Key Insights

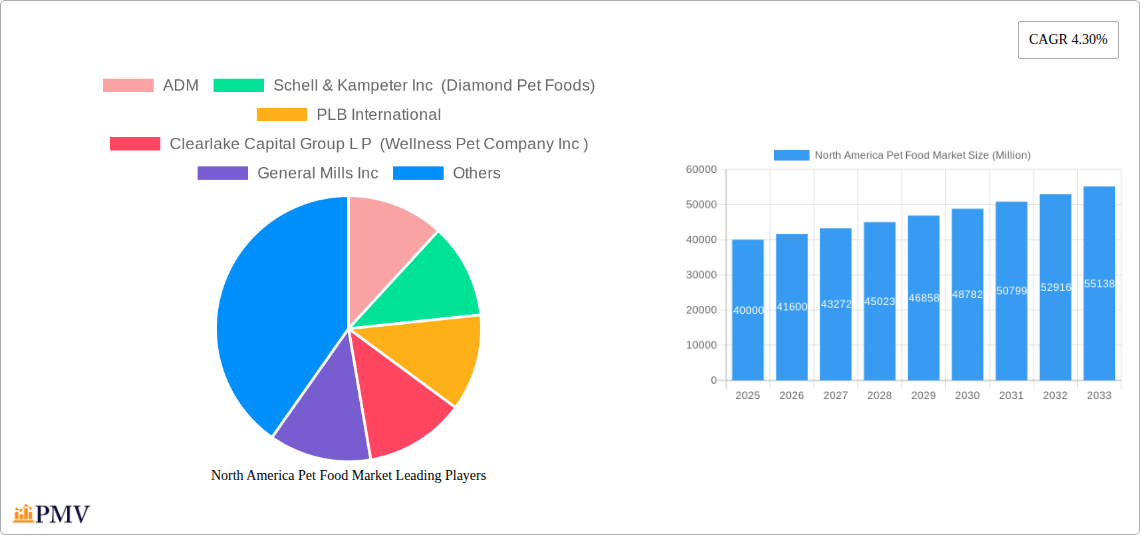

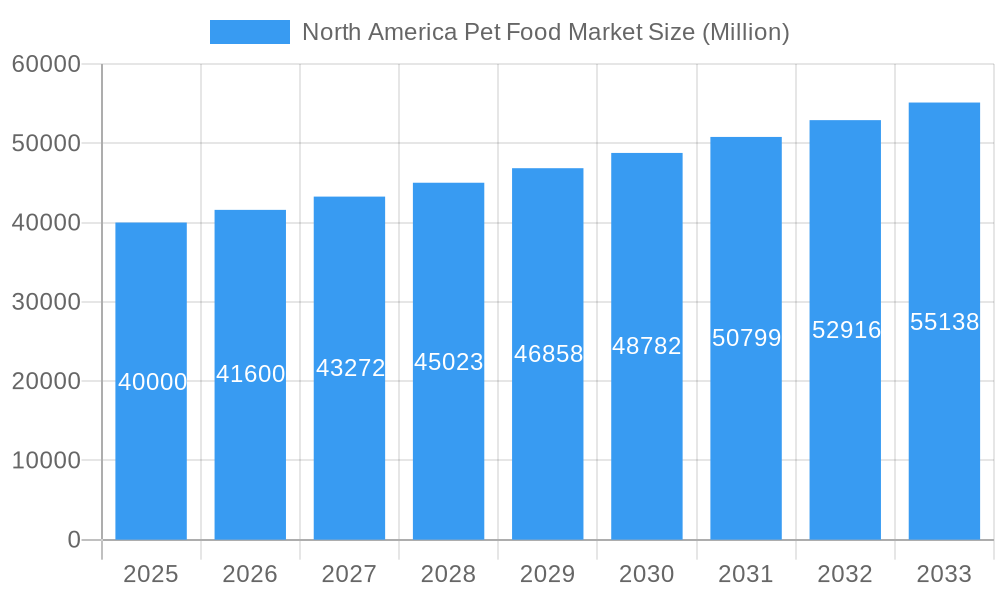

The North American pet food market, valued at approximately $40 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 4.30% from 2025 to 2033. This growth is fueled by several key factors. Increasing pet ownership, particularly of dogs and cats, across the United States, Canada, and Mexico, forms a significant driver. A rising trend towards premiumization, with pet owners prioritizing higher-quality ingredients and specialized diets tailored to their pet's specific needs (e.g., grain-free, organic, hypoallergenic), is another significant factor boosting market value. The convenience offered by online retail channels and the expansion of specialized pet food stores are also contributing to market expansion. While economic downturns could potentially restrain growth, the strong human-animal bond and the increasing willingness to invest in pet health and wellness are expected to mitigate these challenges.

North America Pet Food Market Market Size (In Billion)

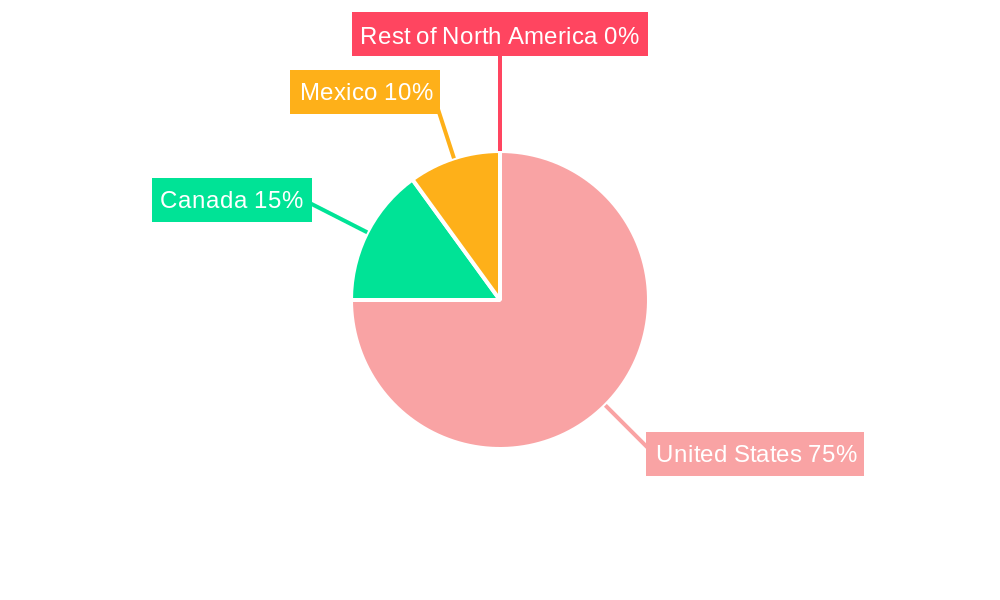

The market segmentation reveals a dynamic landscape. Supermarkets/hypermarkets and convenience stores remain dominant distribution channels, but online sales are experiencing rapid growth, driven by ease of access and competitive pricing. The product segment is dominated by food for cats and dogs, with a notable rise in demand for other veterinary diets reflecting increasing awareness of pet health issues. While the United States commands the largest market share within North America, Canada and Mexico are also showing promising growth trajectories, reflecting increasing pet ownership and disposable income in these regions. Major players like Mars Incorporated, Nestle Purina, and General Mills are leveraging their established brands and distribution networks to maintain market leadership, while smaller, specialized companies are focusing on niche segments (e.g., organic, natural pet food) to carve out their market share. The forecast period suggests sustained growth driven by ongoing trends in pet ownership, premiumization, and evolving consumer preferences.

North America Pet Food Market Company Market Share

North America Pet Food Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America pet food market, offering invaluable insights for industry stakeholders. Covering the period 2019-2033, with a focus on 2025, this report meticulously examines market dynamics, competitive landscapes, and future growth trajectories. The report uses Million for all values.

North America Pet Food Market Market Structure & Competitive Dynamics

The North American pet food market is characterized by a concentrated yet dynamic competitive landscape. Major players like Mars Incorporated, Nestle (Purina), and Colgate-Palmolive Company (Hill's Pet Nutrition Inc) hold significant market share, driving innovation and influencing market trends. However, smaller companies and new entrants continue to challenge the established players through niche product offerings and strategic acquisitions. The market exhibits a high level of consolidation, with mergers and acquisitions (M&A) playing a crucial role in shaping market structure. Recent M&A activities, estimated at xx Million in value in 2024, illustrate the ongoing consolidation trend.

- Market Concentration: Highly concentrated, with top 5 players holding approximately xx% of market share in 2024.

- Innovation Ecosystems: Strong focus on premiumization, natural ingredients, and specialized diets for various pet health conditions.

- Regulatory Frameworks: Subject to evolving regulations related to pet food safety, labeling, and ingredient sourcing.

- Product Substitutes: Limited direct substitutes, but increasing competition from homemade pet food and alternative protein sources.

- End-User Trends: Growing demand for premium, natural, and functional pet foods reflecting the increasing humanization of pets.

- M&A Activities: Significant M&A activity driven by expansion strategies and access to new technologies and product lines. Examples include Clearlake Capital Group L P's acquisition of Wellness Pet Company Inc and other undisclosed deals totaling xx Million in the last five years.

North America Pet Food Market Industry Trends & Insights

The North American pet food market is experiencing dynamic and sustained growth, propelled by several significant trends. The profound humanization of pets continues to be a primary catalyst, with owners increasingly viewing their animals as integral family members. This elevated emotional connection directly fuels the demand for premium, specialized, and health-oriented pet food options. Coupled with a consistent rise in pet ownership across the region, particularly in urban and suburban areas, the market for high-quality nutrition is expanding rapidly.

Technological advancements are revolutionizing every facet of the industry, from cutting-edge research into pet nutrition and the development of novel formulations to advancements in sustainable packaging and sophisticated, direct-to-consumer distribution models. Consumer preferences are clearly shifting towards natural, organic, and functional pet foods designed to address specific health and wellness concerns. This includes specialized diets for weight management, allergy relief, senior pet care, and even targeted nutritional support for specific breeds or life stages. The market's Compound Annual Growth Rate (CAGR) from 2019 to 2024 is estimated to be robust, with the market penetration of premium pet food products projected to exceed [Insert updated percentage here, e.g., 65%] in 2024. The competitive landscape is characterized by intense rivalry among established industry giants and a vibrant ecosystem of innovative startups, fostering continuous product innovation, sophisticated marketing campaigns, and strategic partnerships.

Dominant Markets & Segments in North America Pet Food Market

The United States continues to be the undisputed leader in the North American pet food market, commanding a substantial portion of the total market value, estimated at approximately [Insert updated percentage here, e.g., 70%] in 2024. Within the vast U.S. market, the dog food segment remains the largest and most significant, driven by the sheer volume of dog ownership and the substantial expenditure on their care. The cat food segment follows closely, also demonstrating strong growth, while other pet food categories, including those for small animals, birds, and fish, contribute to the overall market diversity.

- Leading Region: United States (consistently demonstrating the highest consumption and expenditure).

- Leading Country: United States (a mature yet continuously expanding market).

- Leading Distribution Channel: Supermarkets and Hypermarkets continue to lead due to their accessibility and broad product selection. However, online channels are experiencing the most rapid growth, driven by convenience, subscription services, and the increasing availability of specialized products.

- Leading Pet Food Product Segment: Dog Food remains dominant, attributed to higher pet ownership rates, longer lifespans, and the trend of owners investing more in high-quality nutrition for their canine companions.

- Leading Pet Segment: Dogs, reflecting higher ownership numbers and a greater willingness among owners to spend on premium food and treats.

Key Drivers for Dominance (United States):

- Exceptionally high pet ownership rates and a deeply ingrained culture of pet companionship.

- Strong consumer disposable incomes enabling higher spending on pet care and premium products.

- A highly developed and efficient retail infrastructure, encompassing both brick-and-mortar and robust e-commerce platforms.

- Widespread internet penetration and a high adoption rate of online shopping for everyday necessities, including pet food.

North America Pet Food Market Product Innovations

Innovation in the North American pet food market is increasingly focused on holistic pet health and enhanced well-being. A significant trend is the incorporation of novel and sustainable protein sources, such as insect protein (e.g., black soldier fly larvae), which offer a high nutritional profile and a reduced environmental footprint. Functional formulations are also gaining prominence, utilizing specialized ingredients to target specific dietary needs and health concerns. These include prebiotics and probiotics for gut health, omega-3 fatty acids for skin and coat health, antioxidants for immune support, and low-glycemic formulations for diabetic or weight-conscious pets.

Technological advancements are playing a crucial role in improving pet food quality and safety. Advanced processing techniques, such as high-pressure processing (HPP) and freeze-drying, are being adopted to preserve nutritional integrity and enhance shelf-life without the need for excessive artificial preservatives. Innovations in packaging are also addressing consumer demand for sustainability and convenience, with a rise in recyclable materials, portion-controlled packaging, and resealable options. The market is witnessing a proliferation of premium and super-premium product lines that cater to discerning pet owners seeking the highest quality ingredients and scientifically backed formulations for their pets' specific needs, including those with sensitive stomachs, food allergies, and age-related dietary requirements.

Report Segmentation & Scope

This report segments the North American pet food market across various parameters:

- Country: United States, Canada, Mexico, Rest of North America. Growth projections vary significantly with the United States showing the highest growth. Market size in 2025 is estimated at xx Million for the US, xx Million for Canada, xx Million for Mexico, and xx Million for Rest of North America.

- Pet Food Product: Food, Other Veterinary Diets. Food dominates, but Other Veterinary Diets are showing strong growth.

- Pets: Dogs, Cats, Other Pets. Dogs and cats dominate, with other pets forming a smaller niche.

- Distribution Channel: Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, Other Channels. Supermarkets and online channels are the key players.

Each segment is analyzed individually to provide a comprehensive overview of its market size, growth potential, and competitive dynamics.

Key Drivers of North America Pet Food Market Growth

The robust growth trajectory of the North American pet food market is underpinned by a confluence of powerful and evolving factors:

- Rising Pet Ownership and Humanization: An ever-increasing number of households are welcoming pets, and the trend of "pet parenting" or the humanization of pets means owners are prioritizing their pets' health and happiness, mirroring their own dietary choices and standards.

- Premiumization and Demand for Quality: Consumers are demonstrating a growing willingness to invest in higher-quality, specialized, and often more expensive pet food options. This is driven by a desire for healthier ingredients, scientifically formulated diets, and products that offer specific health benefits.

- Exponential E-commerce Growth: The convenience, accessibility, and expanding product variety offered by online retailers have significantly boosted e-commerce sales of pet food. Subscription services and direct-to-consumer models are further enhancing this trend.

- Technological Advancements and Innovation: Continuous research and development in pet nutrition, ingredient sourcing, processing techniques, and sustainable packaging are driving product innovation and meeting evolving consumer demands for healthier, more effective, and environmentally conscious pet food options.

- Focus on Health and Wellness: A heightened awareness of pet health, preventative care, and the role of nutrition in addressing specific medical conditions or life stages is creating a strong demand for functional and therapeutic pet food products.

Challenges in the North America Pet Food Market Sector

The market faces several challenges:

- Supply Chain Disruptions: Global events and increased logistics costs.

- Ingredient Costs: Fluctuations in raw material prices affect profitability.

- Stringent Regulations: Compliance with safety and labeling regulations.

- Intense Competition: Competition from both established and emerging players.

Leading Players in the North America Pet Food Market Market

- ADM

- Schell & Kampeter Inc (Diamond Pet Foods)

- PLB International

- Clearlake Capital Group L P (Wellness Pet Company Inc)

- General Mills Inc

- Mars Incorporated

- Nestle (Purina)

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc)

- Virba

- The J M Smucker Company

Key Developments in North America Pet Food Market Sector

- July 2023: Hill's Pet Nutrition expanded its commitment to sustainable and novel ingredients by launching new products featuring MSC-certified pollock and insect protein. These formulations are specifically designed to address the dietary needs of pets with sensitive skin and stomachs, offering a novel solution for common pet health issues.

- June 2023: Mars Incorporated, a major player in the pet care industry, strategically enhanced its wet cat food portfolio in Canada with the launch of SHEBA BISTRO. This introduction aims to provide cat owners with more gourmet and varied meal options for their feline companions.

- May 2023: Nestle Purina continued its innovation in the treat category with the introduction of new Friskies Playfuls cat treats. This launch targets cat owners seeking engaging and palatable treat options that can also serve as a positive reinforcement tool during interactive play.

- [Insert New Development 1 Here]: [Brief description of the development and its impact on the market.]

- [Insert New Development 2 Here]: [Brief description of the development and its impact on the market.]

Strategic North America Pet Food Market Market Outlook

The North American pet food market is poised for continued growth, driven by increasing pet ownership, premiumization trends, and expanding e-commerce. Strategic opportunities exist for companies focusing on innovation, sustainability, and catering to niche market segments. The focus on pet health and wellness will continue to drive product development and market expansion. Companies with a strong online presence and commitment to sustainable sourcing will be well-positioned to capitalize on future growth.

North America Pet Food Market Segmentation

-

1. Pet Food Product

-

1.1. By Sub Product

-

1.1.1. Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.1.1.1. Kibbles

- 1.1.1.1.2. Other Dry Pet Food

-

1.1.1.1. By Sub Dry Pet Food

- 1.1.2. Wet Pet Food

-

1.1.1. Dry Pet Food

-

1.2. Pet Nutraceuticals/Supplements

- 1.2.1. Milk Bioactives

- 1.2.2. Omega-3 Fatty Acids

- 1.2.3. Probiotics

- 1.2.4. Proteins and Peptides

- 1.2.5. Vitamins and Minerals

- 1.2.6. Other Nutraceuticals

-

1.3. Pet Treats

- 1.3.1. Crunchy Treats

- 1.3.2. Dental Treats

- 1.3.3. Freeze-dried and Jerky Treats

- 1.3.4. Soft & Chewy Treats

- 1.3.5. Other Treats

-

1.4. Pet Veterinary Diets

- 1.4.1. Diabetes

- 1.4.2. Digestive Sensitivity

- 1.4.3. Oral Care Diets

- 1.4.4. Renal

- 1.4.5. Urinary tract disease

- 1.4.6. Other Veterinary Diets

-

1.1. By Sub Product

-

2. Pets

- 2.1. Cats

- 2.2. Dogs

- 2.3. Other Pets

-

3. Distribution Channel

- 3.1. Convenience Stores

- 3.2. Online Channel

- 3.3. Specialty Stores

- 3.4. Supermarkets/Hypermarkets

- 3.5. Other Channels

North America Pet Food Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Pet Food Market Regional Market Share

Geographic Coverage of North America Pet Food Market

North America Pet Food Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.30% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 5.1.1. By Sub Product

- 5.1.1.1. Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.1.1.1. Kibbles

- 5.1.1.1.1.2. Other Dry Pet Food

- 5.1.1.1.1. By Sub Dry Pet Food

- 5.1.1.2. Wet Pet Food

- 5.1.1.1. Dry Pet Food

- 5.1.2. Pet Nutraceuticals/Supplements

- 5.1.2.1. Milk Bioactives

- 5.1.2.2. Omega-3 Fatty Acids

- 5.1.2.3. Probiotics

- 5.1.2.4. Proteins and Peptides

- 5.1.2.5. Vitamins and Minerals

- 5.1.2.6. Other Nutraceuticals

- 5.1.3. Pet Treats

- 5.1.3.1. Crunchy Treats

- 5.1.3.2. Dental Treats

- 5.1.3.3. Freeze-dried and Jerky Treats

- 5.1.3.4. Soft & Chewy Treats

- 5.1.3.5. Other Treats

- 5.1.4. Pet Veterinary Diets

- 5.1.4.1. Diabetes

- 5.1.4.2. Digestive Sensitivity

- 5.1.4.3. Oral Care Diets

- 5.1.4.4. Renal

- 5.1.4.5. Urinary tract disease

- 5.1.4.6. Other Veterinary Diets

- 5.1.1. By Sub Product

- 5.2. Market Analysis, Insights and Forecast - by Pets

- 5.2.1. Cats

- 5.2.2. Dogs

- 5.2.3. Other Pets

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Convenience Stores

- 5.3.2. Online Channel

- 5.3.3. Specialty Stores

- 5.3.4. Supermarkets/Hypermarkets

- 5.3.5. Other Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6. North America Pet Food Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 6.1.1. By Sub Product

- 6.1.1.1. Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.1.1.1. Kibbles

- 6.1.1.1.1.2. Other Dry Pet Food

- 6.1.1.1.1. By Sub Dry Pet Food

- 6.1.1.2. Wet Pet Food

- 6.1.1.1. Dry Pet Food

- 6.1.2. Pet Nutraceuticals/Supplements

- 6.1.2.1. Milk Bioactives

- 6.1.2.2. Omega-3 Fatty Acids

- 6.1.2.3. Probiotics

- 6.1.2.4. Proteins and Peptides

- 6.1.2.5. Vitamins and Minerals

- 6.1.2.6. Other Nutraceuticals

- 6.1.3. Pet Treats

- 6.1.3.1. Crunchy Treats

- 6.1.3.2. Dental Treats

- 6.1.3.3. Freeze-dried and Jerky Treats

- 6.1.3.4. Soft & Chewy Treats

- 6.1.3.5. Other Treats

- 6.1.4. Pet Veterinary Diets

- 6.1.4.1. Diabetes

- 6.1.4.2. Digestive Sensitivity

- 6.1.4.3. Oral Care Diets

- 6.1.4.4. Renal

- 6.1.4.5. Urinary tract disease

- 6.1.4.6. Other Veterinary Diets

- 6.1.1. By Sub Product

- 6.2. Market Analysis, Insights and Forecast - by Pets

- 6.2.1. Cats

- 6.2.2. Dogs

- 6.2.3. Other Pets

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Convenience Stores

- 6.3.2. Online Channel

- 6.3.3. Specialty Stores

- 6.3.4. Supermarkets/Hypermarkets

- 6.3.5. Other Channels

- 6.1. Market Analysis, Insights and Forecast - by Pet Food Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ADM

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Schell & Kampeter Inc (Diamond Pet Foods)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 PLB International

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Clearlake Capital Group L P (Wellness Pet Company Inc )

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 General Mills Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mars Incorporated

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nestle (Purina)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Colgate-Palmolive Company (Hill's Pet Nutrition Inc )

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Virba

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 The J M Smucker Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 ADM

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Pet Food Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Pet Food Market Share (%) by Company 2025

List of Tables

- Table 1: North America Pet Food Market Revenue Million Forecast, by Pet Food Product 2020 & 2033

- Table 2: North America Pet Food Market Revenue Million Forecast, by Pets 2020 & 2033

- Table 3: North America Pet Food Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: North America Pet Food Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: North America Pet Food Market Revenue Million Forecast, by Pet Food Product 2020 & 2033

- Table 6: North America Pet Food Market Revenue Million Forecast, by Pets 2020 & 2033

- Table 7: North America Pet Food Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 8: North America Pet Food Market Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States North America Pet Food Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Pet Food Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Pet Food Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Pet Food Market?

The projected CAGR is approximately 4.30%.

2. Which companies are prominent players in the North America Pet Food Market?

Key companies in the market include ADM, Schell & Kampeter Inc (Diamond Pet Foods), PLB International, Clearlake Capital Group L P (Wellness Pet Company Inc ), General Mills Inc, Mars Incorporated, Nestle (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc ), Virba, The J M Smucker Company.

3. What are the main segments of the North America Pet Food Market?

The market segments include Pet Food Product, Pets, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Meat; Initiatives By the Key Players; Focus on Animal nutrition and Health.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Shift Toward Vegan- Based Diet; Changing Raw Material Prices and Strict Government Rules to Restrict Market Growth.

8. Can you provide examples of recent developments in the market?

July 2023: Hill's Pet Nutrition introduced its new MSC (Marine Stewardship Council) certified pollock and insect protein products for pets with sensitive stomachs and skin lines. They contain vitamins, omega-3 fatty acids, and antioxidants.June 2023: Mars Incorporated launched its premium cat brand SHEBA in Canada, offering cat parents wet formulas through its SHEBA BISTRO line.May 2023: Nestle Purina launched new cat treats under the Friskies "Friskies Playfuls - treats" brand. These treats are round in shape and are available in chicken and liver and salmon and shrimp flavors for adult cats.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Pet Food Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Pet Food Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Pet Food Market?

To stay informed about further developments, trends, and reports in the North America Pet Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence