Key Insights

The global PE Coated Paper Packaging market is poised for substantial expansion, driven by the escalating demand for sustainable and adaptable packaging across diverse sectors. With an estimated market size of $12.89 billion in the base year of 2025, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.72% by 2033. This growth is primarily attributed to the superior barrier properties of PE-coated paper, including exceptional moisture and grease resistance, heat-sealability, and printability. The vibrant food and beverage industry, requiring safe, hygienic, and aesthetically pleasing packaging, is a key market driver. Additionally, increasing consumer preference for convenient, single-serving, and ready-to-eat meals fuels demand for PE-coated paper in applications such as cups, lids, and flexible packaging. The burgeoning e-commerce sector also contributes significantly, leveraging PE-coated paper for its lightweight yet protective shipping solutions.

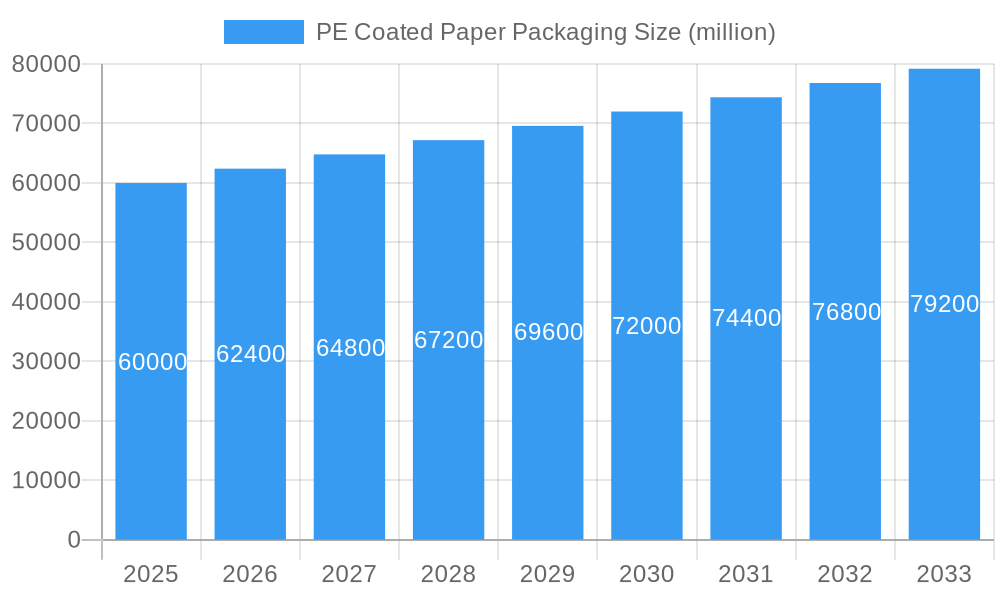

PE Coated Paper Packaging Market Size (In Billion)

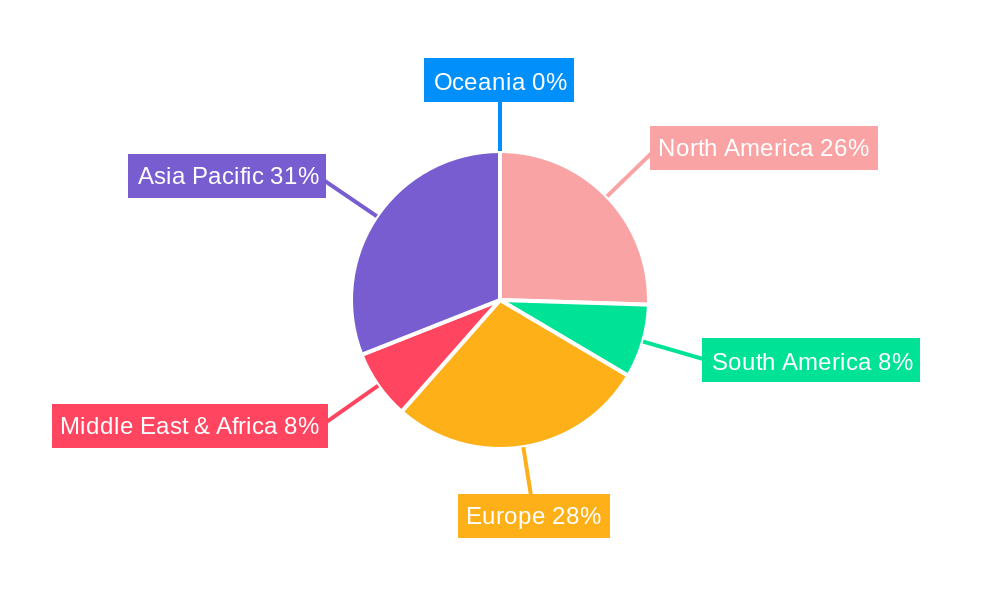

Evolving consumer preferences and regulatory frameworks favoring eco-friendly alternatives are further shaping market dynamics. As traditional plastics face increased scrutiny, PE-coated paper presents a viable option, balancing performance with recyclability when disposed of responsibly. This trend is spurring innovation in biodegradable and compostable PE coatings, thereby broadening the market's scope. Key challenges include volatility in raw material prices, such as paper pulp and polyethylene, and the imperative for robust recycling infrastructure to maximize the sustainability benefits of these products. Geographically, the Asia Pacific region, led by China and India, is set to dominate due to rapid industrialization and a large consumer base. North America and Europe remain significant markets, characterized by mature packaging industries and a strong commitment to sustainable practices. The competitive environment features established players such as Mondi, Sappi, and WestRock, who are actively investing in research and development for advanced coating technologies and portfolio expansion.

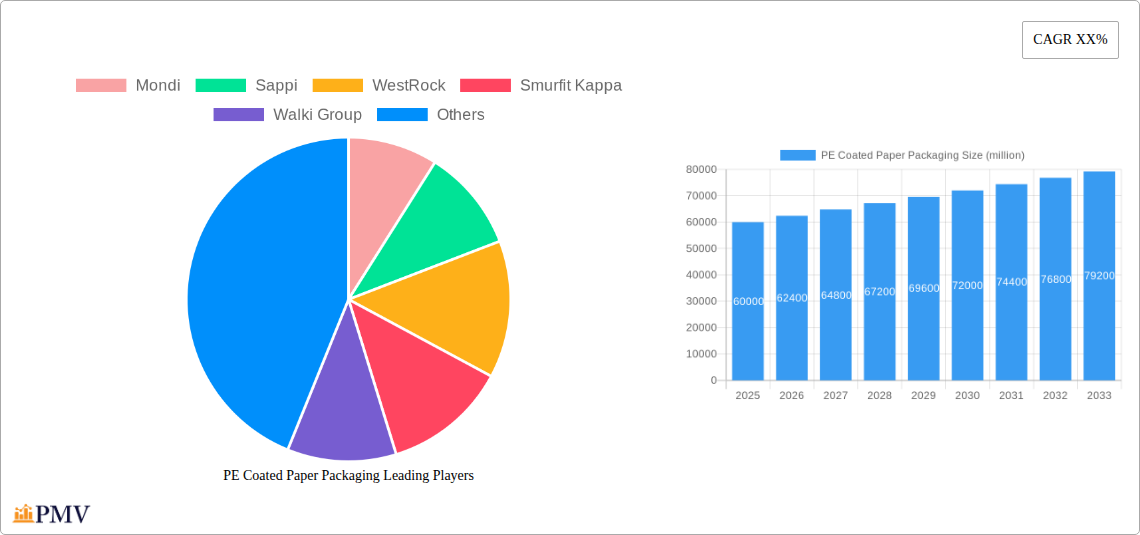

PE Coated Paper Packaging Company Market Share

PE Coated Paper Packaging Market Report: Strategic Insights, Trends, and Future Outlook (2019–2033)

This comprehensive report offers an in-depth analysis of the global PE Coated Paper Packaging market, examining its intricate structure, competitive landscape, emerging trends, and future growth trajectory. Spanning the historical period from 2019 to 2024, with a base year of 2025 and a detailed forecast extending to 2033, this study provides actionable intelligence for stakeholders navigating this dynamic industry. We delve into market segmentation by application and type, identify dominant regions and segments, and highlight key players and their strategic initiatives. The report is designed to empower businesses with the insights needed to capitalize on opportunities and mitigate challenges in the evolving PE coated paper packaging sector. The estimated market size for PE Coated Paper Packaging in 2025 is expected to reach XXX million USD, with a projected CAGR of xx% during the forecast period.

PE Coated Paper Packaging Market Structure & Competitive Dynamics

The PE Coated Paper Packaging market exhibits a moderately concentrated structure, with a few key players holding significant market share. Key companies like Mondi, Sappi, WestRock, Smurfit Kappa, and Stora Enso are prominent contributors, investing heavily in research and development and strategic acquisitions. Innovation ecosystems are flourishing, driven by the demand for sustainable and functional packaging solutions. Regulatory frameworks, particularly those concerning recyclability and single-use plastics, are shaping product development and market entry strategies. Product substitutes, such as entirely plastic-based packaging or alternative paper coatings, present ongoing competitive pressures, requiring continuous innovation in barrier properties and sustainability claims. End-user trends are shifting towards eco-friendly alternatives and enhanced product protection, influencing packaging design and material selection. Mergers and acquisitions (M&A) activity, with deal values estimated in the hundreds of millions, are crucial for consolidating market presence and expanding product portfolios. For instance, the M&A landscape has seen transactions ranging from xx million USD to xx million USD in the last five years. The competitive intensity is further amplified by the presence of specialized players like Billerud, Burgo Group, Cotek Paper, Laufenberg, Behr Bircher Cellpack, Cartonal, and Kebel Premium, each contributing unique expertise and market focus.

PE Coated Paper Packaging Industry Trends & Insights

The PE Coated Paper Packaging market is experiencing robust growth, propelled by a confluence of factors. A primary market growth driver is the increasing global demand for convenient and sustainable food and beverage packaging. Consumers are actively seeking alternatives to traditional plastics, and PE coated paper offers a compelling balance of functionality and environmental consideration. Technological disruptions are central to this evolution, with advancements in coating technologies enabling enhanced barrier properties against moisture, grease, and oxygen, thereby extending product shelf life and reducing food waste. This is particularly relevant for applications like flexible packaging and food trays. Consumer preferences are a significant influencer, with a growing emphasis on visually appealing, safe, and environmentally responsible packaging. Brands are increasingly adopting PE coated paper to align with their sustainability commitments and appeal to eco-conscious consumers. The competitive dynamics within the industry are characterized by a race towards innovation, with companies investing in biodegradable and compostable PE alternatives to address end-of-life concerns. Market penetration of PE coated paper packaging is steadily increasing across various segments, driven by its versatility and cost-effectiveness compared to some premium sustainable materials. The total market size is projected to grow at a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching an estimated value of XXX million USD by the end of the forecast period. Industry developments such as the introduction of novel bio-based PE coatings and enhanced recyclability infrastructure are further bolstering market expansion. For example, investments in R&D for PE coated paper have seen a xx% increase year-on-year, with a focus on improving recyclability and compostability.

Dominant Markets & Segments in PE Coated Paper Packaging

The Flexible Packaging segment is currently the dominant market within PE Coated Paper Packaging, driven by its widespread application in food, beverages, and consumer goods. The inherent properties of PE coated paper, such as its printability, barrier capabilities, and formability, make it an ideal choice for a vast array of flexible packaging solutions, including pouches, sachets, and wrappers. The growth of the e-commerce sector further fuels demand for flexible packaging solutions that offer protection during transit and attractive branding opportunities. Key drivers for this dominance include the segment's adaptability to evolving consumer needs for on-the-go consumption and its cost-effectiveness for high-volume production.

- Key Drivers for Flexible Packaging Dominance:

- Consumer Convenience: Increasing demand for single-serving and ready-to-eat food products.

- E-commerce Growth: Need for lightweight, durable, and brandable packaging for online retail.

- Cost-Effectiveness: Ability to deliver high-quality packaging at competitive price points for mass-market products.

- Printability: Excellent surface for branding, product information, and promotional messaging.

In terms of PE Coated Paper Packaging types, Polyethylene remains the dominant coating. Its excellent moisture barrier properties, grease resistance, and cost-effectiveness make it the go-to choice for a wide range of applications. However, there is a significant upward trend and increasing demand for Biodegradable Polymers as coatings. This shift is largely driven by environmental regulations and growing consumer pressure for sustainable packaging solutions. Regions like Europe and North America are at the forefront of this adoption, owing to stringent waste management policies and heightened consumer awareness. The Trays segment is also experiencing considerable growth, particularly in the fresh food and ready-to-eat meal sectors, where PE coated paper trays offer a sustainable alternative to plastic trays. The Boxes and Cartons segment, while mature, continues to be a significant contributor, benefiting from the demand for sustainable secondary and tertiary packaging solutions.

PE Coated Paper Packaging Product Innovations

Product innovations in PE Coated Paper Packaging are primarily focused on enhancing sustainability and functionality. Developments include the introduction of advanced barrier coatings that offer superior protection against moisture, oxygen, and grease, thereby extending product shelf life. Furthermore, there is a strong emphasis on developing biodegradable and compostable PE coatings derived from renewable resources, catering to the growing demand for eco-friendly packaging solutions. These innovations aim to offer competitive advantages by meeting stringent environmental regulations and aligning with evolving consumer preferences for greener packaging. The integration of smart packaging features, such as temperature indicators, is also an emerging trend.

Report Segmentation & Scope

This report segments the PE Coated Paper Packaging market across two primary dimensions: Application and Type.

Application Segments:

- Flexible Packaging: This segment is anticipated to witness substantial growth, driven by its widespread use in food and beverage packaging, along with the expanding e-commerce sector.

- Cups and Lids: Expected to show steady growth, particularly in the disposable beverage market, with increasing demand for sustainable alternatives.

- Trays: Projected to experience robust expansion, fueled by the rise of the ready-to-eat meal and fresh food delivery industries.

- Boxes and Cartons: A mature segment, but still significant, driven by the demand for sustainable secondary and tertiary packaging across various industries.

- Clamshells: Growth is tied to the convenience food and fast-casual dining sectors.

- Other: Encompasses miscellaneous applications such as paper bags and specialty packaging.

Type Segments:

- Polyethylene: Remains the dominant type, offering excellent barrier properties and cost-effectiveness.

- Biodegradable Polymers: Experiencing rapid growth due to increasing environmental concerns and regulatory mandates.

- Wax: Utilized for specific applications requiring enhanced moisture resistance, particularly in food packaging.

- Other: Includes emerging coating technologies and specialized materials.

The estimated market size for the Flexible Packaging segment is projected to be XXX million USD in 2025, with a CAGR of xx% through 2033. The Biodegradable Polymers segment is expected to grow at an accelerated pace, driven by innovation and regulatory support.

Key Drivers of PE Coated Paper Packaging Growth

The PE Coated Paper Packaging market is propelled by several key drivers. Growing environmental consciousness and stringent regulations mandating the reduction of single-use plastics are pushing industries towards sustainable alternatives. The increasing demand for convenient and portable food and beverage packaging fuels the adoption of PE coated paper for applications like cups, trays, and flexible pouches. Technological advancements in coating formulations are enhancing barrier properties, improving product shelf life, and enabling greater design flexibility. Furthermore, the cost-effectiveness and recyclability of PE coated paper compared to some premium sustainable materials make it an attractive option for manufacturers across diverse sectors. The expansion of the e-commerce sector also contributes significantly, driving demand for lightweight yet protective packaging solutions.

Challenges in the PE Coated Paper Packaging Sector

Despite its growth, the PE Coated Paper Packaging sector faces several challenges. Regulatory complexities and evolving recycling infrastructures can create hurdles for widespread adoption and end-of-life management. Fluctuations in raw material prices, particularly for paper pulp and polyethylene, can impact production costs and profitability. Competition from alternative packaging materials, including other bio-based options and advanced plastic films, remains a significant factor. Ensuring consistent barrier performance across all applications and environmental conditions can also be challenging. Lastly, consumer perception and education regarding the recyclability and environmental impact of PE coated paper products require continuous effort.

Leading Players in the PE Coated Paper Packaging Market

- Mondi

- Sappi

- WestRock

- Smurfit Kappa

- Walki Group

- Stora Enso

- Billerud

- Burgo Group

- Cotek Paper

- Laufenberg

- Behr Bircher Cellpack

- Cartonal

- Kebel Premium

Key Developments in PE Coated Paper Packaging Sector

- 2023, Q4: Mondi launches a new range of high-barrier recyclable PE coated paper for food packaging, enhancing shelf-life and sustainability.

- 2024, Q1: Sappi invests in advanced coating technology to improve the compostability of its PE coated paper products.

- 2024, Q2: WestRock acquires a specialized paperboard producer, strengthening its capacity for coated paper solutions.

- 2024, Q3: Smurfit Kappa announces a strategic partnership to develop innovative PE coated paper packaging for the pharmaceutical industry.

- 2024, Q4: Walki Group expands its biodegradable PE coating capabilities to cater to the growing demand for sustainable flexible packaging.

- 2025, Q1: Stora Enso introduces a new generation of PE coated paper with improved recyclability and reduced material usage.

- 2025, Q2: Billerud announces plans for significant capacity expansion in PE coated paper production to meet rising market demand.

- 2025, Q3: Burgo Group innovates in PE coating for food trays, focusing on improved grease and moisture resistance.

Strategic PE Coated Paper Packaging Market Outlook

The strategic outlook for the PE Coated Paper Packaging market is highly positive, driven by a robust confluence of environmental mandates, consumer preferences for sustainable solutions, and continuous technological innovation. Growth accelerators include the increasing demand for flexible packaging in emerging economies, the development of advanced biodegradable and compostable PE coatings, and the expansion of recycling infrastructure. Companies that focus on offering tailored solutions with superior barrier properties, enhanced recyclability, and compelling sustainability narratives will be well-positioned to capture significant market share. Strategic opportunities lie in expanding into new application areas, forging partnerships for supply chain optimization, and investing in research and development to stay ahead of evolving regulatory landscapes and consumer expectations. The market is poised for sustained growth, offering significant potential for stakeholders who can adapt to its dynamic nature.

PE Coated Paper Packaging Segmentation

-

1. Application

- 1.1. Flexible Packaging

- 1.2. Cups and Lids

- 1.3. Trays

- 1.4. Boxes and Cartons

- 1.5. Clamshells

- 1.6. Other

-

2. Types

- 2.1. Polyethylene

- 2.2. Biodegradable Polymers

- 2.3. Wax

- 2.4. Other

PE Coated Paper Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

PE Coated Paper Packaging Regional Market Share

Geographic Coverage of PE Coated Paper Packaging

PE Coated Paper Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.72% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global PE Coated Paper Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Flexible Packaging

- 5.1.2. Cups and Lids

- 5.1.3. Trays

- 5.1.4. Boxes and Cartons

- 5.1.5. Clamshells

- 5.1.6. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Polyethylene

- 5.2.2. Biodegradable Polymers

- 5.2.3. Wax

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America PE Coated Paper Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Flexible Packaging

- 6.1.2. Cups and Lids

- 6.1.3. Trays

- 6.1.4. Boxes and Cartons

- 6.1.5. Clamshells

- 6.1.6. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Polyethylene

- 6.2.2. Biodegradable Polymers

- 6.2.3. Wax

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America PE Coated Paper Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Flexible Packaging

- 7.1.2. Cups and Lids

- 7.1.3. Trays

- 7.1.4. Boxes and Cartons

- 7.1.5. Clamshells

- 7.1.6. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Polyethylene

- 7.2.2. Biodegradable Polymers

- 7.2.3. Wax

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe PE Coated Paper Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Flexible Packaging

- 8.1.2. Cups and Lids

- 8.1.3. Trays

- 8.1.4. Boxes and Cartons

- 8.1.5. Clamshells

- 8.1.6. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Polyethylene

- 8.2.2. Biodegradable Polymers

- 8.2.3. Wax

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa PE Coated Paper Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Flexible Packaging

- 9.1.2. Cups and Lids

- 9.1.3. Trays

- 9.1.4. Boxes and Cartons

- 9.1.5. Clamshells

- 9.1.6. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Polyethylene

- 9.2.2. Biodegradable Polymers

- 9.2.3. Wax

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific PE Coated Paper Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Flexible Packaging

- 10.1.2. Cups and Lids

- 10.1.3. Trays

- 10.1.4. Boxes and Cartons

- 10.1.5. Clamshells

- 10.1.6. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Polyethylene

- 10.2.2. Biodegradable Polymers

- 10.2.3. Wax

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Mondi

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sappi

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 WestRock

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Smurfit Kappa

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Walki Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Stora Enso

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Billerud

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Burgo Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Cotek Paper

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Laufenberg

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Behr Bircher Cellpack

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Cartonal

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Kebel Premium

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Mondi

List of Figures

- Figure 1: Global PE Coated Paper Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America PE Coated Paper Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America PE Coated Paper Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America PE Coated Paper Packaging Revenue (billion), by Types 2025 & 2033

- Figure 5: North America PE Coated Paper Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America PE Coated Paper Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America PE Coated Paper Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America PE Coated Paper Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America PE Coated Paper Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America PE Coated Paper Packaging Revenue (billion), by Types 2025 & 2033

- Figure 11: South America PE Coated Paper Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America PE Coated Paper Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America PE Coated Paper Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe PE Coated Paper Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe PE Coated Paper Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe PE Coated Paper Packaging Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe PE Coated Paper Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe PE Coated Paper Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe PE Coated Paper Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa PE Coated Paper Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa PE Coated Paper Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa PE Coated Paper Packaging Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa PE Coated Paper Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa PE Coated Paper Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa PE Coated Paper Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific PE Coated Paper Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific PE Coated Paper Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific PE Coated Paper Packaging Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific PE Coated Paper Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific PE Coated Paper Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific PE Coated Paper Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global PE Coated Paper Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global PE Coated Paper Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global PE Coated Paper Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global PE Coated Paper Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global PE Coated Paper Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global PE Coated Paper Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global PE Coated Paper Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global PE Coated Paper Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global PE Coated Paper Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global PE Coated Paper Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global PE Coated Paper Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global PE Coated Paper Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global PE Coated Paper Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global PE Coated Paper Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global PE Coated Paper Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global PE Coated Paper Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global PE Coated Paper Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global PE Coated Paper Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific PE Coated Paper Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the PE Coated Paper Packaging?

The projected CAGR is approximately 9.72%.

2. Which companies are prominent players in the PE Coated Paper Packaging?

Key companies in the market include Mondi, Sappi, WestRock, Smurfit Kappa, Walki Group, Stora Enso, Billerud, Burgo Group, Cotek Paper, Laufenberg, Behr Bircher Cellpack, Cartonal, Kebel Premium.

3. What are the main segments of the PE Coated Paper Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.89 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "PE Coated Paper Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the PE Coated Paper Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the PE Coated Paper Packaging?

To stay informed about further developments, trends, and reports in the PE Coated Paper Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence