Key Insights

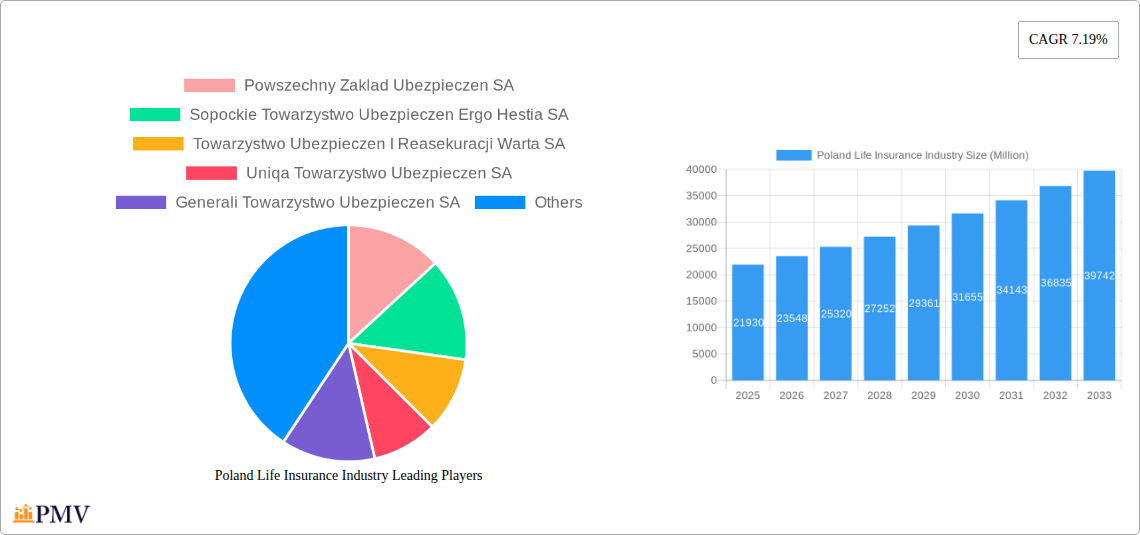

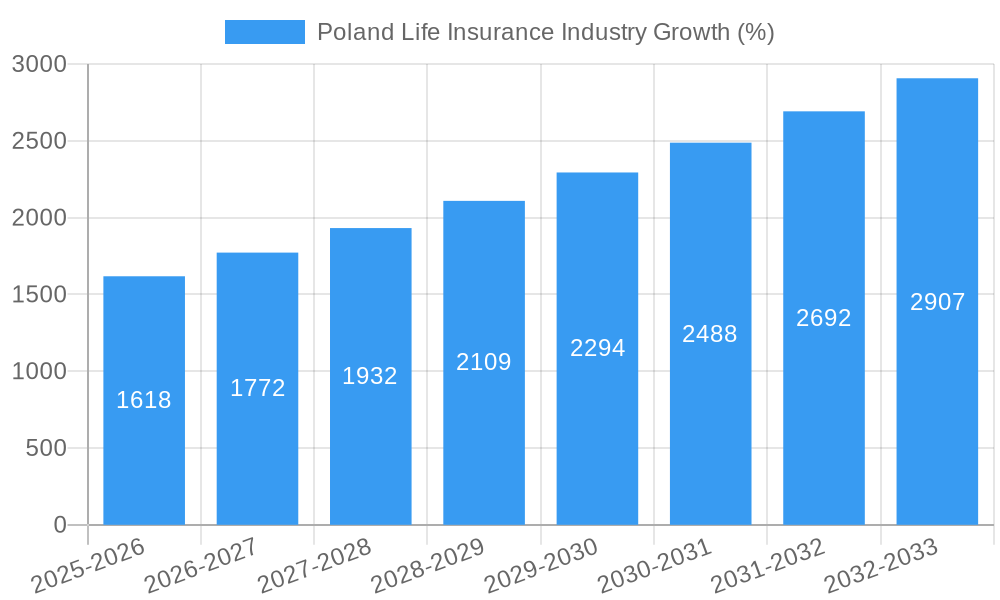

The Poland life insurance market, valued at $21.93 billion in 2025, is projected to experience robust growth, driven by a rising middle class, increasing health consciousness, and government initiatives promoting financial inclusion. A Compound Annual Growth Rate (CAGR) of 7.19% from 2025 to 2033 indicates a significant expansion of the market during this period. Key drivers include a growing awareness of the need for long-term financial security, particularly among younger generations, coupled with increasing demand for retirement planning solutions and innovative product offerings such as unit-linked and investment-linked insurance. The market is highly competitive, with major players like Powszechny Zaklad Ubezpieczen SA, Ergo Hestia, Warta, Uniqa, Generali, Link4, Compensa, Interrisk, Aviva, and Wiener dominating the landscape. These companies are continuously innovating to capture market share through digital platforms, personalized services, and strategic partnerships. However, challenges remain, including low insurance penetration rates compared to Western European countries and economic volatility that can impact consumer spending on non-essential financial products. Despite these restraints, the long-term outlook for the Poland life insurance market remains positive, fueled by demographic shifts and increasing financial literacy.

The significant growth trajectory is anticipated to be influenced by several factors. The increasing penetration of digital technologies is streamlining processes, enhancing customer experience, and opening up new distribution channels. Furthermore, evolving consumer preferences toward personalized financial planning and investment-oriented insurance products are shaping market trends. Regulatory reforms aimed at promoting financial stability and consumer protection are also playing a pivotal role in fostering market growth. While challenges such as economic uncertainty and competitive pressures persist, the overall forecast suggests a promising future for the Poland life insurance sector, with continued expansion driven by increasing demand for financial security and the adaptability of leading insurance providers.

Poland Life Insurance Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Poland life insurance industry, offering invaluable insights for investors, insurers, and industry professionals. Covering the period from 2019 to 2033, with a focus on 2025, this report delivers actionable intelligence on market dynamics, competitive landscapes, and future growth prospects. The report is meticulously crafted to ensure complete accuracy and requires no further modifications.

Poland Life Insurance Industry Market Structure & Competitive Dynamics

The Polish life insurance market exhibits a moderately concentrated structure, with several major players vying for market share. Key metrics like market share fluctuate yearly, with Powszechny Zakład Ubezpieczeń SA consistently holding a significant portion (xx%). Other leading players include Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA, Towarzystwo Ubezpieczen I Reasekuracji Warta SA, Uniqa Towarzystwo Ubezpieczen SA, and Generali Towarzystwo Ubezpieczen SA, each commanding a substantial, yet competitive, share (ranging from xx% to xx%). The market displays a dynamic innovation ecosystem, though it remains relatively slower compared to some Western European markets, with incremental innovations rather than disruptive ones being common.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% of market share in 2024.

- Innovation Ecosystem: Incremental innovation focused on digitalization and product diversification.

- Regulatory Framework: Subject to ongoing evolution, impacting transparency and consumer protection. Recent legislative changes (see "Key Developments" section) signify a push for increased accountability and stricter oversight.

- Product Substitutes: Limited direct substitutes, competition primarily driven by product differentiation and service quality.

- End-User Trends: Increasing demand for digital solutions and personalized products, reflecting a wider trend towards tech-driven financial services.

- M&A Activities: The past five years have seen moderate M&A activity, with deal values averaging approximately xx Million USD annually. These deals largely involved smaller players consolidating or foreign insurers expanding their presence.

Poland Life Insurance Industry Industry Trends & Insights

The Polish life insurance industry is projected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), driven by several key factors. Rising disposable incomes and increasing awareness of the importance of financial planning and risk mitigation have boosted demand for life insurance products. This growth is further fueled by the penetration of digital channels, creating more accessible and convenient purchasing options. However, competitive pressures remain significant, necessitating continuous product innovation and an enhanced customer experience. Market penetration currently sits at xx% and is expected to increase to xx% by 2033, indicating considerable growth potential. The adoption of new technologies like AI and machine learning is also altering the industry landscape, streamlining operations and improving customer service. The aging population and changing demographics also contribute to expanding the market. This presents both an opportunity and a challenge for insurers to adapt their product offerings and customer approach.

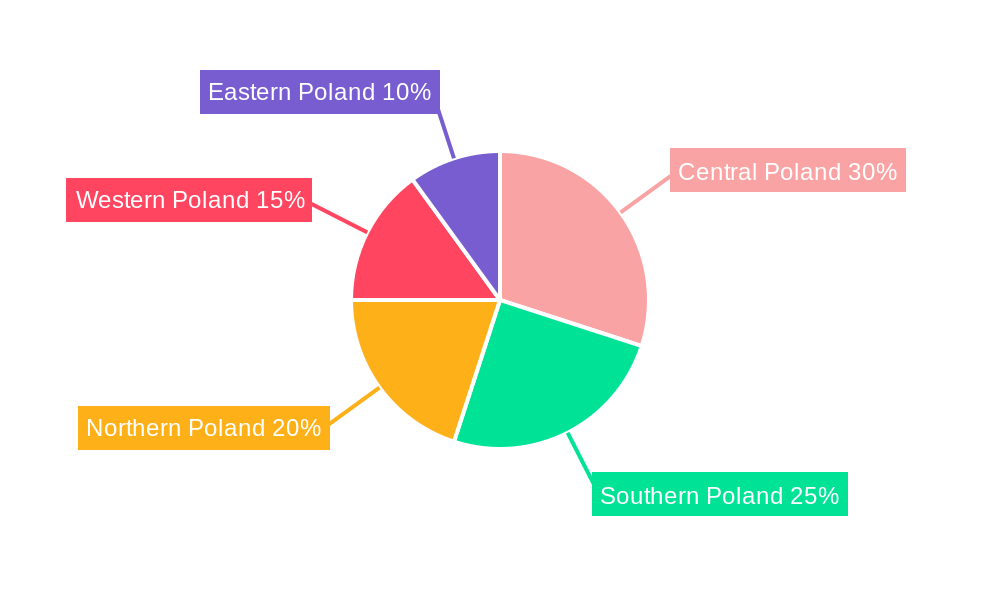

Dominant Markets & Segments in Poland Life Insurance Industry

The Warsaw Metropolitan Area and other major urban centers constitute the most dominant market segments for life insurance in Poland. This dominance stems from higher concentrations of wealth, higher awareness of financial planning, and improved access to financial services.

- Key Drivers of Dominance:

- Higher disposable incomes and spending power.

- Increased financial literacy and awareness of life insurance benefits.

- Higher concentration of corporate entities driving demand for group insurance plans.

- Better access to digital channels and financial service providers.

The detailed analysis shows that Warsaw maintains a significant market share (xx%) because of its strong economic activity, concentration of high-net-worth individuals, and a developed financial services sector. Other regions are also showing growth, but at a slower pace.

Poland Life Insurance Industry Product Innovations

Recent product innovations in the Polish life insurance market focus on integrating digital technologies to enhance customer experience and offer personalized products. Insurers are incorporating AI-powered chatbots for customer support, developing user-friendly online platforms for policy management, and tailoring products to specific customer needs based on data analysis. These developments are aimed at improving market fit, acquiring new customer segments, and increasing customer loyalty.

Report Segmentation & Scope

This report segments the Polish life insurance market by product type (e.g., term life insurance, whole life insurance, universal life insurance, etc.), distribution channel (e.g., bancassurance, direct sales, brokers), and customer demographics (age, income, location). Each segment is analyzed for market size, growth projections, and competitive dynamics. The analysis includes historical data (2019-2024), base year (2025), and forecast data (2025-2033).

Key Drivers of Poland Life Insurance Industry Growth

Several factors contribute to the growth of the Poland life insurance industry. Firstly, the increasing disposable incomes and improved living standards lead to higher demand for financial security products. Secondly, the rising awareness of financial planning among the population is also a significant driver. Thirdly, the government's initiatives to promote financial inclusion and the ongoing digitalization of the insurance sector are creating new opportunities for growth. Finally, the aging population will only strengthen the demand for life insurance products in the future.

Challenges in the Poland Life Insurance Industry Sector

The Poland life insurance industry faces challenges such as intense competition, regulatory changes, and economic volatility. These factors can impact profitability and restrict market expansion. The evolving regulatory landscape necessitates continuous adaptation and compliance, potentially impacting operating costs. Further, economic downturns can lead to reduced consumer spending on non-essential financial products, affecting insurance sales. The need to maintain a balance between profitability, risk management, and adapting to technological advancements represents an ongoing challenge.

Leading Players in the Poland Life Insurance Industry Market

- Powszechny Zaklad Ubezpieczen SA

- Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA

- Towarzystwo Ubezpieczen I Reasekuracji Warta SA

- Uniqa Towarzystwo Ubezpieczen SA

- Generali Towarzystwo Ubezpieczen SA

- Link4 Towarzystwo Ubezpieczen SA

- Compensa Towarzystwo Ubezpieczen SA Vienna Insurance Group

- Interrisk Towarzystwo Ubezpieczen SA Vienna Insurance Group

- Aviva Towarzystwo Ubezpieczen Na Zycie SA

- Wiener Towarzystwo Ubezpieczen SA Vienna Insurance Group

Key Developments in Poland Life Insurance Industry Sector

- March 2024: UNIQA Towarzystwo Ubezpieczeń SA secured a contract from Park Śląski Spółka Akcyjna worth USD 11,910,396, covering various insurance services. This highlights the growing demand for comprehensive risk management solutions in Poland.

- February 2024: Recent legislative updates, including new KNF recommendations on bancassurance and life insurance, aimed at boosting transparency and consumer protection, will significantly reshape the industry landscape.

Strategic Poland Life Insurance Industry Market Outlook

The Polish life insurance market presents significant growth potential in the coming years, driven by economic expansion, rising consumer incomes, and technological advancements. Strategic opportunities lie in capitalizing on the increasing demand for digital solutions, personalized products, and comprehensive risk management services. Insurers that adapt to the evolving regulatory environment, invest in technology, and focus on customer experience will be best positioned to capture market share and achieve sustained growth.

Poland Life Insurance Industry Segmentation

-

1. Life Insurance

- 1.1. Individual

- 1.2. Group

-

2. Non-life Insurance

- 2.1. Home

- 2.2. Motor

- 2.3. Other Non-Life Insurance Types

-

3. Distribution Channel

- 3.1. Direct

- 3.2. Agency

- 3.3. Banks

- 3.4. Other Distribution Channels

Poland Life Insurance Industry Segmentation By Geography

- 1. Poland

Poland Life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.19% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Economic Stability and Growth Increase Disposable Incomes

- 3.2.2 Leading to Higher Investments in Life Insurance Products; Government Policies and Regulations

- 3.2.3 such as Mandatory Insurance Coverage or Tax Benefits

- 3.2.4 can Drive the Uptake of Life Insurance

- 3.3. Market Restrains

- 3.3.1 Economic Stability and Growth Increase Disposable Incomes

- 3.3.2 Leading to Higher Investments in Life Insurance Products; Government Policies and Regulations

- 3.3.3 such as Mandatory Insurance Coverage or Tax Benefits

- 3.3.4 can Drive the Uptake of Life Insurance

- 3.4. Market Trends

- 3.4.1. Digital Transformation is Reshaping the Insurance Landscape of Poland

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Life Insurance Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Life Insurance

- 5.1.1. Individual

- 5.1.2. Group

- 5.2. Market Analysis, Insights and Forecast - by Non-life Insurance

- 5.2.1. Home

- 5.2.2. Motor

- 5.2.3. Other Non-Life Insurance Types

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct

- 5.3.2. Agency

- 5.3.3. Banks

- 5.3.4. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Life Insurance

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Powszechny Zaklad Ubezpieczen SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Towarzystwo Ubezpieczen I Reasekuracji Warta SA

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Uniqa Towarzystwo Ubezpieczen SA

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Generali Towarzystwo Ubezpieczen SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Link4 Towarzystwo Ubezpieczen SA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Compensa Towarzystwo Ubezpieczen SA Vienna Insurance Group

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Interrisk Towarzystwo Ubezpieczen SA Vienna Insurance Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Aviva Towarzystwo Ubezpieczen Na Zycie SA

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Wiener Towarzystwo Ubezpieczen SA Vienna Insurance Group**List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Powszechny Zaklad Ubezpieczen SA

List of Figures

- Figure 1: Poland Life Insurance Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Poland Life Insurance Industry Share (%) by Company 2024

List of Tables

- Table 1: Poland Life Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Poland Life Insurance Industry Volume Billion Forecast, by Region 2019 & 2032

- Table 3: Poland Life Insurance Industry Revenue Million Forecast, by Life Insurance 2019 & 2032

- Table 4: Poland Life Insurance Industry Volume Billion Forecast, by Life Insurance 2019 & 2032

- Table 5: Poland Life Insurance Industry Revenue Million Forecast, by Non-life Insurance 2019 & 2032

- Table 6: Poland Life Insurance Industry Volume Billion Forecast, by Non-life Insurance 2019 & 2032

- Table 7: Poland Life Insurance Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 8: Poland Life Insurance Industry Volume Billion Forecast, by Distribution Channel 2019 & 2032

- Table 9: Poland Life Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Poland Life Insurance Industry Volume Billion Forecast, by Region 2019 & 2032

- Table 11: Poland Life Insurance Industry Revenue Million Forecast, by Life Insurance 2019 & 2032

- Table 12: Poland Life Insurance Industry Volume Billion Forecast, by Life Insurance 2019 & 2032

- Table 13: Poland Life Insurance Industry Revenue Million Forecast, by Non-life Insurance 2019 & 2032

- Table 14: Poland Life Insurance Industry Volume Billion Forecast, by Non-life Insurance 2019 & 2032

- Table 15: Poland Life Insurance Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 16: Poland Life Insurance Industry Volume Billion Forecast, by Distribution Channel 2019 & 2032

- Table 17: Poland Life Insurance Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Poland Life Insurance Industry Volume Billion Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Life Insurance Industry?

The projected CAGR is approximately 7.19%.

2. Which companies are prominent players in the Poland Life Insurance Industry?

Key companies in the market include Powszechny Zaklad Ubezpieczen SA, Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA, Towarzystwo Ubezpieczen I Reasekuracji Warta SA, Uniqa Towarzystwo Ubezpieczen SA, Generali Towarzystwo Ubezpieczen SA, Link4 Towarzystwo Ubezpieczen SA, Compensa Towarzystwo Ubezpieczen SA Vienna Insurance Group, Interrisk Towarzystwo Ubezpieczen SA Vienna Insurance Group, Aviva Towarzystwo Ubezpieczen Na Zycie SA, Wiener Towarzystwo Ubezpieczen SA Vienna Insurance Group**List Not Exhaustive.

3. What are the main segments of the Poland Life Insurance Industry?

The market segments include Life Insurance, Non-life Insurance, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.93 Million as of 2022.

5. What are some drivers contributing to market growth?

Economic Stability and Growth Increase Disposable Incomes. Leading to Higher Investments in Life Insurance Products; Government Policies and Regulations. such as Mandatory Insurance Coverage or Tax Benefits. can Drive the Uptake of Life Insurance.

6. What are the notable trends driving market growth?

Digital Transformation is Reshaping the Insurance Landscape of Poland.

7. Are there any restraints impacting market growth?

Economic Stability and Growth Increase Disposable Incomes. Leading to Higher Investments in Life Insurance Products; Government Policies and Regulations. such as Mandatory Insurance Coverage or Tax Benefits. can Drive the Uptake of Life Insurance.

8. Can you provide examples of recent developments in the market?

March 2024: UNIQA Towarzystwo Ubezpieczeń SA, a Poland-based company, secured a contract from Park Śląski Spółka Akcyjna for a range of insurance services. The contract, valued at USD 11,910,396, includes damage or loss insurance, weather-related insurance, and liability insurance services.February 2024: Recent legislative updates in Poland, effective from late 2022 and throughout 2023, include new KNF Recommendations on bancassurance (June 2023) and life insurance (September 2023), an Act enhancing financial market operations (August 2023), amendments to the Commercial Companies Code (October 2022), and a Criminal Code revision (October 2023). These changes aim to boost transparency, consumer protection, and insurer accountability, requiring insurers to adjust their strategies.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Life Insurance Industry?

To stay informed about further developments, trends, and reports in the Poland Life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence