments

- 20.2.4.5. Financials (Based on Availability)

- 20.2.5 Sklar Corporation

- 20.2.5.1. Overview

- 20.2.5.2. Products

- 20.2.5.3. SWOT Analysis

- 20.2.5.4. Recent Developments

- 20.2.5.5. Financials (Based on Availability)

- 20.2.6 Henke Sass Wolf GmbH

- 20.2.6.1. Overview

- 20.2.6.2. Products

- 20.2.6.3. SWOT Analysis

- 20.2.6.4. Recent Developments

- 20.2.6.5. Financials (Based on Availability)

- 20.2.7 Medtronic PLC

- 20.2.7.1. Overview

- 20.2.7.2. Products

- 20.2.7.3. SWOT Analysis

- 20.2.7.4. Recent Developments

- 20.2.7.5. Financials (Based on Availability)

- 20.2.8 B Braun Melsungen AG

- 20.2.8.1. Overview

- 20.2.8.2. Products

- 20.2.8.3. SWOT Analysis

- 20.2.8.4. Recent Developments

- 20.2.8.5. Financials (Based on Availability)

- 20.2.9 Richard Wolf GmbH

- 20.2.9.1. Overview

- 20.2.9.2. Products

- 20.2.9.3. SWOT Analysis

- 20.2.9.4. Recent Developments

- 20.2.9.5. Financials (Based on Availability)

- 20.2.10 Karl Storz GmbH & Co KG

- 20.2.10.1. Overview

- 20.2.10.2. Products

- 20.2.10.3. SWOT Analysis

- 20.2.10.4. Recent Developments

- 20.2.10.5. Financials (Based on Availability)

- 20.2.11 Conmed Corporation

- 20.2.11.1. Overview

- 20.2.11.2. Products

- 20.2.11.3. SWOT Analysis

- 20.2.11.4. Recent Developments

- 20.2.11.5. Financials (Based on Availability)

- 20.2.12 Johnson & Johnson

- 20.2.12.1. Overview

- 20.2.12.2. Products

- 20.2.12.3. SWOT Analysis

- 20.2.12.4. Recent Developments

- 20.2.12.5. Financials (Based on Availability)

- 20.2.13 Stryker Corporation

- 20.2.13.1. Overview

- 20.2.13.2. Products

- 20.2.13.3. SWOT Analysis

- 20.2.13.4. Recent Developments

- 20.2.13.5. Financials (Based on Availability)

- 20.2.14 Zimmer Biomet Holdings Inc

- 20.2.14.1. Overview

- 20.2.14.2. Products

- 20.2.14.3. SWOT Analysis

- 20.2.14.4. Recent Developments

- 20.2.14.5. Financials (Based on Availability)

- 20.2.1 Millennium Surgical

List of Figures

- Figure 1: European Arthroscopy Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European Arthroscopy Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: European Arthroscopy Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European Arthroscopy Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 5: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 6: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 7: European Arthroscopy Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: European Arthroscopy Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 15: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 17: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 19: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 21: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 23: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 25: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 26: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 27: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 28: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 29: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 31: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 32: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 33: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 34: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 35: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 37: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 38: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 39: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 40: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 41: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 43: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 44: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 45: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 46: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 47: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 48: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 49: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 50: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 51: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 52: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 53: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 54: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 55: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 56: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 57: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 58: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 59: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 60: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Arthroscopy Devices Industry?

The projected CAGR is approximately 2.48%.

2. Which companies are prominent players in the European Arthroscopy Devices Industry?

Key companies in the market include Millennium Surgical, Smith & Nephew PLC, Arthrex Inc, GPC Medical, Sklar Corporation, Henke Sass Wolf GmbH, Medtronic PLC, B Braun Melsungen AG, Richard Wolf GmbH, Karl Storz GmbH & Co KG, Conmed Corporation, Johnson & Johnson, Stryker Corporation, Zimmer Biomet Holdings Inc.

3. What are the main segments of the European Arthroscopy Devices Industry?

The market segments include Application, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 382.38 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidences of Sports Injuries; Rising Geriatric Population; Technological Advancements in Arthroscopic Implants.

6. What are the notable trends driving market growth?

Knee Arthroscopy is Expected to Witness a Significant Growth Over the Forecast Period..

7. Are there any restraints impacting market growth?

Lack of Skilled Surgeons; Stringent Regulatory Requirements.

8. Can you provide examples of recent developments in the market?

September 2022: Olympus Corporation launched VISERA ELITE III, the new surgical visualization platform. VISERA ELITE III offers various imaging functions. It has been launched in Europe, Japan, and many other parts of the world.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Arthroscopy Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Arthroscopy Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Arthroscopy Devices Industry?

To stay informed about further developments, trends, and reports in the European Arthroscopy Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence