Key Insights

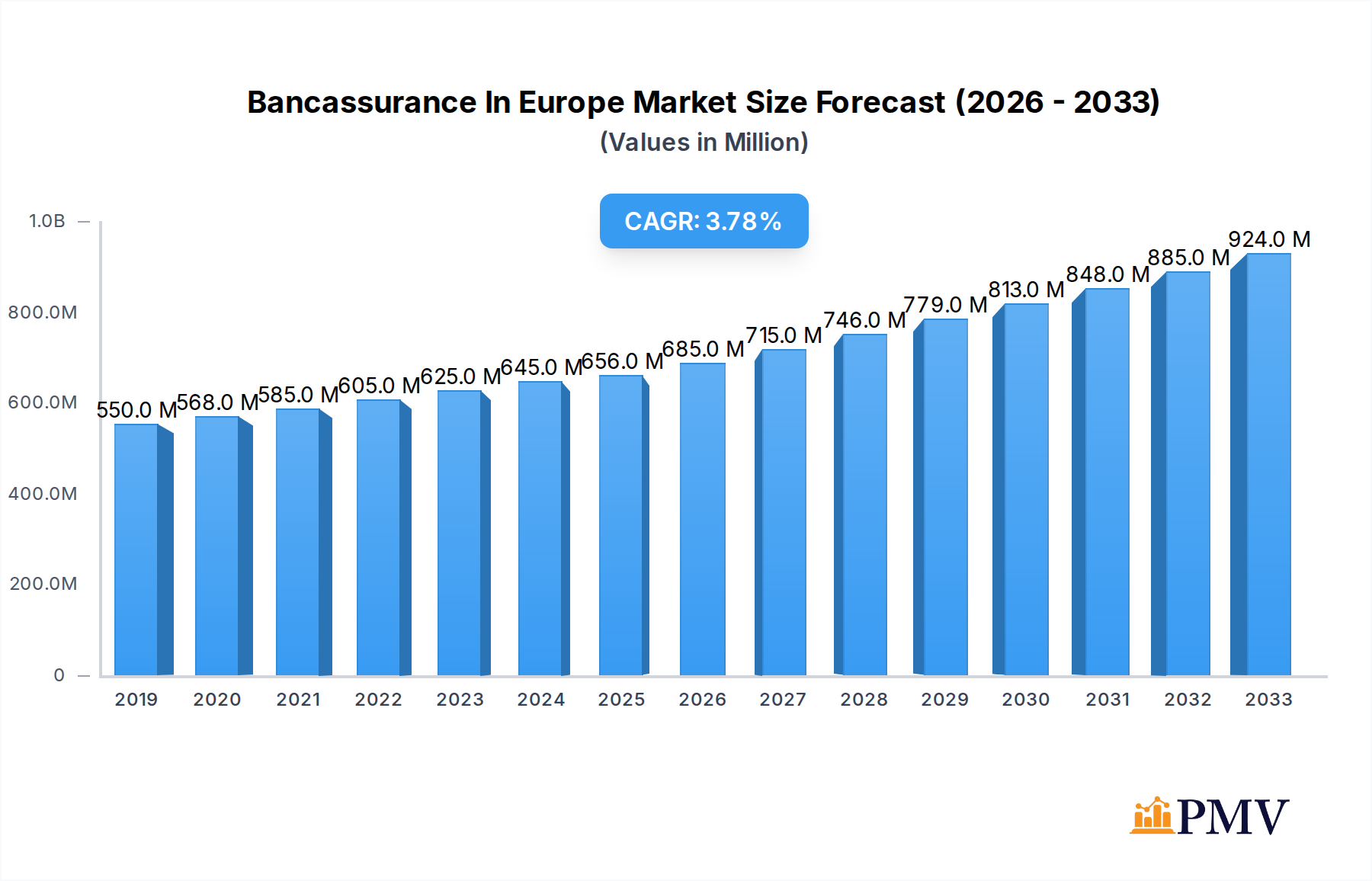

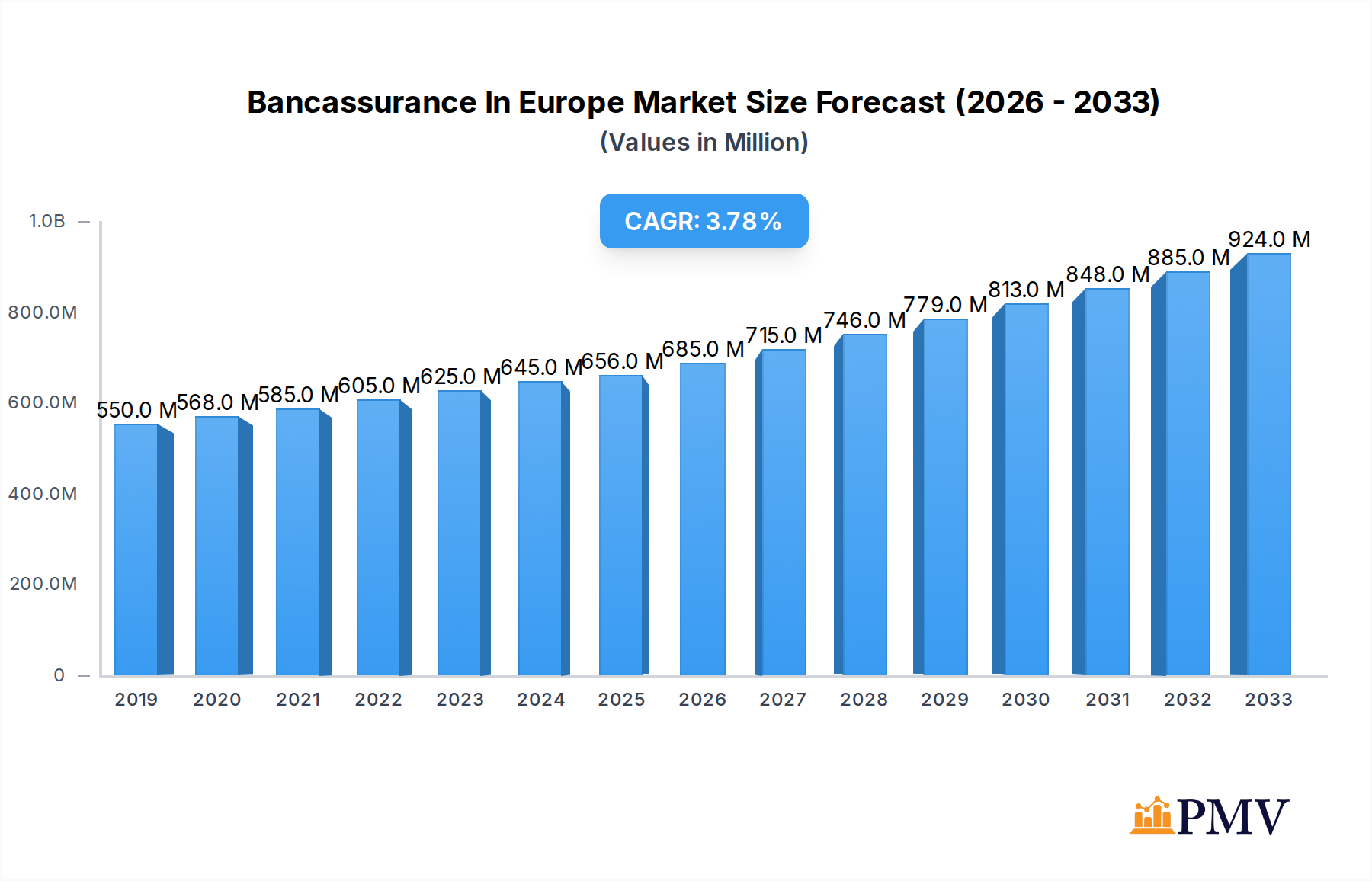

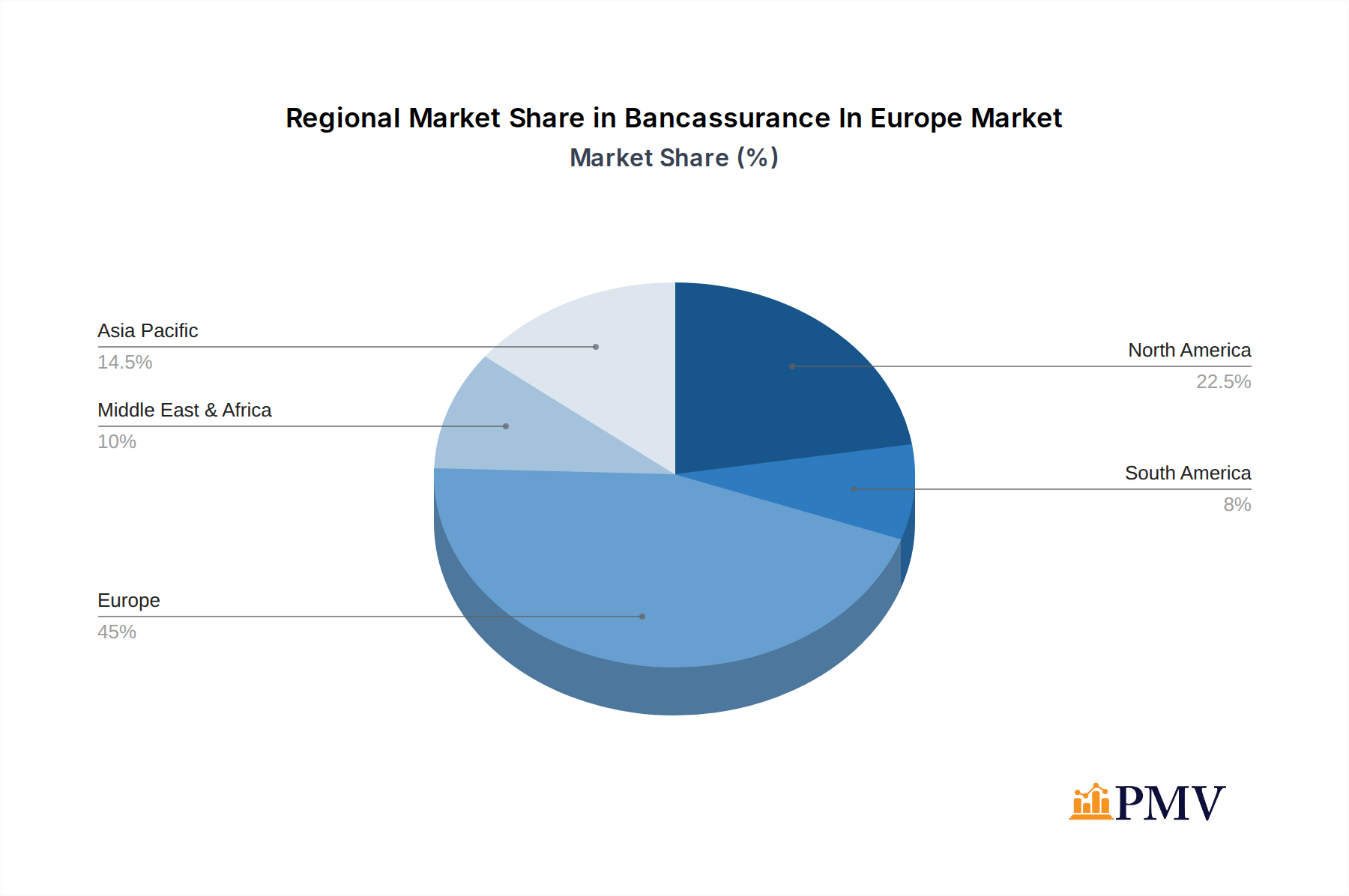

The European Bancassurance market is poised for significant expansion, projected to reach $656 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.56% through to 2033. This growth is primarily propelled by a confluence of factors including evolving customer preferences for integrated financial services, the inherent trust consumers place in their banking institutions, and the strategic imperative for banks to diversify revenue streams beyond traditional lending. Life insurance products are expected to lead segment growth, driven by increasing awareness of long-term financial planning and the demand for wealth accumulation solutions. Non-life insurance, encompassing general insurance and protection products, will also witness steady progress as banks increasingly offer comprehensive financial protection packages. Geographically, Europe, with its mature financial sector and dense banking network, will remain the dominant region, followed by North America and Asia Pacific, which are exhibiting strong growth potential. The increasing adoption of digital platforms and personalized offerings by bancassurance providers are key trends shaping the market landscape.

Bancassurance In Europe Market Size (In Million)

Despite the promising outlook, the Bancassurance market in Europe faces certain challenges that warrant strategic attention. Stricter regulatory environments, particularly concerning consumer protection and product suitability, can impose compliance burdens and potentially dampen innovation. Intense competition from established insurance companies and emerging InsurTech players also necessitates continuous adaptation and differentiation. Furthermore, fluctuations in economic conditions and interest rates can impact consumer spending power and the attractiveness of certain insurance products. However, the strategic focus of leading companies like AG Insurance, AXA, Allianz, and Generali on leveraging digital transformation, enhancing customer engagement through tailored product offerings, and forging stronger partnerships with banks is expected to mitigate these restraints. The market is actively consolidating, with key players seeking strategic alliances and acquisitions to expand their product portfolios and geographical reach, thereby solidifying their competitive positions.

Bancassurance In Europe Company Market Share

Unlock critical insights into the burgeoning European bancassurance landscape. This in-depth report provides a strategic overview of market dynamics, emerging trends, dominant segments, and competitive strategies shaping the future of banking and insurance integration across the continent. With a study period spanning 2019–2033 and a base year of 2025, this analysis is essential for insurers, banks, investors, and policymakers seeking to capitalize on this evolving market. Explore granular data, actionable insights, and expert predictions for optimal strategic decision-making.

Bancassurance In Europe Market Structure & Competitive Dynamics

The European bancassurance market exhibits a highly concentrated structure, driven by the dominance of a few large banking groups and established insurance providers. Innovation ecosystems are rapidly evolving, with a significant push towards digital bancassurance solutions, fueled by customer demand for seamless online experiences and personalized product offerings. Regulatory frameworks, while generally supportive, continue to adapt to the complexities of cross-selling financial products, impacting distribution channels and consumer protection. Product substitutes are increasingly prevalent, including direct-to-consumer insurance models and embedded insurance solutions, intensifying competition. End-user trends highlight a growing preference for bundled financial services and the convenience of acquiring insurance through trusted banking channels. Mergers and acquisitions (M&A) remain a significant feature, with deal values in the past year reaching an estimated €5,000 Million. Key M&A activities are driven by strategic objectives to expand market reach, enhance product portfolios, and leverage technological advancements.

- Market Concentration: Dominated by a few key players, indicating a mature yet competitive environment.

- Innovation Ecosystems: Strong focus on digital transformation, API integration, and data analytics for personalized offerings.

- Regulatory Frameworks: Evolving landscape impacting data privacy, consumer protection, and cross-border operations.

- Product Substitutes: Growing threat from InsurTech startups and embedded insurance solutions.

- End-User Trends: Increasing demand for convenience, digital accessibility, and integrated financial solutions.

- M&A Activities: Strategic consolidations and partnerships to gain market share and technological capabilities, with estimated deal values of €5,000 Million.

Bancassurance In Europe Industry Trends & Insights

The European bancassurance industry is experiencing robust growth, propelled by several key market growth drivers. The increasing financial literacy and evolving consumer expectations for integrated financial services are primary catalysts. Banks are leveraging their extensive customer bases and trusted relationships to distribute a wider array of insurance products, thereby enhancing customer lifetime value and revenue diversification. Technological disruptions are at the forefront of this transformation, with advancements in AI, machine learning, and big data analytics enabling hyper-personalization of insurance products and claims processing. The adoption of digital bancassurance platforms and mobile banking apps is accelerating, making insurance more accessible and convenient for consumers. These digital initiatives are supported by ongoing investments in InsurTech solutions and the integration of third-party APIs. Consumer preferences are shifting towards flexible, modular insurance policies that can be tailored to individual needs and life stages. There is a growing demand for simple, transparent products that can be purchased easily through digital channels. The competitive landscape is characterized by a dynamic interplay between traditional financial institutions and emerging InsurTech players, fostering innovation and driving down costs. Market penetration for bancassurance products continues to rise across Europe, particularly in segments like life insurance and home insurance. The Compound Annual Growth Rate (CAGR) for the European bancassurance market is projected to be around 7.5% over the forecast period, reaching an estimated market size of €150,000 Million by 2033. Strategic partnerships between banks and insurers are becoming more sophisticated, focusing on joint product development, data sharing, and co-branded marketing campaigns to maximize customer acquisition and retention. The emphasis on customer-centricity and the delivery of exceptional digital experiences are critical success factors in this evolving market. The integration of IoT devices for usage-based insurance and the application of predictive analytics for risk assessment are further shaping the industry's trajectory, promising more efficient and personalized insurance solutions.

Dominant Markets & Segments in Bancassurance In Europe

Life Insurance currently holds a dominant position within the European bancassurance market, accounting for an estimated 65% of total bancassurance premiums. This dominance is underpinned by a confluence of economic policies, regulatory support for long-term savings products, and a historical preference for life insurance as a core financial planning tool among European consumers. Banks find it natural to offer life insurance products, such as whole life, term life, and investment-linked policies, to their existing client base, particularly to individuals seeking to secure their families' financial futures and plan for retirement. The inherent trust associated with banking institutions facilitates the cross-selling of these often complex, long-term financial commitments. Economic stability and favorable interest rate environments in certain European nations further bolster demand for life insurance products that offer guaranteed returns or long-term growth potential.

In contrast, Non-life Insurance, while growing rapidly, currently represents approximately 35% of the bancassurance market. However, its growth trajectory is steeper, driven by increasing consumer awareness of the need for protection against various risks and the convenience of purchasing insurance alongside other financial services. Key non-life segments experiencing significant traction include:

- Motor Insurance: Banks are increasingly integrating motor insurance offers, especially in markets where car ownership is high. Initiatives like the collaboration between Admiral Seguros and ING Spain for digital auto insurance highlight this trend.

- Home Insurance: Bundling home insurance with mortgage products remains a popular and effective strategy for bancassurance providers.

- Travel Insurance: Often offered as an add-on to credit cards or debit cards, travel insurance is a high-volume, low-premium product that complements banking services.

- Protection Insurance: This includes critical illness cover and income protection, gaining traction as consumers prioritize comprehensive financial security.

The dominance of life insurance is likely to persist in the short to medium term due to established distribution channels and consumer habits. However, the growth potential of non-life segments is substantial, driven by innovation in product design, digital distribution, and a rising demand for protection against everyday risks. Economic policies that encourage savings and investment, coupled with infrastructure that supports digital financial services, are key drivers of dominance in both segments. Furthermore, the regulatory environment, which often supports the sale of investment-linked life insurance through banks, contributes to its leading position.

Bancassurance In Europe Product Innovations

European bancassurance providers are at the forefront of product innovation, driven by the need to meet evolving customer demands and stay competitive. Innovations are centered around digital integration, personalization, and embedded solutions. Key developments include the creation of digital-first insurance products, offering seamless online application and claims processes. Usage-based insurance models, particularly in motor and home insurance, are gaining traction, leveraging IoT data to offer more accurate pricing and personalized coverage. Bundled insurance packages that combine life, non-life, and even investment products into single, easily manageable policies are also a significant trend. These innovations provide competitive advantages by enhancing customer convenience, improving risk assessment accuracy, and offering greater value for money.

Report Segmentation & Scope

This report meticulously segments the European bancassurance market by Type of Insurance, providing granular analysis for:

- Life Insurance: This segment encompasses a wide range of products including term life, whole life, universal life, and investment-linked insurance. Projections indicate continued strong market share, with a projected market size of €97,500 Million by 2033, driven by demand for retirement planning and wealth accumulation. Competitive dynamics are characterized by established players and a focus on long-term customer relationships.

- Non-life Insurance: This segment includes motor, home, travel, and protection insurance. It is expected to witness higher growth rates, with a projected market size of €52,500 Million by 2033. Key growth drivers include increased consumer awareness of risk and the convenience of integrated banking and insurance services. Competitive dynamics are increasingly influenced by InsurTech innovation and digital distribution channels.

Key Drivers of Bancassurance In Europe Growth

Several interconnected factors are propelling the growth of the bancassurance sector in Europe.

- Digital Transformation: The widespread adoption of mobile banking and online platforms by banks is making insurance products more accessible and convenient to purchase.

- Customer Trust and Relationships: Banks leverage their established trust and deep customer relationships to effectively cross-sell insurance products, reducing customer acquisition costs.

- Diversification of Revenue Streams: For banks, bancassurance offers a crucial avenue to diversify revenue beyond traditional lending and fee-based services.

- Regulatory Support and Evolving Frameworks: Supportive regulatory environments in many European countries facilitate the integration of insurance distribution within banking operations.

- Demand for Integrated Financial Solutions: Consumers increasingly prefer a one-stop-shop for their financial needs, making bundled banking and insurance products highly attractive.

Challenges in the Bancassurance In Europe Sector

Despite its growth, the European bancassurance sector faces significant challenges.

- Regulatory Complexity and Compliance: Navigating diverse and evolving regulatory landscapes across different European countries poses substantial compliance burdens.

- Competition from InsurTech and Direct Insurers: The rise of agile InsurTech startups and aggressive direct-to-consumer insurance models intensifies competition for market share.

- Customer Perception and Trust Erosion: In some instances, aggressive cross-selling tactics by banks can lead to customer dissatisfaction and erode trust in bancassurance products.

- Integration of Legacy Systems: Many established banks grapple with integrating new digital bancassurance platforms with their existing, often outdated, IT infrastructure.

- Product Simplification and Transparency: Ensuring that complex insurance products are clearly communicated and easily understood by consumers remains a persistent challenge.

Leading Players in the Bancassurance In Europe Market

- AG Insurance

- Credit Agricole

- Aviva

- AXA

- BNP Paribas Cardif

- Zurich

- Intesa Sanpaolo

- CNP Assurances

- Allianz

- Generali

Key Developments in Bancassurance In Europe Sector

- June 2023: Admiral Seguros collaborated with ING Spain for a digital bancassurance venture. The collaboration stemmed from Admiral Group's expansion of its distribution network with insurance solutions. This joint partnership led to the creation of ING Orange Auto Insurance, a digital product designed to revolutionize the insurance sector.

- February 2023: European insurance group Talanx strengthened its regional presence in the Polish market by signing a ten-year bancassurance deal with Bank Millennium. This agreement expanded its portfolio in the life protection and non-motor business.

Strategic Bancassurance In Europe Market Outlook

The strategic outlook for the European bancassurance market is exceptionally promising, driven by the continued digitization of financial services and an increasing demand for comprehensive financial solutions. Future growth will be accelerated by deeper integration of AI and machine learning for hyper-personalized product offerings and proactive customer engagement. Strategic opportunities lie in expanding into underserved markets, developing innovative embedded insurance solutions for non-traditional channels, and fostering strategic partnerships with FinTech companies. The focus on customer-centricity, data-driven insights, and the seamless integration of banking and insurance journeys will be paramount for sustained success and market leadership in the coming years.

Bancassurance In Europe Segmentation

-

1. Type of Insurance

- 1.1. Life Insurance

- 1.2. Non-life Insurance

Bancassurance In Europe Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Bancassurance In Europe Regional Market Share

Geographic Coverage of Bancassurance In Europe

Bancassurance In Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 5.1.1. Life Insurance

- 5.1.2. Non-life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 6. Global Bancassurance In Europe Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 6.1.1. Life Insurance

- 6.1.2. Non-life Insurance

- 6.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 7. North America Bancassurance In Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 7.1.1. Life Insurance

- 7.1.2. Non-life Insurance

- 7.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 8. South America Bancassurance In Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 8.1.1. Life Insurance

- 8.1.2. Non-life Insurance

- 8.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 9. Europe Bancassurance In Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 9.1.1. Life Insurance

- 9.1.2. Non-life Insurance

- 9.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 10. Middle East & Africa Bancassurance In Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 10.1.1. Life Insurance

- 10.1.2. Non-life Insurance

- 10.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 11. Asia Pacific Bancassurance In Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 11.1.1. Life Insurance

- 11.1.2. Non-life Insurance

- 11.1. Market Analysis, Insights and Forecast - by Type of Insurance

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AG Insurance

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Credit Agricole

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Aviva**List Not Exhaustive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AXA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BNP Paribas Cardif

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Zurich

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Intesa Sanpaolo

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CNP Assurances

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Allianz

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Generali

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 AG Insurance

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Bancassurance In Europe Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Bancassurance In Europe Revenue (Million), by Type of Insurance 2025 & 2033

- Figure 3: North America Bancassurance In Europe Revenue Share (%), by Type of Insurance 2025 & 2033

- Figure 4: North America Bancassurance In Europe Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Bancassurance In Europe Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America Bancassurance In Europe Revenue (Million), by Type of Insurance 2025 & 2033

- Figure 7: South America Bancassurance In Europe Revenue Share (%), by Type of Insurance 2025 & 2033

- Figure 8: South America Bancassurance In Europe Revenue (Million), by Country 2025 & 2033

- Figure 9: South America Bancassurance In Europe Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Bancassurance In Europe Revenue (Million), by Type of Insurance 2025 & 2033

- Figure 11: Europe Bancassurance In Europe Revenue Share (%), by Type of Insurance 2025 & 2033

- Figure 12: Europe Bancassurance In Europe Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Bancassurance In Europe Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa Bancassurance In Europe Revenue (Million), by Type of Insurance 2025 & 2033

- Figure 15: Middle East & Africa Bancassurance In Europe Revenue Share (%), by Type of Insurance 2025 & 2033

- Figure 16: Middle East & Africa Bancassurance In Europe Revenue (Million), by Country 2025 & 2033

- Figure 17: Middle East & Africa Bancassurance In Europe Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Bancassurance In Europe Revenue (Million), by Type of Insurance 2025 & 2033

- Figure 19: Asia Pacific Bancassurance In Europe Revenue Share (%), by Type of Insurance 2025 & 2033

- Figure 20: Asia Pacific Bancassurance In Europe Revenue (Million), by Country 2025 & 2033

- Figure 21: Asia Pacific Bancassurance In Europe Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Bancassurance In Europe Revenue Million Forecast, by Type of Insurance 2020 & 2033

- Table 2: Global Bancassurance In Europe Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Bancassurance In Europe Revenue Million Forecast, by Type of Insurance 2020 & 2033

- Table 4: Global Bancassurance In Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Global Bancassurance In Europe Revenue Million Forecast, by Type of Insurance 2020 & 2033

- Table 9: Global Bancassurance In Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Brazil Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Argentina Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Bancassurance In Europe Revenue Million Forecast, by Type of Insurance 2020 & 2033

- Table 14: Global Bancassurance In Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Russia Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Benelux Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Nordics Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Bancassurance In Europe Revenue Million Forecast, by Type of Insurance 2020 & 2033

- Table 25: Global Bancassurance In Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Turkey Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Israel Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: GCC Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: North Africa Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Africa Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Bancassurance In Europe Revenue Million Forecast, by Type of Insurance 2020 & 2033

- Table 33: Global Bancassurance In Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 34: China Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: India Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Japan Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Korea Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: ASEAN Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Oceania Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Bancassurance In Europe Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bancassurance In Europe?

The projected CAGR is approximately 4.56%.

2. Which companies are prominent players in the Bancassurance In Europe?

Key companies in the market include AG Insurance, Credit Agricole, Aviva**List Not Exhaustive, AXA, BNP Paribas Cardif, Zurich, Intesa Sanpaolo, CNP Assurances, Allianz, Generali.

3. What are the main segments of the Bancassurance In Europe?

The market segments include Type of Insurance.

4. Can you provide details about the market size?

The market size is estimated to be USD 656 Million as of 2022.

5. What are some drivers contributing to market growth?

Regulatory and Technological Developments.

6. What are the notable trends driving market growth?

The Rising Need for Non-Life Insurance is Propelling Expansion in the Bancassurance Market.

7. Are there any restraints impacting market growth?

Competition from Other Distribution Channels.

8. Can you provide examples of recent developments in the market?

June 2023: Admiral Seguros collaborated with ING Spain for a digital bancassurance venture. The collaboration stemmed from Admiral Group's expansion of its distribution network with insurance solutions. This joint partnership led to the creation of ING Orange Auto Insurance, a digital product designed to revolutionize the insurance sector.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Bancassurance In Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Bancassurance In Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Bancassurance In Europe?

To stay informed about further developments, trends, and reports in the Bancassurance In Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence