Key Insights

The global market for Implantable Collamer Lenses (ICLs) is poised for substantial growth, projected to reach $11.3 billion in 2025 with an impressive Compound Annual Growth Rate (CAGR) of 11.35% during the forecast period of 2025-2033. This robust expansion is primarily fueled by a growing awareness of advanced vision correction alternatives to traditional spectacles and contact lenses, coupled with an increasing incidence of refractive errors like myopia, hyperopia, and astigmatism. The rising adoption of ICLs in hospitals and specialized ophthalmology clinics, driven by their superior visual outcomes, reduced complications, and patient satisfaction, forms a significant catalyst for this market's ascent. Furthermore, technological advancements leading to improved lens designs, such as specialized aspherical lenses offering enhanced visual clarity and reduced aberrations, are contributing to higher demand. The market is also benefiting from an aging global population, which often experiences age-related vision issues that ICLs can effectively address.

ICL Implantable Lens Market Size (In Billion)

The competitive landscape is characterized by the presence of key players such as Alcon, Abbott, and Carl Zeiss, who are actively involved in research and development to introduce innovative ICL solutions. These companies are focusing on expanding their product portfolios, enhancing surgical techniques, and broadening their geographical reach to tap into emerging markets. While the market demonstrates strong growth potential, certain factors could influence its trajectory. High procedure costs and the need for specialized surgical expertise, though diminishing with advancements, remain considerations. However, the escalating demand for high-quality vision correction, coupled with increased disposable incomes in developing economies and supportive healthcare infrastructure, is expected to outweigh these restraints, propelling the ICL implantable lens market to new heights throughout the forecast period. The market's segmentation by application into hospitals and ophthalmology clinics, and by type into spherical and aspherical lenses, highlights the diverse needs catered to by this evolving segment of ophthalmic surgery.

ICL Implantable Lens Company Market Share

This in-depth market research report provides a detailed examination of the global ICL (Implantable Collamer Lens) market, offering insights into market size, growth drivers, segmentation, competitive dynamics, and future outlook. The report covers the study period from 2019 to 2033, with the base year and estimated year both being 2025, and the forecast period extending from 2025 to 2033. The historical period encompasses 2019 to 2024. We project the global ICL implantable lens market to reach approximately 6 billion USD by 2025, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period, reaching an estimated xx billion USD by 2033.

ICL Implantable Lens Market Structure & Competitive Dynamics

The global ICL implantable lens market exhibits a moderately concentrated structure, dominated by a few key players while also featuring emerging innovators. Market concentration is influenced by high research and development investments, stringent regulatory approvals, and the proprietary nature of advanced lens technologies. The innovation ecosystem thrives on continuous improvements in biomaterials, optical designs, and surgical techniques, driven by companies like Alcon, Abbott, and Carl Zeiss. Regulatory frameworks, particularly those of the FDA and EMA, play a crucial role in market entry and product lifecycle management, influencing the speed and scope of innovation. Product substitutes, such as traditional intraocular lenses (IOLs) and refractive surgeries like LASIK and PRK, present a competitive landscape, although ICLs offer distinct advantages for specific patient profiles, including those with high myopia or astigmatism not suitable for other procedures. End-user trends are shifting towards minimally invasive procedures, faster visual recovery, and improved quality of vision, directly impacting the demand for advanced ICLs. Merger and acquisition (M&A) activities, estimated to be in the range of several hundred million USD, are strategically employed by larger players to acquire innovative technologies, expand market reach, and consolidate their positions. For instance, recent M&A deals have focused on acquiring companies with novel toric ICL designs and advanced biomaterial coatings, contributing to a market value estimated at 7 billion USD in 2024.

ICL Implantable Lens Industry Trends & Insights

The ICL implantable lens industry is experiencing robust growth, propelled by a confluence of technological advancements, evolving consumer preferences, and a growing prevalence of refractive errors worldwide. Market growth drivers include the increasing demand for vision correction solutions beyond traditional eyeglasses and contact lenses, particularly among younger demographics seeking lifestyle improvements and the ability to reduce or eliminate dependence on corrective eyewear. The rising incidence of high myopia and astigmatism, conditions where ICLs demonstrate significant efficacy, further fuels market expansion. Technological disruptions are at the forefront, with continuous innovation in lens design, material science, and surgical techniques. Aspherical ICL designs are gaining traction due to their ability to provide sharper, more natural vision, reducing spherical aberrations. Furthermore, advancements in hydrophobic acrylic materials and anti-reflective coatings are enhancing biocompatibility and minimizing posterior capsule opacification, leading to improved patient outcomes and increased adoption. Consumer preferences are increasingly leaning towards elective vision correction procedures that offer predictable results and a high degree of visual satisfaction. The shift towards patient-centric care and the desire for a higher quality of life are key motivators for individuals seeking ICL implantation. The competitive dynamics within the industry are characterized by a strong emphasis on clinical evidence, surgeon training, and post-operative support to build patient and physician confidence. Market penetration for ICLs, while still lower than traditional IOLs, is steadily increasing, particularly in developed markets where disposable incomes are higher and access to advanced medical technologies is widespread. The estimated market penetration stands at xx% in developed regions, with significant growth potential in emerging economies. The overall market is projected to witness a CAGR of xx% over the forecast period, reaching an estimated value of 12 billion USD by 2033.

Dominant Markets & Segments in ICL Implantable Lens

The ICL implantable lens market is currently dominated by Ophthalmology Clinics as the primary application segment, driven by their specialized focus on eye care and surgical procedures. These clinics offer a concentrated patient pool seeking advanced refractive correction solutions. Within the Types segmentation, Aspherical ICLs are witnessing a significant surge in demand, outperforming spherical counterparts due to their superior optical performance and ability to correct visual aberrations, leading to enhanced visual acuity and quality.

Key Drivers for Dominance in Ophthalmology Clinics:

- Specialized Expertise: Ophthalmologists in these clinics possess the specialized knowledge and surgical skills required for ICL implantation, fostering patient trust and procedural success.

- Advanced Infrastructure: Clinics are equipped with state-of-the-art diagnostic and surgical equipment, crucial for accurate patient assessment and precise ICL placement.

- Patient Education & Counseling: Dedicated patient counseling services within clinics effectively address patient concerns, explain the benefits of ICLs, and manage expectations, leading to higher conversion rates.

- Referral Networks: Strong referral networks from optometrists and general practitioners funnel patients requiring advanced refractive correction directly to these specialized centers.

Dominance Analysis of Aspherical ICLs:

Aspherical ICLs have emerged as the preferred choice for a growing segment of the patient population. Their advanced optical design minimizes spherical aberrations, which are inherent in the human eye and conventional spherical lenses. This reduction in aberrations translates to:

- Sharper Visual Acuity: Patients experience clearer vision, especially in low-light conditions.

- Improved Contrast Sensitivity: The ability to discern subtle differences in shades and textures is enhanced.

- Reduced Glare and Halos: A significant benefit for patients who experience discomfort with traditional corrective lenses or procedures.

The increasing awareness of these benefits among both patients and ophthalmic surgeons, coupled with advancements in manufacturing that have made aspherical ICLs more accessible, is driving their market dominance. The segment is projected to contribute over 70% to the overall ICL market revenue in the coming years. The global market size for ICLs in ophthalmology clinics is estimated to be around 5 billion USD, with the aspherical segment accounting for approximately 3.5 billion USD in 2025.

ICL Implantable Lens Product Innovations

Recent product innovations in the ICL implantable lens market are focused on enhancing patient outcomes and expanding the range of treatable refractive errors. Innovations include the development of novel toric ICLs with improved astigmatism correction capabilities and enhanced rotational stability, minimizing the need for recalibration. Furthermore, advancements in biocompatible materials and anti-reflective coatings are reducing the risk of inflammation and posterior capsular opacification, leading to longer-lasting visual clarity. The introduction of extended depth of focus (EDOF) ICLs is also a significant development, offering a wider range of clear vision from near to far, further reducing the reliance on reading glasses. These technological advancements provide a significant competitive advantage to manufacturers, driving market adoption and patient satisfaction.

Report Segmentation & Scope

This report segments the ICL implantable lens market into key application areas and product types.

Application Segments:

- Hospitals: This segment encompasses ICL procedures performed within hospital settings, often catering to more complex cases or patients with co-existing medical conditions. The market size for hospitals is estimated at 1 billion USD in 2025, with a projected CAGR of xx%.

- Ophthalmology Clinics: As detailed previously, this segment represents the largest share, driven by specialized refractive surgery practices. The market size for ophthalmology clinics is estimated at 5 billion USD in 2025, with a projected CAGR of xx%.

Type Segments:

- Spherical ICLs: These lenses are designed to correct spherical refractive errors. The market size for spherical ICLs is estimated at 1.5 billion USD in 2025, with a projected CAGR of xx%.

- Aspherical ICLs: These lenses offer enhanced optical quality by minimizing aberrations. The market size for aspherical ICLs is estimated at 3.5 billion USD in 2025, with a projected CAGR of xx%.

The scope of this report extends to analyzing the market dynamics, competitive landscape, and growth prospects for each of these segments across the defined study and forecast periods.

Key Drivers of ICL Implantable Lens Growth

Several key factors are driving the growth of the ICL implantable lens market.

- Rising Prevalence of Refractive Errors: The global increase in myopia, hyperopia, and astigmatism creates a larger addressable patient pool.

- Technological Advancements: Continuous innovation in lens design, materials, and surgical techniques improves efficacy and patient satisfaction.

- Growing Demand for Premium Vision Correction: Patients are increasingly seeking solutions that offer independence from glasses and contact lenses with superior visual quality.

- Aging Population: An aging demographic contributes to a higher incidence of cataracts, for which ICLs can be a secondary refractive solution.

- Favorable Reimbursement Policies: In certain regions, increasing coverage for advanced vision correction procedures is boosting adoption.

Challenges in the ICL Implantable Lens Sector

Despite the positive growth trajectory, the ICL implantable lens sector faces several challenges:

- High Cost of Procedures: The premium pricing of ICLs can be a barrier for a significant portion of the population, particularly in price-sensitive markets.

- Stringent Regulatory Approvals: Obtaining regulatory clearance for new ICL models and technologies can be a lengthy and expensive process, slowing down market entry.

- Limited Surgeon Training and Awareness: A consistent need for comprehensive training programs for surgeons to ensure optimal implantation techniques and patient outcomes.

- Availability of Substitutes: Competition from established refractive surgery procedures like LASIK and PRK, as well as traditional eyewear.

- Patient-Specific Suitability: Not all patients are suitable candidates for ICL implantation, requiring careful screening and selection.

Leading Players in the ICL Implantable Lens Market

- Aurolab

- Alcon

- Abbott

- Hoya Surgical Optics

- Bausch+Lomb

- Carl Zeiss

- Aaren Scientific

- Ophtec

- Rayner

- Lenstec

- HumanOptics

- Biotech Visioncare

- Omni Lens

- Eagle Optics

- SIFI Medtech

- Wuxi Vision Pro

Key Developments in ICL Implantable Lens Sector

- 2023: Launch of new-generation toric ICLs with enhanced rotational stability and improved astigmatism correction by leading manufacturers.

- 2022: Significant advancements in biomaterial research leading to more biocompatible and inflammation-resistant ICL designs.

- 2021: Introduction of extended depth of focus (EDOF) ICLs, expanding the range of clear vision for patients.

- 2020: Increased focus on minimally invasive surgical techniques for ICL implantation, leading to faster patient recovery times.

- 2019: Strategic partnerships formed between ICL manufacturers and key opinion leaders to drive surgeon education and adoption.

Strategic ICL Implantable Lens Market Outlook

The strategic outlook for the ICL implantable lens market is highly promising, driven by continued technological innovation and a growing global demand for premium vision correction solutions. The market is poised for substantial expansion as manufacturers invest in developing lenses with enhanced optical performance, improved biocompatibility, and broader applicability for diverse patient needs. The increasing awareness and acceptance of ICLs as a viable alternative to glasses and contact lenses, coupled with the potential for significant improvements in quality of life, will continue to fuel market growth. Emerging markets represent a significant untapped potential, with opportunities for strategic market entry and partnerships to increase accessibility and adoption. Furthermore, the development of personalized ICL solutions tailored to individual patient profiles is expected to be a key growth accelerator in the coming years.

ICL Implantable Lens Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Ophthalmology Clinics

-

2. Types

- 2.1. Spherical

- 2.2. Aspherical

ICL Implantable Lens Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

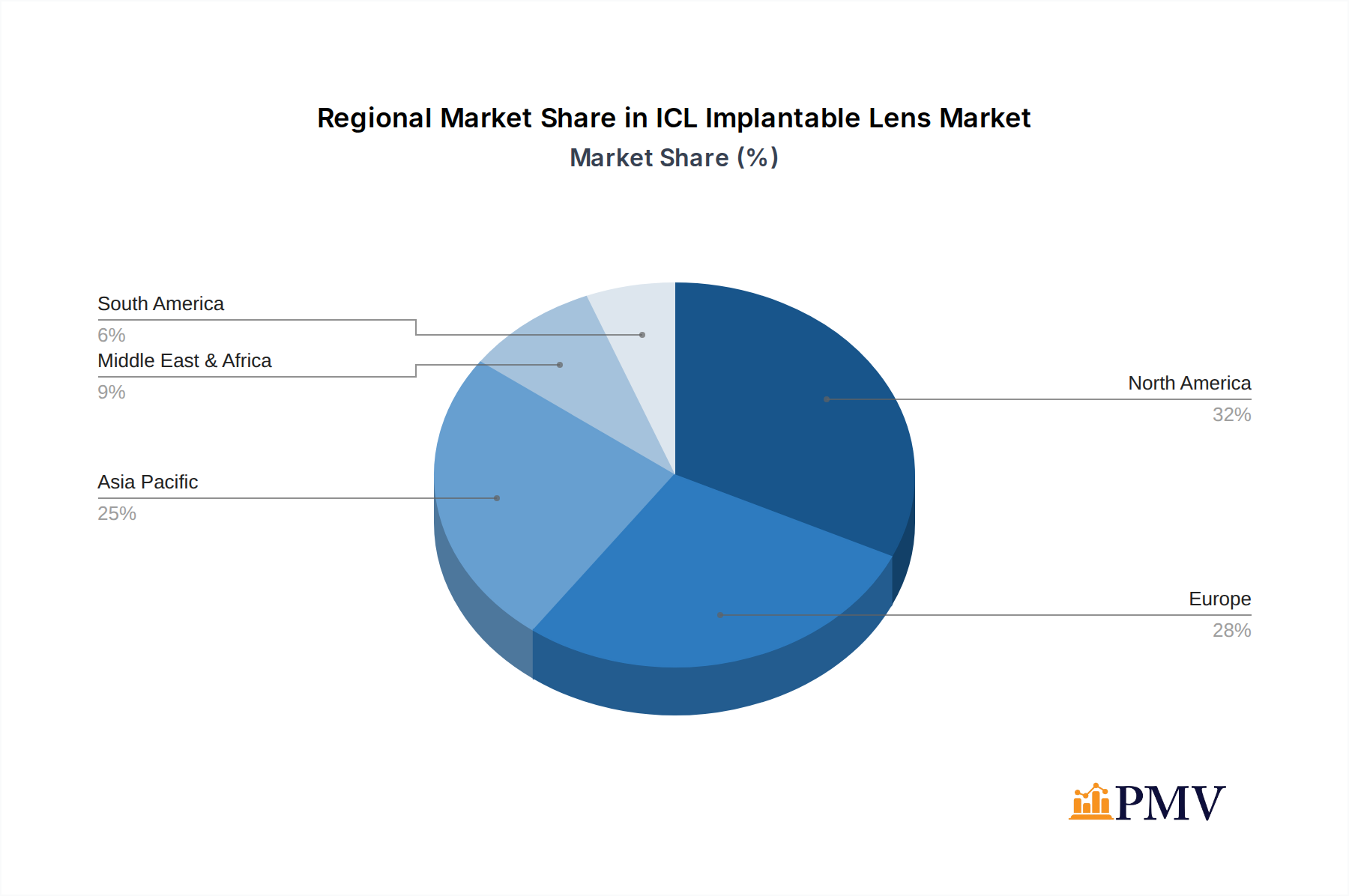

ICL Implantable Lens Regional Market Share

Geographic Coverage of ICL Implantable Lens

ICL Implantable Lens REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Ophthalmology Clinics

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Spherical

- 5.2.2. Aspherical

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global ICL Implantable Lens Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Ophthalmology Clinics

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Spherical

- 6.2.2. Aspherical

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America ICL Implantable Lens Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Ophthalmology Clinics

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Spherical

- 7.2.2. Aspherical

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America ICL Implantable Lens Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Ophthalmology Clinics

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Spherical

- 8.2.2. Aspherical

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe ICL Implantable Lens Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Ophthalmology Clinics

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Spherical

- 9.2.2. Aspherical

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa ICL Implantable Lens Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Ophthalmology Clinics

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Spherical

- 10.2.2. Aspherical

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific ICL Implantable Lens Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Ophthalmology Clinics

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Spherical

- 11.2.2. Aspherical

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Aurolab

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Alcon

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Abbott

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hoya Surgical Optics

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Bausch+Lomb

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Carl Zeiss

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Aaren Scientific

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Ophtec

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Rayner

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Lenstec

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 HumanOptics

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Biotech Visioncare

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Omni Lens

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Eagle Optics

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 SIFI Medtech

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Wuxi Vision Pro

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Aurolab

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global ICL Implantable Lens Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America ICL Implantable Lens Revenue (billion), by Application 2025 & 2033

- Figure 3: North America ICL Implantable Lens Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America ICL Implantable Lens Revenue (billion), by Types 2025 & 2033

- Figure 5: North America ICL Implantable Lens Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America ICL Implantable Lens Revenue (billion), by Country 2025 & 2033

- Figure 7: North America ICL Implantable Lens Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America ICL Implantable Lens Revenue (billion), by Application 2025 & 2033

- Figure 9: South America ICL Implantable Lens Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America ICL Implantable Lens Revenue (billion), by Types 2025 & 2033

- Figure 11: South America ICL Implantable Lens Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America ICL Implantable Lens Revenue (billion), by Country 2025 & 2033

- Figure 13: South America ICL Implantable Lens Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe ICL Implantable Lens Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe ICL Implantable Lens Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe ICL Implantable Lens Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe ICL Implantable Lens Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe ICL Implantable Lens Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe ICL Implantable Lens Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa ICL Implantable Lens Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa ICL Implantable Lens Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa ICL Implantable Lens Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa ICL Implantable Lens Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa ICL Implantable Lens Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa ICL Implantable Lens Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific ICL Implantable Lens Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific ICL Implantable Lens Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific ICL Implantable Lens Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific ICL Implantable Lens Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific ICL Implantable Lens Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific ICL Implantable Lens Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global ICL Implantable Lens Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global ICL Implantable Lens Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global ICL Implantable Lens Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global ICL Implantable Lens Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global ICL Implantable Lens Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global ICL Implantable Lens Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global ICL Implantable Lens Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global ICL Implantable Lens Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global ICL Implantable Lens Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global ICL Implantable Lens Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global ICL Implantable Lens Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global ICL Implantable Lens Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global ICL Implantable Lens Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global ICL Implantable Lens Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global ICL Implantable Lens Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global ICL Implantable Lens Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global ICL Implantable Lens Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global ICL Implantable Lens Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific ICL Implantable Lens Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the ICL Implantable Lens?

The projected CAGR is approximately 11.35%.

2. Which companies are prominent players in the ICL Implantable Lens?

Key companies in the market include Aurolab, Alcon, Abbott, Hoya Surgical Optics, Bausch+Lomb, Carl Zeiss, Aaren Scientific, Ophtec, Rayner, Lenstec, HumanOptics, Biotech Visioncare, Omni Lens, Eagle Optics, SIFI Medtech, Wuxi Vision Pro.

3. What are the main segments of the ICL Implantable Lens?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.3 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "ICL Implantable Lens," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the ICL Implantable Lens report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the ICL Implantable Lens?

To stay informed about further developments, trends, and reports in the ICL Implantable Lens, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence