Key Insights

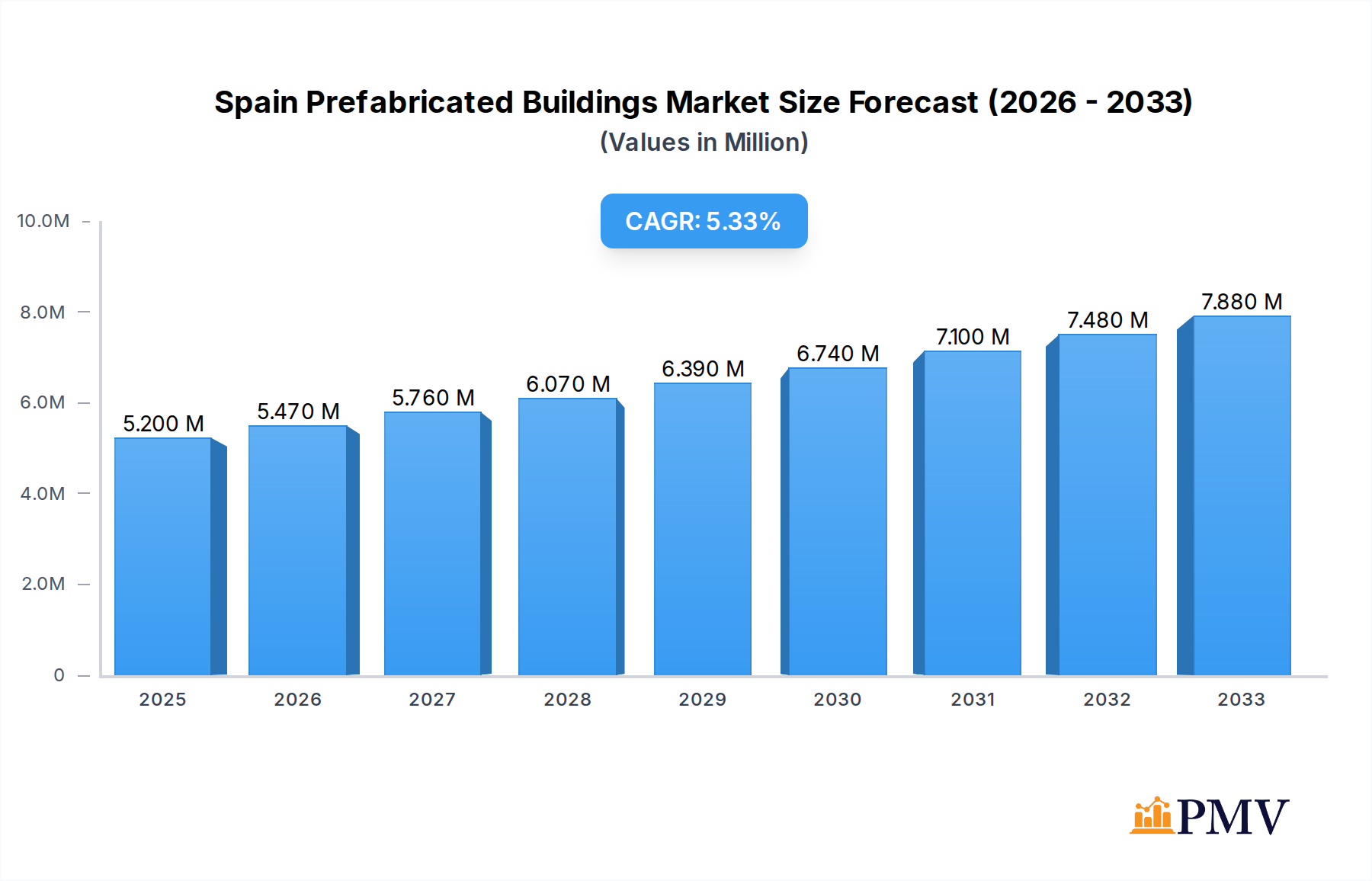

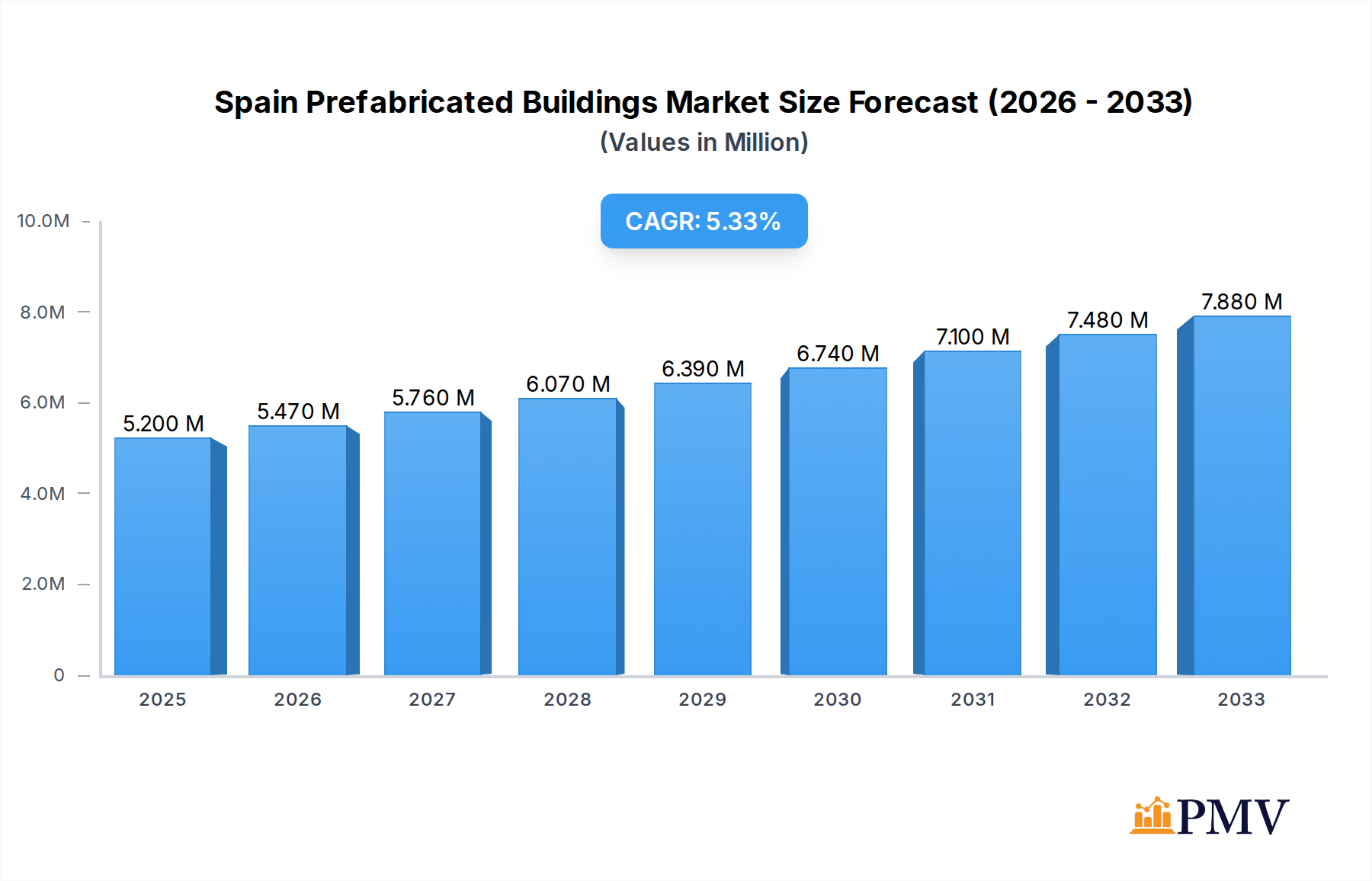

The Spanish prefabricated buildings market is poised for robust growth, driven by increasing demand for efficient, sustainable, and cost-effective construction solutions. With a market size of approximately €5.20 million in 2025, the sector is projected to expand at a Compound Annual Growth Rate (CAGR) of 5.28% during the forecast period of 2025-2033. This sustained growth is fueled by government initiatives promoting affordable housing, the growing adoption of green building practices, and the inherent advantages of prefabrication, such as reduced construction time and enhanced quality control. The market is experiencing a significant shift towards modular construction, with both residential and commercial sectors actively embracing these innovative building methods. Material innovation, particularly in concrete and timber, is further enhancing the appeal and versatility of prefabricated structures. Key drivers include the need for faster project completion, a skilled labor shortage in traditional construction, and an increasing awareness of the environmental benefits associated with factory-built components.

Spain Prefabricated Buildings Market Market Size (In Million)

The competitive landscape in Spain is characterized by a mix of established modular construction providers and new entrants, all vying for market share through product innovation and strategic partnerships. Companies are increasingly focusing on offering customizable solutions to cater to diverse client needs. While the market presents considerable opportunities, certain restraints, such as initial perception challenges and the need for standardized regulations across different regions, need to be addressed for even more accelerated growth. However, the overarching trend points towards a significant expansion in the application of prefabricated buildings across various segments, including residential developments, commercial spaces, and other specialized structures. The value unit for this market is in millions of Euros. The market's trajectory suggests a transformative phase, where prefabricated construction is set to play a pivotal role in shaping Spain's future built environment.

Spain Prefabricated Buildings Market Company Market Share

This in-depth report provides a detailed analysis of the Spain prefabricated buildings market, encompassing market size, growth drivers, trends, competitive landscape, and future outlook. Leveraging advanced analytical methodologies, this study offers actionable insights for stakeholders seeking to capitalize on the burgeoning opportunities within the Spanish modular construction sector. The report covers the historical period from 2019 to 2024, with a base year of 2025 and a comprehensive forecast period extending to 2033.

Spain Prefabricated Buildings Market Market Structure & Competitive Dynamics

The Spain prefabricated buildings market is characterized by a moderately concentrated structure, with a mix of established large-scale manufacturers and agile niche players. Innovation is a key differentiator, driven by advancements in sustainable building materials, energy efficiency, and smart building technologies. The regulatory framework in Spain, while evolving, generally supports off-site construction through initiatives promoting speed, cost-effectiveness, and quality. Product substitutes, such as traditional on-site construction, continue to exist, but the inherent advantages of modular construction – reduced timelines, predictable costs, and minimal site disruption – are increasingly gaining traction. End-user preferences are shifting towards faster project completion, environmentally conscious building solutions, and flexible, adaptable spaces. Mergers and acquisitions (M&A) activities are expected to play a role in consolidating the market, with potential deal values ranging from XX Million to XX Million as companies seek to expand their capabilities and market reach. Key players are actively investing in R&D to enhance their product offerings and gain a competitive edge.

- Market Concentration: Moderate, with leading players holding significant, but not dominant, market share.

- Innovation Ecosystem: Driven by advancements in materials science, digital design (BIM), and off-site manufacturing processes.

- Regulatory Framework: Supportive of sustainable and efficient building practices, with ongoing efforts to streamline permitting for modular projects.

- Product Substitutes: Traditional on-site construction, though facing increasing competition from prefab solutions.

- End-User Trends: Demand for speed, sustainability, cost predictability, and flexible designs.

- M&A Activities: Expected to increase as companies seek scale and diversification.

Spain Prefabricated Buildings Market Industry Trends & Insights

The Spain prefabricated buildings market is experiencing robust growth, fueled by a confluence of macroeconomic factors and evolving industry dynamics. A significant Compound Annual Growth Rate (CAGR) of XX% is projected over the forecast period. This expansion is primarily driven by the increasing demand for rapid housing solutions, driven by population growth and urbanization, particularly in key Spanish cities. The government's focus on affordable housing initiatives and infrastructure development further bolsters the adoption of modular construction, which offers cost-effectiveness and faster deployment compared to conventional building methods. Technological advancements in manufacturing, including the integration of robotics and automation in off-site building solutions, are enhancing precision, reducing waste, and improving the overall quality of prefabricated units.

Furthermore, a growing awareness of environmental sustainability is a significant trend. Prefabricated buildings, with their controlled manufacturing environments, typically generate less waste and have a smaller carbon footprint. This aligns with Spain's commitment to green building practices and the EU's sustainability goals. The appeal of energy-efficient modular homes and commercial spaces is also on the rise, as consumers and businesses seek to reduce operational costs and environmental impact. The increasing adoption of BIM (Building Information Modeling) in the design and manufacturing phases allows for greater accuracy, better project management, and enhanced collaboration, contributing to the overall efficiency and appeal of prefabricated solutions.

Consumer preferences are evolving towards more customizable and aesthetically pleasing prefabricated options. Manufacturers are responding by offering a wider range of design choices, finishes, and smart home integration, blurring the lines between modular and traditional bespoke construction. The market penetration of prefabricated buildings in Spain is steadily increasing, driven by successful project implementations in both the residential and commercial sectors, including schools, hospitals, and temporary event structures. The sector is also witnessing greater investment in research and development, focusing on innovative materials like cross-laminated timber (CLT) and advanced insulation techniques to further enhance performance and sustainability. The competitive landscape is intensifying, with both domestic and international players vying for market share, leading to greater innovation and competitive pricing.

Dominant Markets & Segments in Spain Prefabricated Buildings Market

The Spain prefabricated buildings market exhibits distinct dominance across various geographical regions and application segments. Within Spain, the residential sector currently holds the largest market share, driven by a persistent demand for housing solutions, particularly in urban and peri-urban areas experiencing population influx. The economic policies promoting affordable housing and the rising preference for faster home construction are key drivers of this dominance.

- Leading Application Segment: Residential.

- Key Drivers: Affordable housing initiatives, rapid urbanization, preference for faster construction timelines, increasing nuclear families.

- Dominance Analysis: The residential segment benefits from government incentives, a large potential buyer base, and the inherent speed of modular construction that addresses the acute need for new homes. The market size for residential prefabricated buildings is estimated to be XX Million in the base year 2025.

The commercial sector is a rapidly growing segment, encompassing applications such as offices, retail spaces, and hospitality facilities. The inherent flexibility, speed of deployment, and cost-effectiveness of prefabricated buildings make them an attractive option for businesses looking to expand or establish new premises quickly. Infrastructure development projects, including the construction of schools, healthcare facilities, and temporary event venues, also contribute significantly to the commercial segment's growth.

- Emerging Application Segment: Commercial.

- Key Drivers: Need for flexible office spaces, rapid retail expansion, demand for modular healthcare and educational facilities, temporary structures for events.

- Dominance Analysis: The commercial segment's growth is propelled by its adaptability to various business needs, enabling quick setup and scalability. The projected market size for commercial prefabricated buildings in 2025 is XX Million.

From a material perspective, concrete prefabricated buildings have historically dominated due to their durability, structural integrity, and familiarity within the construction industry. However, there is a significant and growing trend towards timber prefabricated buildings, particularly those utilizing cross-laminated timber (CLT), due to their superior sustainability credentials, lighter weight, and faster installation times.

Dominant Material Type: Concrete.

- Key Drivers: Established industry practices, high durability and fire resistance, availability of skilled labor, cost-effectiveness for large-scale projects.

- Dominance Analysis: Concrete's established presence in traditional construction translates into its current dominance in the prefabricated market. The market size for concrete prefabricated buildings in 2025 is estimated at XX Million.

Fastest Growing Material Type: Timber.

- Key Drivers: Environmental sustainability, lighter weight, faster installation, aesthetic appeal, carbon sequestration properties.

- Dominance Analysis: Timber's rise is directly linked to increasing environmental regulations and consumer demand for green building solutions. The market size for timber prefabricated buildings in 2025 is projected to be XX Million.

Metal prefabricated buildings are also gaining traction, especially for industrial applications, temporary structures, and modular extensions, owing to their strength, durability, and ease of assembly. Glass prefabricated buildings are increasingly being used in contemporary architectural designs for commercial and residential purposes, offering aesthetic appeal and natural light.

Spain Prefabricated Buildings Market Product Innovations

Product innovation in the Spain prefabricated buildings market is primarily focused on enhancing sustainability, energy efficiency, and smart technology integration. Advancements include the development of advanced insulation materials, energy-generating components like solar panels, and smart home systems for automated climate control and security. Manufacturers are also innovating in design flexibility, offering a wider range of modular configurations and finishes to meet diverse aesthetic preferences. The use of high-performance, eco-friendly materials such as cross-laminated timber (CLT) and recycled steel is on the rise. These innovations aim to reduce the environmental impact, lower operational costs for end-users, and improve the overall living and working experience within prefabricated structures, giving manufacturers a significant competitive advantage.

Report Segmentation & Scope

This report segments the Spain prefabricated buildings market across key dimensions to provide a granular view of market dynamics. The segmentation includes:

- Material Type: This segment analyzes the market share and growth prospects for Concrete, Glass, Metal, Timber, and Other Material Types. The concrete segment is projected to hold a substantial market share in 2025, estimated at XX Million, while the timber segment is expected to exhibit the highest growth rate.

- Application: The market is segmented into Residential, Commercial, and Other Applications. The residential sector is anticipated to be the largest segment in 2025, with a market size of XX Million, driven by housing demand. The commercial segment is expected to witness robust growth, reaching an estimated XX Million by 2025.

Each segment is analyzed for its market size, growth projections, and competitive dynamics, offering a comprehensive understanding of where opportunities lie.

Key Drivers of Spain Prefabricated Buildings Market Growth

The Spain prefabricated buildings market is propelled by several interconnected drivers. Technological advancements in manufacturing, including automation and digital design (BIM), are increasing efficiency and quality. Economic factors, such as government initiatives for affordable housing and infrastructure development, create significant demand. Regulatory support for sustainable and fast-track construction methods further encourages adoption. The growing demand for energy-efficient and eco-friendly building solutions is a crucial driver, aligning with global sustainability targets. Furthermore, the inherent benefits of reduced construction time and predictable costs are highly attractive to both developers and end-users, especially in a competitive real estate market.

Challenges in the Spain Prefabricated Buildings Market Sector

Despite its growth potential, the Spain prefabricated buildings market faces certain challenges. Regulatory hurdles and complex permitting processes in some regions can slow down project timelines. Perception issues and lingering doubts about the quality and durability of prefabricated structures compared to traditional buildings can hinder wider adoption. Supply chain disruptions and the availability of specialized raw materials can impact production schedules and costs. Limited skilled labor for advanced off-site manufacturing techniques also presents a challenge. Furthermore, initial capital investment for setting up state-of-the-art manufacturing facilities can be substantial, acting as a barrier for smaller players.

Leading Players in the Spain Prefabricated Buildings Market Market

- Europa Prefabri

- Cualimetal

- Atlantida Homes

- Compacthabit

- Pacadar Group

- Mader House

- ABC Modular

- Prefabri Steel

- Casas Mundiales

- Turboconstroi

- Armodul

Key Developments in Spain Prefabricated Buildings Market Sector

- November 2023: Algeco, the world’s largest modular and off-site building solutions brand in Europe, secured a large order for new, state-of-the-art GRIDSERVE Electrical Forecourts®. The latest generation of Algeco modular buildings are helping to meet the increasing demand for GrisEnergy Electric Forecourts®, across the nation.

- September 2023: ADRA in Spain, with the help of donors and partners within ADRA's global network, funded the construction of 8 prefabricated shelters in a village in the Atlas Mountains near the epicenter of the earthquake in Morocco. The project consists of 8 modular houses, each 16 square meters (172 square feet) long, providing families with temporary, safe, and high-quality shelter. Each module features 4 bedrooms, a latrine, a shower, and a communal kitchen, with an outdoor area for children.

Strategic Spain Prefabricated Buildings Market Market Outlook

The strategic outlook for the Spain prefabricated buildings market is exceptionally positive, driven by ongoing urbanization, increasing demand for sustainable construction, and supportive government policies. Future market potential lies in the continued innovation of energy-efficient and smart modular solutions, catering to the growing environmental consciousness. Strategic opportunities include expanding into underserved regions within Spain, developing niche market applications such as modular student housing and senior living facilities, and fostering stronger collaborations between manufacturers, designers, and regulatory bodies to streamline project approvals. The emphasis on circular economy principles and the use of recycled materials will also be a key growth accelerator. Investment in R&D for advanced modular technologies and a focus on customer-centric design will be paramount for sustained growth and market leadership.

Spain Prefabricated Buildings Market Segmentation

-

1. Material Type

- 1.1. Concrete

- 1.2. Glass

- 1.3. Metal

- 1.4. Timber

- 1.5. Other Material Types

-

2. Application

- 2.1. Residential

- 2.2. Commercial

- 2.3. Other Ap

Spain Prefabricated Buildings Market Segmentation By Geography

- 1. Spain

Spain Prefabricated Buildings Market Regional Market Share

Geographic Coverage of Spain Prefabricated Buildings Market

Spain Prefabricated Buildings Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Concrete

- 5.1.2. Glass

- 5.1.3. Metal

- 5.1.4. Timber

- 5.1.5. Other Material Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Other Ap

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Spain Prefabricated Buildings Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Concrete

- 6.1.2. Glass

- 6.1.3. Metal

- 6.1.4. Timber

- 6.1.5. Other Material Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential

- 6.2.2. Commercial

- 6.2.3. Other Ap

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Europa Prefabri

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Cualimetal

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Atlantida Homes

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Compacthabit

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Pacadar Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mader House

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ABC Modular

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Prefabri Steel **List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Casas Mundiales

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Turboconstroi

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Armodul

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Europa Prefabri

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Prefabricated Buildings Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Spain Prefabricated Buildings Market Share (%) by Company 2025

List of Tables

- Table 1: Spain Prefabricated Buildings Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Spain Prefabricated Buildings Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Spain Prefabricated Buildings Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Spain Prefabricated Buildings Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 5: Spain Prefabricated Buildings Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Spain Prefabricated Buildings Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Prefabricated Buildings Market?

The projected CAGR is approximately 5.28%.

2. Which companies are prominent players in the Spain Prefabricated Buildings Market?

Key companies in the market include Europa Prefabri, Cualimetal, Atlantida Homes, Compacthabit, Pacadar Group, Mader House, ABC Modular, Prefabri Steel **List Not Exhaustive, Casas Mundiales, Turboconstroi, Armodul.

3. What are the main segments of the Spain Prefabricated Buildings Market?

The market segments include Material Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.20 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in residential construction driving the market; Development of hospitality infrastructure driving the market.

6. What are the notable trends driving market growth?

Increase in investment among infrastructural sector.

7. Are there any restraints impacting market growth?

Limited access to financing; Shortage of skilled labor.

8. Can you provide examples of recent developments in the market?

November 2023: Algeco, the world’s largest modular and off-site building solutions brand in Europe, has secured a large order for new, state-of-the-art GRIDSERVE Electrical Forecourts® The latest generation of Algeco modular buildings are helping to meet the increasing demand for GrisEnergy Electric Forecourts®, across the nation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Prefabricated Buildings Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Prefabricated Buildings Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Prefabricated Buildings Market?

To stay informed about further developments, trends, and reports in the Spain Prefabricated Buildings Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence