Key Insights

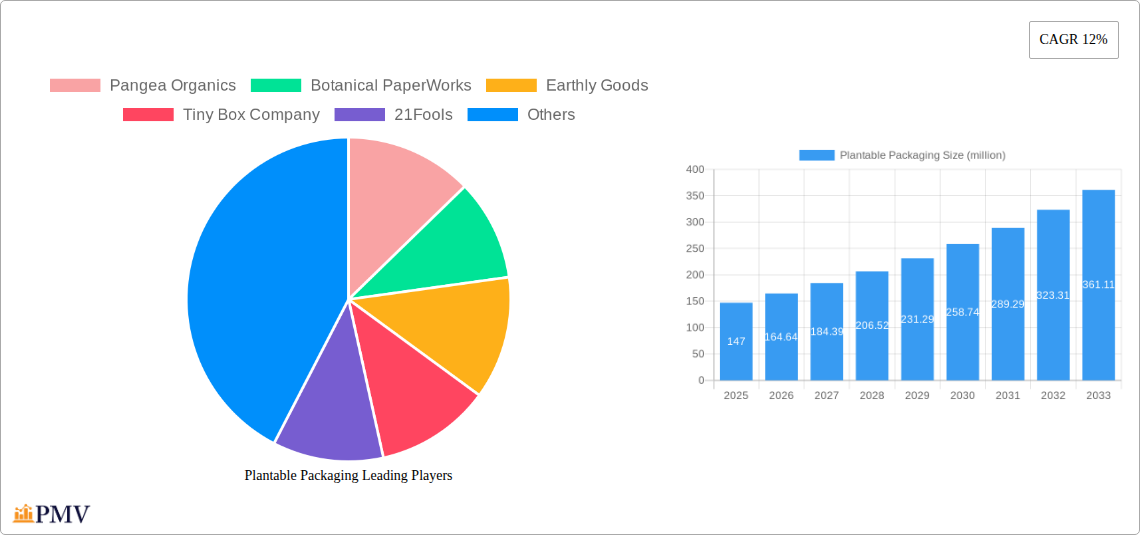

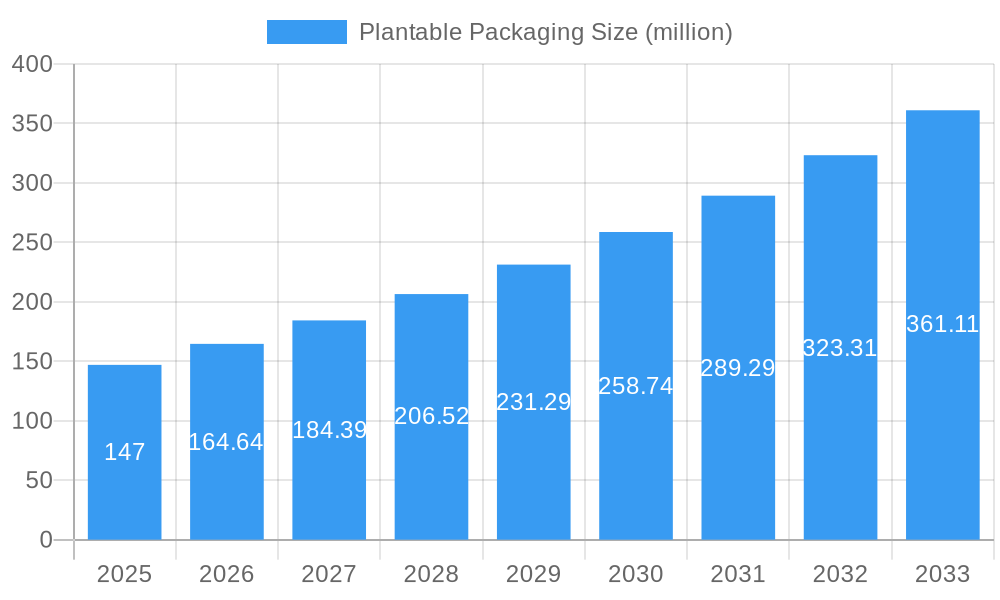

The global plantable packaging market is experiencing robust expansion, driven by a growing consumer and corporate demand for sustainable and eco-friendly alternatives to traditional packaging materials. Valued at an estimated USD 147 million in 2025, the market is projected to surge at a Compound Annual Growth Rate (CAGR) of approximately 12% throughout the forecast period of 2025-2033. This significant growth is fueled by increasing environmental awareness, stringent government regulations promoting sustainable practices, and the unique value proposition of packaging that can be planted to grow into new life. Industries such as retail, food, and pharmaceuticals are increasingly adopting plantable packaging solutions to enhance their brand image, reduce waste, and contribute to biodiversity. Flexible packaging, in particular, is witnessing substantial adoption due to its versatility and cost-effectiveness in applications ranging from product wraps to seed-infused envelopes.

Plantable Packaging Market Size (In Million)

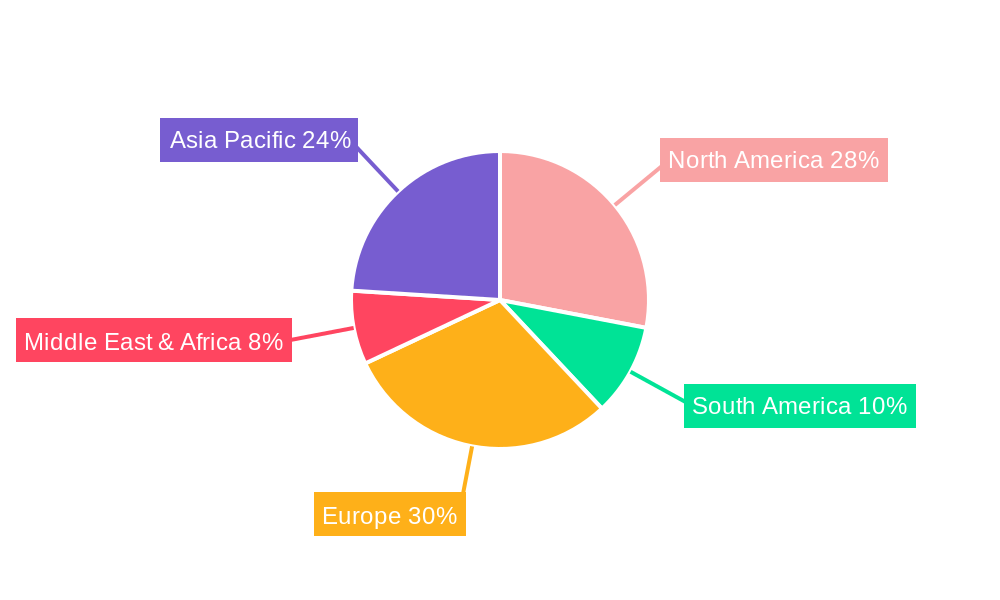

The market's upward trajectory is further propelled by ongoing innovations in material science and manufacturing processes, leading to more durable, versatile, and aesthetically pleasing plantable packaging options. Emerging trends include the integration of biodegradable inks and adhesives, the development of packaging for a wider array of plantable materials, and the creation of customizable designs for promotional purposes. While the market is poised for substantial growth, certain restraints such as higher initial production costs compared to conventional packaging and consumer education gaps regarding the proper disposal and planting of these materials, need to be addressed. However, the overwhelming shift towards a circular economy and the increasing preference for brands with strong sustainability credentials are expected to outweigh these challenges, positioning plantable packaging as a pivotal component of the future packaging landscape across key regions like North America, Europe, and Asia Pacific.

Plantable Packaging Company Market Share

Detailed Report Description: Plantable Packaging Market Analysis (2019–2033)

Unlock the burgeoning potential of sustainable packaging with our comprehensive report on the Plantable Packaging Market. This in-depth analysis offers a detailed exploration of market dynamics, key trends, dominant segments, and competitive landscapes from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this report provides actionable insights for stakeholders seeking to capitalize on the rapidly growing demand for eco-friendly packaging solutions. The report covers critical areas such as market growth drivers, technological innovations, competitive strategies, and regulatory influences, providing a robust foundation for strategic decision-making.

Plantable Packaging Market Structure & Competitive Dynamics

The global plantable packaging market exhibits a moderately concentrated structure, with a significant presence of both established players and innovative startups. Key companies such as Pangea Organics, Botanical PaperWorks, Earthly Goods, Tiny Box Company, 21Fools, Little Green Paper Shop, Green Field Paper, UK Seed Paper, GreenField Paper Company, Eco Marketing Solutions, The Mend, Searo, FlexSea, Evoware, Sway Innovation Co., and Dong Guan on the Way Packaging Products Co., Ltd. are actively shaping the market's trajectory. Innovation ecosystems are thriving, fueled by advancements in biodegradable materials and seed-embedding technologies, fostering a dynamic environment for new product development and enhanced functionality. Regulatory frameworks are increasingly favoring sustainable packaging solutions, with growing pressure on businesses to adopt environmentally responsible practices, thereby driving market penetration. Product substitutes, while present in traditional packaging, face increasing competition from the unique value proposition of plantable packaging, which offers end-of-life biodegradability and value-added seeding capabilities. End-user trends demonstrate a strong preference for brands aligning with environmental consciousness, directly impacting the adoption of plantable packaging across various sectors. Mergers and acquisitions (M&A) activities are anticipated to play a crucial role in market consolidation and expansion. While specific M&A deal values are in flux, the strategic importance of acquiring innovative technologies and expanding market reach suggests significant investment in this space. Current market share analysis indicates a growing, albeit distributed, market presence for key players, with a notable upward trend in the adoption of sustainable packaging solutions. The market is poised for substantial growth as consumer and regulatory pressures continue to align.

Plantable Packaging Industry Trends & Insights

The plantable packaging industry is experiencing remarkable growth, driven by a confluence of environmental consciousness, technological advancements, and evolving consumer preferences. The market penetration of plantable packaging is accelerating as businesses across various sectors recognize its unique value proposition of biodegradability and potential to bloom. This growth is underpinned by a strong CAGR, indicative of robust expansion over the forecast period. Key market growth drivers include increasing consumer demand for sustainable products, heightened awareness of plastic pollution, and supportive government regulations aimed at reducing waste. Technological disruptions are at the forefront, with ongoing research and development in advanced biodegradable materials, seed infusion techniques, and customizable seed compositions for diverse applications. These innovations are enhancing the functional properties and aesthetic appeal of plantable packaging, making it a more viable and attractive alternative to conventional options.

Consumer preferences are a significant catalyst, with a growing segment of the population actively seeking brands that demonstrate environmental responsibility. The "plantable" aspect resonates deeply, offering a tangible and positive end-of-life solution for packaging waste. This trend extends across multiple demographics, fostering a broader market acceptance. Competitive dynamics are intensifying as new players enter the market and existing ones innovate to capture market share. Companies are differentiating themselves through unique seed varieties, material compositions, and custom design services. The rise of e-commerce has also created new opportunities for plantable packaging, particularly for direct-to-consumer brands looking to enhance their sustainable image. Furthermore, the growing adoption of circular economy principles is pushing the industry towards innovative solutions that minimize waste and maximize resource utilization. The industry's ability to adapt to these evolving trends, coupled with continuous product innovation, will be crucial for sustained growth and market leadership in the coming years. The estimated market size is projected to reach several billion dollars by the end of the forecast period, highlighting the immense growth potential.

Dominant Markets & Segments in Plantable Packaging

The Retail application segment is poised to dominate the plantable packaging market due to its extensive reach and direct consumer interaction. Within retail, the Flexible Packaging type is anticipated to hold a substantial market share. This dominance is driven by several key factors:

- Consumer Demand for Sustainable Products: Consumers are increasingly making purchasing decisions based on a brand's environmental impact. Retail products packaged in plantable materials offer a clear and tangible demonstration of a brand's commitment to sustainability, directly influencing purchasing behavior.

- Brand Differentiation and Marketing: Plantable packaging provides a unique marketing advantage for retail brands, allowing them to create memorable unboxing experiences and foster customer loyalty through the novelty of planting the packaging.

- Evolving Regulatory Landscape: Governments worldwide are implementing stricter regulations on single-use plastics and promoting eco-friendly alternatives, which directly benefits the adoption of plantable packaging in the retail sector. For instance, initiatives promoting extended producer responsibility and waste reduction are creating a favorable environment.

- Versatility of Flexible Packaging: Flexible plantable packaging solutions, such as pouches, bags, and wraps, offer a cost-effective and adaptable option for a wide range of retail goods, from apparel and cosmetics to small electronics and artisanal products. The ability to customize designs and sizes further enhances its appeal.

- Economic Policies Supporting Green Initiatives: Government subsidies, tax incentives, and public procurement policies that favor sustainable products are indirectly boosting the demand for plantable packaging in the retail sector.

- Infrastructure Development for Biodegradable Materials: Investments in research and development and manufacturing infrastructure for biodegradable materials are making plantable packaging more accessible and cost-competitive, further solidifying its position in the retail market.

The Food application segment is also a significant contributor, particularly for packaging items where minimal contamination is paramount and shelf-life considerations are met. In this segment, both Flexible Packaging and Rigid Packaging will find their niches, with flexible options dominating for smaller, single-serve items and rigid packaging for more delicate or bulkier food products. The Pharmaceutical segment is expected to see a steady, albeit slower, growth due to stringent regulatory requirements and a higher emphasis on material inertness and sterility, where Rigid Packaging may see initial adoption for certain niche applications. The Industrial and Others segments, including items like greeting cards, stationery, and promotional materials, represent emerging growth areas where the novelty and eco-friendly nature of plantable packaging are highly valued. The overall trend points towards a significant market penetration in retail, followed closely by food, with other sectors demonstrating promising future growth potential as awareness and technological capabilities advance.

Plantable Packaging Product Innovations

Plantable packaging innovations are revolutionizing the sustainable materials sector. Companies are developing advanced biodegradable papers infused with a variety of seeds, ranging from wildflowers and herbs to vegetables. These innovations focus on enhancing seed viability, improving printability, and ensuring the structural integrity of the packaging. Applications are expanding beyond simple product containment to include interactive marketing tools, educational kits, and promotional merchandise that leave a lasting, positive environmental impact. The competitive advantage lies in the unique "grow-your-own" proposition, offering consumers an engaging and eco-conscious end-of-life solution for packaging waste. Technological trends include the integration of plantable materials into complex packaging structures and the development of specialized seed coatings for optimal germination in diverse environments.

Report Segmentation & Scope

The Plantable Packaging Market has been segmented across key Applications and Types to provide a granular understanding of market dynamics.

Application Segments:

- Retail: This segment is projected to experience robust growth, driven by increasing consumer preference for sustainable goods and brand differentiation. Market size estimations indicate significant adoption for apparel, cosmetics, and lifestyle products.

- Food: Expected to witness substantial expansion, especially for products where eco-friendly packaging enhances brand appeal and appeals to health-conscious consumers. Growth projections are positive, with a focus on biodegradable and compostable food packaging solutions.

- Pharmaceutical: This segment, while more niche, shows promising growth driven by the increasing demand for sustainable packaging in healthcare products and medical supplies, particularly for non-critical items.

- Industrial: This segment is anticipated to grow steadily as industries seek to reduce their environmental footprint and explore innovative packaging alternatives.

- Others: Encompasses a diverse range of applications including stationery, greeting cards, promotional materials, and event supplies, where the novelty and eco-friendly nature of plantable packaging are highly valued.

Type Segments:

- Flexible Packaging: This type is projected to dominate the market due to its versatility, cost-effectiveness, and suitability for a wide range of products, especially in the retail and food sectors.

- Rigid Packaging: While a smaller segment currently, it is expected to grow, particularly for premium products, delicate items, and applications requiring enhanced structural protection where plantable materials can be integrated.

Key Drivers of Plantable Packaging Growth

The growth of the plantable packaging sector is propelled by several interconnected drivers. Increasing consumer demand for sustainable products is a primary impetus, as environmentally conscious buyers actively seek out brands committed to reducing their ecological impact. This is amplified by growing awareness of plastic pollution and its detrimental effects on ecosystems, creating a strong market push for biodegradable alternatives. Supportive government regulations and initiatives promoting waste reduction and the use of eco-friendly materials also play a crucial role, creating a favorable policy environment. Furthermore, technological advancements in biodegradable materials and seed embedding techniques are making plantable packaging more cost-effective, versatile, and aesthetically appealing, thereby enhancing its market viability. The inherent unique value proposition of plantable packaging, offering a tangible end-of-life benefit, further strengthens its appeal.

Challenges in the Plantable Packaging Sector

Despite its promising growth, the plantable packaging sector faces several challenges. Higher production costs compared to conventional packaging can be a significant barrier, particularly for smaller businesses. Ensuring seed viability and germination rates across different storage conditions and climates requires meticulous material science and quality control. Limited awareness and understanding among some consumer segments and industries can hinder rapid adoption. Regulatory hurdles and the need for standardized certifications for biodegradability and compostability can create complexity. Supply chain complexities and scalability issues for specialized biodegradable materials can also impact availability and pricing. Finally, competition from other sustainable packaging solutions necessitates continuous innovation and value proposition refinement.

Leading Players in the Plantable Packaging Market

- Pangea Organics

- Botanical PaperWorks

- Earthly Goods

- Tiny Box Company

- 21Fools

- Little Green Paper Shop

- Green Field Paper

- UK Seed Paper

- GreenField Paper Company

- Eco Marketing Solutions

- The Mend

- Searo

- FlexSea

- Evoware

- Sway Innovation Co.

- Dong Guan on the Way Packaging Products Co.,Ltd.

Key Developments in Plantable Packaging Sector

- 2023: Launch of new seed-infused paper formulations with enhanced moisture resistance for food packaging applications.

- 2023: Increased partnerships between packaging manufacturers and seed suppliers to optimize germination rates and seed diversity.

- 2023: Growing adoption of plantable packaging for promotional merchandise and corporate gifting, emphasizing sustainability initiatives.

- 2024: Development of specialized plantable packaging for e-commerce shipping, offering both protection and an eco-friendly unboxing experience.

- 2024: Increased investment in research for plantable packaging that can decompose and enrich soil with specific nutrients.

- 2024: Stringent new regulations introduced in several regions promoting circular economy principles, boosting the demand for plantable and biodegradable packaging solutions.

Strategic Plantable Packaging Market Outlook

The strategic outlook for the plantable packaging market is exceptionally positive, driven by a sustained and growing demand for sustainable solutions. Growth accelerators include continued innovation in material science, leading to more versatile and cost-effective plantable packaging options. The expanding awareness among consumers and businesses about the environmental benefits of such packaging will further fuel adoption. Strategic opportunities lie in targeting key application segments like retail and food, where the impact and visibility of sustainable packaging are highest. Furthermore, forging strategic partnerships with brands seeking to enhance their eco-friendly credentials and investing in R&D to address current challenges like cost and scalability will be crucial for market leadership. The market is well-positioned for significant expansion, offering substantial potential for companies committed to innovation and sustainability.

Plantable Packaging Segmentation

-

1. Application

- 1.1. Retail

- 1.2. Food

- 1.3. Pharmaceutical

- 1.4. Industrial

- 1.5. Others

-

2. Types

- 2.1. Flexible Packaging

- 2.2. Rigid Packaging

Plantable Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Plantable Packaging Regional Market Share

Geographic Coverage of Plantable Packaging

Plantable Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Retail

- 5.1.2. Food

- 5.1.3. Pharmaceutical

- 5.1.4. Industrial

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Flexible Packaging

- 5.2.2. Rigid Packaging

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Plantable Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Retail

- 6.1.2. Food

- 6.1.3. Pharmaceutical

- 6.1.4. Industrial

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Flexible Packaging

- 6.2.2. Rigid Packaging

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Plantable Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Retail

- 7.1.2. Food

- 7.1.3. Pharmaceutical

- 7.1.4. Industrial

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Flexible Packaging

- 7.2.2. Rigid Packaging

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Plantable Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Retail

- 8.1.2. Food

- 8.1.3. Pharmaceutical

- 8.1.4. Industrial

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Flexible Packaging

- 8.2.2. Rigid Packaging

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Plantable Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Retail

- 9.1.2. Food

- 9.1.3. Pharmaceutical

- 9.1.4. Industrial

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Flexible Packaging

- 9.2.2. Rigid Packaging

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Plantable Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Retail

- 10.1.2. Food

- 10.1.3. Pharmaceutical

- 10.1.4. Industrial

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Flexible Packaging

- 10.2.2. Rigid Packaging

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Plantable Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Retail

- 11.1.2. Food

- 11.1.3. Pharmaceutical

- 11.1.4. Industrial

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Flexible Packaging

- 11.2.2. Rigid Packaging

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pangea Organics

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Botanical PaperWorks

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Earthly Goods

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Tiny Box Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 21Fools

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Little Green Paper Shop

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Green Field Paper

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 UK Seed Paper

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 GreenField Paper Company

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Eco Marketing Solutions

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 The Mend

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Searo

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 FlexSea

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Evoware

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Sway Innovation Co.

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Dong Guan on the Way Packaging Products Co.

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Ltd.

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Pangea Organics

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Plantable Packaging Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Plantable Packaging Revenue (million), by Application 2025 & 2033

- Figure 3: North America Plantable Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Plantable Packaging Revenue (million), by Types 2025 & 2033

- Figure 5: North America Plantable Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Plantable Packaging Revenue (million), by Country 2025 & 2033

- Figure 7: North America Plantable Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Plantable Packaging Revenue (million), by Application 2025 & 2033

- Figure 9: South America Plantable Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Plantable Packaging Revenue (million), by Types 2025 & 2033

- Figure 11: South America Plantable Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Plantable Packaging Revenue (million), by Country 2025 & 2033

- Figure 13: South America Plantable Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Plantable Packaging Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Plantable Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Plantable Packaging Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Plantable Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Plantable Packaging Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Plantable Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Plantable Packaging Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Plantable Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Plantable Packaging Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Plantable Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Plantable Packaging Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Plantable Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Plantable Packaging Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Plantable Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Plantable Packaging Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Plantable Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Plantable Packaging Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Plantable Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Plantable Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Plantable Packaging Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Plantable Packaging Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Plantable Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Plantable Packaging Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Plantable Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Plantable Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Plantable Packaging Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Plantable Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Plantable Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Plantable Packaging Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Plantable Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Plantable Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Plantable Packaging Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Plantable Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Plantable Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Plantable Packaging Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Plantable Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Plantable Packaging Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plantable Packaging?

The projected CAGR is approximately 12%.

2. Which companies are prominent players in the Plantable Packaging?

Key companies in the market include Pangea Organics, Botanical PaperWorks, Earthly Goods, Tiny Box Company, 21Fools, Little Green Paper Shop, Green Field Paper, UK Seed Paper, GreenField Paper Company, Eco Marketing Solutions, The Mend, Searo, FlexSea, Evoware, Sway Innovation Co., Dong Guan on the Way Packaging Products Co., Ltd..

3. What are the main segments of the Plantable Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 147 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Plantable Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Plantable Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Plantable Packaging?

To stay informed about further developments, trends, and reports in the Plantable Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence