Key Insights

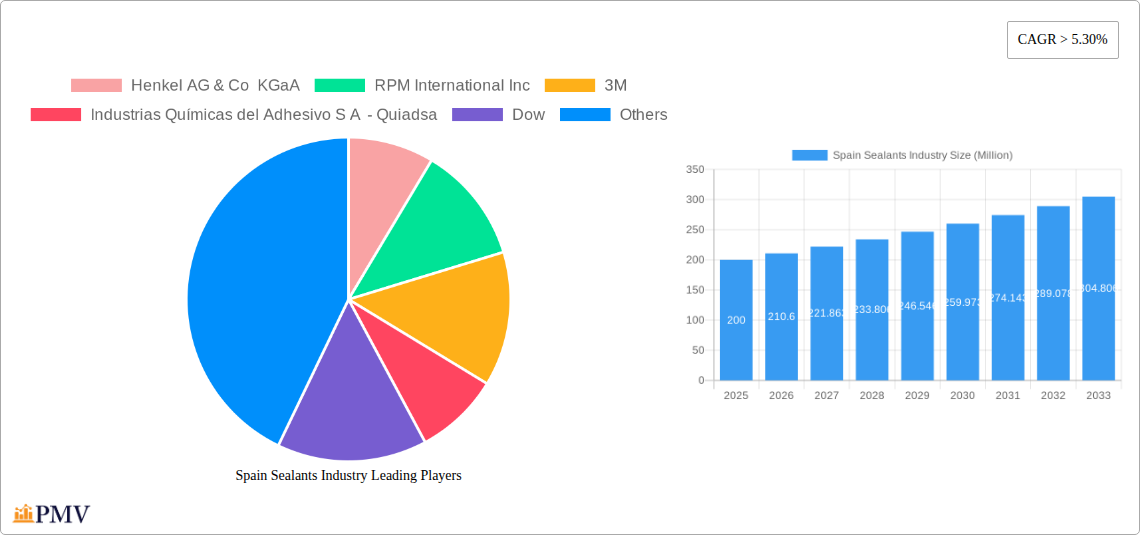

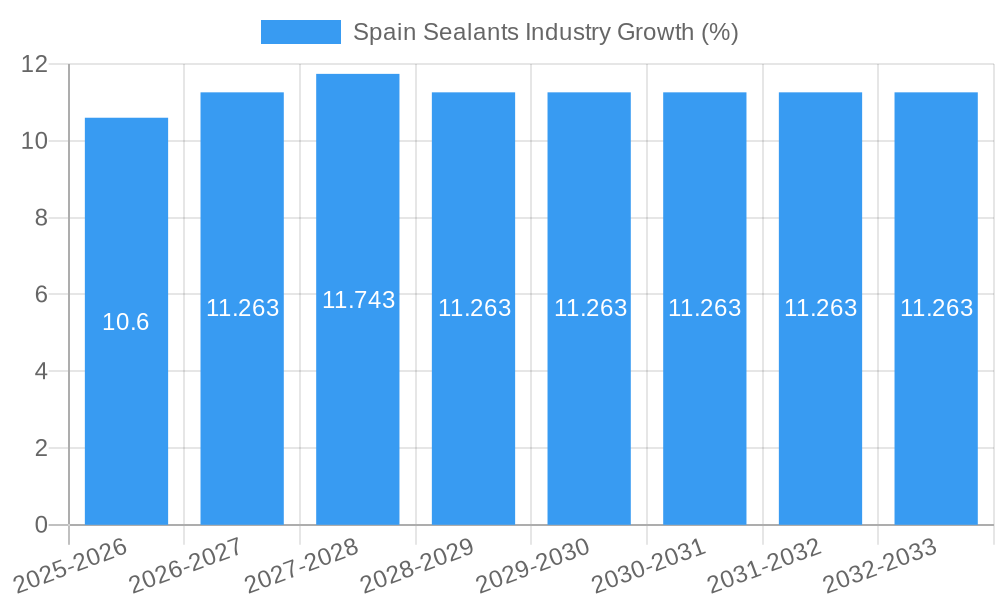

The Spain sealants market, valued at approximately €[Estimate based on market size XX and currency conversion if available; otherwise, use a reasonable estimate based on similar markets. For example: €200 million] in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 5.30% from 2025 to 2033. This expansion is fueled by several key drivers. The burgeoning construction sector in Spain, driven by both residential and infrastructure projects, presents significant demand for sealants. Furthermore, increasing investments in the automotive and aerospace industries, which utilize sealants extensively for bonding and sealing components, contribute to market growth. The growing adoption of high-performance sealants with enhanced durability and sustainability also plays a crucial role. Demand is further stimulated by the rising popularity of eco-friendly and energy-efficient building technologies. Specific resin types like acrylic, epoxy, and polyurethane are experiencing high demand, owing to their versatility across various applications.

However, the market is not without its challenges. Economic fluctuations and raw material price volatility can negatively impact market growth. Competition amongst established players such as Henkel, RPM International, 3M, and Sika, requires continuous innovation and strategic product differentiation. Furthermore, stringent environmental regulations pertaining to volatile organic compounds (VOCs) in sealants necessitate manufacturers to focus on developing and adopting more environmentally friendly formulations. Despite these restraints, the long-term outlook remains positive, with the market expected to reach approximately €[Estimate based on CAGR and 2025 value; for example: €350 million] by 2033, driven by the aforementioned factors and continued investment in infrastructure and industrial development within Spain. The segment analysis reveals that Building and Construction is likely the largest end-user industry, followed by Automotive and Aerospace.

This comprehensive report provides a detailed analysis of the Spain sealants industry, offering invaluable insights for businesses, investors, and stakeholders. The study covers the period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. The report segments the market by end-user industry (Aerospace, Automotive, Building and Construction, Healthcare, Other End-user Industries) and resin type (Acrylic, Epoxy, Polyurethane, Silicone, Other Resins), providing a granular understanding of market dynamics and growth potential. The estimated market size in 2025 is XX Million.

Spain Sealants Industry Market Structure & Competitive Dynamics

The Spain sealants market exhibits a moderately concentrated structure, with key players like Henkel AG & Co KGaA, RPM International Inc, 3M, Industrias Químicas del Adhesivo S A - Quiadsa, Dow, QS Adhesives & Sealants SL, Soudal Holding N V, MAPEI S p A, Sika AG, and Grupa Selena holding significant market share. Market share data for 2024 indicates that the top five players collectively account for approximately 65% of the market.

Innovation within the sector is driven by advancements in resin technology and the development of high-performance sealants tailored to specific end-user needs. The regulatory framework, particularly concerning environmental regulations and safety standards, influences product formulation and manufacturing processes. Product substitution is a moderate factor, with competition from alternative materials such as tapes and gaskets.

End-user trends are a major driver, with increasing demand from the building and construction sector, fueled by infrastructure projects and renovation activities. The automotive industry also presents a significant market, demanding high-performance sealants for enhanced vehicle durability and fuel efficiency. Mergers and acquisitions (M&A) activity has been moderate in recent years, with deal values averaging approximately XX Million per transaction. Recent deals primarily involved smaller players consolidating their positions within niche segments.

Spain Sealants Industry Industry Trends & Insights

The Spain sealants market is experiencing steady growth, with a Compound Annual Growth Rate (CAGR) of approximately 5% projected from 2025 to 2033. Several factors contribute to this growth. Firstly, the robust construction sector, driven by both public and private investments in infrastructure development and residential projects, creates significant demand for construction sealants. Secondly, increasing automotive production and the demand for higher-performing vehicles stimulate the growth of the automotive sealant segment.

Technological advancements, such as the development of more durable, eco-friendly, and specialized sealants, are further propelling market expansion. Consumer preference for high-quality, long-lasting, and environmentally sustainable products influences industry innovation and drives the adoption of premium sealants. Intense competition among established players and new entrants leads to product diversification, pricing pressures, and continuous improvements in sealant performance. Market penetration of specialized sealants, such as those used in aerospace and healthcare applications, is growing steadily, although it remains a relatively smaller segment compared to the construction and automotive sectors.

Dominant Markets & Segments in Spain Sealants Industry

The Building and Construction sector dominates the Spain sealants market, accounting for approximately 60% of total market value in 2024. Key drivers include:

- Robust Infrastructure Development: Significant investments in Spain's infrastructure, including road networks, bridges, and public buildings, fuel demand for construction sealants.

- Residential Construction Boom: Increased housing demand and ongoing urbanization contribute to the growth of this segment.

- Government Initiatives: Supportive government policies promoting sustainable construction practices also boost demand.

Within resin types, Polyurethane sealants hold the largest market share due to their versatility, durability, and suitability for a wide range of applications. Silicone sealants also represent a substantial segment, valued for their weather resistance and adhesion properties. Other resin types, such as acrylic and epoxy, cater to more specialized applications.

Spain Sealants Industry Product Innovations

Recent product innovations focus on enhancing sealant performance, sustainability, and ease of application. Manufacturers are developing sealants with improved weather resistance, UV stability, and chemical resistance. Emphasis is also placed on reducing VOC emissions and incorporating recycled materials to meet environmental regulations and consumer demands. These innovations provide competitive advantages by offering improved product functionality, enhanced durability, and better environmental profiles. New application methods, such as automated dispensing systems, improve efficiency and reduce labor costs.

Report Segmentation & Scope

The report segments the Spain sealants market across various end-user industries: Aerospace (XX Million in 2025, growing at xx% CAGR), Automotive (XX Million in 2025, growing at xx% CAGR), Building and Construction (XX Million in 2025, growing at xx% CAGR), Healthcare (XX Million in 2025, growing at xx% CAGR), and Other End-user Industries (XX Million in 2025, growing at xx% CAGR). Each segment is further categorized by resin type: Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins, with individual growth projections and competitive analyses provided for each sub-segment.

Key Drivers of Spain Sealants Industry Growth

Several key factors drive the growth of the Spain sealants industry. Firstly, significant government investment in infrastructure projects fuels demand for construction sealants. Secondly, the automotive sector's continued expansion, with growing demand for high-performance vehicles, boosts the demand for specialized automotive sealants. Thirdly, technological advancements lead to the development of innovative sealants with superior properties, including improved durability, adhesion, and environmental compatibility.

Challenges in the Spain Sealants Industry Sector

The Spain sealants industry faces challenges including fluctuating raw material prices, which impact production costs and profitability. Stringent environmental regulations require manufacturers to invest in eco-friendly technologies, adding to operational expenses. Intense competition from both domestic and international players creates pricing pressures and necessitates continuous product innovation. Supply chain disruptions can also affect production and timely delivery of sealants to end-users.

Leading Players in the Spain Sealants Industry Market

- Henkel AG & Co KGaA

- RPM International Inc

- 3M

- Industrias Químicas del Adhesivo S A - Quiadsa

- Dow

- QS Adhesives & Sealants SL

- Soudal Holding N V

- MAPEI S p A

- Sika AG

- Grupa Selena

Key Developments in Spain Sealants Industry Sector

- April 2019: Dow completed the separation of its Material Science division through a spin-off of Dow Inc. This restructuring impacted the supply chain and market dynamics for certain sealant raw materials.

Strategic Spain Sealants Industry Market Outlook

The Spain sealants market presents significant growth potential over the forecast period. Continued investment in infrastructure, technological advancements driving product innovation, and the increasing demand for high-performance sealants across various end-user industries create a favorable outlook. Companies focusing on sustainable and specialized sealant solutions are expected to witness greater success. Strategic partnerships and acquisitions could play a key role in shaping market dynamics and achieving a competitive edge.

Spain Sealants Industry Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Healthcare

- 1.5. Other End-user Industries

-

2. Resin

- 2.1. Acrylic

- 2.2. Epoxy

- 2.3. Polyurethane

- 2.4. Silicone

- 2.5. Other Resins

Spain Sealants Industry Segmentation By Geography

- 1. Spain

Spain Sealants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand from the Construction Industry in Saudi Arabia; Other Drivers

- 3.3. Market Restrains

- 3.3.1. ; Impact of COVID-19 Pandemic on Global Economy

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Sealants Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Healthcare

- 5.1.5. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Resin

- 5.2.1. Acrylic

- 5.2.2. Epoxy

- 5.2.3. Polyurethane

- 5.2.4. Silicone

- 5.2.5. Other Resins

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Henkel AG & Co KGaA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 RPM International Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 3M

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Industrias Químicas del Adhesivo S A - Quiadsa

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Dow

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 QS Adhesives & Sealants SL

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Soudal Holding N V

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 MAPEI S p A

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Sika AG

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Grupa Selena

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Henkel AG & Co KGaA

List of Figures

- Figure 1: Spain Sealants Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain Sealants Industry Share (%) by Company 2024

List of Tables

- Table 1: Spain Sealants Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain Sealants Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 3: Spain Sealants Industry Revenue Million Forecast, by Resin 2019 & 2032

- Table 4: Spain Sealants Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Spain Sealants Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Spain Sealants Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 7: Spain Sealants Industry Revenue Million Forecast, by Resin 2019 & 2032

- Table 8: Spain Sealants Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Sealants Industry?

The projected CAGR is approximately > 5.30%.

2. Which companies are prominent players in the Spain Sealants Industry?

Key companies in the market include Henkel AG & Co KGaA, RPM International Inc, 3M, Industrias Químicas del Adhesivo S A - Quiadsa, Dow, QS Adhesives & Sealants SL, Soudal Holding N V, MAPEI S p A, Sika AG, Grupa Selena.

3. What are the main segments of the Spain Sealants Industry?

The market segments include End User Industry, Resin.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand from the Construction Industry in Saudi Arabia; Other Drivers.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

; Impact of COVID-19 Pandemic on Global Economy.

8. Can you provide examples of recent developments in the market?

April 2019: Dow completed the separation of its Material Science division through a spin-off of Dow Inc.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Sealants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Sealants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Sealants Industry?

To stay informed about further developments, trends, and reports in the Spain Sealants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence