Key Insights

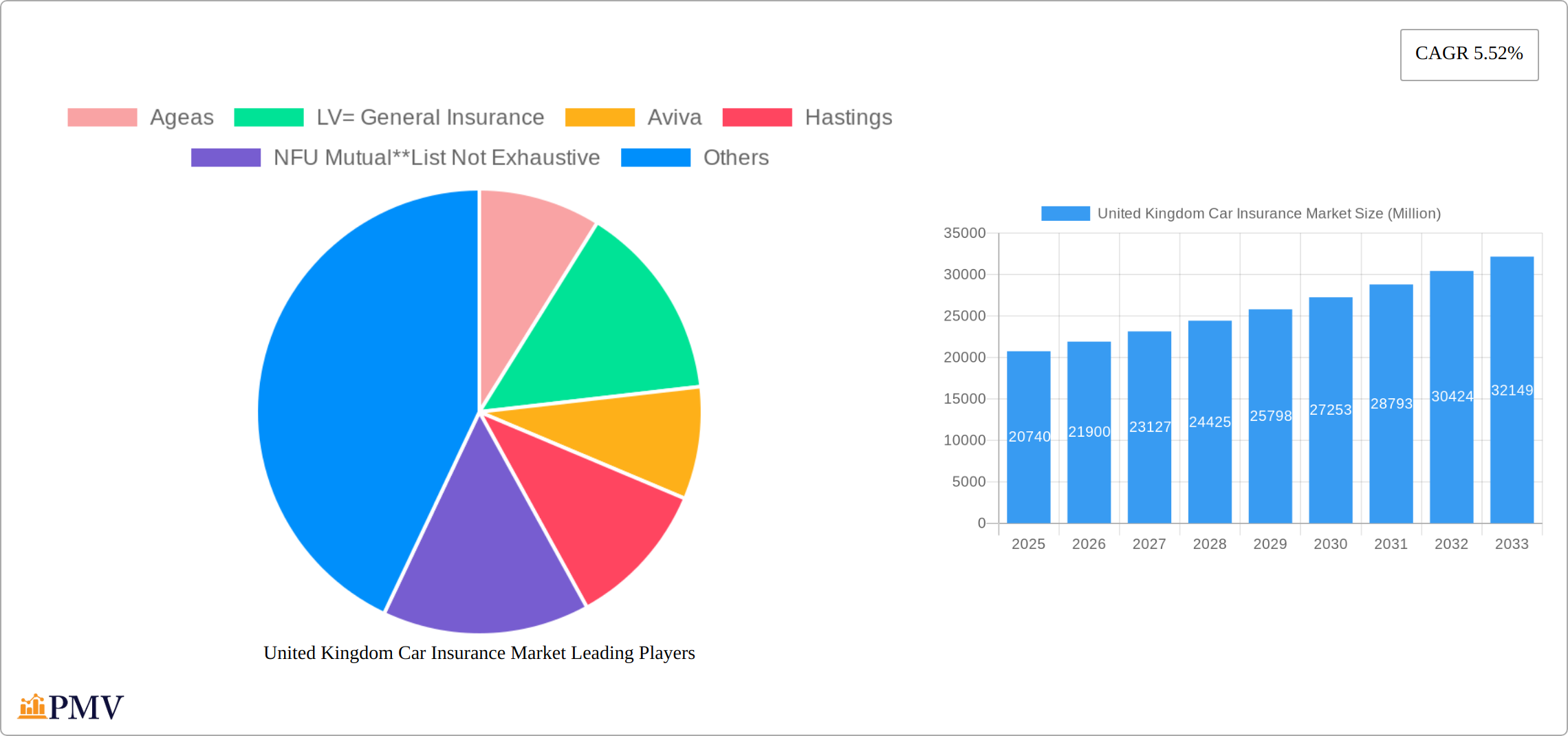

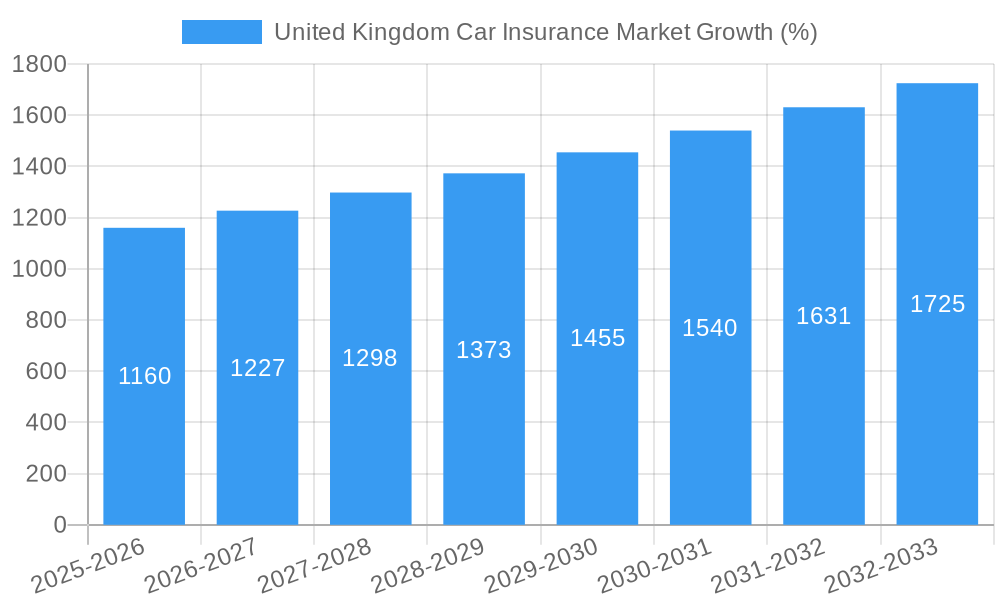

The United Kingdom car insurance market, valued at approximately £20.74 billion in 2025, is projected to experience robust growth, driven by a rising vehicle ownership rate, increasing urbanization, and stricter government regulations concerning mandatory insurance coverage. The market's Compound Annual Growth Rate (CAGR) of 5.52% from 2025 to 2033 indicates a significant expansion, fueled by factors such as the growing popularity of telematics-based insurance, the increasing adoption of online distribution channels for ease of purchase and comparison, and the introduction of innovative insurance products tailored to specific customer needs. Competition remains intense among established players like Aviva, Direct Line Group, and Admiral Group, along with the rise of digital-first insurers. While economic fluctuations and changes in consumer behavior could pose challenges, the long-term outlook for the UK car insurance market remains positive, with significant opportunities for growth in segments like comprehensive coverage for personal vehicles and the expansion of services offered through online platforms. Further growth is likely to be supported by ongoing technological advancements like AI-powered risk assessment models leading to more accurate pricing and fraud detection capabilities.

The segmentation within the UK car insurance market reveals that third-party liability coverage remains a significant portion, although comprehensive and optional coverages are showing consistent growth, reflecting a rising consumer preference for greater protection. Personal vehicles constitute a larger segment compared to commercial vehicles, although the latter is expected to see growth due to expanding business activities. Distribution channels are undergoing transformation with online sales increasingly gaining traction, yet traditional channels like individual agents and brokers continue to hold substantial market share. The geographical concentration is primarily within the UK itself, with regional variations primarily driven by population density, income levels, and vehicle ownership patterns. Despite challenges like increasing claims costs and regulatory changes, the market demonstrates resilience and is predicted to continue its upward trajectory over the forecast period.

United Kingdom Car Insurance Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the United Kingdom car insurance market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report meticulously examines market size, segmentation, competitive dynamics, and future growth prospects. The study incorporates historical data (2019-2024) and leverages advanced analytical methodologies to deliver actionable intelligence.

United Kingdom Car Insurance Market Structure & Competitive Dynamics

The UK car insurance market is characterized by a moderately concentrated landscape with several major players vying for market share. Key competitors include Ageas, LV= General Insurance, Aviva, Hastings, NFU Mutual, RSA, AXA, Esure, Direct Line Group, and Admiral Group. However, the market also encompasses numerous smaller insurers, contributing to a dynamic competitive environment. Market share analysis reveals that the top five players command approximately xx% of the total market in 2025, indicating a degree of consolidation. Innovation is driven by technological advancements, such as telematics and AI-powered risk assessment tools, leading to more personalized and cost-effective insurance products. The regulatory framework, overseen by the Financial Conduct Authority (FCA), plays a crucial role in maintaining consumer protection and market stability. Product substitutes, such as peer-to-peer insurance platforms, are gradually gaining traction, posing a challenge to traditional insurers. End-user trends towards digitalization and personalized services are reshaping customer expectations. Furthermore, mergers and acquisitions (M&A) activities, with deal values totaling approximately £xx Million in the past five years, demonstrate ongoing industry consolidation and strategic expansion.

- Market Concentration: Top 5 players hold approximately xx% market share (2025).

- M&A Activity: Total deal value estimated at £xx Million (2019-2024).

- Innovation: Telematics, AI-powered risk assessment, and peer-to-peer platforms are shaping the market.

- Regulatory Framework: FCA oversight ensures consumer protection and market stability.

United Kingdom Car Insurance Market Industry Trends & Insights

The UK car insurance market exhibits a steady growth trajectory, driven primarily by increasing vehicle ownership, rising urbanization, and stringent government regulations mandating minimum insurance coverage. Technological disruptions, particularly the adoption of telematics and AI, are enhancing risk assessment accuracy and driving product innovation. Consumers are increasingly demanding personalized insurance packages and seamless digital experiences, impacting the distribution channels and product offerings. Intense competition among insurers is spurring price wars and incentivizing innovation in customer service. The Compound Annual Growth Rate (CAGR) for the market is estimated at xx% during the forecast period (2025-2033), with market penetration projected to reach xx% by 2033. Furthermore, the shift towards electric vehicles is expected to influence insurance pricing and product development. These factors contribute to a dynamic and evolving market landscape.

Dominant Markets & Segments in United Kingdom Car Insurance Market

The UK car insurance market is dominated by the personal vehicle segment, which accounts for approximately xx% of the total market in 2025. Within coverage types, Collision/Comprehensive/Other Optional Coverage holds a significantly larger market share than Third-Party Liability Coverage, reflecting consumer preference for broader protection. Online distribution channels are experiencing rapid growth, driven by increased internet penetration and consumer preference for convenient digital transactions.

- Leading Segment: Personal Vehicles (approximately xx% market share in 2025).

- Dominant Coverage: Collision/Comprehensive/Other Optional Coverage.

- Fastest-Growing Channel: Online Distribution.

Key Drivers:

- Economic Factors: Rising disposable incomes and increased vehicle ownership.

- Technological Advancements: Telematics, AI, and digital distribution channels.

- Regulatory Policies: Mandatory insurance requirements and consumer protection regulations.

United Kingdom Car Insurance Market Product Innovations

The UK car insurance market is witnessing significant product innovation, particularly in the area of telematics-based insurance. These products leverage connected car technology to monitor driver behavior and offer customized premiums based on individual risk profiles. Insurers are also incorporating AI-powered fraud detection systems and utilizing big data analytics to enhance risk assessment accuracy and streamline claims processing. This leads to more competitive pricing and personalized service offerings. The market fit for these innovations is strong, given the increasing demand for affordable and tailored insurance products.

Report Segmentation & Scope

This report segments the UK car insurance market based on coverage type (Third-Party Liability Coverage, Collision/Comprehensive/Other Optional Coverage), application (Personal Vehicles, Commercial Vehicles), and distribution channel (Direct Sales, Individual Agents, Brokers, Banks, Online, Other Distribution Channels). Each segment's growth projections, market sizes, and competitive dynamics are analyzed in detail. For example, the Online distribution channel is projected to experience significant growth due to the increasing adoption of digital platforms. The Commercial Vehicles segment is expected to show moderate growth, driven by the expansion of the logistics and transportation sectors.

Key Drivers of United Kingdom Car Insurance Market Growth

Several key factors fuel the growth of the UK car insurance market. These include increasing vehicle ownership, driven by economic growth and rising living standards. Technological advancements, such as telematics and AI-powered risk assessment, are improving the efficiency and personalization of insurance products. Stringent government regulations mandating minimum insurance coverage further contribute to market growth.

Challenges in the United Kingdom Car Insurance Market Sector

The UK car insurance market faces challenges including intense competition that pressures profit margins. Fluctuations in fuel prices and economic downturns impact consumer spending on insurance. Moreover, regulatory changes and evolving consumer expectations necessitate continuous adaptation and innovation from insurers. Fraudulent claims also represent a significant challenge, requiring robust risk management strategies.

Leading Players in the United Kingdom Car Insurance Market Market

- Ageas

- LV= General Insurance

- Aviva

- Hastings

- NFU Mutual

- RSA

- AXA

- Esure

- Direct Line Group

- Admiral Group

Key Developments in United Kingdom Car Insurance Market Sector

- October 2023: ARAG SE partnered with Hastings Direct to offer vehicle hire insurance as an add-on to their motor insurance policies, impacting the add-on insurance segment.

- December 2022: Covea Insurance and BGL Insurance launched "Nutshell," a new car insurance brand, impacting market competition and customer choice.

Strategic United Kingdom Car Insurance Market Market Outlook

The UK car insurance market presents significant growth opportunities, particularly in areas such as telematics-based insurance and personalized risk assessment. Strategic partnerships and technological innovation will be crucial for insurers to remain competitive. Focus on customer experience and efficient claims management will drive future success. The market's continued growth is predicated on steady economic expansion, increasing vehicle ownership, and the adoption of advanced technologies.

United Kingdom Car Insurance Market Segmentation

-

1. Coverage

- 1.1. Third-Party Liability Coverage

- 1.2. Collision/Comprehensive/Other Optional Coverage

-

2. Application

- 2.1. Personal Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Direct Sales

- 3.2. Individual Agents

- 3.3. Brokers

- 3.4. Banks

- 3.5. Online

- 3.6. Other Distribution Channels

United Kingdom Car Insurance Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Car Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.52% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Adoption of Innovative Tracking Technologies

- 3.3. Market Restrains

- 3.3.1. Rising Competition of Banks with Fintech and Financial Services

- 3.4. Market Trends

- 3.4.1. Growth of Car Sales as Demand for Electric Car in United Kingdom

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 5.1.1. Third-Party Liability Coverage

- 5.1.2. Collision/Comprehensive/Other Optional Coverage

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct Sales

- 5.3.2. Individual Agents

- 5.3.3. Brokers

- 5.3.4. Banks

- 5.3.5. Online

- 5.3.6. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 6. Asia Pacific United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1 China

- 6.1.2 Japan

- 6.1.3 India

- 6.1.4 South Korea

- 6.1.5 Taiwan

- 6.1.6 Australia

- 6.1.7 Rest of Asia-Pacific

- 7. North America United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1 United States

- 7.1.2 Canada

- 7.1.3 Mexico

- 8. Europe United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 Germany

- 8.1.2 France

- 8.1.3 Italy

- 8.1.4 United Kingdom

- 8.1.5 Netherlands

- 8.1.6 Rest of Europe

- 9. South America United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1 Brazil

- 9.1.2 Argentina

- 9.1.3 Rest of South America

- 10. Middle East & Africa United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 UAE

- 10.1.2 South Africa

- 10.1.3 Saudi Arabia

- 10.1.4 Rest of MEA

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Ageas

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 LV= General Insurance

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Aviva

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Hastings

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 NFU Mutual**List Not Exhaustive

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 RSA

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Axa

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Esure

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Direct Line Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Admiral Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Ageas

List of Figures

- Figure 1: United Kingdom Car Insurance Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: United Kingdom Car Insurance Market Share (%) by Company 2024

List of Tables

- Table 1: United Kingdom Car Insurance Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: United Kingdom Car Insurance Market Revenue Million Forecast, by Coverage 2019 & 2032

- Table 3: United Kingdom Car Insurance Market Revenue Million Forecast, by Application 2019 & 2032

- Table 4: United Kingdom Car Insurance Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: United Kingdom Car Insurance Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Japan United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: India United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: South Korea United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Taiwan United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Australia United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Asia-Pacific United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Germany United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Italy United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: United Kingdom United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Netherlands United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Brazil United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Argentina United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Rest of South America United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 30: UAE United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: South Africa United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Saudi Arabia United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Rest of MEA United Kingdom Car Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: United Kingdom Car Insurance Market Revenue Million Forecast, by Coverage 2019 & 2032

- Table 35: United Kingdom Car Insurance Market Revenue Million Forecast, by Application 2019 & 2032

- Table 36: United Kingdom Car Insurance Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 37: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Car Insurance Market?

The projected CAGR is approximately 5.52%.

2. Which companies are prominent players in the United Kingdom Car Insurance Market?

Key companies in the market include Ageas, LV= General Insurance, Aviva, Hastings, NFU Mutual**List Not Exhaustive, RSA, Axa, Esure, Direct Line Group, Admiral Group.

3. What are the main segments of the United Kingdom Car Insurance Market?

The market segments include Coverage, Application, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.74 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Innovative Tracking Technologies.

6. What are the notable trends driving market growth?

Growth of Car Sales as Demand for Electric Car in United Kingdom.

7. Are there any restraints impacting market growth?

Rising Competition of Banks with Fintech and Financial Services.

8. Can you provide examples of recent developments in the market?

October 2023: ARAG SE agreed to supply vehicle hire insurance for Hastings Direct. The vehicle hire insurance policy will be offered to over a million Hastings Direct motor insurance customers as an optional add-on to their primary motor policy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Car Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Car Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Car Insurance Market?

To stay informed about further developments, trends, and reports in the United Kingdom Car Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence