Key Insights

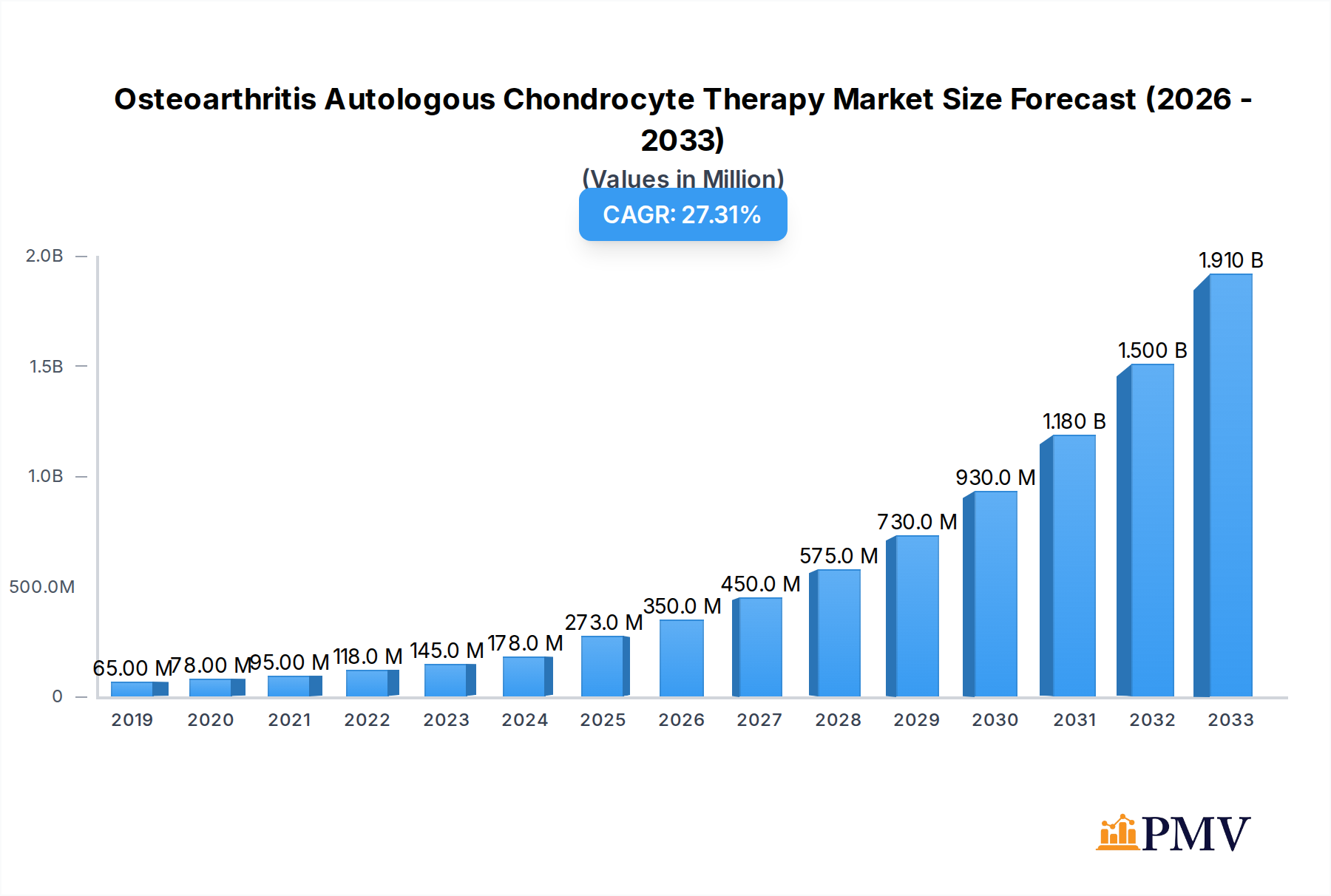

The Osteoarthritis Autologous Chondrocyte Therapy market is poised for remarkable expansion, projected to reach a substantial USD 273 million by 2025, fueled by an impressive Compound Annual Growth Rate (CAGR) of 30.8% through 2033. This dynamic growth is primarily driven by the increasing prevalence of osteoarthritis globally, a degenerative joint condition affecting millions. Advances in regenerative medicine and cell therapy technologies have led to the development of more effective and minimally invasive treatment options, such as second and third-generation autologous chondrocyte implantation (ACI) techniques. These newer generations offer enhanced cell viability and improved integration with the damaged cartilage, leading to better patient outcomes and a higher adoption rate. The growing awareness among both patients and healthcare providers regarding the benefits of ACI, including reduced pain, improved joint function, and the potential for cartilage regeneration, further propels market growth.

Osteoarthritis Autologous Chondrocyte Therapy Market Size (In Million)

Key trends shaping this market include a significant shift towards personalized medicine, where patient-specific cells are used for treatment, leading to higher efficacy and fewer side effects. The market is also witnessing a rise in clinical trials and research initiatives aimed at expanding the application of ACI to other joint conditions and optimizing current procedures. Despite the promising outlook, certain restraints may temper immediate growth, such as the high cost associated with ACI procedures and the limited availability of trained professionals and specialized centers. However, ongoing technological innovations, coupled with an increasing healthcare expenditure and supportive government initiatives in certain regions, are expected to mitigate these challenges. The market segmentation by application, with Primary Osteoarthritis dominating, and by type, showcasing the rise of advanced ACI generations, highlights the evolving landscape of cartilage repair treatments.

Osteoarthritis Autologous Chondrocyte Therapy Company Market Share

Osteoarthritis Autologous Chondrocyte Therapy Market Structure & Competitive Dynamics

The Osteoarthritis Autologous Chondrocyte Therapy market is characterized by a moderate to high level of concentration, with a few key players dominating the innovative landscape. Companies like Vericel, Japan Tissue Engineering, Orthocell, and CO.DON GmbH are at the forefront, investing heavily in research and development to advance next-generation chondrocyte-based treatments. The innovation ecosystem is fueled by ongoing clinical trials and the pursuit of regulatory approvals for improved autologous chondrocyte implantation (ACI) techniques, particularly the progression from 2nd Gen C-ACI to more advanced 3rd Gen M-ACI. Regulatory frameworks, primarily driven by agencies such as the FDA and EMA, play a critical role in shaping market entry and product lifecycle management, necessitating rigorous clinical evidence and manufacturing standards.

Product substitutes, including surgical interventions like total knee arthroplasty and less invasive procedures, pose a significant competitive challenge. However, the unique regenerative potential of autologous chondrocyte therapy offers distinct advantages for specific patient profiles and lesion types. End-user trends are shifting towards personalized medicine and biologics that can address the underlying pathology of osteoarthritis rather than merely managing symptoms. Merger and acquisition (M&A) activities, while not as extensive as in broader pharmaceutical markets, are strategically important for consolidating expertise and expanding market reach. For instance, significant M&A deals in the cell therapy space have collectively amounted to hundreds of millions of dollars, signaling a strong investor interest in this regenerative medicine segment. Understanding these dynamics is crucial for navigating the competitive terrain and identifying growth opportunities within the global Osteoarthritis Autologous Chondrocyte Therapy market.

Osteoarthritis Autologous Chondrocyte Therapy Industry Trends & Insights

The Osteoarthritis Autologous Chondrocyte Therapy market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 8.5% between 2019 and 2033. This upward trajectory is driven by a confluence of factors, including the increasing global prevalence of osteoarthritis, a condition affecting millions worldwide, and a growing demand for advanced, regenerative treatment options. The base year of 2025 marks a significant point, with the market already valued at an estimated $2.3 billion, reflecting substantial current investment and adoption. The forecast period of 2025–2033 anticipates this value to surge considerably, reaching an estimated $4.8 billion by 2033. This growth is underpinned by advancements in cell culture techniques and delivery systems, leading to more effective and targeted therapies.

Technological disruptions are central to this evolution. The transition from earlier generations of autologous chondrocyte implantation (ACI) to more refined 3rd Gen M-ACI techniques signifies a leap forward in treatment efficacy and patient outcomes. These newer generations often involve bio-scaffolds or matrix-induced delivery, enhancing chondrocyte integration and cartilage regeneration. Consumer preferences are increasingly leaning towards biologics that offer the potential for true tissue repair and pain relief, moving away from purely palliative interventions. The patient pool for osteoarthritis treatment is expanding due to an aging global population and a rise in obesity, both significant risk factors for the condition. Market penetration for autologous chondrocyte therapy, while still lower than traditional surgical options, is steadily increasing as clinical evidence strengthens and reimbursement policies become more favorable.

Furthermore, the industry is witnessing a growing understanding of the different types of osteoarthritis, differentiating between primary osteoarthritis, which arises from aging and wear-and-tear, and secondary osteoarthritis, often resulting from trauma or underlying medical conditions. This nuanced understanding allows for more tailored therapeutic approaches, boosting the effectiveness of autologous chondrocyte therapies for specific patient cohorts. The competitive landscape is dynamic, with established players and emerging biotech firms vying for market share through product innovation, strategic partnerships, and intellectual property development. The collective market capitalization of key companies in the autologous chondrocyte therapy sector is in the billions, indicating substantial financial backing and market confidence. Addressing unmet medical needs in cartilage repair remains a primary focus, driving continued investment and research into this promising field of regenerative medicine.

Dominant Markets & Segments in Osteoarthritis Autologous Chondrocyte Therapy

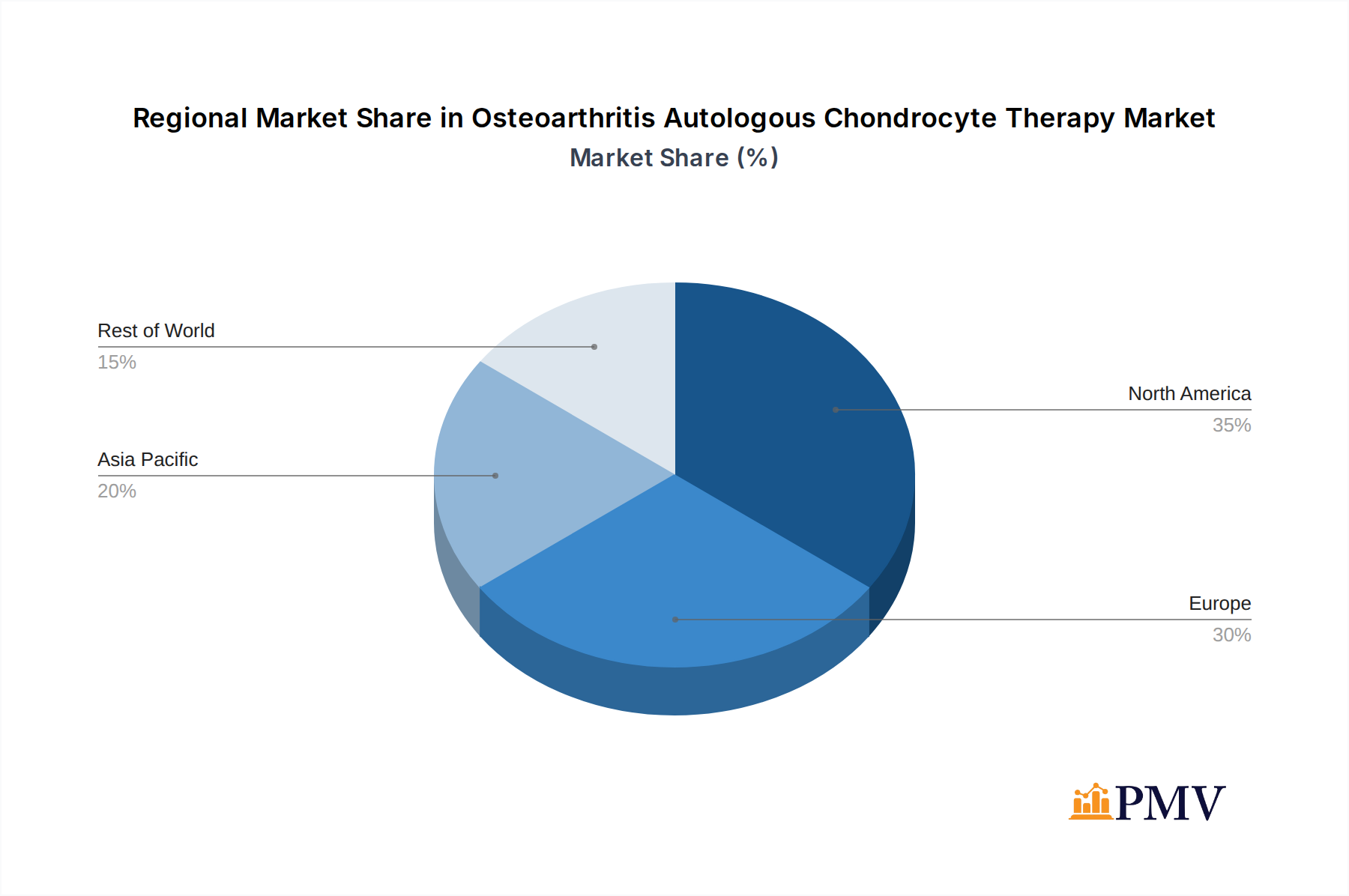

The global Osteoarthritis Autologous Chondrocyte Therapy market exhibits distinct regional and segment-specific dominance. Geographically, North America, particularly the United States, currently commands the largest market share. This dominance is attributed to factors such as high healthcare expenditure, advanced healthcare infrastructure, a large patient population suffering from osteoarthritis, and a proactive regulatory environment that supports the development and adoption of innovative medical technologies. The economic policies in these regions often incentivize research and development, leading to earlier market penetration of novel treatments like autologous chondrocyte therapy.

Within the application segment, Primary Osteoarthritis represents the largest and most rapidly growing segment. This is directly linked to the aging global population and the inherent degenerative nature of primary osteoarthritis. As individuals live longer, the incidence of wear-and-tear related cartilage damage increases significantly, creating a substantial demand for effective regenerative solutions. The economic burden of managing chronic pain and impaired mobility associated with primary osteoarthritis also drives the search for long-term restorative therapies. The market size for primary osteoarthritis treatment applications is estimated to be in the range of billions of dollars.

Regarding treatment types, 3rd Gen M-ACI is emerging as the dominant and fastest-growing segment. While 2nd Gen C-ACI laid the groundwork for ACI, the advancements in matrix-induced techniques (M-ACI) offer improved cell viability, integration, and matrix deposition, leading to superior cartilage repair outcomes. This technological superiority translates into greater clinical acceptance and a higher adoption rate among orthopedic surgeons. The market share for 3rd Gen M-ACI is projected to surpass that of 2nd Gen C-ACI within the forecast period. The market for 3rd Gen M-ACI is expected to reach hundreds of millions of dollars by 2033. These advancements are supported by robust clinical data showcasing enhanced functional recovery and reduced revision rates.

Osteoarthritis Autologous Chondrocyte Therapy Product Innovations

Product innovations in Osteoarthritis Autologous Chondrocyte Therapy are primarily focused on enhancing the efficacy and patient experience of ACI. The evolution from 2nd Gen C-ACI to 3rd Gen M-ACI represents a significant leap, integrating chondrocytes with advanced bio-scaffolds or matrices. These innovations aim to improve cell survival, proliferation, and differentiation, leading to better neocartilage formation and restoration of joint function. Companies are investing in proprietary cell expansion techniques and novel delivery systems to ensure optimal graft integration and long-term outcomes, targeting both primary and secondary osteoarthritis applications. This competitive advantage is crucial in a market seeking durable solutions for cartilage defects.

Report Segmentation & Scope

This report meticulously segments the Osteoarthritis Autologous Chondrocyte Therapy market, offering in-depth analysis across key areas. The segmentation encompasses Application, distinguishing between Primary Osteoarthritis and Secondary Osteoarthritis. Primary Osteoarthritis, driven by age-related degeneration, represents a substantial market size in the billions. Secondary Osteoarthritis, stemming from trauma or underlying medical conditions, presents a growing niche. Further segmentation by Types includes 2nd Gen C-ACI and 3rd Gen M-ACI. The 3rd Gen M-ACI segment is projected to exhibit higher growth, estimated to reach hundreds of millions in market value by 2033, due to its enhanced therapeutic profile and improving competitive dynamics. The scope includes a detailed historical analysis from 2019–2024 and a forward-looking forecast from 2025–2033, with a base year of 2025.

Key Drivers of Osteoarthritis Autologous Chondrocyte Therapy Growth

The growth of the Osteoarthritis Autologous Chondrocyte Therapy market is propelled by several key drivers. The rising global incidence of osteoarthritis, exacerbated by an aging population and increasing rates of obesity, creates a vast and expanding patient pool. Technological advancements, particularly the development of superior 3rd Gen M-ACI techniques, are enhancing treatment efficacy and patient outcomes, fostering greater adoption. Favorable reimbursement policies and increasing healthcare expenditure in developed nations also support market expansion, allowing for greater accessibility to these advanced therapies. Furthermore, a growing preference among patients and clinicians for regenerative medicine solutions that aim for true tissue repair over symptom management is a significant accelerator.

Challenges in the Osteoarthritis Autologous Chondrocyte Therapy Sector

Despite promising growth, the Osteoarthritis Autologous Chondrocyte Therapy sector faces several challenges. Regulatory hurdles remain significant, with the need for extensive and costly clinical trials to demonstrate safety and efficacy, leading to longer approval timelines. High treatment costs can limit patient access and reimbursement in certain regions, impacting market penetration. Complex manufacturing processes for autologous cell therapies present logistical challenges and can lead to supply chain disruptions, affecting consistent availability. Competitive pressures from established surgical procedures and the development of alternative regenerative therapies also necessitate continuous innovation and evidence generation to maintain market relevance.

Leading Players in the Osteoarthritis Autologous Chondrocyte Therapy Market

- Vericel

- Japan Tissue Engineering

- Orthocell

- CO.DON GmbH

Key Developments in Osteoarthritis Autologous Chondrocyte Therapy Sector

- 2023: Vericel announced positive topline results from its Phase III study for its next-generation ACI product, demonstrating significant improvements in pain and function for patients with knee cartilage defects.

- 2022: Japan Tissue Engineering secured regulatory approval for a new indication of its autologous chondrocyte implantation system, expanding its market reach.

- 2021: Orthocell advanced its leading cell therapy candidate into further clinical trials for osteoarthritis, showing promising early-stage data.

- 2020: CO.DON GmbH received expanded reimbursement coverage for its autologous chondrocyte implantation therapy in key European markets, increasing patient access.

- 2019: Advancements in bio-scaffold technology for matrix-induced ACI (M-ACI) began to show early positive impacts on clinical outcomes, signaling the shift towards 3rd Gen therapies.

Strategic Osteoarthritis Autologous Chondrocyte Therapy Market Outlook

The strategic outlook for the Osteoarthritis Autologous Chondrocyte Therapy market is highly positive, driven by unmet medical needs and continuous innovation. The transition towards 3rd Gen M-ACI therapies, offering superior regenerative capabilities, will be a key growth accelerator. Expansion into new geographical markets and securing favorable reimbursement policies in emerging economies will unlock significant potential. Strategic partnerships between leading players and research institutions can further foster innovation and accelerate the development of next-generation treatments. Addressing the current challenges related to cost and accessibility through technological advancements and value-based healthcare models will be crucial for sustained market leadership and maximizing the therapeutic impact of autologous chondrocyte therapy.

Osteoarthritis Autologous Chondrocyte Therapy Segmentation

-

1. Application

- 1.1. Primary Osteoarthritis

- 1.2. Secondary Osteoarthritis

-

2. Types

- 2.1. 2nd Gen C-ACI

- 2.2. 3rd Gen M-ACI

Osteoarthritis Autologous Chondrocyte Therapy Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Osteoarthritis Autologous Chondrocyte Therapy Regional Market Share

Geographic Coverage of Osteoarthritis Autologous Chondrocyte Therapy

Osteoarthritis Autologous Chondrocyte Therapy REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 30.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Osteoarthritis Autologous Chondrocyte Therapy Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Primary Osteoarthritis

- 5.1.2. Secondary Osteoarthritis

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 2nd Gen C-ACI

- 5.2.2. 3rd Gen M-ACI

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Osteoarthritis Autologous Chondrocyte Therapy Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Primary Osteoarthritis

- 6.1.2. Secondary Osteoarthritis

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 2nd Gen C-ACI

- 6.2.2. 3rd Gen M-ACI

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Osteoarthritis Autologous Chondrocyte Therapy Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Primary Osteoarthritis

- 7.1.2. Secondary Osteoarthritis

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 2nd Gen C-ACI

- 7.2.2. 3rd Gen M-ACI

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Osteoarthritis Autologous Chondrocyte Therapy Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Primary Osteoarthritis

- 8.1.2. Secondary Osteoarthritis

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 2nd Gen C-ACI

- 8.2.2. 3rd Gen M-ACI

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Primary Osteoarthritis

- 9.1.2. Secondary Osteoarthritis

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 2nd Gen C-ACI

- 9.2.2. 3rd Gen M-ACI

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Primary Osteoarthritis

- 10.1.2. Secondary Osteoarthritis

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 2nd Gen C-ACI

- 10.2.2. 3rd Gen M-ACI

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Vericel

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Japan Tissue Engineering

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Orthocell

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CO.DON GmbH

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.1 Vericel

List of Figures

- Figure 1: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Application 2025 & 2033

- Figure 3: North America Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Types 2025 & 2033

- Figure 5: North America Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Country 2025 & 2033

- Figure 7: North America Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Application 2025 & 2033

- Figure 9: South America Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Types 2025 & 2033

- Figure 11: South America Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Country 2025 & 2033

- Figure 13: South America Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Osteoarthritis Autologous Chondrocyte Therapy Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Osteoarthritis Autologous Chondrocyte Therapy Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Osteoarthritis Autologous Chondrocyte Therapy?

The projected CAGR is approximately 30.8%.

2. Which companies are prominent players in the Osteoarthritis Autologous Chondrocyte Therapy?

Key companies in the market include Vericel, Japan Tissue Engineering, Orthocell, CO.DON GmbH.

3. What are the main segments of the Osteoarthritis Autologous Chondrocyte Therapy?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 273 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Osteoarthritis Autologous Chondrocyte Therapy," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Osteoarthritis Autologous Chondrocyte Therapy report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Osteoarthritis Autologous Chondrocyte Therapy?

To stay informed about further developments, trends, and reports in the Osteoarthritis Autologous Chondrocyte Therapy, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence