Key Insights

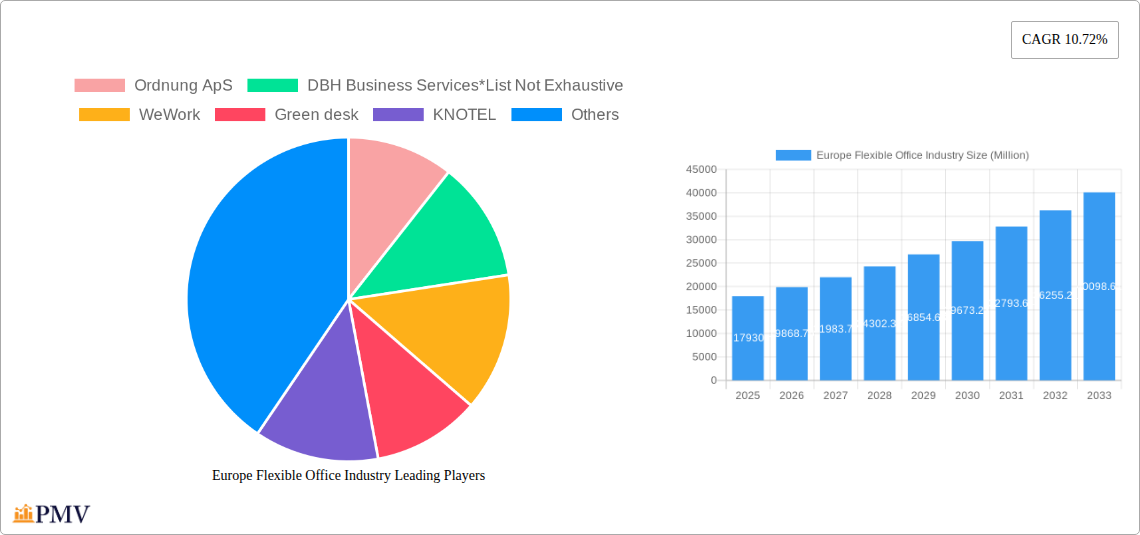

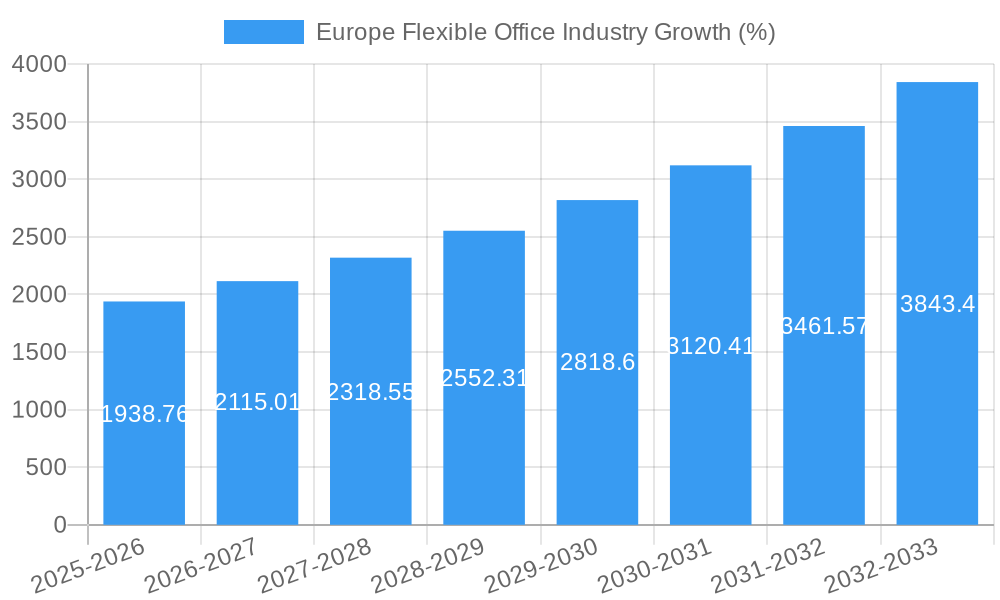

The European flexible office market, valued at €17.93 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 10.72% from 2025 to 2033. This surge is driven by several key factors. The increasing adoption of hybrid work models across various sectors, including IT & Telecommunications, Media & Entertainment, and Retail & Consumer Goods, is a significant catalyst. Businesses are seeking cost-effective solutions with greater flexibility to adapt to fluctuating workforce needs, leading to a preference for flexible workspace arrangements over traditional long-term leases. Technological advancements, such as improved booking platforms and workspace management software, further enhance the appeal and accessibility of these services. Furthermore, a growing entrepreneurial landscape and the rise of startups contribute significantly to the demand for flexible office spaces, particularly co-working spaces and virtual offices. Germany, France, and the United Kingdom currently represent the largest national markets within Europe, though other countries like the Netherlands and Sweden are exhibiting substantial growth potential. Competition among providers, including established players like Regus and WeWork alongside smaller, specialized operators, is fostering innovation and driving down costs.

However, the market faces some challenges. Economic downturns can negatively impact demand, particularly for more expensive private office spaces. The fluctuating availability of suitable locations in prime business districts and the rising cost of real estate in major European cities are potential restraints on market expansion. Competition is intensifying, requiring providers to offer innovative services and attractive pricing models to maintain a competitive edge. Future market growth will depend on factors such as continued economic stability, the sustained popularity of hybrid work models, and the ability of providers to adapt to evolving customer preferences and technological advancements. The continued expansion of high-speed internet infrastructure across Europe will also be crucial in supporting the growth of virtual office options.

Europe Flexible Office Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Europe flexible office industry, offering invaluable insights for investors, businesses, and industry professionals. Covering the period from 2019 to 2033, with a focus on 2025, this report unveils market dynamics, growth drivers, challenges, and future opportunities within this rapidly evolving sector. The report meticulously examines market segmentation by type (Private Offices, Co-working Spaces, Virtual Offices) and end-user (IT & Telecommunications, Media & Entertainment, Retail & Consumer Goods), presenting a detailed forecast for the 2025-2033 period. With a focus on key players like WeWork, Regus Group, and many more, this report is your essential guide to navigating the complexities of the European flexible office market. The report projects a market size of xx Million by 2025 and xx Million by 2033.

Europe Flexible Office Industry Market Structure & Competitive Dynamics

The European flexible office market exhibits a moderately concentrated structure, with a few major players commanding significant market share. WeWork, Regus Group, and IWG PLC collectively hold an estimated xx% of the market, while numerous smaller operators and independent providers constitute the remaining share. The industry is characterized by a dynamic competitive landscape marked by continuous innovation, mergers and acquisitions (M&A), and evolving regulatory frameworks. Recent M&A activity, such as Industrious' acquisition of Great Room Offices and Welkin & Meraki in May 2022, demonstrates the industry's consolidation trend. This deal, valued at xx Million, significantly boosted Industrious' European presence. Other notable players include Ordnung ApS, DBH Business Services, Green desk, KNOTEL, The Office Group, WOJO, Mindspace, and Matrikel. The market's innovation ecosystem thrives on technological advancements in workspace management software and flexible leasing models. These are further augmented by evolving end-user preferences, demanding more adaptable and technologically advanced workspaces. Regulatory frameworks, varying across European nations, play a crucial role in shaping the operational landscape. Product substitutes, such as traditional office spaces and home offices, continue to present competitive pressure.

Europe Flexible Office Industry Industry Trends & Insights

The European flexible office market is experiencing robust growth, driven by several key factors. The increasing adoption of hybrid work models, fueled by technological advancements and changing employee preferences, is a major catalyst. The shift towards agile work cultures, coupled with the demand for cost-effective and flexible workspace solutions, is further stimulating market expansion. Technological disruptions, such as the implementation of smart office technologies and workspace management platforms, enhance operational efficiency and user experience. Consumer preferences are shifting towards experience-driven workspaces, favoring locations with amenities and collaborative environments. The industry's CAGR during the historical period (2019-2024) is estimated at xx%, with a projected CAGR of xx% during the forecast period (2025-2033). Market penetration is steadily increasing, particularly in major urban centers across Europe. Competitive dynamics are influenced by factors such as pricing strategies, service offerings, and geographical reach.

Dominant Markets & Segments in Europe Flexible Office Industry

Leading Regions/Countries: The UK, Germany, and France represent the dominant markets within Europe, driven by strong economic activity, robust infrastructure, and a high concentration of businesses adopting flexible work arrangements. These countries offer large talent pools, favorable business environments and well-established transportation networks.

Dominant Segments:

- By Type: Co-working spaces currently hold the largest market share, fueled by the rising popularity of collaborative work environments and the cost-effectiveness of shared facilities. Private offices continue to attract businesses seeking greater privacy and control over their workspace. Virtual offices cater to the needs of entrepreneurs and remote workers.

- By End-User: The IT and Telecommunications sector, followed by Media and Entertainment, are the leading end-users of flexible office spaces. These sectors are characterized by high employee mobility and a need for adaptable workspaces.

Key Drivers:

- Economic Policies: Government incentives for business growth and flexible work arrangements contribute significantly to market expansion in various regions.

- Infrastructure: Well-developed transportation networks and reliable internet connectivity are crucial for supporting the growth of flexible workspaces, especially in major urban hubs.

Europe Flexible Office Industry Product Innovations

The flexible office industry showcases ongoing innovation in workspace design, technology integration, and service offerings. Smart building technologies, incorporating IoT sensors and data analytics for optimizing energy consumption and enhancing workspace management, are gaining traction. Companies are integrating advanced booking systems, communication platforms, and virtual reality tools to enhance user experience and operational efficiency. These innovations address the increasing demand for flexible, efficient, and technologically advanced workspaces, directly impacting market competition and customer satisfaction.

Report Segmentation & Scope

This report segments the European flexible office market by Type: Private Offices, Co-working Spaces, and Virtual Offices; and by End-User: IT and Telecommunications, Media and Entertainment, and Retail and Consumer Goods. Each segment's growth projections, market size, and competitive dynamics are analyzed, providing a comprehensive understanding of the market's various facets. For instance, the co-working space segment is projected to experience significant growth due to its affordability and collaborative features, while the private office segment will maintain a steady growth trajectory driven by the need for privacy and dedicated workspaces for teams. The virtual office segment will see moderate growth, driven by the continued rise of remote work.

Key Drivers of Europe Flexible Office Industry Growth

The European flexible office industry's growth is fueled by several key drivers: the increasing adoption of hybrid and remote work models, technological advancements improving workspace management, evolving consumer preferences towards experience-driven work environments, and supportive government policies encouraging flexible work arrangements. These factors contribute to the expanding demand for adaptable and efficient workspace solutions across diverse industry sectors.

Challenges in the Europe Flexible Office Industry Sector

The sector faces challenges such as intense competition, economic uncertainties impacting demand, regulatory complexities varying across European nations, and potential supply chain disruptions affecting the availability of workspace solutions and related services. These factors can influence market growth and profitability, requiring strategic adaptations from operators.

Leading Players in the Europe Flexible Office Industry Market

- Ordnung ApS

- DBH Business Services

- WeWork

- Green desk

- KNOTEL

- The Office Group

- WOJO

- Mindspace

- Matrikel

- Regus Group

Key Developments in Europe Flexible Office Industry Sector

- July 2022: Upflex partnered with Landmark Space, integrating its technology platform for on-demand workspace booking. This significantly enhanced Landmark Space's operational efficiency and user experience.

- May 2022: Industrious' acquisition of Great Room Offices and Welkin & Meraki expanded its European footprint and market share, intensifying competition within the sector.

Strategic Europe Flexible Office Industry Market Outlook

The European flexible office market presents significant growth potential driven by ongoing technological advancements, evolving work styles, and the increasing demand for adaptable and efficient workspace solutions. Strategic opportunities lie in providing innovative workspace designs, integrating advanced technologies, offering customized service packages, and expanding into underserved markets. Focusing on sustainability and creating collaborative communities within flexible workspaces will be key differentiators in the coming years.

Europe Flexible Office Industry Segmentation

-

1. Type

- 1.1. Private Offices

- 1.2. Coworking Spaces

- 1.3. Virtual Offices

-

2. End User

- 2.1. IT and Telecommunications

- 2.2. Media and Entertainment

- 2.3. Retail and Consumer Goods

Europe Flexible Office Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Rest of Europe

Europe Flexible Office Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.72% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Disposable Income and Middle-Class Expansion; Increased Awareness of Roofing Solutions

- 3.3. Market Restrains

- 3.3.1. The presence of counterfeit or substandard roofing materials in the market poses a significant challenge; The roofing industry faces a shortage of skilled labor

- 3.4. Market Trends

- 3.4.1. Western Europe Leading the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Private Offices

- 5.1.2. Coworking Spaces

- 5.1.3. Virtual Offices

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. IT and Telecommunications

- 5.2.2. Media and Entertainment

- 5.2.3. Retail and Consumer Goods

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Private Offices

- 6.1.2. Coworking Spaces

- 6.1.3. Virtual Offices

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. IT and Telecommunications

- 6.2.2. Media and Entertainment

- 6.2.3. Retail and Consumer Goods

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Kingdom Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Private Offices

- 7.1.2. Coworking Spaces

- 7.1.3. Virtual Offices

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. IT and Telecommunications

- 7.2.2. Media and Entertainment

- 7.2.3. Retail and Consumer Goods

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. France Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Private Offices

- 8.1.2. Coworking Spaces

- 8.1.3. Virtual Offices

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. IT and Telecommunications

- 8.2.2. Media and Entertainment

- 8.2.3. Retail and Consumer Goods

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of Europe Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Private Offices

- 9.1.2. Coworking Spaces

- 9.1.3. Virtual Offices

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. IT and Telecommunications

- 9.2.2. Media and Entertainment

- 9.2.3. Retail and Consumer Goods

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Germany Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 11. France Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 12. Italy Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 13. United Kingdom Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 14. Netherlands Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 15. Sweden Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 16. Rest of Europe Europe Flexible Office Industry Analysis, Insights and Forecast, 2019-2031

- 17. Competitive Analysis

- 17.1. Market Share Analysis 2024

- 17.2. Company Profiles

- 17.2.1 Ordnung ApS

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 DBH Business Services*List Not Exhaustive

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 WeWork

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 Green desk

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 KNOTEL

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.6 The Office Group

- 17.2.6.1. Overview

- 17.2.6.2. Products

- 17.2.6.3. SWOT Analysis

- 17.2.6.4. Recent Developments

- 17.2.6.5. Financials (Based on Availability)

- 17.2.7 WOJO

- 17.2.7.1. Overview

- 17.2.7.2. Products

- 17.2.7.3. SWOT Analysis

- 17.2.7.4. Recent Developments

- 17.2.7.5. Financials (Based on Availability)

- 17.2.8 Mindspace

- 17.2.8.1. Overview

- 17.2.8.2. Products

- 17.2.8.3. SWOT Analysis

- 17.2.8.4. Recent Developments

- 17.2.8.5. Financials (Based on Availability)

- 17.2.9 Matrikel

- 17.2.9.1. Overview

- 17.2.9.2. Products

- 17.2.9.3. SWOT Analysis

- 17.2.9.4. Recent Developments

- 17.2.9.5. Financials (Based on Availability)

- 17.2.10 Regus Group

- 17.2.10.1. Overview

- 17.2.10.2. Products

- 17.2.10.3. SWOT Analysis

- 17.2.10.4. Recent Developments

- 17.2.10.5. Financials (Based on Availability)

- 17.2.1 Ordnung ApS

List of Figures

- Figure 1: Europe Flexible Office Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Flexible Office Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Flexible Office Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Flexible Office Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Flexible Office Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 4: Europe Flexible Office Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Flexible Office Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Flexible Office Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Flexible Office Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: Europe Flexible Office Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 15: Europe Flexible Office Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Europe Flexible Office Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 17: Europe Flexible Office Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 18: Europe Flexible Office Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Europe Flexible Office Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 20: Europe Flexible Office Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 21: Europe Flexible Office Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Europe Flexible Office Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 23: Europe Flexible Office Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 24: Europe Flexible Office Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Flexible Office Industry?

The projected CAGR is approximately 10.72%.

2. Which companies are prominent players in the Europe Flexible Office Industry?

Key companies in the market include Ordnung ApS, DBH Business Services*List Not Exhaustive, WeWork, Green desk, KNOTEL, The Office Group, WOJO, Mindspace, Matrikel, Regus Group.

3. What are the main segments of the Europe Flexible Office Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.93 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Disposable Income and Middle-Class Expansion; Increased Awareness of Roofing Solutions.

6. What are the notable trends driving market growth?

Western Europe Leading the Market.

7. Are there any restraints impacting market growth?

The presence of counterfeit or substandard roofing materials in the market poses a significant challenge; The roofing industry faces a shortage of skilled labor.

8. Can you provide examples of recent developments in the market?

July 2022: Upflex, a leading global provider of hybrid workspace solutions, has signed a significant commercial deal with Landmark Space, one of the UK's largest providers of flexible workspaces. The deal makes Landmark the first Flex workspace operator to use Upflex's technology platform to manage Landmark's on-demand services, enabling seamless real-time booking of desks and meeting rooms across Landmark's Space network.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Flexible Office Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Flexible Office Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Flexible Office Industry?

To stay informed about further developments, trends, and reports in the Europe Flexible Office Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence