Key Insights

The European electric vehicle (EV) battery market is experiencing robust growth, driven by stringent emission regulations, increasing EV adoption, and supportive government policies. The market, valued at approximately €XX million in 2025 (assuming a logical extrapolation from the provided CAGR of 24.50% and a base year of 2025), is projected to expand significantly, reaching €YY million by 2033. This substantial growth is fueled by the rising demand for various EV types, including passenger cars, light commercial vehicles (LCVs), and buses, across major European nations like Germany, France, and the UK. The market's segmentation reveals strong preferences for specific battery chemistries (NMC and NCA are likely leading), forms (prismatic and pouch cells dominating), and capacities (concentrated in the 40-80 kWh range). The rapid expansion of domestic battery manufacturing capacity, driven by companies like Northvolt and others, is further boosting the market. However, challenges remain, including the potential for supply chain disruptions concerning crucial raw materials like lithium, cobalt, and nickel, and the need for continued investment in battery recycling infrastructure to address environmental concerns.

The competitive landscape is highly dynamic, with a mix of established international players like CATL, LG Energy Solution, and Panasonic, alongside emerging European manufacturers such as Northvolt. These companies are investing heavily in R&D to enhance battery technology, focusing on improvements in energy density, lifespan, and charging speed. The strategic partnerships and joint ventures being formed between battery manufacturers and automotive OEMs underscore the industry's focus on securing supply chains and accelerating the transition to electric mobility. The interplay of technological advancements, governmental incentives, and the growing consumer demand for EVs will continue to shape the future of the European EV battery market. This presents lucrative opportunities for innovative companies willing to navigate the complexities of this fast-evolving industry.

Europe Electric Vehicle Battery Industry: 2019-2033 Market Analysis & Forecast

This comprehensive report provides an in-depth analysis of the European electric vehicle (EV) battery industry, covering the period from 2019 to 2033. It offers crucial insights into market dynamics, competitive landscapes, technological advancements, and future growth prospects, empowering businesses to make informed strategic decisions. The report utilizes a robust data-driven approach, incorporating market sizing, segmentation, and forecasting to present a clear picture of the industry’s evolution. Key players such as SAIC Volkswagen Power Battery Co Ltd, CATL, and NorthVolt AB are analyzed in detail.

Europe Electric Vehicle Battery Industry Market Structure & Competitive Dynamics

The European EV battery market is characterized by a dynamic interplay of established players and emerging innovators. Market concentration is moderate, with a few dominant players holding significant market share, but a growing number of smaller companies competing fiercely. Innovation ecosystems are thriving, driven by substantial R&D investments and collaborative partnerships between battery manufacturers, automotive OEMs, and research institutions. Stringent regulatory frameworks, including those focused on sustainability and safety, significantly influence industry strategies. Product substitutes, such as fuel cells, are present but face challenges in terms of cost and infrastructure. End-user trends are shifting towards higher energy density, faster charging, and improved safety, shaping the development of next-generation batteries. M&A activities are frequent, reflecting the industry's consolidation and efforts to secure access to resources and technology.

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2025, while the remaining xx% is distributed among smaller players.

- M&A Activity: The total value of M&A deals in the European EV battery industry between 2019 and 2024 reached approximately xx Million. Major deals included (examples only, data needed for actual deals).

- Innovation Ecosystems: Strong collaborations between universities, research centers, and companies drive innovation in battery chemistry, manufacturing processes, and recycling technologies.

Europe Electric Vehicle Battery Industry Industry Trends & Insights

The European EV battery industry is experiencing exponential growth, propelled by several key factors. The increasing adoption of electric vehicles, driven by stringent emission regulations and growing environmental awareness, is a primary growth driver. Technological advancements, such as improvements in battery chemistry and manufacturing processes, are leading to higher energy densities, longer lifespans, and reduced costs. Consumer preferences are shifting towards EVs, prioritizing factors such as range, charging time, and overall vehicle performance. The competitive landscape is intensifying, with companies investing heavily in R&D and capacity expansion to meet the growing demand. The Compound Annual Growth Rate (CAGR) for the European EV battery market is estimated to be xx% during the forecast period (2025-2033). Market penetration of EVs is also expected to increase significantly, reaching an estimated xx% of total vehicle sales by 2033. This growth will be driven by increasing government support for EV adoption, improvements in charging infrastructure, and decreasing battery costs.

Dominant Markets & Segments in Europe Electric Vehicle Battery Industry

The passenger car segment dominates the European EV battery market, accounting for approximately xx% of total demand in 2025. Germany and France are leading countries in terms of both EV adoption and battery manufacturing. The NMC battery chemistry holds the largest market share, followed by LFP and NCA chemistries. The demand for batteries with capacities above 80 kWh is expected to grow rapidly as higher-range EVs gain popularity.

Key Drivers for Dominant Segments:

- Economic Policies: Government subsidies and tax incentives for EV purchases significantly influence market growth.

- Infrastructure: Expansion of charging infrastructure is crucial for supporting wider EV adoption.

- Technological Advancements: Continuous improvements in battery technology, leading to enhanced performance and lower costs.

Dominance Analysis: Germany's dominance is partly due to its strong automotive industry and substantial investments in battery manufacturing. France is also a significant player, with its government actively supporting the development of its domestic battery industry.

Europe Electric Vehicle Battery Industry Product Innovations

Recent innovations in the European EV battery industry focus on improving energy density, reducing costs, and enhancing safety. This includes advancements in battery chemistry (e.g., solid-state batteries), improvements in manufacturing processes (e.g., cell-to-pack technology), and the development of more sustainable battery materials. These innovations are enhancing the performance and affordability of EV batteries, thus accelerating their market penetration. The integration of advanced battery management systems (BMS) further enhances safety and extends battery lifespan.

Report Segmentation & Scope

This report segments the European EV battery market across various parameters:

- Material Type: Cobalt, Lithium, Manganese, Natural Graphite, Nickel, Other Materials. Growth is expected to be driven by the increasing demand for lithium and nickel.

- Country: France, Germany, Hungary, Italy, Poland, Sweden, UK, Rest-of-Europe. Germany and France are projected to remain the leading markets.

- Body Type: Bus, LCV, M&HDT, Passenger Car. Passenger cars will continue to dominate.

- Battery Chemistry: LFP, NCA, NCM, NMC, Others. NMC and LFP are expected to maintain significant market shares.

- Capacity: Less than 15 kWh, 15 kWh to 40 kWh, 40 kWh to 80 kWh, Above 80 kWh. Demand for higher capacity batteries will rise.

- Battery Form: Cylindrical, Pouch, Prismatic. Prismatic cells are gaining traction due to their high energy density and cost-effectiveness.

- Method: Laser, Wire.

- Component: Anode, Cathode, Electrolyte, Separator.

- Propulsion Type: BEV, PHEV. BEVs will continue to be the dominant propulsion type.

Each segment's growth projection, market size, and competitive dynamics are thoroughly analyzed within the full report.

Key Drivers of Europe Electric Vehicle Battery Industry Growth

The European EV battery industry's growth is fueled by a combination of factors. Stringent environmental regulations aimed at reducing carbon emissions are driving the adoption of EVs. Government incentives and subsidies are stimulating both demand and domestic battery production. Technological advancements, including improved battery chemistries and manufacturing processes, are leading to greater energy density, longer lifespan, and lower costs. Increasing consumer demand for EVs, due to factors like improved performance and range, is also a significant growth driver.

Challenges in the Europe Electric Vehicle Battery Industry Sector

The industry faces challenges, including securing a stable supply of raw materials, especially lithium and cobalt. Geopolitical risks and potential supply chain disruptions pose risks. The high initial cost of EV batteries remains a barrier to wider adoption. Furthermore, concerns about battery safety and recyclability need to be addressed. Competition is fierce, requiring companies to constantly innovate and improve their products and manufacturing processes to maintain market share. These challenges result in an estimated xx Million loss in revenue annually (predicted figure, further data needed).

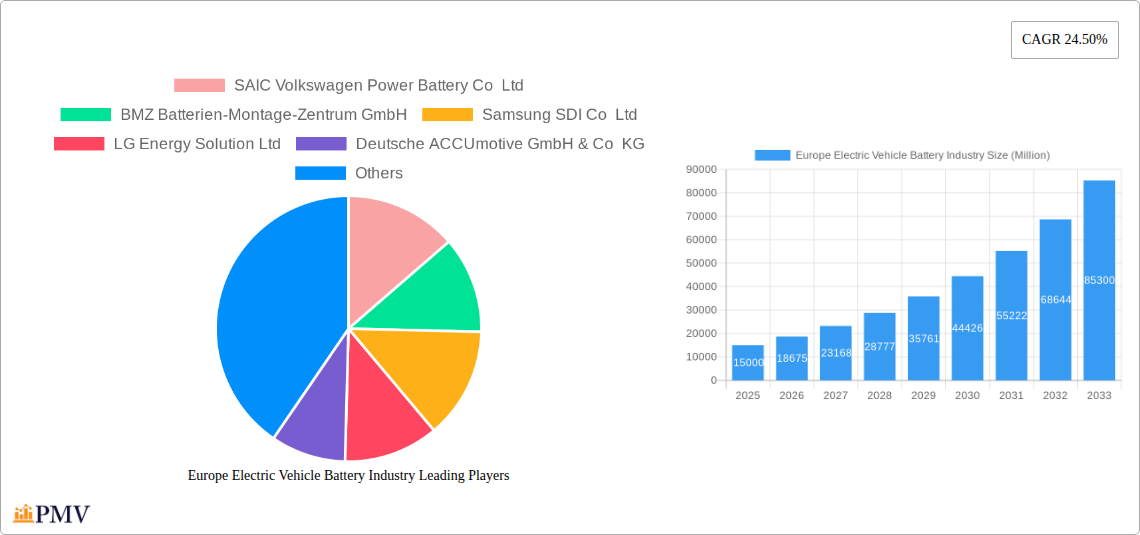

Leading Players in the Europe Electric Vehicle Battery Industry Market

- SAIC Volkswagen Power Battery Co Ltd

- BMZ Batterien-Montage-Zentrum GmbH

- Samsung SDI Co Ltd

- LG Energy Solution Ltd

- Deutsche ACCUmotive GmbH & Co KG

- TOSHIBA Corp

- Contemporary Amperex Technology Co Ltd (CATL)

- BYD Company Ltd

- Groupe Renault

- SK Innovation Co Ltd

- Ningbo Tuopu Group Co Ltd

- Panasonic Holdings Corporation

- NorthVolt AB

- SVOLT Energy Technology Co Ltd (SVOLT)

Key Developments in Europe Electric Vehicle Battery Industry Sector

- June 2023: IMCO invests USD 400 Million in Northvolt AB, supporting its expansion and sustainable supply chain.

- June 2023: CATL launches Qiji Energy, a battery swap solution for heavy-duty trucks, utilizing 3rd-generation LFP battery chemistry with NP and CTP technologies.

- February 2023: SK nexilis signs a five-year deal to supply copper foils to Northvolt, with expected sales reaching KRW 1.4 trillion.

These developments signal a continued push towards sustainable and innovative battery technologies, impacting market competitiveness and growth.

Strategic Europe Electric Vehicle Battery Industry Market Outlook

The European EV battery market is poised for significant growth in the coming years, driven by increasing EV adoption, technological advancements, and supportive government policies. Strategic opportunities exist for companies to invest in R&D, expand manufacturing capacity, and secure access to raw materials. Focus on sustainable and environmentally friendly battery technologies will be crucial for long-term success. The development of advanced battery recycling technologies will also be vital for reducing environmental impact and ensuring resource security. Companies that can effectively navigate the regulatory landscape and meet the evolving needs of consumers will be best positioned to capture market share in this rapidly expanding sector.

Europe Electric Vehicle Battery Industry Segmentation

-

1. Body Type

- 1.1. Bus

- 1.2. LCV

- 1.3. M&HDT

- 1.4. Passenger Car

-

2. Propulsion Type

- 2.1. BEV

- 2.2. PHEV

-

3. Battery Chemistry

- 3.1. LFP

- 3.2. NCA

- 3.3. NCM

- 3.4. NMC

- 3.5. Others

-

4. Capacity

- 4.1. 15 kWh to 40 kWh

- 4.2. 40 kWh to 80 kWh

- 4.3. Above 80 kWh

- 4.4. Less than 15 kWh

-

5. Battery Form

- 5.1. Cylindrical

- 5.2. Pouch

- 5.3. Prismatic

-

6. Method

- 6.1. Laser

- 6.2. Wire

-

7. Component

- 7.1. Anode

- 7.2. Cathode

- 7.3. Electrolyte

- 7.4. Separator

-

8. Material Type

- 8.1. Cobalt

- 8.2. Lithium

- 8.3. Manganese

- 8.4. Natural Graphite

- 8.5. Nickel

- 8.6. Other Materials

Europe Electric Vehicle Battery Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Electric Vehicle Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 24.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Exponential Increase in Automotive Sector

- 3.3. Market Restrains

- 3.3.1. Digitization of R&D Operations in Automotive Sector

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Body Type

- 5.1.1. Bus

- 5.1.2. LCV

- 5.1.3. M&HDT

- 5.1.4. Passenger Car

- 5.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.2.1. BEV

- 5.2.2. PHEV

- 5.3. Market Analysis, Insights and Forecast - by Battery Chemistry

- 5.3.1. LFP

- 5.3.2. NCA

- 5.3.3. NCM

- 5.3.4. NMC

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Capacity

- 5.4.1. 15 kWh to 40 kWh

- 5.4.2. 40 kWh to 80 kWh

- 5.4.3. Above 80 kWh

- 5.4.4. Less than 15 kWh

- 5.5. Market Analysis, Insights and Forecast - by Battery Form

- 5.5.1. Cylindrical

- 5.5.2. Pouch

- 5.5.3. Prismatic

- 5.6. Market Analysis, Insights and Forecast - by Method

- 5.6.1. Laser

- 5.6.2. Wire

- 5.7. Market Analysis, Insights and Forecast - by Component

- 5.7.1. Anode

- 5.7.2. Cathode

- 5.7.3. Electrolyte

- 5.7.4. Separator

- 5.8. Market Analysis, Insights and Forecast - by Material Type

- 5.8.1. Cobalt

- 5.8.2. Lithium

- 5.8.3. Manganese

- 5.8.4. Natural Graphite

- 5.8.5. Nickel

- 5.8.6. Other Materials

- 5.9. Market Analysis, Insights and Forecast - by Region

- 5.9.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Body Type

- 6. Germany Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Electric Vehicle Battery Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 SAIC Volkswagen Power Battery Co Ltd

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 BMZ Batterien-Montage-Zentrum GmbH

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Samsung SDI Co Ltd

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 LG Energy Solution Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Deutsche ACCUmotive GmbH & Co KG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 TOSHIBA Corp

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Contemporary Amperex Technology Co Ltd (CATL)

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 BYD Company Ltd

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Groupe Renault

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 SK Innovation Co Ltd

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Ningbo Tuopu Group Co Ltd

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Panasonic Holdings Corporation

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 NorthVolt AB

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 SVOLT Energy Technology Co Ltd (SVOLT)

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.1 SAIC Volkswagen Power Battery Co Ltd

List of Figures

- Figure 1: Europe Electric Vehicle Battery Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Electric Vehicle Battery Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Body Type 2019 & 2032

- Table 3: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Propulsion Type 2019 & 2032

- Table 4: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Battery Chemistry 2019 & 2032

- Table 5: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Capacity 2019 & 2032

- Table 6: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Battery Form 2019 & 2032

- Table 7: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Method 2019 & 2032

- Table 8: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 9: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 10: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 11: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Germany Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: France Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Italy Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: United Kingdom Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Netherlands Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Sweden Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of Europe Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Body Type 2019 & 2032

- Table 20: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Propulsion Type 2019 & 2032

- Table 21: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Battery Chemistry 2019 & 2032

- Table 22: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Capacity 2019 & 2032

- Table 23: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Battery Form 2019 & 2032

- Table 24: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Method 2019 & 2032

- Table 25: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 26: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 27: Europe Electric Vehicle Battery Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: United Kingdom Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Germany Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: France Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Italy Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Spain Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Netherlands Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Belgium Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Sweden Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Norway Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Poland Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Denmark Europe Electric Vehicle Battery Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Electric Vehicle Battery Industry?

The projected CAGR is approximately 24.50%.

2. Which companies are prominent players in the Europe Electric Vehicle Battery Industry?

Key companies in the market include SAIC Volkswagen Power Battery Co Ltd, BMZ Batterien-Montage-Zentrum GmbH, Samsung SDI Co Ltd, LG Energy Solution Ltd, Deutsche ACCUmotive GmbH & Co KG, TOSHIBA Corp, Contemporary Amperex Technology Co Ltd (CATL), BYD Company Ltd, Groupe Renault, SK Innovation Co Ltd, Ningbo Tuopu Group Co Ltd, Panasonic Holdings Corporation, NorthVolt AB, SVOLT Energy Technology Co Ltd (SVOLT).

3. What are the main segments of the Europe Electric Vehicle Battery Industry?

The market segments include Body Type, Propulsion Type, Battery Chemistry, Capacity, Battery Form, Method, Component, Material Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Exponential Increase in Automotive Sector.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Digitization of R&D Operations in Automotive Sector.

8. Can you provide examples of recent developments in the market?

June 2023: The Investment Management Corporation of Ontario (IMCO) announced that it is investing USD 400 million in Northvolt AB. The funds will enable Northvolt's planned expansion, aligned with IMCO and the company's commitment to a deeply sustainable battery supply chain.June 2023: CATL announced that it launched Qiji Energy, a battery swap solution for heavy-duty trucks. The solution consists of Qiji Swapping Electric Blocks, Qiji Battery Swap Station, and Qiji Cloud Platform. Based on the CATL’s 3rd-generation LFP battery chemistry, Qiji Swapping Electric Blocks adopt the innovative NP (Non Propagation) technology and CTP (cell-to-pack) technology, striking a balance between safety and usage costs. Qiji Battery Swap Station enables one-stop swapping for different truck models and brands.February 2023: SK nexilis to supply copper foils to Northvolt. The deal is valid for five years from 2024, and the sales under the contract are expected to reach KRW 1.4 trillion.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Electric Vehicle Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Electric Vehicle Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Electric Vehicle Battery Industry?

To stay informed about further developments, trends, and reports in the Europe Electric Vehicle Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence