Key Insights

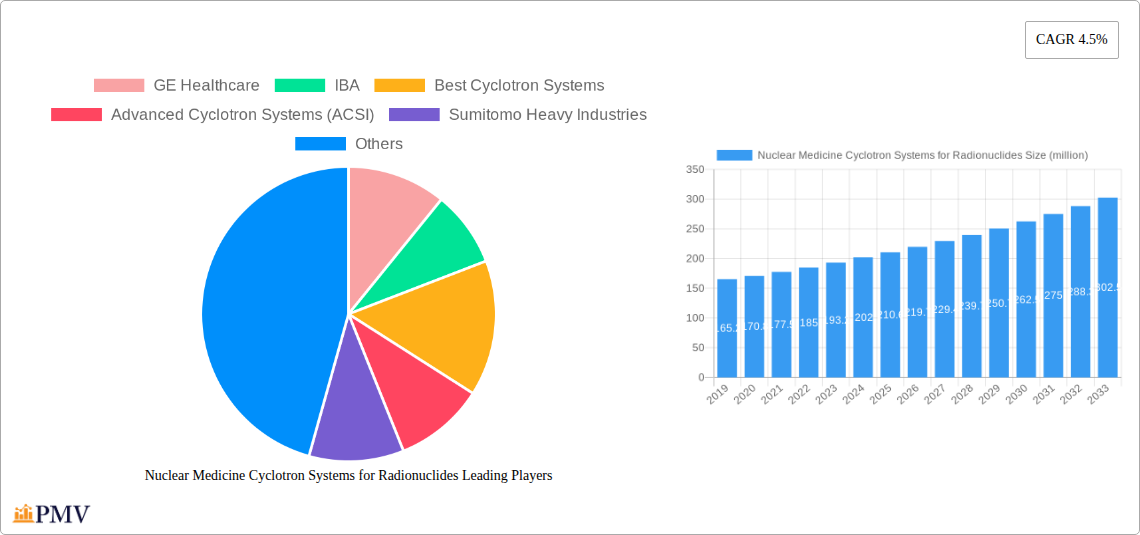

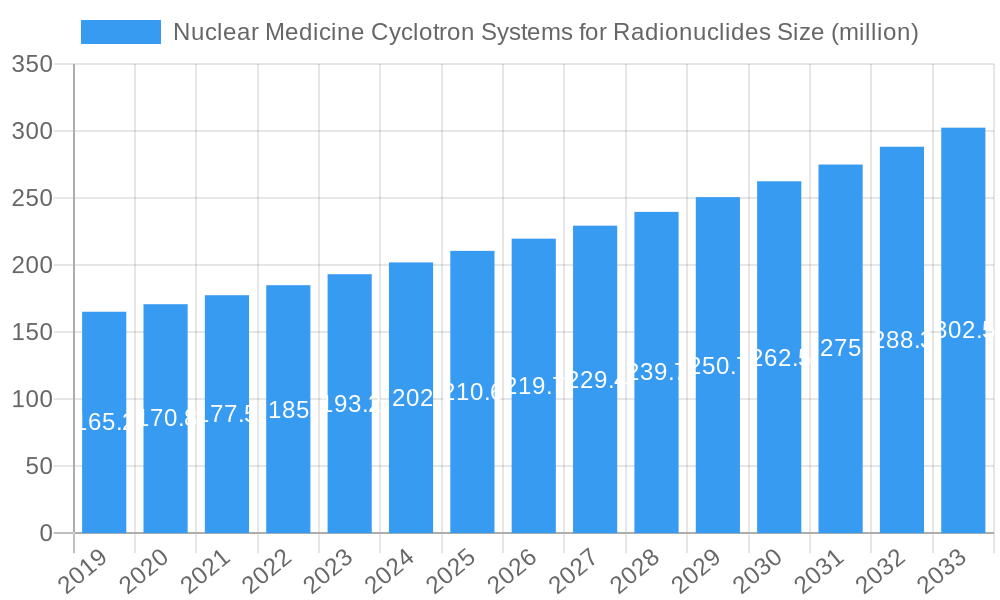

The global market for Nuclear Medicine Cyclotron Systems for Radionuclides is poised for robust growth, projected to reach approximately USD 210.6 million in 2025 with a Compound Annual Growth Rate (CAGR) of 4.5% over the forecast period of 2025-2033. This expansion is primarily driven by the increasing demand for advanced diagnostic and therapeutic applications in nuclear medicine. The growing prevalence of chronic diseases, coupled with rising healthcare expenditure and an aging global population, significantly fuels the need for accurate and early disease detection and personalized treatment solutions offered by cyclotron-produced radionuclides. Technological advancements in cyclotron design, leading to higher efficiency, smaller footprints, and increased radionuclide production capabilities, are further stimulating market penetration. The market is segmented by application into Diagnosis Radionuclides and Treatment Radionuclides, with diagnosis applications currently holding a larger share due to their widespread use in imaging modalities like PET scans.

Nuclear Medicine Cyclotron Systems for Radionuclides Market Size (In Million)

The market’s growth trajectory is further supported by ongoing research and development efforts focused on expanding the utility of radiopharmaceuticals in areas such as oncology, cardiology, and neurology. While the market is characterized by significant investment in high-energy cyclotrons for producing a wider range of isotopes, there's also a growing interest in compact and more accessible cyclotron systems for distributed radiopharmaceutical production. Key players like GE Healthcare and IBA are at the forefront, investing in innovation and strategic partnerships to expand their product portfolios and geographical reach. Despite the positive outlook, potential restraints such as the high initial cost of cyclotron systems and stringent regulatory approvals for radiopharmaceuticals may present challenges. However, the expanding pipeline of novel radiopharmaceuticals and the continuous drive for precision medicine are expected to outweigh these limitations, ensuring sustained market expansion in the coming years.

Nuclear Medicine Cyclotron Systems for Radionuclides Company Market Share

This in-depth market research report provides a detailed analysis of the global Nuclear Medicine Cyclotron Systems for Radionuclides market, a critical segment powering advanced medical imaging and therapeutic applications. Spanning a study period from 2019 to 2033, with a base year of 2025, this report offers unparalleled insights into market dynamics, growth drivers, technological advancements, and competitive landscapes. We dissect market concentration, innovation ecosystems, regulatory frameworks, product substitutes, end-user trends, and M&A activities, providing actionable intelligence for stakeholders.

The report covers key segments including Diagnosis Radionuclides and Treatment Radionuclides, and further categorizes systems by Cyclotron Less than 12 MeV, Cyclotron 13-18 MeV, Cyclotron 19-24 MeV, and Cyclotron More than 24 MeV. With meticulous data collection and expert analysis, we project the market's trajectory, identifying opportunities and challenges within this rapidly evolving sector. This report is essential for industry leaders, investors, researchers, and policymakers seeking to understand and capitalize on the future of nuclear medicine.

Nuclear Medicine Cyclotron Systems for Radionuclides Market Structure & Competitive Dynamics

The global Nuclear Medicine Cyclotron Systems for Radionuclides market exhibits a moderately concentrated structure, with a few key players holding significant market share, estimated at over 70% collectively. Innovation ecosystems are robust, driven by continuous research and development in particle accelerator technology and radioisotope production. Regulatory frameworks, primarily governed by national health authorities and international standards bodies, are stringent, influencing product development and market entry. Product substitutes, while evolving, currently offer limited direct replacement for cyclotron-produced radionuclides in high-demand applications. End-user trends indicate a growing preference for on-site radionuclide production, reducing reliance on centralized facilities and transportation logistics, thereby enhancing patient access and diagnostic timeliness. Mergers and acquisitions (M&A) activity, while not consistently high in volume, often involve substantial deal values, with recent transactions estimated in the range of xx million to xx million USD, aimed at consolidating market position, acquiring technological expertise, or expanding product portfolios. The competitive landscape is characterized by a strong emphasis on product reliability, technological sophistication, and comprehensive service offerings.

Nuclear Medicine Cyclotron Systems for Radionuclides Industry Trends & Insights

The Nuclear Medicine Cyclotron Systems for Radionuclides industry is poised for significant expansion, driven by an escalating demand for advanced diagnostic and therapeutic radiopharmaceuticals. Market growth is propelled by several key factors, including the increasing prevalence of chronic diseases such as cancer and neurological disorders, which necessitate sophisticated imaging techniques for early detection and effective management. The aging global population further contributes to this demand, as older demographics are more susceptible to conditions requiring nuclear medicine interventions. Technological advancements are revolutionizing the field, with next-generation cyclotrons offering improved efficiency, reduced footprint, and enhanced safety profiles, making them more accessible to smaller medical centers and research institutions. The ongoing development of novel radiotracers for targeted therapies and personalized medicine is also a major growth catalyst. Consumer preferences are shifting towards integrated solutions that encompass not only the cyclotron hardware but also the associated software, radiopharmacy expertise, and maintenance services. Competitive dynamics are intensifying, with established players investing heavily in R&D to develop more compact, cost-effective, and versatile cyclotron systems. Emerging markets, particularly in Asia-Pacific and Latin America, present substantial untapped potential, fueled by improving healthcare infrastructure and increasing government investments in medical technology. The market penetration of cyclotron-based radionuclide production is projected to grow steadily, reaching an estimated xx% by 2033. The compound annual growth rate (CAGR) for the forecast period (2025–2033) is anticipated to be in the range of 6.5% to 7.5%, reflecting the robust underlying demand and continuous innovation.

Dominant Markets & Segments in Nuclear Medicine Cyclotron Systems for Radionuclides

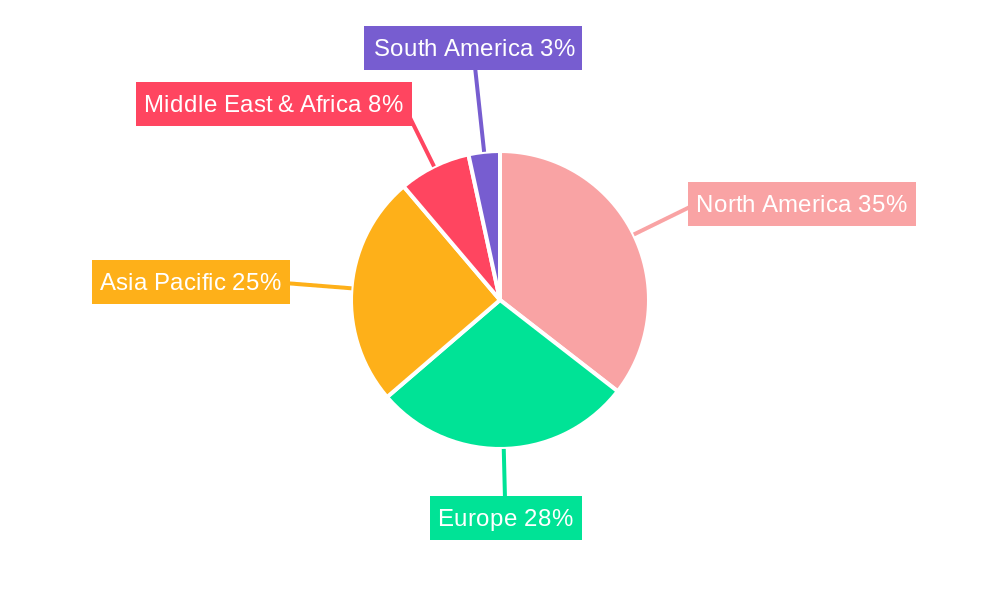

The Diagnosis Radionuclides segment stands as the dominant force within the Nuclear Medicine Cyclotron Systems for Radionuclides market, largely attributed to the widespread use of positron emission tomography (PET) and single-photon emission computed tomography (SPECT) in oncology, cardiology, and neurology. Within this broad segment, Cyclotron 13-18 MeV systems represent a significant sub-segment, offering a versatile energy range suitable for producing a wide array of commonly used diagnostic isotopes like Fluorine-18 (¹⁸F) and Carbon-11 (¹¹C) with optimal efficiency. The leading region globally is North America, driven by a well-established healthcare infrastructure, high adoption rates of advanced medical technologies, and substantial government funding for medical research and development.

Key Drivers of Dominance in North America:

- Economic Policies: Favorable reimbursement policies for nuclear medicine procedures and significant private and public investment in healthcare infrastructure.

- Infrastructure: A dense network of hospitals, research centers, and imaging facilities equipped with advanced PET/CT and SPECT/CT scanners.

- Technological Adoption: Early and widespread adoption of cyclotron technology for on-site radionuclide production, enhancing research capabilities and patient access.

- Research and Development: A strong ecosystem of academic institutions and pharmaceutical companies actively engaged in developing new radiopharmaceuticals and cyclotron applications.

Globally, the Types segment of Cyclotron 19-24 MeV is also experiencing considerable growth, particularly for institutions requiring the production of higher-energy isotopes or with more specialized research requirements. The Treatment Radionuclides segment, while smaller, is projected for robust growth, fueled by advancements in targeted alpha therapy (TAT) and peptide receptor radionuclide therapy (PRRT). The economic policies in key countries, such as tax incentives for healthcare technology adoption and grants for medical research, play a crucial role in fostering market expansion.

Nuclear Medicine Cyclotron Systems for Radionuclides Product Innovations

Recent product innovations in Nuclear Medicine Cyclotron Systems for Radionuclides focus on enhancing operational efficiency, reducing system footprints, and expanding the range of producible isotopes. Manufacturers are developing more compact and integrated cyclotron designs, suitable for installation in smaller hospital settings and research laboratories. Advancements in superconducting magnet technology have led to more powerful yet energy-efficient systems. Furthermore, there's a strong emphasis on developing cyclotrons capable of producing a wider spectrum of radionuclides for both diagnostic and therapeutic applications, including those for targeted radionuclide therapy. These innovations aim to lower the cost of ownership, improve accessibility, and broaden the clinical utility of on-site radionuclide production.

Report Segmentation & Scope

This comprehensive report segments the Nuclear Medicine Cyclotron Systems for Radionuclides market across key parameters to provide granular insights. The segmentation includes:

Application:

- Diagnosis Radionuclides: This segment focuses on cyclotrons used for producing isotopes for medical imaging, crucial for diagnosing a wide range of diseases. Growth projections for this segment are strong, driven by increasing diagnostic needs.

- Treatment Radionuclides: This segment encompasses cyclotrons utilized for generating isotopes used in cancer therapy and other therapeutic applications. This segment is expected to witness rapid expansion due to advancements in radiopharmaceutical therapies.

Types:

- Cyclotron Less than 12 MeV: Primarily used for producing specific, lower-energy isotopes, often in specialized research settings.

- Cyclotron 13-18 MeV: A widely adopted category, capable of producing essential diagnostic radionuclides like ¹⁸F and ¹¹C, with significant market share and steady growth.

- Cyclotron 19-24 MeV: Offers greater versatility for producing a broader range of isotopes, catering to more advanced research and therapeutic needs, showing robust growth.

- Cyclotron More than 24 MeV: Designed for producing higher-energy isotopes or for large-scale production, serving major research institutions and radiopharmacies, with steady but specialized demand.

Key Drivers of Nuclear Medicine Cyclotron Systems for Radionuclides Growth

The growth of the Nuclear Medicine Cyclotron Systems for Radionuclides market is propelled by several interconnected factors. The escalating global burden of cancer and neurodegenerative diseases necessitates advanced diagnostic imaging techniques like PET, which rely heavily on cyclotron-produced isotopes. Technological advancements in accelerator physics and radioisotope production are leading to more efficient, compact, and cost-effective cyclotron systems, lowering barriers to adoption for smaller healthcare facilities. Favorable government initiatives and increasing healthcare expenditure in emerging economies are further stimulating market demand. The continuous development of novel radiopharmaceuticals for targeted therapies and personalized medicine also acts as a significant growth accelerator, creating a demand for versatile cyclotron capabilities.

Challenges in the Nuclear Medicine Cyclotron Systems for Radionuclides Sector

Despite its robust growth, the Nuclear Medicine Cyclotron Systems for Radionuclides sector faces several challenges. The high initial capital investment required for cyclotron installation and infrastructure remains a significant barrier, particularly for smaller institutions or those in less developed regions. Stringent regulatory requirements for licensing, operation, and quality control of radiopharmaceuticals add complexity and cost to market entry and ongoing operations. Supply chain disruptions for critical components and raw materials can impact production timelines and operational continuity. Furthermore, the availability of skilled personnel for operating and maintaining these sophisticated systems can be a limiting factor. Competitive pressures from established players and emerging technologies also necessitate continuous innovation and cost optimization.

Leading Players in the Nuclear Medicine Cyclotron Systems for Radionuclides Market

- GE Healthcare

- IBA

- Best Cyclotron Systems

- Advanced Cyclotron Systems (ACSI)

- Sumitomo Heavy Industries

- Longevous Beamtech

Key Developments in Nuclear Medicine Cyclotron Systems for Radionuclides Sector

- 2023 October: GE Healthcare announces advancements in its PET tracer portfolio and cyclotron technology, aiming to expand accessibility for diagnostic imaging.

- 2023 September: IBA receives regulatory approval for a new compact cyclotron model designed for decentralized radionuclide production, enhancing local supply capabilities.

- 2023 July: Sumitomo Heavy Industries showcases its latest superconducting cyclotron technology, emphasizing improved beam stability and energy efficiency at a leading industry conference.

- 2022 December: Advanced Cyclotron Systems (ACSI) announces a strategic partnership with a major radiopharmacy network to expand its service offerings and radionuclide distribution.

- 2022 September: Best Cyclotron Systems unveils a new generation of smaller, more affordable cyclotrons targeted at community hospitals and research labs.

Strategic Nuclear Medicine Cyclotron Systems for Radionuclides Market Outlook

The strategic outlook for the Nuclear Medicine Cyclotron Systems for Radionuclides market is exceptionally positive, characterized by sustained growth and transformative innovation. Future market potential lies in the increasing integration of cyclotrons into routine clinical practice, driven by the demand for personalized medicine and the expansion of targeted radionuclide therapies. Key growth accelerators include ongoing R&D in novel radioisotopes, the development of artificial intelligence (AI)-powered operational optimization for cyclotron systems, and strategic collaborations between cyclotron manufacturers, radiopharmaceutical developers, and healthcare providers. Opportunities exist in expanding market penetration in underserved regions and in developing more sustainable and energy-efficient cyclotron technologies to address environmental concerns.

Nuclear Medicine Cyclotron Systems for Radionuclides Segmentation

-

1. Application

- 1.1. Diagnosis Radionuclides

- 1.2. Treatment Radionuclides

-

2. Types

- 2.1. Cyclotron Less than 12 MeV

- 2.2. Cyclotron 13-18 MeV

- 2.3. Cyclotron 19-24 MeV

- 2.4. Cyclotron More than 24 MeV

Nuclear Medicine Cyclotron Systems for Radionuclides Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Nuclear Medicine Cyclotron Systems for Radionuclides Regional Market Share

Geographic Coverage of Nuclear Medicine Cyclotron Systems for Radionuclides

Nuclear Medicine Cyclotron Systems for Radionuclides REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Diagnosis Radionuclides

- 5.1.2. Treatment Radionuclides

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cyclotron Less than 12 MeV

- 5.2.2. Cyclotron 13-18 MeV

- 5.2.3. Cyclotron 19-24 MeV

- 5.2.4. Cyclotron More than 24 MeV

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Nuclear Medicine Cyclotron Systems for Radionuclides Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Diagnosis Radionuclides

- 6.1.2. Treatment Radionuclides

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cyclotron Less than 12 MeV

- 6.2.2. Cyclotron 13-18 MeV

- 6.2.3. Cyclotron 19-24 MeV

- 6.2.4. Cyclotron More than 24 MeV

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Nuclear Medicine Cyclotron Systems for Radionuclides Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Diagnosis Radionuclides

- 7.1.2. Treatment Radionuclides

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cyclotron Less than 12 MeV

- 7.2.2. Cyclotron 13-18 MeV

- 7.2.3. Cyclotron 19-24 MeV

- 7.2.4. Cyclotron More than 24 MeV

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Nuclear Medicine Cyclotron Systems for Radionuclides Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Diagnosis Radionuclides

- 8.1.2. Treatment Radionuclides

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cyclotron Less than 12 MeV

- 8.2.2. Cyclotron 13-18 MeV

- 8.2.3. Cyclotron 19-24 MeV

- 8.2.4. Cyclotron More than 24 MeV

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Nuclear Medicine Cyclotron Systems for Radionuclides Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Diagnosis Radionuclides

- 9.1.2. Treatment Radionuclides

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cyclotron Less than 12 MeV

- 9.2.2. Cyclotron 13-18 MeV

- 9.2.3. Cyclotron 19-24 MeV

- 9.2.4. Cyclotron More than 24 MeV

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Diagnosis Radionuclides

- 10.1.2. Treatment Radionuclides

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cyclotron Less than 12 MeV

- 10.2.2. Cyclotron 13-18 MeV

- 10.2.3. Cyclotron 19-24 MeV

- 10.2.4. Cyclotron More than 24 MeV

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Diagnosis Radionuclides

- 11.1.2. Treatment Radionuclides

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Cyclotron Less than 12 MeV

- 11.2.2. Cyclotron 13-18 MeV

- 11.2.3. Cyclotron 19-24 MeV

- 11.2.4. Cyclotron More than 24 MeV

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 GE Healthcare

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 IBA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Best Cyclotron Systems

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Advanced Cyclotron Systems (ACSI)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sumitomo Heavy Industries

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Longevous Beamtech

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 GE Healthcare

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Application 2025 & 2033

- Figure 3: North America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Types 2025 & 2033

- Figure 5: North America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Country 2025 & 2033

- Figure 7: North America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Application 2025 & 2033

- Figure 9: South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Types 2025 & 2033

- Figure 11: South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Country 2025 & 2033

- Figure 13: South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Nuclear Medicine Cyclotron Systems for Radionuclides Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Nuclear Medicine Cyclotron Systems for Radionuclides Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Nuclear Medicine Cyclotron Systems for Radionuclides?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Nuclear Medicine Cyclotron Systems for Radionuclides?

Key companies in the market include GE Healthcare, IBA, Best Cyclotron Systems, Advanced Cyclotron Systems (ACSI), Sumitomo Heavy Industries, Longevous Beamtech.

3. What are the main segments of the Nuclear Medicine Cyclotron Systems for Radionuclides?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 210.6 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Nuclear Medicine Cyclotron Systems for Radionuclides," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Nuclear Medicine Cyclotron Systems for Radionuclides report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Nuclear Medicine Cyclotron Systems for Radionuclides?

To stay informed about further developments, trends, and reports in the Nuclear Medicine Cyclotron Systems for Radionuclides, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence