Key Insights

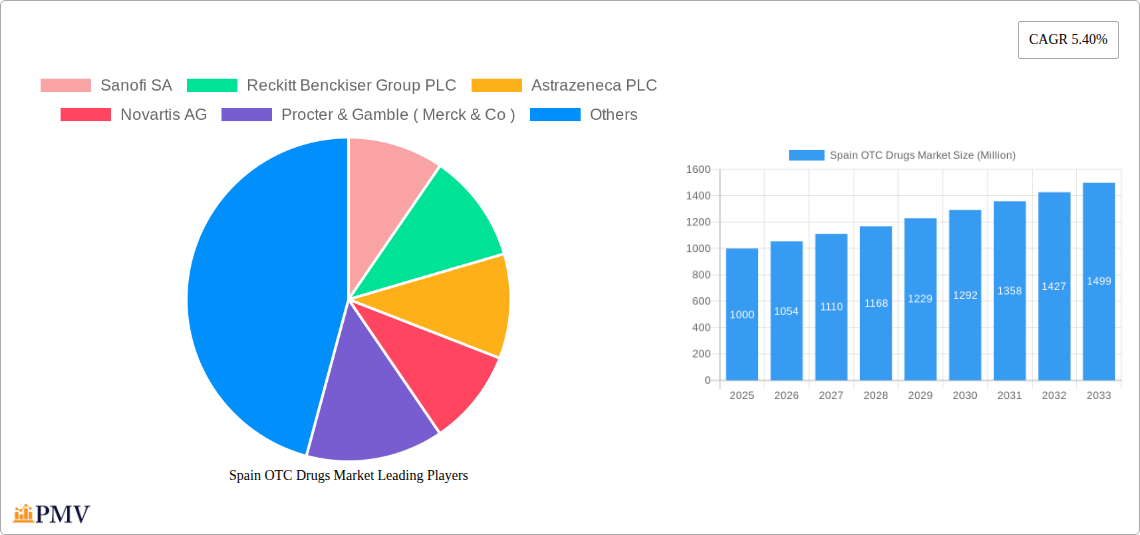

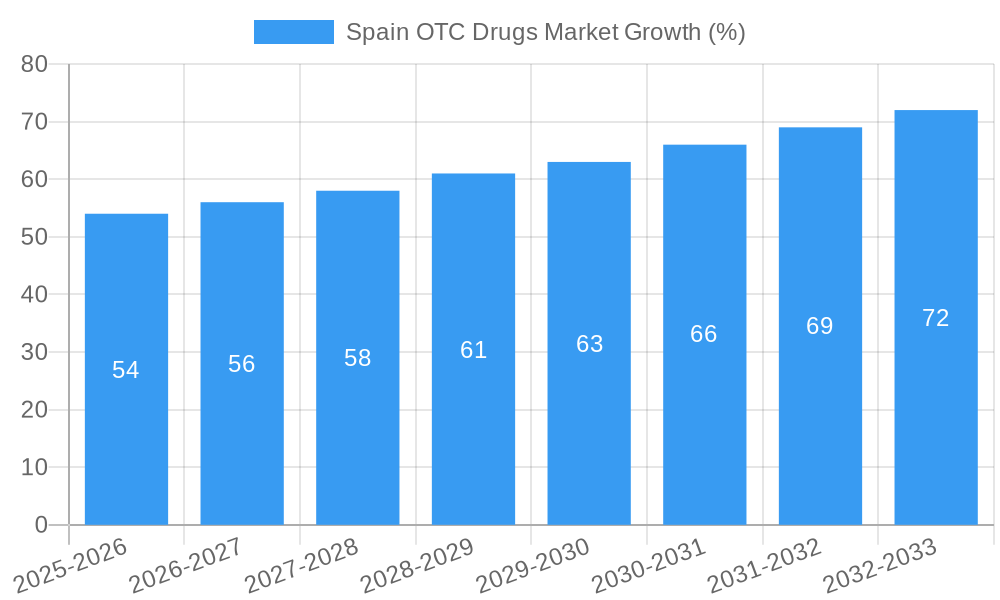

The Spain OTC Drugs Market, valued at approximately €[Estimate based on market size XX and value unit Million. For example, if XX = 1000, then the value is €1000 Million in 2025], exhibits robust growth potential, projected to expand at a compound annual growth rate (CAGR) of 5.40% from 2025 to 2033. This growth is fueled by several key drivers. Increasing prevalence of chronic conditions like allergies and gastrointestinal issues necessitates greater self-medication, boosting demand for OTC products. Furthermore, a rising elderly population and increased healthcare awareness among consumers contribute significantly to market expansion. The convenience of online pharmacies and broader retail availability further enhance market accessibility. Segment-wise, Cough, Cold, and Flu products, Analgesics, and Gastrointestinal products are major revenue generators, reflecting prevalent health concerns within the Spanish population. However, regulatory scrutiny and pricing pressures pose potential restraints on market growth. Competition among established pharmaceutical giants like Sanofi, Reckitt Benckiser, and Pfizer, alongside the emergence of smaller players, creates a dynamic and competitive landscape.

Looking ahead, several trends are shaping the future of the Spain OTC drugs market. The increasing adoption of digital health solutions, including telehealth and e-commerce, is creating new avenues for distribution and consumer engagement. Growing consumer preference for natural and herbal remedies presents opportunities for innovative product development and marketing strategies. The market is also witnessing a surge in personalized medicine approaches, with tailored OTC products catering to specific individual needs becoming increasingly prevalent. Companies are investing heavily in research and development to introduce novel formulations and delivery systems, enhancing efficacy and improving patient compliance. The market's future success will depend on adapting to these trends, navigating regulatory hurdles, and successfully marketing products to a health-conscious and increasingly digitally connected consumer base.

Spain OTC Drugs Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Spain OTC drugs market, offering valuable insights for industry stakeholders, investors, and market researchers. Spanning the period from 2019 to 2033, with 2025 as the base year and a forecast period from 2025 to 2033, this report unveils the market's structure, competitive dynamics, growth drivers, and future outlook. The market is segmented by product type (Cough, Cold, and Flu Products; Analgesics; Dermatology Products; Gastrointestinal Products; Vitamin, Mineral, and Supplement (VMS) Products; Weight-loss/Dietary Products; Ophthalmic Products; Sleeping Aids; Other Product Types) and distribution channel (Retail Pharmacies; Online Pharmacies; Other Distribution Channels). Key players such as Sanofi SA, Reckitt Benckiser Group PLC, AstraZeneca PLC, and others are analyzed for their market share and strategic initiatives. The report's projected market value in 2025 is estimated at XX Million.

Spain OTC Drugs Market Market Structure & Competitive Dynamics

The Spain OTC drugs market exhibits a moderately concentrated structure, with several multinational pharmaceutical companies holding significant market share. The market is characterized by a dynamic innovation ecosystem, driven by the continuous development of new formulations and delivery systems. Regulatory frameworks, primarily overseen by the Spanish Agency of Medicines and Medical Devices (AEMPS), play a crucial role in shaping market dynamics. The presence of generic and over-the-counter (OTC) substitutes significantly impacts pricing and competition. End-user trends, such as increasing self-medication practices and health consciousness, are fueling market growth. M&A activities have been relatively moderate in recent years, with deal values totaling approximately XX Million in the historical period (2019-2024).

- Market Concentration: The top 5 players hold approximately XX% of the market share in 2025.

- Innovation: Focus on developing targeted therapies, improved formulations, and convenient delivery systems.

- Regulatory Landscape: Stringent regulations governing product registration and advertising.

- Substitutes: Generic drugs and home remedies pose competitive challenges.

- End-User Trends: Rising demand for convenient, effective, and natural OTC remedies.

- M&A Activity: Consolidation expected to continue, driven by the desire to expand product portfolios and market reach.

Spain OTC Drugs Market Industry Trends & Insights

The Spain OTC drugs market is projected to experience a CAGR of XX% during the forecast period (2025-2033). Key growth drivers include increasing prevalence of chronic diseases, rising healthcare expenditure, and a growing elderly population. Technological disruptions, such as the increasing use of digital health platforms and telemedicine, are transforming market access and consumer behavior. Consumer preferences are shifting towards natural and herbal remedies, alongside personalized healthcare solutions. Intense competition necessitates continuous innovation and strategic partnerships to maintain market share. Market penetration of online pharmacies is steadily increasing, particularly among younger demographics.

Dominant Markets & Segments in Spain OTC Drugs Market

Within the Spain OTC drugs market, Analgesics and Cough, Cold, and Flu Products represent the dominant segments, driven by high prevalence of associated ailments. Retail pharmacies constitute the primary distribution channel, although online pharmacies are witnessing significant growth. The Madrid and Catalonia regions are leading the market due to higher population density and greater healthcare expenditure.

- Leading Segments:

- Analgesics: High prevalence of musculoskeletal disorders and headaches.

- Cough, Cold, and Flu Products: Seasonal fluctuations in demand, influenced by weather patterns.

- Dermatology Products: Growing awareness of skin health and increased availability of OTC treatments.

- Key Drivers:

- Economic factors: Increasing disposable income and healthcare expenditure.

- Demographic factors: Aging population and high prevalence of chronic diseases.

- Retail Pharmacy Dominance: Extensive network and trusted relationship with consumers.

- Online Pharmacy Growth: Convenience and accessibility, particularly for younger consumers.

Spain OTC Drugs Market Product Innovations

Recent product innovations in the Spain OTC drugs market emphasize improved formulations, targeted therapies, and convenient delivery systems. Technological advancements, such as nanotechnology and personalized medicine, are shaping the development of new products with enhanced efficacy and safety profiles. Companies are focusing on natural ingredients and herbal remedies to cater to the rising consumer demand for safer alternatives. These innovations aim to improve treatment outcomes and enhance patient compliance.

Report Segmentation & Scope

This report provides a comprehensive segmentation of the Spain OTC drugs market, encompassing various product types and distribution channels. Each segment's growth trajectory, market size, and competitive dynamics are analyzed in detail.

- Product: Cough, Cold, and Flu Products (XX Million), Analgesics (XX Million), Dermatology Products (XX Million), Gastrointestinal Products (XX Million), VMS Products (XX Million), Weight-loss/Dietary Products (XX Million), Ophthalmic Products (XX Million), Sleeping Aids (XX Million), Other Product Types (XX Million).

- Distribution Channel: Retail Pharmacies (XX Million), Online Pharmacies (XX Million), Other Distribution Channels (XX Million).

Key Drivers of Spain OTC Drugs Market Growth

Several factors fuel the expansion of the Spain OTC drugs market. The rising prevalence of chronic diseases, increased healthcare expenditure, and an aging population are key contributors. Technological advancements drive innovation and improve accessibility. Favorable government policies and regulations encourage market expansion.

Challenges in the Spain OTC Drugs Market Sector

The Spanish OTC drugs market faces challenges such as stringent regulatory requirements, price competition from generic drugs, and the increasing demand for more effective and safe treatment options. Supply chain disruptions and fluctuating raw material costs further complicate market dynamics. The evolving healthcare landscape presents both opportunities and hurdles to navigate.

Leading Players in the Spain OTC Drugs Market Market

- Sanofi SA

- Reckitt Benckiser Group PLC

- AstraZeneca PLC

- Novartis AG

- Procter & Gamble ( Merck & Co )

- Leo Pharma AS

- Bristol-Myers Squibb

- Johnson & Johnson

- Cardinal Health

- Takeda Pharmaceutical Company Ltd

- Bayer

- GlaxoSmithKline PLC

- Pfizer Inc

Key Developments in Spain OTC Drugs Market Sector

- January 2023: Launch of a new analgesic formulation by Sanofi SA.

- June 2022: Reckitt Benckiser Group PLC acquired a smaller OTC company, expanding its product portfolio.

- November 2021: New regulations regarding online pharmacy operations implemented by the AEMPS.

Strategic Spain OTC Drugs Market Market Outlook

The Spain OTC drugs market presents significant growth potential driven by several factors including the increasing prevalence of chronic diseases, an aging population, and growing demand for self-care solutions. Strategic partnerships, innovation in product development, and expansion into the digital healthcare space present lucrative opportunities for market players. Companies focusing on personalized medicine and natural ingredients are likely to gain a competitive edge.

Spain OTC Drugs Market Segmentation

-

1. Product

- 1.1. Cough, Cold, and Flu Products

- 1.2. Analgesics

- 1.3. Dermatology Products

- 1.4. Gastrointestinal Products

- 1.5. Vitamin, Mineral, and Supplement (VMS) Products

- 1.6. Weight-loss/Dietary Products

- 1.7. Ophthalmic Products

- 1.8. Sleeping Aids

- 1.9. Other Product Types

-

2. Distribution Channel

- 2.1. Retail Pharmacies

- 2.2. Online Pharmacies

- 2.3. Other Distribution Channels

Spain OTC Drugs Market Segmentation By Geography

- 1. Spain

Spain OTC Drugs Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Inclination of Pharmaceutical Companies to Switch From Rx to OTC Drugs; Increasing Self Medication Among the General Population; High Penetration in Emerging Markets

- 3.3. Market Restrains

- 3.3.1. Incorrect Self Diagnosis; Probability of Substance Abuse

- 3.4. Market Trends

- 3.4.1 The Cough

- 3.4.2 Cold

- 3.4.3 and Flu Products Segment is Expected to Dominate the Market over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain OTC Drugs Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Cough, Cold, and Flu Products

- 5.1.2. Analgesics

- 5.1.3. Dermatology Products

- 5.1.4. Gastrointestinal Products

- 5.1.5. Vitamin, Mineral, and Supplement (VMS) Products

- 5.1.6. Weight-loss/Dietary Products

- 5.1.7. Ophthalmic Products

- 5.1.8. Sleeping Aids

- 5.1.9. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Retail Pharmacies

- 5.2.2. Online Pharmacies

- 5.2.3. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Sanofi SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Reckitt Benckiser Group PLC

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Astrazeneca PLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Novartis AG

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Procter & Gamble ( Merck & Co )

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Leo Pharma AS

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Bristol-Myers Squibb

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Johnson and Johnson

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Cardinal Health

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Takeda Pharamaceutical Company Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Bayer

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 GlaxoSmithKline PLC

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Pfizer Inc

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 Sanofi SA

List of Figures

- Figure 1: Spain OTC Drugs Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain OTC Drugs Market Share (%) by Company 2024

List of Tables

- Table 1: Spain OTC Drugs Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain OTC Drugs Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Spain OTC Drugs Market Revenue Million Forecast, by Product 2019 & 2032

- Table 4: Spain OTC Drugs Market Volume K Unit Forecast, by Product 2019 & 2032

- Table 5: Spain OTC Drugs Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: Spain OTC Drugs Market Volume K Unit Forecast, by Distribution Channel 2019 & 2032

- Table 7: Spain OTC Drugs Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Spain OTC Drugs Market Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Spain OTC Drugs Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Spain OTC Drugs Market Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: Spain OTC Drugs Market Revenue Million Forecast, by Product 2019 & 2032

- Table 12: Spain OTC Drugs Market Volume K Unit Forecast, by Product 2019 & 2032

- Table 13: Spain OTC Drugs Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 14: Spain OTC Drugs Market Volume K Unit Forecast, by Distribution Channel 2019 & 2032

- Table 15: Spain OTC Drugs Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Spain OTC Drugs Market Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain OTC Drugs Market?

The projected CAGR is approximately 5.40%.

2. Which companies are prominent players in the Spain OTC Drugs Market?

Key companies in the market include Sanofi SA, Reckitt Benckiser Group PLC, Astrazeneca PLC, Novartis AG, Procter & Gamble ( Merck & Co ), Leo Pharma AS, Bristol-Myers Squibb, Johnson and Johnson, Cardinal Health, Takeda Pharamaceutical Company Ltd, Bayer, GlaxoSmithKline PLC, Pfizer Inc.

3. What are the main segments of the Spain OTC Drugs Market?

The market segments include Product, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Inclination of Pharmaceutical Companies to Switch From Rx to OTC Drugs; Increasing Self Medication Among the General Population; High Penetration in Emerging Markets.

6. What are the notable trends driving market growth?

The Cough. Cold. and Flu Products Segment is Expected to Dominate the Market over the Forecast Period.

7. Are there any restraints impacting market growth?

Incorrect Self Diagnosis; Probability of Substance Abuse.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain OTC Drugs Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain OTC Drugs Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain OTC Drugs Market?

To stay informed about further developments, trends, and reports in the Spain OTC Drugs Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence