Key Insights

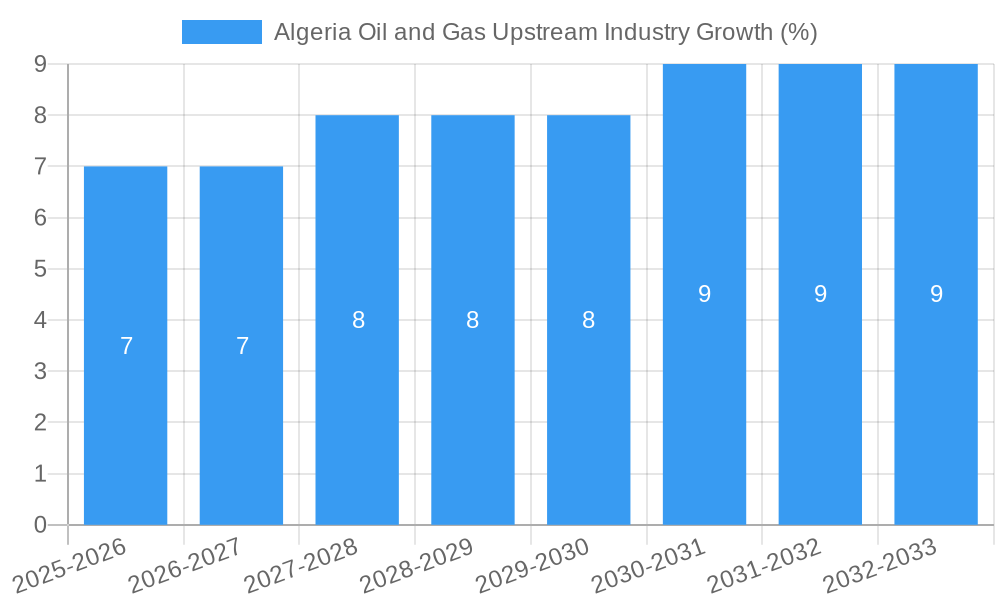

The Algerian oil and gas upstream industry, while facing headwinds, presents a promising investment landscape for the foreseeable future. The market, currently valued in the hundreds of millions (a precise figure cannot be provided without the missing market size "XX" value), is experiencing steady growth, reflected in a Compound Annual Growth Rate (CAGR) exceeding 2.32%. This positive trajectory is driven by several factors: Algeria's significant hydrocarbon reserves, ongoing efforts to modernize its infrastructure, and the persistent global demand for energy despite the rise of renewables. However, the sector is not without its challenges. Aging infrastructure, the need for substantial investment in exploration and production technologies, and fluctuating global oil prices pose significant constraints. The segmentation of the market into onshore and offshore projects, further categorized by existing, pipeline, and upcoming initiatives, highlights the diverse investment opportunities available within the Algerian energy sector. Major players like Engie SA, TotalEnergies SA, BP PLC, and Sonatrach SPA are actively involved, showcasing the industry's importance to both domestic and international stakeholders.

The forecast period (2025-2033) anticipates continued growth, although the pace may vary depending on global economic conditions and geopolitical factors. Successful navigation of the sector's challenges will depend on strategic investments in technological innovation, effective management of resources, and collaborations between international and domestic players. The industry's future success hinges on a balanced approach, capitalizing on the country's significant reserves while addressing the imperative of sustainability and diversification in the energy mix. The expansion of the pipeline and upcoming projects segments indicates a focus on future growth and development, despite the limitations posed by aging infrastructure and global market volatility.

Algeria Oil and Gas Upstream Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of Algeria's oil and gas upstream industry, covering the period from 2019 to 2033. It offers in-depth insights into market structure, competitive dynamics, key players, industry trends, and future growth prospects. The report is essential for industry professionals, investors, and policymakers seeking a thorough understanding of this dynamic sector. The base year for this analysis is 2025, with estimations for 2025 and forecasts extending to 2033. The historical period analyzed covers 2019-2024.

Algeria Oil and Gas Upstream Industry Market Structure & Competitive Dynamics

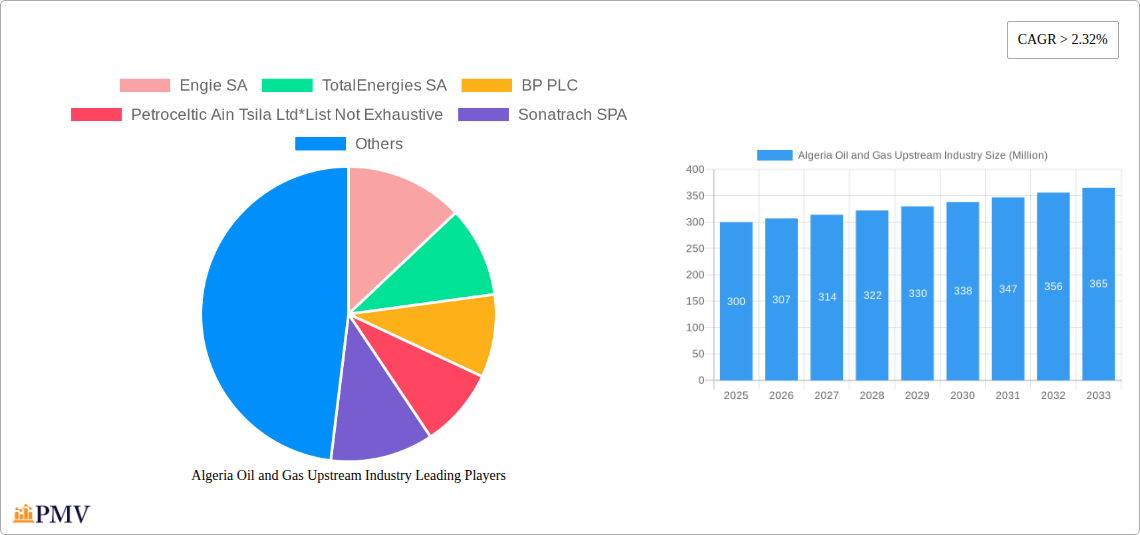

Algeria's oil and gas upstream sector is characterized by a mix of international and national players, with Sonatrach SPA holding a dominant position. Market concentration is relatively high, with a few major companies controlling a significant share of production and exploration activities. The regulatory framework plays a crucial role, influencing investment decisions and operational strategies. The presence of both onshore and offshore operations introduces varying levels of complexity and cost structures.

Market Concentration: Sonatrach maintains a significant market share, estimated at xx% in 2025. International players like Engie SA, TotalEnergies SA, and BP PLC hold substantial shares, although their exact percentages are commercially sensitive. Petroceltic Ain Tsila Ltd also contributes to the market.

Innovation Ecosystems: Investment in technology and innovation is crucial for enhancing efficiency and exploring new reserves. Collaboration between international companies and Sonatrach is driving technological advancements in exploration and production.

Mergers & Acquisitions (M&A): The sector has witnessed significant M&A activity, including Eni SpA's acquisition of BP's upstream assets in Amenas and Salah in September 2022. While the precise value of this deal isn’t publicly disclosed, we estimate it at xx Million. Further M&A activity is expected, driven by the need for consolidation and access to new resources.

Product Substitutes: While there are no direct substitutes for oil and gas in the upstream sector, alternative energy sources, such as renewable energy, pose a long-term competitive threat, especially for gas.

End-User Trends: The global demand for oil and gas influences Algeria's upstream sector. Fluctuations in global energy prices directly impact investment decisions and production levels.

Algeria Oil and Gas Upstream Industry Industry Trends & Insights

The Algerian oil and gas upstream industry is experiencing a complex interplay of factors affecting its growth trajectory. While global energy demand and prices continue to be significant drivers, domestic policy, technological advancements, and the global transition to lower-carbon energy sources are reshaping the industry landscape.

The industry's Compound Annual Growth Rate (CAGR) is projected at xx% during the forecast period (2025-2033), reflecting a combination of factors. Increased exploration and production efforts, particularly in areas such as the Berkine Basin, contribute positively. However, the aging infrastructure and potential for resource depletion create challenges for sustained high growth.

Technological disruptions, such as the adoption of advanced drilling techniques and enhanced oil recovery (EOR) methods, are improving efficiency and boosting output. However, these advancements require significant capital investment and expertise. Consumer preferences for cleaner energy sources and stricter environmental regulations also influence investment in the sector. The successful integration of new technologies will be crucial for maintaining competitiveness in the global energy market. Market penetration of advanced technologies remains at xx% in 2025, projected to rise to xx% by 2033.

Dominant Markets & Segments in Algeria Oil and Gas Upstream Industry

The Algerian oil and gas upstream industry is dominated by onshore operations, which currently account for a larger share of production. However, exploration and development efforts are increasingly focused on offshore resources, creating opportunities for growth in this segment.

Onshore:

- Key Drivers: Existing infrastructure, established production areas, and relatively lower exploration costs compared to offshore operations.

- Dominance Analysis: Onshore currently holds the largest share of production, due to mature fields and easier access. However, production from onshore fields is expected to decline gradually over the forecast period.

Offshore:

- Key Drivers: Potential for significant undiscovered reserves, driving exploration and investment. Government incentives for offshore development are additional drivers.

- Dominance Analysis: While currently less dominant than onshore, offshore production is expected to gain significant traction as new discoveries are made and developed, potentially becoming a major contributor to overall production by 2033.

Existing Projects: These projects contribute significantly to the current production levels, though their output may decline over time.

Projects in Pipeline: These represent potential future production increases, but their realization is subject to various factors, including funding, regulatory approvals, and technological feasibility.

Upcoming Projects: These are early-stage projects with significant uncertainties; their contribution to production is subject to a long-term perspective.

Algeria Oil and Gas Upstream Industry Product Innovations

Innovation in the Algerian oil and gas upstream sector is primarily focused on improving exploration and production efficiency through the adoption of enhanced oil recovery techniques and advanced drilling technologies. These innovations aim to optimize resource extraction, reduce operating costs, and improve environmental performance. The successful integration of these technologies is crucial for maintaining competitiveness and achieving sustainable growth in a changing energy landscape.

Report Segmentation & Scope

This report segments the Algerian oil and gas upstream market by location (onshore and offshore) and project status (existing projects, projects in pipeline, and upcoming projects). Each segment is analyzed with respect to its market size, growth projections, and competitive dynamics. Growth projections for onshore operations are estimated at xx% CAGR from 2025-2033. Offshore operations are projected to experience a higher CAGR of xx% over the same period, driven by increased investment and exploration. Competitive dynamics within each segment are shaped by the presence of both domestic and international players.

Key Drivers of Algeria Oil and Gas Upstream Industry Growth

Several factors drive the growth of Algeria's oil and gas upstream industry. These include:

- Government policies: Government initiatives to support exploration and production, coupled with favorable fiscal terms, incentivize investment.

- Technological advancements: The adoption of advanced drilling techniques and EOR methods significantly enhances efficiency and output.

- Global energy demand: Continued global demand for oil and gas ensures a market for Algerian production, despite the global shift toward renewable energy.

Challenges in the Algeria Oil and Gas Upstream Industry Sector

The Algerian oil and gas upstream industry faces several challenges, including:

- Aging infrastructure: Maintaining and upgrading existing infrastructure requires substantial investment.

- Resource depletion: Many established fields are in their later stages of production, requiring efforts to enhance oil recovery or explore new reserves.

- Geopolitical risks: Political stability and security concerns can disrupt operations and hinder investment.

- Regulatory hurdles: Bureaucratic procedures and permitting can delay projects and add to the costs.

Leading Players in the Algeria Oil and Gas Upstream Industry Market

- Engie SA

- TotalEnergies SA

- BP PLC

- Petroceltic Ain Tsila Ltd

- Sonatrach SPA

Key Developments in Algeria Oil and Gas Upstream Industry Sector

- March 2022: Eni and Sonatrach announced a significant oil and gas discovery in the Zemlet el Arbi concession, potentially containing 140 Million barrels of oil. This discovery boosts Algeria's oil reserves and strengthens its position in the global energy market.

- September 2022: Eni SpA acquired BP's upstream assets in Amenas and Salah, gaining access to significant gas production capacity and strengthening its presence in the Algerian market. This acquisition highlights ongoing consolidation within the sector.

Strategic Algeria Oil and Gas Upstream Industry Market Outlook

The Algerian oil and gas upstream industry is poised for continued growth, albeit with a more nuanced outlook than in the past. While global trends towards decarbonization present challenges, Algeria's significant hydrocarbon reserves and ongoing exploration efforts offer considerable potential. Strategic opportunities lie in leveraging technological advancements to enhance efficiency, attracting foreign investment through favorable regulatory environments, and developing offshore resources to bolster production capacity. Strategic partnerships, focusing on technology transfer and joint ventures, will be key for success.

Algeria Oil and Gas Upstream Industry Segmentation

-

1. Location

-

1.1. Onshore

-

1.1.1. Overview

- 1.1.1.1. Existing Projects

- 1.1.1.2. Projects in Pipeline

- 1.1.1.3. Upcoming Projects

-

1.1.1. Overview

- 1.2. Offshore

-

1.1. Onshore

Algeria Oil and Gas Upstream Industry Segmentation By Geography

- 1. Algeria

Algeria Oil and Gas Upstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 2.32% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Demand for Clean Energy Sources4.; Supportive Government Policies

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing Adoption of Other Alternative Clean Energy Sources

- 3.4. Market Trends

- 3.4.1. Onshore Gas Field Production to Witness Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Algeria Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Location

- 5.1.1. Onshore

- 5.1.1.1. Overview

- 5.1.1.1.1. Existing Projects

- 5.1.1.1.2. Projects in Pipeline

- 5.1.1.1.3. Upcoming Projects

- 5.1.1.1. Overview

- 5.1.2. Offshore

- 5.1.1. Onshore

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Algeria

- 5.1. Market Analysis, Insights and Forecast - by Location

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Engie SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 TotalEnergies SA

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 BP PLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Petroceltic Ain Tsila Ltd*List Not Exhaustive

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Sonatrach SPA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.1 Engie SA

List of Figures

- Figure 1: Algeria Oil and Gas Upstream Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Algeria Oil and Gas Upstream Industry Share (%) by Company 2024

List of Tables

- Table 1: Algeria Oil and Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Algeria Oil and Gas Upstream Industry Revenue Million Forecast, by Location 2019 & 2032

- Table 3: Algeria Oil and Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Algeria Oil and Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Algeria Oil and Gas Upstream Industry Revenue Million Forecast, by Location 2019 & 2032

- Table 6: Algeria Oil and Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Algeria Oil and Gas Upstream Industry?

The projected CAGR is approximately > 2.32%.

2. Which companies are prominent players in the Algeria Oil and Gas Upstream Industry?

Key companies in the market include Engie SA, TotalEnergies SA, BP PLC, Petroceltic Ain Tsila Ltd*List Not Exhaustive, Sonatrach SPA.

3. What are the main segments of the Algeria Oil and Gas Upstream Industry?

The market segments include Location .

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Demand for Clean Energy Sources4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Onshore Gas Field Production to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Other Alternative Clean Energy Sources.

8. Can you provide examples of recent developments in the market?

In March 2022, Eni and Sonatrach announced a substantial oil and accompanying gas discovery in the Zemlet el Arbi concession in the Algerian desert's Berkine North Basin. This concession is being operated in a joint venture with Sonatrach (51%), Eni (49%), and other parties. According to preliminary assessments of the extent of the discovery, there may be 140 million barrels of oil in place.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Algeria Oil and Gas Upstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Algeria Oil and Gas Upstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Algeria Oil and Gas Upstream Industry?

To stay informed about further developments, trends, and reports in the Algeria Oil and Gas Upstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence