Key Insights

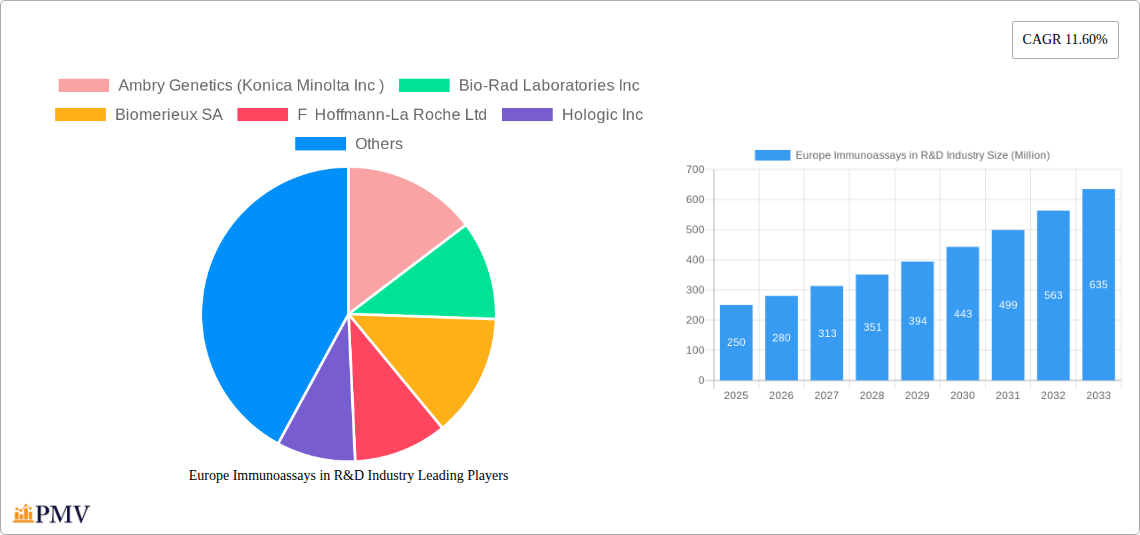

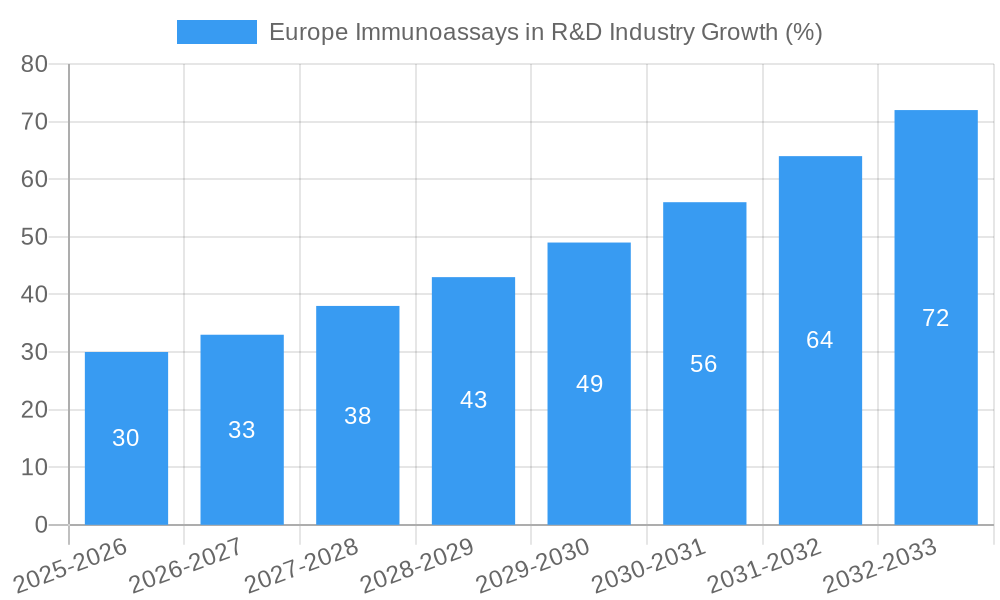

The European immunoassays market within the R&D sector is experiencing robust growth, driven by the increasing prevalence of cancers like prostate, breast, lung, and colorectal, coupled with advancements in biomarker discovery and technological improvements in immunoassay platforms. The market, valued at approximately €[Estimate based on XX Million and European market share - Assume a 25% European share for illustrative purposes. Let's say €250 Million in 2025], is projected to expand at a Compound Annual Growth Rate (CAGR) of 11.60% between 2025 and 2033. This growth is fueled by several key factors: the rising adoption of personalized medicine demanding more precise diagnostic tools, continuous innovation in immunoassay technologies offering higher sensitivity and throughput, and increased funding for cancer research across the European Union. Significant investments from both public and private sectors are accelerating the development and deployment of advanced immunoassay techniques, specifically in OMICS technologies and imaging technologies which enable earlier and more accurate disease detection. This, in turn, drives the demand for sophisticated immunoassay-based R&D services and products.

The market segmentation reveals a strong demand for immunoassays across various cancer types, with prostate, breast, and lung cancer segments leading the way. The protein biomarker segment currently dominates the market, though genetic biomarkers are witnessing significant growth owing to their potential for early disease detection and prognostic capabilities. Competition is fierce among established players like Roche, Thermo Fisher, and Bio-Rad, alongside emerging companies focusing on innovative technologies. The regulatory landscape, including the European Medicines Agency (EMA) guidelines on diagnostic approvals, plays a critical role in shaping market dynamics, influencing both innovation and market access. Further expansion is anticipated across the region due to increasing collaborations between research institutions, pharmaceutical companies, and biotech firms, promoting efficient translation of research findings into clinically relevant diagnostics. The UK, Germany, and France are major contributors to this market, with significant potential for growth in other Western European countries driven by enhanced healthcare infrastructure and growing investments in life sciences.

This comprehensive report provides an in-depth analysis of the Europe Immunoassays in R&D Industry market, covering market size, growth drivers, competitive landscape, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report is crucial for industry stakeholders, investors, and researchers seeking a complete understanding of this dynamic sector. It offers actionable insights and forecasts to inform strategic decision-making.

Europe Immunoassays in R&D Industry Market Structure & Competitive Dynamics

The European immunoassays market within the R&D sector is characterized by a moderately concentrated landscape with several multinational corporations holding significant market share. The market is dynamic, driven by continuous innovation, evolving regulatory frameworks, and ongoing mergers and acquisitions (M&A) activity. Key players engage in strategic collaborations and partnerships to expand their product portfolios and geographic reach. The market concentration ratio (CR5) for 2025 is estimated at xx%.

- Market Share: Thermo Fisher Scientific, Roche, and Abbott collectively hold approximately xx% of the market share in 2025. Smaller players focus on niche segments or specific technologies.

- Innovation Ecosystems: Collaboration between academic institutions, research organizations, and industry players fosters innovation, driving the development of novel immunoassays and biomarker discovery.

- Regulatory Frameworks: Stringent regulatory requirements in Europe influence product development timelines and market entry strategies. Compliance with CE marking and other standards is crucial.

- Product Substitutes: Emerging technologies such as next-generation sequencing (NGS) and advanced imaging techniques present some level of substitution, though immunoassays remain crucial due to their sensitivity, cost-effectiveness, and established clinical utility.

- End-User Trends: Growing demand for personalized medicine and early disease detection drives the adoption of advanced immunoassays for research and development purposes.

- M&A Activity: The past five years have witnessed xx M&A deals in the European immunoassays market, with a total value exceeding xx Million. These activities have reshaped the market landscape and spurred further consolidation.

Europe Immunoassays in R&D Industry Industry Trends & Insights

The European immunoassays market in the R&D sector is projected to experience robust growth, with a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is driven by several key factors:

- Rising Prevalence of Chronic Diseases: The increasing incidence of cancers (prostate, breast, lung, colorectal, cervical) and other chronic diseases fuels demand for sensitive and specific immunoassay-based diagnostic tools.

- Technological Advancements: Continuous improvements in immunoassay technologies, such as multiplex assays and microfluidic devices, enhance throughput, sensitivity, and accuracy. The incorporation of OMICS technologies into immunoassays offers powerful diagnostic and research capabilities.

- Personalized Medicine: The shift towards personalized medicine necessitates accurate and reliable biomarker detection, which further strengthens the demand for advanced immunoassays.

- Increased Research Funding: Significant investments in biomedical research and development from government agencies and private organizations propel innovation in immunoassay technologies.

- Market Penetration: The market penetration of immunoassays in R&D settings is expected to increase significantly, driven by the advantages of these technologies in accelerating drug discovery and development. This is further supported by the increasing adoption of automated and high-throughput assays.

- Competitive Dynamics: Intense competition among major players stimulates innovation and accelerates the adoption of new technologies. Companies are investing in R&D to develop improved immunoassays and gain a competitive advantage.

Dominant Markets & Segments in Europe Immunoassays in R&D Industry

The European immunoassays market in the R&D sector shows variations in dominance across different segments.

By Disease: Prostate cancer, breast cancer, and colorectal cancer represent the largest segments due to their high prevalence and significant unmet needs for effective diagnostic tools.

By Type: Protein biomarkers remain dominant due to their established clinical utility and ease of detection. However, genetic biomarkers are witnessing significant growth due to technological advances and the growing understanding of the genetic basis of diseases.

By Profiling Technology: Immunoassays remain the most widely used technology, given their established reliability and wide applications. However, the integration of OMICS technologies is gaining traction, providing a more holistic understanding of disease mechanisms and enabling the development of more sophisticated diagnostic tools.

Geographic Dominance: Germany, France, and the UK are the leading markets in Europe, driven by their robust healthcare infrastructure, substantial research funding, and high concentration of pharmaceutical and biotechnology companies. These regions also have mature regulatory frameworks supporting the growth of innovative immunoassays. Key drivers include favorable economic policies supporting R&D, advanced healthcare infrastructure, and a strong talent pool of scientists and researchers.

Europe Immunoassays in R&D Industry Product Innovations

Recent advancements in immunoassays for R&D include the development of highly multiplexed assays capable of detecting hundreds of biomarkers simultaneously. This, coupled with miniaturized platforms and improved automation, significantly accelerates research and development processes. Furthermore, novel immunoassay formats employing advanced signal transduction methods, such as electrochemical or optical techniques, are enhancing sensitivity and specificity. These innovations directly address the needs of researchers seeking faster, more sensitive, and more efficient ways to characterize biomarkers, accelerating the progress of drug discovery and diagnostics.

Report Segmentation & Scope

This report segments the European immunoassays market in the R&D sector across several dimensions:

By Disease: Prostate cancer, breast cancer, lung cancer, colorectal cancer, cervical cancer, and other diseases. Each segment is analyzed considering prevalence rates, diagnostic needs, and market size projections.

By Type: Protein biomarkers, genetic biomarkers, and other types. The analysis includes assessment of the performance characteristics of different biomarker types and their suitability for various applications.

By Profiling Technology: OMICS Technology, Imaging Technology, Immunoassays, and Cytogenetics. The report comprehensively assesses market size, growth rates, and competitive dynamics for each technology segment.

Each segment is analyzed in terms of market size, growth projections, and competitive dynamics, offering a holistic view of this diverse market.

Key Drivers of Europe Immunoassays in R&D Industry Growth

The European immunoassays market is fueled by several key drivers. Firstly, the increasing prevalence of chronic diseases creates a significant demand for advanced diagnostic tools. Secondly, substantial investments in biomedical research and technological advancements are continuously improving immunoassay technologies. Finally, the growing adoption of personalized medicine and the rise of OMICS-driven approaches are creating new opportunities for innovation and market expansion. Regulatory support and collaboration between public and private entities contribute to the market's growth as well.

Challenges in the Europe Immunoassays in R&D Industry Sector

Despite considerable growth potential, the European immunoassays market in R&D faces some challenges. Stringent regulatory requirements can prolong product development timelines and increase costs. Competition from alternative technologies, particularly emerging OMICS methods, poses a competitive threat. Supply chain disruptions and pricing pressures also need to be considered to ensure a sustainable growth trajectory. These challenges require careful strategic planning and proactive mitigation strategies.

Leading Players in the Europe Immunoassays in R&D Industry Market

- Ambry Genetics (Konica Minolta Inc)

- Bio-Rad Laboratories Inc

- Biomerieux SA

- F Hoffmann-La Roche Ltd

- Hologic Inc

- Thermo Fisher Scientific Inc

- Epigenomics AG

- Quest Diagnostics

- Qiagen AG

- Creative Diagnostics

- 23andMe

- Johnson & Johnson Services Inc

- Illumina Inc

- Abbott Laboratories Inc

- PerkinElmer Inc

- Agilent Technologies

Key Developments in Europe Immunoassays in R&D Industry Sector

- November 2020: Agilent Technologies launched the Biomarker Pathologist Training Program.

- March 2020: Proteomedix launched Proclarix, a blood-based prostate cancer diagnostic test, in Europe.

Strategic Europe Immunoassays in R&D Industry Market Outlook

The future of the European immunoassays market in R&D is promising. Continued technological innovation, growing demand driven by increasing disease prevalence and the rise of personalized medicine, coupled with strategic collaborations and partnerships, will further accelerate market expansion. The integration of Artificial Intelligence and machine learning into immunoassay platforms promises to revolutionize diagnostics and significantly improve the accuracy and efficiency of biomarker analysis. This presents substantial opportunities for established players and emerging companies to capitalize on this growing market.

Europe Immunoassays in R&D Industry Segmentation

-

1. Disease

- 1.1. Prostate Cancer

- 1.2. Breast Cancer

- 1.3. Lung Cancer

- 1.4. Colorectal Cancer

- 1.5. Cervical Cancer

- 1.6. Other Diseases

-

2. Type

- 2.1. Protein Biomarkers

- 2.2. Genetic Biomarkers

- 2.3. Other Types

-

3. Profiling Technology

- 3.1. OMICS Technology

- 3.2. Imaging Technology

- 3.3. Immunoassays

- 3.4. Cytogenetics

Europe Immunoassays in R&D Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Immunoassays in R&D Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.60% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Burden of Cancer and Higher Acceptance for Treatment; Increasing Focus on Innovative Drug Development

- 3.3. Market Restrains

- 3.3.1. High Cost of Diagnosis

- 3.4. Market Trends

- 3.4.1. The Lung Cancer Segment is Expected to Hold a Major Market Share in the European Cancer Biomarkers Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Disease

- 5.1.1. Prostate Cancer

- 5.1.2. Breast Cancer

- 5.1.3. Lung Cancer

- 5.1.4. Colorectal Cancer

- 5.1.5. Cervical Cancer

- 5.1.6. Other Diseases

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Protein Biomarkers

- 5.2.2. Genetic Biomarkers

- 5.2.3. Other Types

- 5.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 5.3.1. OMICS Technology

- 5.3.2. Imaging Technology

- 5.3.3. Immunoassays

- 5.3.4. Cytogenetics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Disease

- 6. Europe Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Disease

- 6.1.1. Prostate Cancer

- 6.1.2. Breast Cancer

- 6.1.3. Lung Cancer

- 6.1.4. Colorectal Cancer

- 6.1.5. Cervical Cancer

- 6.1.6. Other Diseases

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Protein Biomarkers

- 6.2.2. Genetic Biomarkers

- 6.2.3. Other Types

- 6.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 6.3.1. OMICS Technology

- 6.3.2. Imaging Technology

- 6.3.3. Immunoassays

- 6.3.4. Cytogenetics

- 6.1. Market Analysis, Insights and Forecast - by Disease

- 7. United Kingdom Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Disease

- 7.1.1. Prostate Cancer

- 7.1.2. Breast Cancer

- 7.1.3. Lung Cancer

- 7.1.4. Colorectal Cancer

- 7.1.5. Cervical Cancer

- 7.1.6. Other Diseases

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Protein Biomarkers

- 7.2.2. Genetic Biomarkers

- 7.2.3. Other Types

- 7.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 7.3.1. OMICS Technology

- 7.3.2. Imaging Technology

- 7.3.3. Immunoassays

- 7.3.4. Cytogenetics

- 7.1. Market Analysis, Insights and Forecast - by Disease

- 8. France Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Disease

- 8.1.1. Prostate Cancer

- 8.1.2. Breast Cancer

- 8.1.3. Lung Cancer

- 8.1.4. Colorectal Cancer

- 8.1.5. Cervical Cancer

- 8.1.6. Other Diseases

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Protein Biomarkers

- 8.2.2. Genetic Biomarkers

- 8.2.3. Other Types

- 8.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 8.3.1. OMICS Technology

- 8.3.2. Imaging Technology

- 8.3.3. Immunoassays

- 8.3.4. Cytogenetics

- 8.1. Market Analysis, Insights and Forecast - by Disease

- 9. Italy Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Disease

- 9.1.1. Prostate Cancer

- 9.1.2. Breast Cancer

- 9.1.3. Lung Cancer

- 9.1.4. Colorectal Cancer

- 9.1.5. Cervical Cancer

- 9.1.6. Other Diseases

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Protein Biomarkers

- 9.2.2. Genetic Biomarkers

- 9.2.3. Other Types

- 9.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 9.3.1. OMICS Technology

- 9.3.2. Imaging Technology

- 9.3.3. Immunoassays

- 9.3.4. Cytogenetics

- 9.1. Market Analysis, Insights and Forecast - by Disease

- 10. Spain Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Disease

- 10.1.1. Prostate Cancer

- 10.1.2. Breast Cancer

- 10.1.3. Lung Cancer

- 10.1.4. Colorectal Cancer

- 10.1.5. Cervical Cancer

- 10.1.6. Other Diseases

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Protein Biomarkers

- 10.2.2. Genetic Biomarkers

- 10.2.3. Other Types

- 10.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 10.3.1. OMICS Technology

- 10.3.2. Imaging Technology

- 10.3.3. Immunoassays

- 10.3.4. Cytogenetics

- 10.1. Market Analysis, Insights and Forecast - by Disease

- 11. Rest of Europe Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Disease

- 11.1.1. Prostate Cancer

- 11.1.2. Breast Cancer

- 11.1.3. Lung Cancer

- 11.1.4. Colorectal Cancer

- 11.1.5. Cervical Cancer

- 11.1.6. Other Diseases

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Protein Biomarkers

- 11.2.2. Genetic Biomarkers

- 11.2.3. Other Types

- 11.3. Market Analysis, Insights and Forecast - by Profiling Technology

- 11.3.1. OMICS Technology

- 11.3.2. Imaging Technology

- 11.3.3. Immunoassays

- 11.3.4. Cytogenetics

- 11.1. Market Analysis, Insights and Forecast - by Disease

- 12. Germany Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 13. France Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 14. Italy Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 15. United Kingdom Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 16. Netherlands Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 17. Sweden Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 18. Rest of Europe Europe Immunoassays in R&D Industry Analysis, Insights and Forecast, 2019-2031

- 19. Competitive Analysis

- 19.1. Market Share Analysis 2024

- 19.2. Company Profiles

- 19.2.1 Ambry Genetics (Konica Minolta Inc )

- 19.2.1.1. Overview

- 19.2.1.2. Products

- 19.2.1.3. SWOT Analysis

- 19.2.1.4. Recent Developments

- 19.2.1.5. Financials (Based on Availability)

- 19.2.2 Bio-Rad Laboratories Inc

- 19.2.2.1. Overview

- 19.2.2.2. Products

- 19.2.2.3. SWOT Analysis

- 19.2.2.4. Recent Developments

- 19.2.2.5. Financials (Based on Availability)

- 19.2.3 Biomerieux SA

- 19.2.3.1. Overview

- 19.2.3.2. Products

- 19.2.3.3. SWOT Analysis

- 19.2.3.4. Recent Developments

- 19.2.3.5. Financials (Based on Availability)

- 19.2.4 F Hoffmann-La Roche Ltd

- 19.2.4.1. Overview

- 19.2.4.2. Products

- 19.2.4.3. SWOT Analysis

- 19.2.4.4. Recent Developments

- 19.2.4.5. Financials (Based on Availability)

- 19.2.5 Hologic Inc

- 19.2.5.1. Overview

- 19.2.5.2. Products

- 19.2.5.3. SWOT Analysis

- 19.2.5.4. Recent Developments

- 19.2.5.5. Financials (Based on Availability)

- 19.2.6 Thermo Fisher Scientific Inc

- 19.2.6.1. Overview

- 19.2.6.2. Products

- 19.2.6.3. SWOT Analysis

- 19.2.6.4. Recent Developments

- 19.2.6.5. Financials (Based on Availability)

- 19.2.7 Epigenomics AG

- 19.2.7.1. Overview

- 19.2.7.2. Products

- 19.2.7.3. SWOT Analysis

- 19.2.7.4. Recent Developments

- 19.2.7.5. Financials (Based on Availability)

- 19.2.8 Quest Diagnostics

- 19.2.8.1. Overview

- 19.2.8.2. Products

- 19.2.8.3. SWOT Analysis

- 19.2.8.4. Recent Developments

- 19.2.8.5. Financials (Based on Availability)

- 19.2.9 Qiagen AG

- 19.2.9.1. Overview

- 19.2.9.2. Products

- 19.2.9.3. SWOT Analysis

- 19.2.9.4. Recent Developments

- 19.2.9.5. Financials (Based on Availability)

- 19.2.10 Creative Diagnostics

- 19.2.10.1. Overview

- 19.2.10.2. Products

- 19.2.10.3. SWOT Analysis

- 19.2.10.4. Recent Developments

- 19.2.10.5. Financials (Based on Availability)

- 19.2.11 23andMe

- 19.2.11.1. Overview

- 19.2.11.2. Products

- 19.2.11.3. SWOT Analysis

- 19.2.11.4. Recent Developments

- 19.2.11.5. Financials (Based on Availability)

- 19.2.12 Johnson & Johnson Services Inc

- 19.2.12.1. Overview

- 19.2.12.2. Products

- 19.2.12.3. SWOT Analysis

- 19.2.12.4. Recent Developments

- 19.2.12.5. Financials (Based on Availability)

- 19.2.13 Illumina Inc

- 19.2.13.1. Overview

- 19.2.13.2. Products

- 19.2.13.3. SWOT Analysis

- 19.2.13.4. Recent Developments

- 19.2.13.5. Financials (Based on Availability)

- 19.2.14 Abbott Laboratories Inc

- 19.2.14.1. Overview

- 19.2.14.2. Products

- 19.2.14.3. SWOT Analysis

- 19.2.14.4. Recent Developments

- 19.2.14.5. Financials (Based on Availability)

- 19.2.15 PerkinElmer Inc *List Not Exhaustive

- 19.2.15.1. Overview

- 19.2.15.2. Products

- 19.2.15.3. SWOT Analysis

- 19.2.15.4. Recent Developments

- 19.2.15.5. Financials (Based on Availability)

- 19.2.16 Agilent Technologies

- 19.2.16.1. Overview

- 19.2.16.2. Products

- 19.2.16.3. SWOT Analysis

- 19.2.16.4. Recent Developments

- 19.2.16.5. Financials (Based on Availability)

- 19.2.1 Ambry Genetics (Konica Minolta Inc )

List of Figures

- Figure 1: Europe Immunoassays in R&D Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Immunoassays in R&D Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 3: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 5: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 15: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 17: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Germany Europe Immunoassays in R&D Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 20: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 21: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 22: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 24: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 25: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 26: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 28: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 29: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 30: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 31: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 32: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 33: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 34: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 35: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 36: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 37: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Profiling Technology 2019 & 2032

- Table 38: Europe Immunoassays in R&D Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Immunoassays in R&D Industry?

The projected CAGR is approximately 11.60%.

2. Which companies are prominent players in the Europe Immunoassays in R&D Industry?

Key companies in the market include Ambry Genetics (Konica Minolta Inc ), Bio-Rad Laboratories Inc, Biomerieux SA, F Hoffmann-La Roche Ltd, Hologic Inc, Thermo Fisher Scientific Inc, Epigenomics AG, Quest Diagnostics, Qiagen AG, Creative Diagnostics, 23andMe, Johnson & Johnson Services Inc, Illumina Inc, Abbott Laboratories Inc, PerkinElmer Inc *List Not Exhaustive, Agilent Technologies.

3. What are the main segments of the Europe Immunoassays in R&D Industry?

The market segments include Disease, Type, Profiling Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Burden of Cancer and Higher Acceptance for Treatment; Increasing Focus on Innovative Drug Development.

6. What are the notable trends driving market growth?

The Lung Cancer Segment is Expected to Hold a Major Market Share in the European Cancer Biomarkers Market.

7. Are there any restraints impacting market growth?

High Cost of Diagnosis.

8. Can you provide examples of recent developments in the market?

In November 2020, Agilent Technologies announced the launch of the Biomarker Pathologist Training Program, a global initiative created to empower pathologists to score biomarkers accurately and confidently.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Immunoassays in R&D Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Immunoassays in R&D Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Immunoassays in R&D Industry?

To stay informed about further developments, trends, and reports in the Europe Immunoassays in R&D Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence