Key Insights

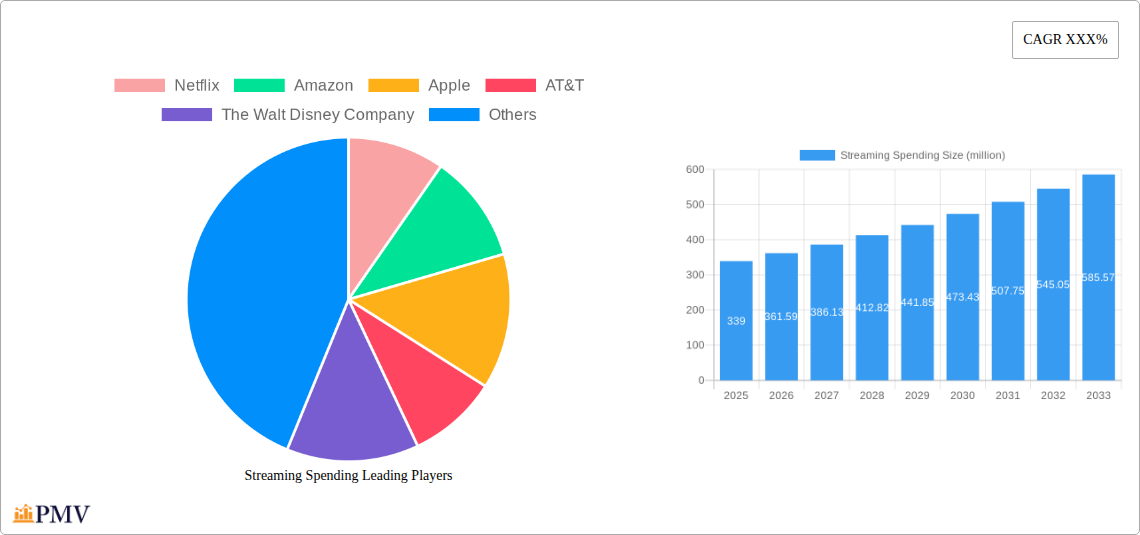

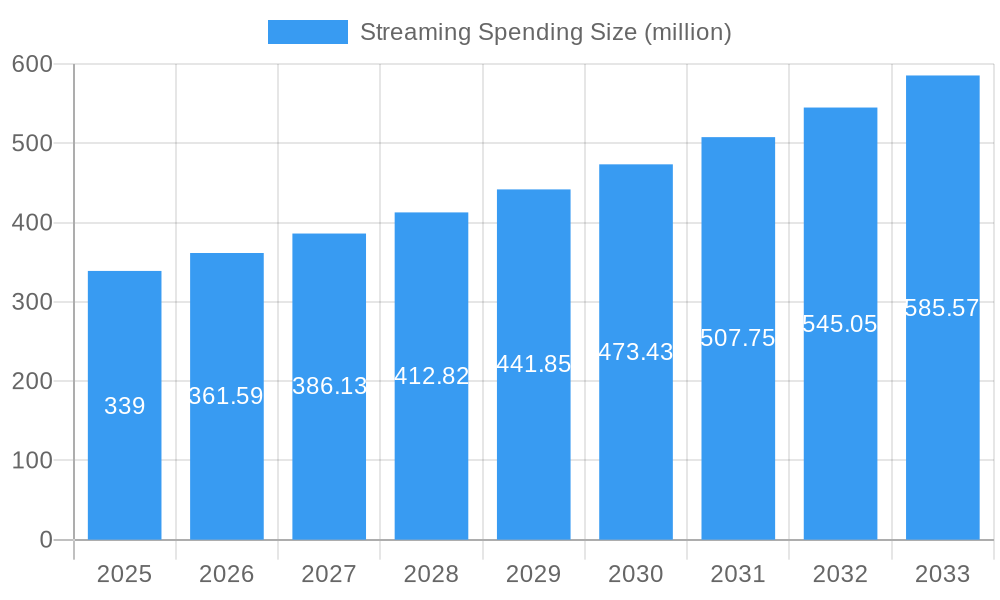

The global Streaming Spending market is experiencing robust expansion, projected to reach $339 million in 2025, with a significant Compound Annual Growth Rate (CAGR) of 10.7% expected to sustain this momentum through the forecast period of 2025-2033. This growth is propelled by an increasing consumer demand for on-demand entertainment and educational content across diverse platforms. Key drivers include the widespread adoption of high-speed internet, the proliferation of smart devices, and the continuous innovation in content delivery and user experience by major players like Netflix, Amazon, and Disney. The shift in consumer behavior towards convenient, personalized viewing habits further fuels this market, making it an attractive landscape for both established media giants and emerging streaming services.

Streaming Spending Market Size (In Million)

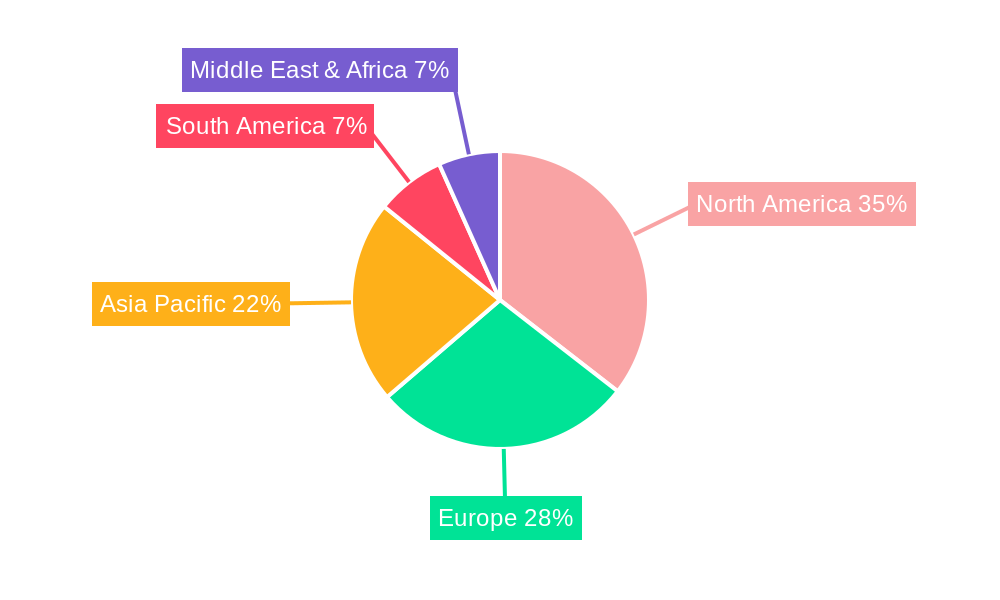

The market is segmented across various applications, with Media, Education, and Sports emerging as dominant forces, alongside a strong presence in Music. The diverse subscription models, including SVOD, TVOD, and AVOD, cater to a broad spectrum of consumer preferences and financial capabilities, ensuring accessibility and continued engagement. While the market is characterized by intense competition among industry leaders such as Apple, AT&T, and Tencent, and the continuous introduction of compelling original content, it also faces challenges. These may include escalating content acquisition costs, the increasing saturation of the market with numerous service providers, and evolving regulatory landscapes. Nevertheless, the overarching trend of digital content consumption and the strategic expansion into new geographical regions, particularly in Asia Pacific and Europe, suggest a highly promising future for the streaming spending sector.

Streaming Spending Company Market Share

Comprehensive Report: Global Streaming Spending Market Analysis (2019-2033)

This in-depth report provides a detailed analysis of the global streaming spending market, covering historical trends, current dynamics, and future projections. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period extending to 2033, this report offers unparalleled insights for industry stakeholders. We meticulously analyze key segments including Media, Education, Sports, and Music, across various SVOD, TVOD, and AVOD models. Leading companies such as Netflix, Amazon, Apple, AT&T, The Walt Disney Company, Tencent, MNC Corporation, Saban Capital Group, Inc., Baidu, and Pacific Century Group are extensively profiled. Dive into actionable insights, market projections, and strategic outlooks crucial for navigating this rapidly evolving digital landscape.

Streaming Spending Market Structure & Competitive Dynamics

The global streaming spending market exhibits a dynamic and increasingly concentrated structure, driven by aggressive expansion and strategic acquisitions by major players. Market concentration is high, with Netflix and Amazon leading in subscriber numbers and revenue, followed closely by Apple TV+ and The Walt Disney Company. Innovation ecosystems are thriving, fueled by significant investments in original content production, advanced recommendation algorithms, and cloud infrastructure. Regulatory frameworks are evolving, with a growing focus on content moderation, data privacy, and anti-monopoly measures in key regions like North America and Europe. Product substitutes, including traditional linear television, physical media, and piracy, continue to exist but their influence is diminishing as user experience and content accessibility improve across streaming platforms. End-user trends indicate a strong preference for personalized content, on-demand access, and multi-device compatibility, driving the adoption of SVOD services. Merger and acquisition (M&A) activities are prevalent, with significant deal values reflecting the consolidation and strategic partnerships aimed at expanding content libraries and subscriber bases. For instance, major content acquisitions and platform integrations are reshaping the competitive landscape.

- Market Share: Netflix holds an estimated 30% global market share, followed by Amazon Prime Video at 20%, and Disney+ at 15% as of the base year 2025.

- M&A Deal Values: Recent significant acquisitions in the media and technology sectors have seen deal values exceeding $10,000 million, signaling intense competition and strategic realignment.

- Innovation Focus: Key areas of innovation include AI-driven content discovery, interactive streaming experiences, and enhanced audio-visual technologies.

- Regulatory Impact: New regulations concerning data usage and content licensing are projected to influence platform strategies and content production budgets.

Streaming Spending Industry Trends & Insights

The global streaming spending market is experiencing robust growth, propelled by a confluence of technological advancements, shifting consumer behaviors, and expanding content offerings. The average annual growth rate (CAGR) is projected to be approximately 12.5% from 2025 to 2033, underscoring the sector's significant expansion potential. Market penetration continues to rise, particularly in emerging economies, as internet infrastructure improves and the affordability of streaming devices increases. A primary growth driver is the increasing demand for high-quality, on-demand entertainment, with consumers actively migrating from traditional linear TV to subscription-based services for greater flexibility and a wider selection of content. The proliferation of original content, including exclusive series, films, and documentaries, has become a critical differentiator, with major players like Netflix, Amazon, and Disney investing billions of dollars annually in production. Technological disruptions, such as the advent of 5G technology and advancements in artificial intelligence for personalized recommendations, are further enhancing the user experience and driving engagement. The competitive landscape is intense, characterized by fierce competition for subscriber acquisition and retention, leading to strategies such as bundling services, offering tiered subscription plans, and exploring new revenue streams like advertising. Consumer preferences are increasingly sophisticated, with a growing emphasis on user interface design, content diversity across genres and languages, and seamless multi-platform accessibility. The integration of social features and interactive elements within streaming platforms is also emerging as a trend to foster community and enhance user engagement. Furthermore, the rise of niche streaming services catering to specific interests, such as anime, documentaries, or educational content, indicates a maturing market catering to diverse audience segments. The ongoing battle for content rights, especially for live sports and major movie releases, continues to shape the market, influencing pricing strategies and partnership models.

- CAGR: Expected to reach 12.5% from 2025 to 2033.

- Market Penetration: Projected to exceed 70% of global internet households by 2033.

- Content Investment: Annual global investment in original streaming content is estimated to reach over $150,000 million by 2028.

- Technological Adoption: AI-powered personalization is a key factor in improving user retention rates, contributing to an estimated 5% increase in subscription longevity.

- Consumer Behavior: A significant shift towards ad-supported tiers (AVOD) is observed, with an estimated 25% of new subscribers opting for these more affordable options.

Dominant Markets & Segments in Streaming Spending

The global streaming spending market is characterized by its expansive reach across various regions and segments, with North America currently holding the dominant position, driven by high disposable incomes and advanced digital infrastructure. Within the application segments, Media continues to be the largest and most influential, encompassing entertainment, news, and general video content. This dominance is further amplified by the overwhelming popularity of the SVOD (Subscription-based Video on Demand) model, which offers unparalleled convenience and access to vast content libraries. Key drivers for this dominance include strong economic policies that foster digital innovation, extensive broadband penetration, and a deeply ingrained consumer culture that embraces on-demand entertainment. The United States, in particular, represents a colossal market for streaming services, boasting the highest subscriber numbers and revenue generation.

- Leading Region: North America, projected to maintain its dominance through 2033 due to sustained economic growth and high adoption rates.

- Dominant Application: Media (encompassing entertainment, news, and general video content), expected to account for over 80% of total streaming spending.

- Dominant Type: SVOD (Subscription-based Video on Demand), driven by its subscription revenue model and extensive content libraries.

- Key Drivers for Media Dominance:

- High Disposable Income: Consumers in leading regions have the financial capacity to subscribe to multiple services.

- Robust Internet Infrastructure: Widespread availability of high-speed internet supports seamless streaming experiences.

- Content Production Hubs: Proximity to major film and television production centers fuels a continuous supply of desirable content.

- Digital Savvy Population: A large segment of the population is comfortable with and actively seeks out digital entertainment solutions.

Beyond North America, Europe presents a significant and growing market, with countries like the UK, Germany, and France showing strong adoption rates. Asia-Pacific is emerging as a critical growth frontier, propelled by countries like China and India, where increasing internet access and a burgeoning middle class are fueling demand for streaming services. While Media remains the largest application, the Sports segment is experiencing accelerated growth, driven by exclusive broadcast rights and the increasing demand for live event streaming. This growth is further bolstered by advancements in AVOD (Advertisement-based Video on Demand), offering a more accessible entry point for sports enthusiasts. The Education segment is also witnessing a steady rise, particularly with the integration of online learning platforms and specialized educational content, further diversified by SVOD and TVOD models. Music streaming, though a mature market, continues to expand, with evolving subscription models and the integration of artist-exclusive content. The interplay between these application segments and the different service types (SVOD, TVOD, AVOD) creates a complex yet opportunity-rich landscape. For instance, the bundling of various application types within a single subscription, such as a media package with a sports add-on, is a growing trend that enhances user value and platform stickiness. The future trajectory of these segments will be heavily influenced by regional economic policies, technological advancements in content delivery, and evolving consumer preferences for content consumption.

- Emerging Markets: Asia-Pacific is projected to exhibit the highest growth rate, with an estimated CAGR of 15% for the forecast period.

- Sports Streaming Growth: Expected to grow at a CAGR of 13% driven by exclusive rights and live event demand.

- Education Technology Integration: The convergence of education and streaming is anticipated to grow by 10% annually.

- AVOD Adoption in Sports: Increasing adoption of ad-supported tiers for sports content, making it more accessible to a wider audience.

Streaming Spending Product Innovations

Product innovations in the streaming spending market are focused on enhancing user experience, diversifying content delivery, and optimizing monetization strategies. Companies are investing heavily in AI-powered recommendation engines that offer hyper-personalized content suggestions, significantly improving user engagement and retention. Advancements in video and audio streaming technologies, including 4K HDR, Dolby Atmos, and immersive VR experiences, are creating more compelling viewing and listening environments. The integration of interactive features, such as shoppable content and live polling, is blurring the lines between passive consumption and active participation. Furthermore, the development of tiered subscription models, including ad-supported options and premium ad-free tiers, caters to a wider range of consumer budgets and preferences. These innovations aim to capture a larger market share by offering superior value and convenience, thereby solidifying competitive advantages in a crowded marketplace.

Report Segmentation & Scope

This report meticulously segments the global streaming spending market across key application and type categories. The Media segment, encompassing entertainment and general video content, is projected to witness substantial growth due to continued demand for on-demand viewing. Within Media, SVOD is expected to retain its leading position, driven by extensive content libraries and subscription models. The Education segment is poised for significant expansion as e-learning and specialized educational content gain traction, with both SVOD and TVOD models playing crucial roles. The Sports segment is a high-growth area, fueled by the acquisition of exclusive broadcast rights and the increasing popularity of live streaming, with AVOD and SVOD models being key enablers. The Music segment, while more mature, continues to evolve with new subscription tiers and exclusive artist content, primarily utilizing SVOD models. Projections indicate a combined market size exceeding $500,000 million by 2033, with SVOD holding the largest share, followed by AVOD and then TVOD.

- Media (SVOD): Projected market size of $250,000 million by 2033, with a CAGR of 11%.

- Education (SVOD/TVOD): Estimated market size of $75,000 million by 2033, with a CAGR of 13%.

- Sports (AVOD/SVOD): Expected market size of $150,000 million by 2033, with a CAGR of 14%.

- Music (SVOD): Projected market size of $60,000 million by 2033, with a CAGR of 9%.

Key Drivers of Streaming Spending Growth

The exponential growth in streaming spending is propelled by a potent combination of factors. Technological advancements, particularly the widespread availability of high-speed internet and the proliferation of smart devices, have democratized access to digital content. Economic factors, including rising disposable incomes and the increasing affordability of subscription services, have further fueled consumer adoption. Regulatory supportive frameworks in many regions have encouraged investment and innovation within the digital media landscape. For instance, the increasing adoption of 5G networks enables seamless streaming of high-definition content, reducing buffering and improving user experience. The widespread availability of mobile devices and smart TVs has made streaming accessible in virtually any location. Furthermore, the competitive pricing strategies of streaming providers, including tiered subscription plans and promotional offers, have made these services more attractive to a broader consumer base.

- Technological Enablers: Widespread broadband penetration and 5G deployment.

- Economic Factors: Growing disposable incomes and affordable subscription models.

- Consumer Behavior: Shift towards on-demand content and preference for personalization.

- Content Investment: Massive investment in original and exclusive content by key players.

Challenges in the Streaming Spending Sector

Despite robust growth, the streaming spending sector faces several significant challenges that could impede future expansion. Intense competition among numerous players leads to subscriber fatigue and increased churn rates, as consumers may find it overwhelming to manage multiple subscriptions. The high cost of content acquisition and production, especially for premium original series and live sports rights, puts immense pressure on profitability and necessitates continuous revenue generation strategies. Regulatory hurdles, including data privacy laws, content moderation policies, and potential antitrust actions, can impact operational flexibility and business models. Supply chain issues, particularly related to the availability of skilled content creators and advanced streaming infrastructure, can also pose a bottleneck. The ever-present threat of piracy continues to erode potential revenue. For example, the increasing cost of acquiring exclusive sports rights has driven up subscription prices, leading to concerns about affordability for some consumer segments.

- Subscriber Churn: High competition leading to increased customer attrition.

- Content Costs: Escalating expenses for original productions and exclusive rights.

- Regulatory Scrutiny: Evolving data privacy and content governance laws.

- Piracy: Ongoing threat to revenue streams.

- Market Saturation: Growing number of services leading to consumer choice fatigue.

Leading Players in the Streaming Spending Market

- Netflix

- Amazon

- Apple

- AT&T

- The Walt Disney Company

- Tencent

- MNC Corporation

- Saban Capital Group, Inc.

- Baidu

- Pacific Century Group

Key Developments in Streaming Spending Sector

- 2023 Q1: Netflix launches its ad-supported tier, expanding AVOD offerings and targeting a wider audience with an estimated 10% revenue increase from this segment.

- 2023 Q2: Amazon invests $10,000 million in exclusive NFL broadcast rights, bolstering its sports streaming portfolio and attracting new subscribers.

- 2023 Q3: Apple TV+ announces a slate of new original films and series, signaling continued investment in high-quality content production.

- 2023 Q4: The Walt Disney Company completes the integration of Hulu into its streaming strategy, aiming for a more consolidated consumer offering.

- 2024 Q1: Tencent secures significant streaming rights for popular esports tournaments in Asia, demonstrating its growing dominance in the region's gaming and entertainment sector.

- 2024 Q2: AT&T continues to streamline its media assets, focusing on core connectivity services while exploring strategic partnerships in the streaming space.

- 2024 Q3: Saban Capital Group, Inc. announces a strategic investment in a new streaming technology startup, aiming to foster innovation in interactive content delivery.

- 2024 Q4: Baidu expands its iQIYI platform with new educational content offerings, tapping into the growing demand for online learning in China.

- 2025 Q1: MNC Corporation announces ambitious expansion plans into new international markets, targeting a 15% subscriber growth by the end of the year.

- 2025 Q2: Pacific Century Group explores potential acquisitions of niche streaming services to diversify its content portfolio and reach specialized audiences.

Strategic Streaming Spending Market Outlook

The strategic outlook for the streaming spending market is overwhelmingly positive, characterized by sustained growth and evolving consumer engagement. The continued expansion of high-speed internet infrastructure globally, coupled with the increasing penetration of smart devices, will serve as significant growth accelerators. Key players are expected to focus on diversifying revenue streams beyond traditional subscriptions, including robust advertising models and the integration of e-commerce. Strategic partnerships and acquisitions will remain crucial for consolidating market share, acquiring exclusive content, and expanding into new geographical territories. The development of interactive and immersive streaming experiences, leveraging technologies like AI and VR, presents substantial opportunities for enhancing user engagement and creating unique value propositions. The increasing demand for localized and diverse content will drive further investment in regional productions, opening up new markets and catering to a wider array of consumer preferences, ultimately shaping a more dynamic and personalized streaming future.

- Growth Accelerators: Ubiquitous high-speed internet, smart device adoption, and diversified revenue models.

- Strategic Focus: Content diversification, international expansion, and technological innovation.

- Future Opportunities: Interactive streaming, personalized content delivery, and strategic M&A.

- Market Potential: Expected to exceed $800,000 million in global revenue by 2033.

Streaming Spending Segmentation

-

1. Application

- 1.1. Media

- 1.2. Education

- 1.3. Sports

- 1.4. Music

-

2. Type

- 2.1. SVOD (Subscription-based Video on Demand)

- 2.2. TVOD (Transactional-based Video on Demand)

- 2.3. AVOD (Advertisement-based Video on Demand)

Streaming Spending Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Streaming Spending Regional Market Share

Geographic Coverage of Streaming Spending

Streaming Spending REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Media

- 5.1.2. Education

- 5.1.3. Sports

- 5.1.4. Music

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. SVOD (Subscription-based Video on Demand)

- 5.2.2. TVOD (Transactional-based Video on Demand)

- 5.2.3. AVOD (Advertisement-based Video on Demand)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Streaming Spending Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Media

- 6.1.2. Education

- 6.1.3. Sports

- 6.1.4. Music

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. SVOD (Subscription-based Video on Demand)

- 6.2.2. TVOD (Transactional-based Video on Demand)

- 6.2.3. AVOD (Advertisement-based Video on Demand)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Streaming Spending Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Media

- 7.1.2. Education

- 7.1.3. Sports

- 7.1.4. Music

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. SVOD (Subscription-based Video on Demand)

- 7.2.2. TVOD (Transactional-based Video on Demand)

- 7.2.3. AVOD (Advertisement-based Video on Demand)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Streaming Spending Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Media

- 8.1.2. Education

- 8.1.3. Sports

- 8.1.4. Music

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. SVOD (Subscription-based Video on Demand)

- 8.2.2. TVOD (Transactional-based Video on Demand)

- 8.2.3. AVOD (Advertisement-based Video on Demand)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Streaming Spending Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Media

- 9.1.2. Education

- 9.1.3. Sports

- 9.1.4. Music

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. SVOD (Subscription-based Video on Demand)

- 9.2.2. TVOD (Transactional-based Video on Demand)

- 9.2.3. AVOD (Advertisement-based Video on Demand)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Streaming Spending Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Media

- 10.1.2. Education

- 10.1.3. Sports

- 10.1.4. Music

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. SVOD (Subscription-based Video on Demand)

- 10.2.2. TVOD (Transactional-based Video on Demand)

- 10.2.3. AVOD (Advertisement-based Video on Demand)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Streaming Spending Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Media

- 11.1.2. Education

- 11.1.3. Sports

- 11.1.4. Music

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. SVOD (Subscription-based Video on Demand)

- 11.2.2. TVOD (Transactional-based Video on Demand)

- 11.2.3. AVOD (Advertisement-based Video on Demand)

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Netflix

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amazon

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Apple

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AT&T

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 The Walt Disney Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Tecent

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 MNC Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Saban Capital Group,Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Baidu

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pacific Century Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Netflix

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Streaming Spending Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Streaming Spending Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Streaming Spending Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Streaming Spending Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Streaming Spending Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Streaming Spending Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Streaming Spending Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Streaming Spending Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Streaming Spending Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Streaming Spending Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Streaming Spending Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Streaming Spending Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Streaming Spending Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Streaming Spending Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Streaming Spending Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Streaming Spending Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Streaming Spending Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Streaming Spending Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Streaming Spending Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Streaming Spending Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Streaming Spending Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Streaming Spending Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Streaming Spending Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Streaming Spending Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Streaming Spending Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Streaming Spending Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Streaming Spending Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Streaming Spending Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Streaming Spending Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Streaming Spending Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Streaming Spending Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Streaming Spending Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Streaming Spending Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Streaming Spending Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Streaming Spending Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Streaming Spending Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Streaming Spending Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Streaming Spending Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Streaming Spending Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Streaming Spending Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Streaming Spending Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Streaming Spending Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Streaming Spending Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Streaming Spending Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Streaming Spending Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Streaming Spending Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Streaming Spending Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Streaming Spending Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Streaming Spending Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Streaming Spending Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Streaming Spending?

The projected CAGR is approximately 10.7%.

2. Which companies are prominent players in the Streaming Spending?

Key companies in the market include Netflix, Amazon, Apple, AT&T, The Walt Disney Company, Tecent, MNC Corporation, Saban Capital Group,Inc., Baidu, Pacific Century Group.

3. What are the main segments of the Streaming Spending?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Streaming Spending," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Streaming Spending report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Streaming Spending?

To stay informed about further developments, trends, and reports in the Streaming Spending, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence